2020 Mortgage and Interest Rates Update

Amid COVID-19, the mortgage and interest rates have dropped significantly while mortgage delinquency rate surges in some states as the unemployment rate rises. In this conversation with Daniel Gat, a senior mortgage banker, we talk about the mortgage delinquency situation in California, especially in the Bay Area and what it means for home buyers and investors, as well as some trends of the Bay Area housing market in this particular time of the pandemic. We will also share some data and advice for you to take into account while deciding whether to buy or invest during this special time period.

This is an excerpt from the 10th Bay Area Housing Townhall Webinar – Interest Rates, Guidelines, and Expectations. Watch the video version here, or check out the full recording of the webinar on our HG-TV page, or our YouTube channel.

Helen: Now I want to go into the mortgage industry update, and I know Daniel will have a lot of input on this. I put together a few charts and slides, and I’d love to know what you think of these reports.

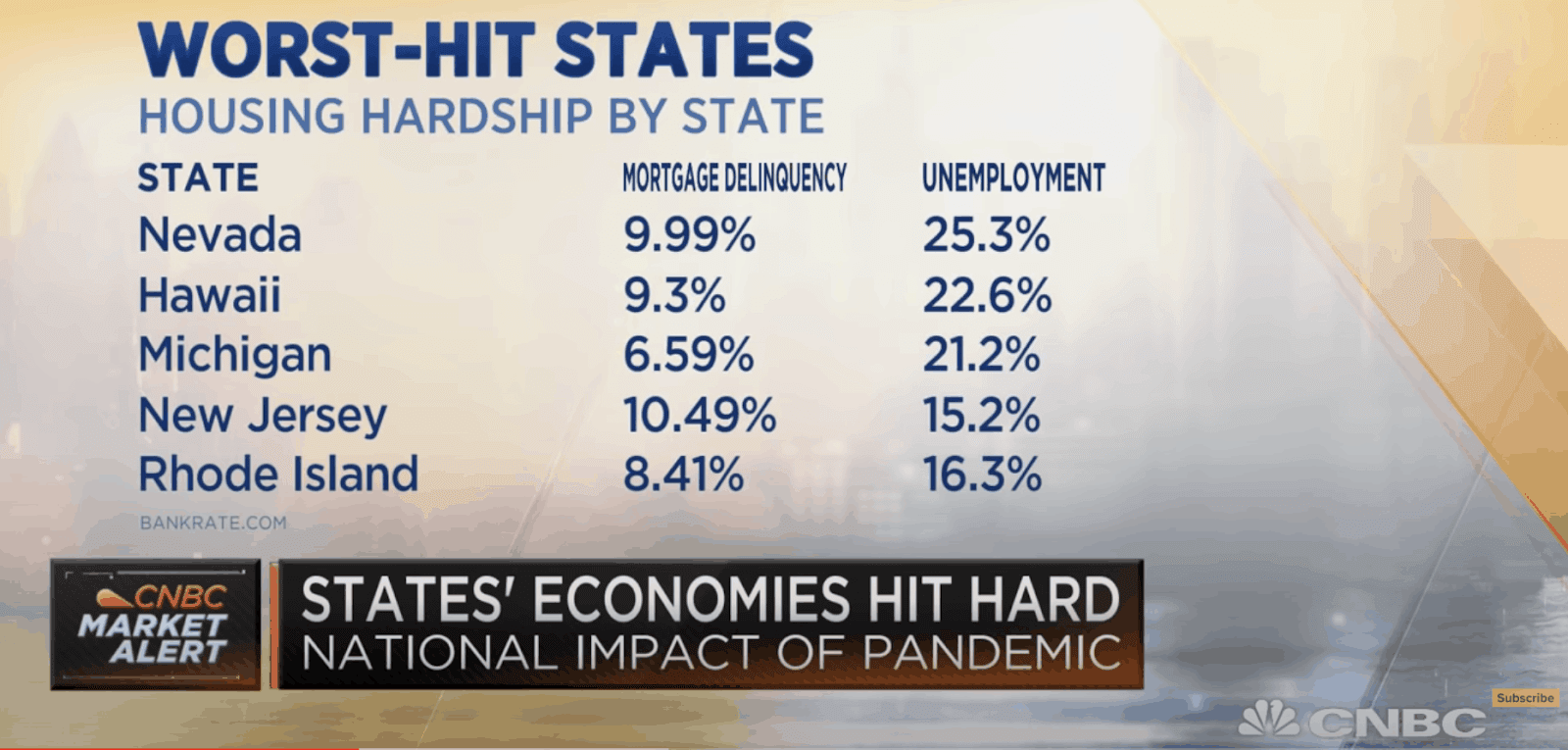

Now, I saw it on CNBC, they were talking about the mortgage delinquency. The hardest-hit states are Nevada, Hawaii, Michigan, New Jersey, and Rhode Island. In a sense, I was relieved that it’s not California. We can see in this chart that the unemployment rate in Nevada is 25.3%, Hawaii 22.6%, Michigan 21.2%, New Jersey 15.2%, and Rhode Island 16.3%. You know, the unemployment rate really tightly correlates to mortgage delinquency. I don’t know if you have any numbers on California delinquency, Daniel, do you follow that?

Daniel: I don’t have solid numbers, but I have an opinion on it if that helps. My opinion is that, not even the whole state, take the Bay Area and Los Angeles as an example, the two biggest metropolitan areas in California. I don’t think that the majority of people that are being economically affected by the pandemic, and I say the majority because there are always exceptions to the case, are not in a financial position to be homeowners in the western part of California essentially.

I have a lot of clients ask me that too. They say – well, you know, I want to wait until October or November, because everybody who’s in forbearance is all going to lose their houses, and I’m going to pick it up for a good deal. I said – well, think about that really, the majority of people that own houses in the Bay Area or in Los Angeles probably do not have jobs like retail job and restaurant work. Of course, you have Los Angeles people in the entertainment industry that are being affected that could be home buyers.

But in the East Bay and in the Bay Area in general, I find that most of the buyers are involved in work that primarily could be done from home and they’re not really economically impacted in the same way, where they may have a pay cut temporarily for 20 or 25 percent. They’re not going to lose their house in the same sense that we’re in Nevada as somebody who makes $40,000 or $50,000 a year, they could own a five-bedroom house in Nevada. I mean, I literally have a friend, he makes fifty thousand dollars a year, and he owns a five-bedroom three-bathroom house with a pool because it costs $180,000 in Las Vegas, so it’s a different market, so I don’t see that.

I think a lot of delinquencies in California if there are any, I don’t know if they’re counting forbearance as delinquencies or not, but if there are, I would feel that maybe a lot of people may have gone into forbearance just to be precautionary or to take advantage of the fact that it’s something that they could do without being potentially penalized. I don’t have the statistics but my guess would be that California would probably be a lot less, at least if you’re considering the metropolitan areas.

Helen: Actually I absolutely agree with you. I work with a lot of investors and they’re interested in investing in a lot of different areas. When they asked me – which market should I focus on? I always say that you have to look at employment in that area. I know a lot of people love Nevada. My only thing about Nevada is that it’s so highly relying on one single industry, casino. Actually tourism as well, so if that goes, then pretty much the whole market is gonna go down. There are a lot of different factors, but really the most important factor to look at is the employment in that area.

In terms of what you were saying about forbearance, as a matter of fact, I have some other slides I want to show. Not necessarily about California but definitely something about the forbearance.

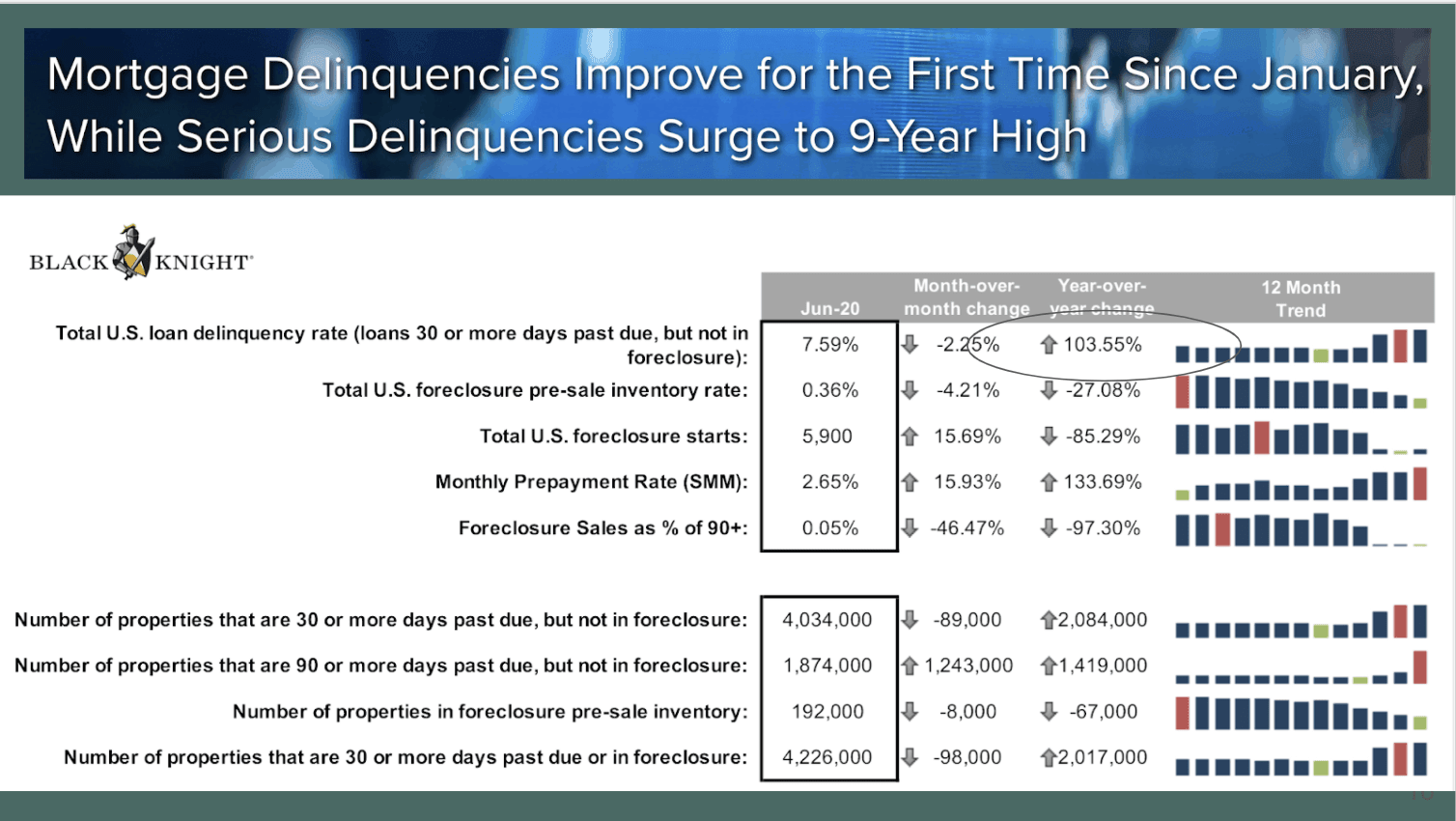

Here is a chart that shows the mortgage delinquencies improved for the first time since January. We’ve been having higher and higher mortgage delinquency since January, but then the serious delinquencies, meaning 90 days plus, have surged to a 9-year high, which is from our last recession. Now let’s look a the total U.S. loan delinquency rate here, I think it was 7.8% and it came down to 7.59%, but then compared to last year, it has gone up 103.55%. It is quite a bit, and this is talking about over 30 days delinquency, that’s over two million houses.

Just like what you were saying, they are offering these forbearances currently. Personally, I know people who actually took advantage of that, not because they cannot afford it, just because they want to be careful, it’s like might as well do it, because they are offering that. Of course, that doesn’t apply to every single person, but I’m just saying that partially some people took the forbearances because they feel like they can, why not, you know, just take advantage of that for now.

Now, will this whole mortgage delinquencies really lead to the foreclosures? That’s the biggest question, because our last recession was really due to so many foreclosures. From 2008 to 2011, or maybe even 2012, I think 80% to 90% of my business was in short sales, or foreclosures like REO business, that’s it. You rarely have regular sales at the time. But now, what will happen if they have delinquency, are they really going to go into foreclosures?

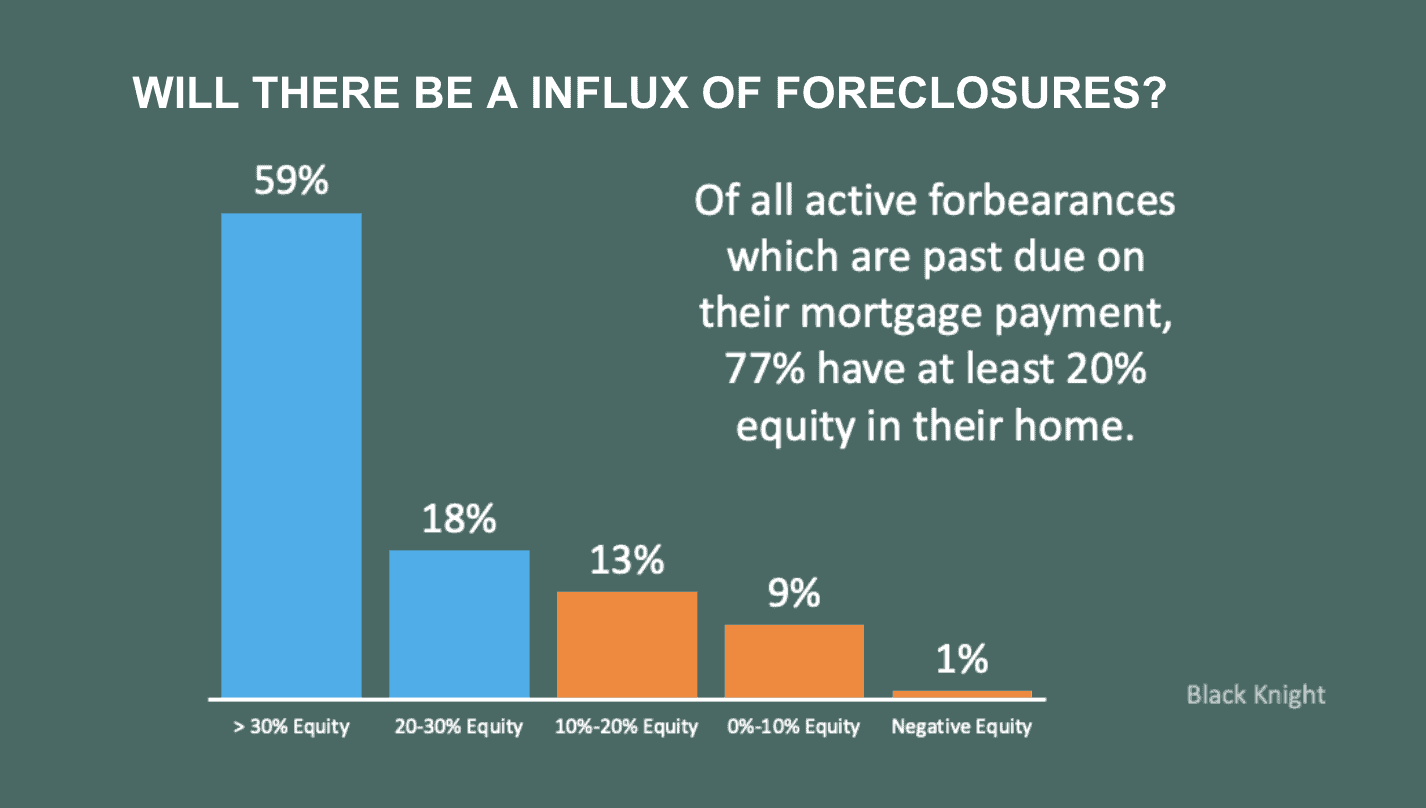

This is really interesting, the data above it’s by Block Knight, and they show that over 77% of these forbearances actually have at least 20% equity in their home, which means that they can just sell their home instead of going through the short sales, or being foreclosed on. If the last recession was mainly because there was no equity in it so that’s why everybody was doing short sales and foreclosure, so I definitely agree with you Daniel, that I think the forbearance is just some people are taking advantage of it right now, but is it going to lead to massive foreclosures? I really don’t feel that will happen, especially in the Bay Area and LA area.

Daniel: I was going to agree with that, too. If it happens, it’s not going to be in the Bay Area or LA. I certainly could see that happening, maybe in a market like Las Vegas, especially if the casinos closed back down again, because right now they may have 20% equity, but if the housing market in that small area starts crashing, then maybe they don’t have equity anymore. And they’re out of work, and they may end up in a situation where they have foreclosures there, but I don’t see it in Los Angeles and Bay Area.

What we’re going through now is very different from what we went through in 2008. It’s not the same thing. 2008 was caused by bad lending essentially, and everybody was able to buy a house without having to prove what their income was, they could get 100% finance then. It was a disaster waiting to be made, whereas this is a very different thing. There is a great number of people in this country that are hurting right now, because they’re not able to work, or they’ve lost their jobs, but it’s a different situation in the sense that it’s not a housing bubble that’s popped that was created artificially. This has to do with a pandemic that’s having a, hopefully, temporary impact on the economy, not a long-term impact, only time will tell.

Again I try to look at it from our markets like the Bay Area and Los Angeles, and I feel like they’re almost, not completely, but almost immune to what’s going on. Because I’d say 80% to 90% of the people that can afford homeownership in these areas are not in the lines of work that are being heavily enough affected by the pandemic that they’re not able to make their payments, and that they would potentially have to lose their house.

Furthermore, as you imagine because people do have equity, and in the moments, we just looked at some numbers, the housing prices are still going up, at least for single-family. We saw that in the numbers that you showed. In a market where they’re still going up, there’s no reason to foreclose. I think there are a lot of people, I hear it from clients all the time – I’m gonna wait for this big foreclosure and I’m going to buy a house for 50 cents or a dollar, and I time it. By the time you think that comes, it’ll actually cost you a dollar fifty to buy the same house, so you know, it’s a way that you can’t win – the longer you wait in California, the more expensive a house is, almost always speaking historically. You can’t wait for opportunity, the opportunity is now, when they’re giving away money. This is like the most opportune time, in my opinion.

Helen: Yeah, and I always say unless you’re a flipper. For flippers, I do agree that you should be very careful right now. It is risky to flip homes, but if you’re buying for yourself for the long term, this is the time where you need to take advantage of the low interest rate because once it goes up, I don’t know if it will come back down. This is a historic low. When I first started investing, I was buying at 7% or 7.25% mortgage rates at the time. Now is below 3%, we gotta take advantage of that.

Daniel: Absolutely.

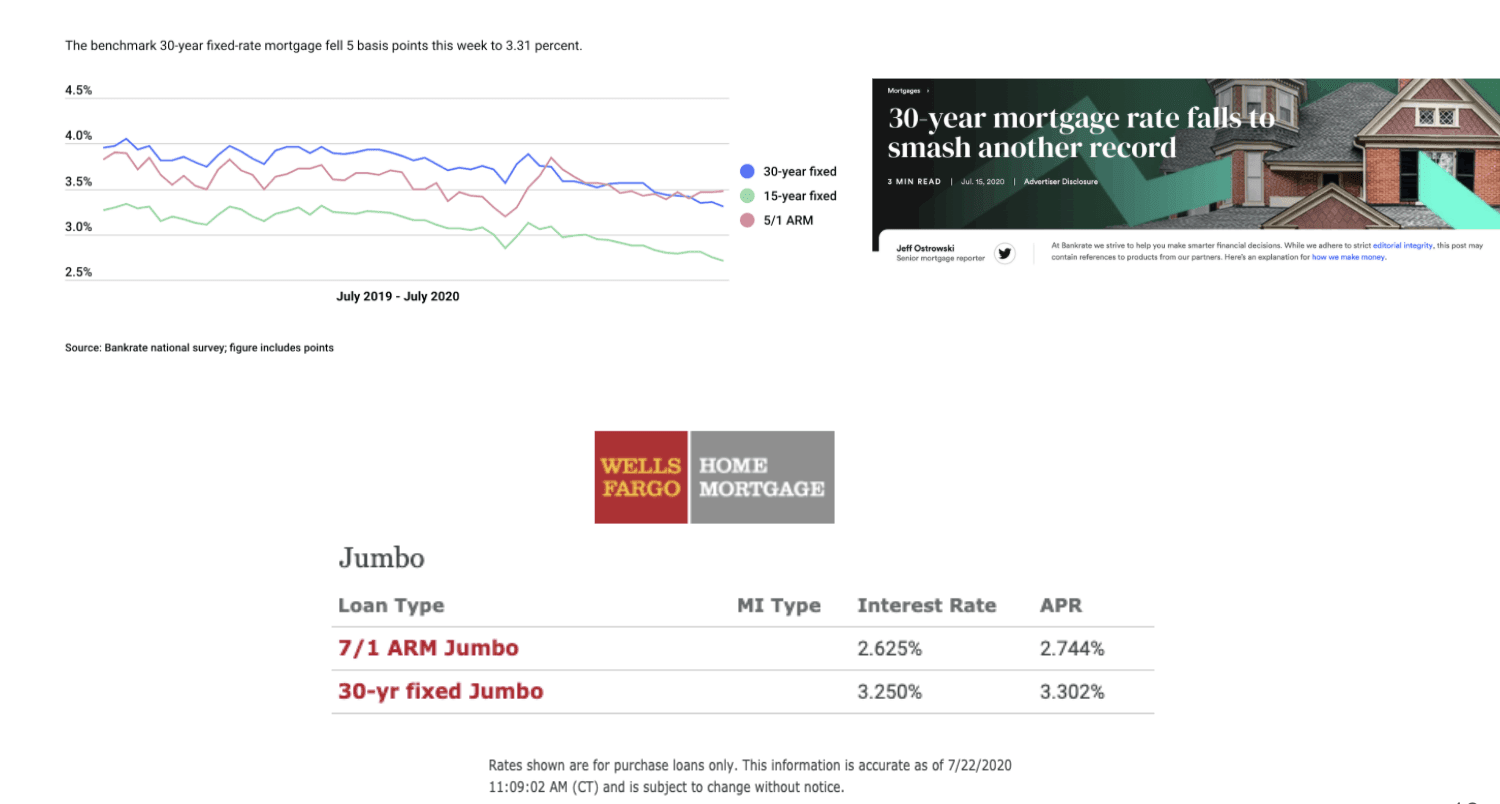

Helen: And let’s see, this is the mortgage rate chart here. As you see again, 30 years have come down quite a bit. Maybe Daniel can definitely give me a little bit more information about this, but even 30 years it has gone down to a record low right now. I just pulled these rates from Wells Fargo, this actually has not changed since the last webinar. It is still at 3.25% for 30 years fixed jumbo. I know you cannot just call it – okay, 3.25%, everybody gets that. Of course, it depends on your credit score, depends on your loan to value, it depends on a lot of different factors. So maybe this is a good time to ask you, Daniel, what are the most important things that people need to pay attention to before they ask for a rate quote?

Daniel: Yeah well, I mean it’s just important to understand what you see in the media. I see a ton of articles that say the 30-year rate is now at 2.99% or something like that. It’s important to know that any of these numbers are usually based on a couple of scenarios. One is the base conforming nationwide loan limit, which is $510,400 loan amount nationwide. They’re based on a 25% down payment because there’s better pricing at 25% versus 20%. Furthermore, a lot of times that rate may include points, so additional fees you have to pay a bank to get a lower rate. And it depends on the exact scenario, of course, there’s a big variance, every scenario is different, so just know that you can’t just blanket and say – what is my rate? That’s like saying – how much does a car cost? It could be for 20 bucks, or it could be a Maybach for $200,000, so it’s an arbitrary question, and you have to be more very detailed about it.

When you’re talking to lenders it’s important to specify your exact scenario – what is your credit score, what purchase price are you looking to buy at, what down payment are you looking at, and what type of property is it, whether it be a condo or townhome or single-family or multi-unit, all of those are going to have different rates. It’s important to be very specific with your lender as to if you’re just trying to get quotes on rates to be very specific about the scenario and ask the lender if there are any points associated with the rates that they quote. Because what I find is a lot of lenders quote the lowest rate they possibly can without mentioning, since this is a verbal quote, the costs associated with that rate, just to get somebody interested in working with them. So if you’re really trying to shop and get a comparison, know what are the costs associated with the rate, and make sure the rate is based on an actual scenario you’re looking for.

These days I’m seeing, you know, for example, today I spoke with someone that was looking to buy an $800,000 single-family home with 25% down payment, he had good credit, everything was in great shape, and we quoted 2.75% 30-year fix with half a point. So the right scenarios, there are some amazing options out there. Honestly, I always tell everybody the same thing. I’ve been doing this for 15 plus years, but if I had done this for 150 years, I would say the same thing – rates have never been better than they are right now.

And to your point as a flipper. Yes, now’s a little bit of a risky time for a flipper, because there’s still some own specific for them to live in or to hold long term. Even as an investor, as a long-term role I honestly think it’s a phenomenal time because you can buy, have such cheap money to borrow, and you can wait out the market. Even if in two, three years from now, the prices do come down a little bit, historically speaking over a 10-year period, there’s never been in the history that, recorded history, at least that I’m aware of, any time that over a 10-year span housing prices in Los Angeles or the Bay Area have ended up less than where they were 10 years prior, which tells me that as long as you’re willing to hold long term, I don’t think you can go wrong as far as making money and appreciation of your property in these particular markets. It’s very specific, I know somebody in Maryland who bought in 2007, where now 13 years later, they still haven’t recovered from the value drop that they had. So it’s very specific that we are in a unique market where appreciation truly never seems to end, although there are differences here and there, really in a 10-year run, nobody has failed at this yet.

Helen: Absolutely, and from our experience as a realtor, we always recommend a few loan officers that we’ve worked with, we know they’re honest, we know that they do a very good job. But sometimes our clients do say – hey, I saw an ad and they are quoting 2.75%. As a matter of fact, we just had somebody who said that. This online loan program said that she can get 2.75% or 2.65% for 30 years fixed, and then, of course, she insisted going with them, and then during escrow, they said – nope, sorry, you don’t qualify for that 2.75%, you qualify for this higher rate. Now she is stuck because she is under contract. There is this timeline that she has to fulfill, she doesn’t have time to shop around anymore, so it is really important. On top of that, this online platform, whoever that person’s loan officer is, never gave us any update. We never know what’s going on, our client couldn’t even find or get in touch with them. They will contact you when they have updates, that’s about it. They’re not going to talk to you in between this time frame, so you have to be very careful. We always say find someone you can trust. Find the reviews or your realtors have worked with these loan officers. They are the one who will tell you the truth, and also do a good job, but don’t just randomly find an online lending program out there. I mean if you’re a refi, or not under some time crunch, maybe you can test it out, I guess, but if you’re doing a purchase, just be very careful who you’re choosing in terms of financing.

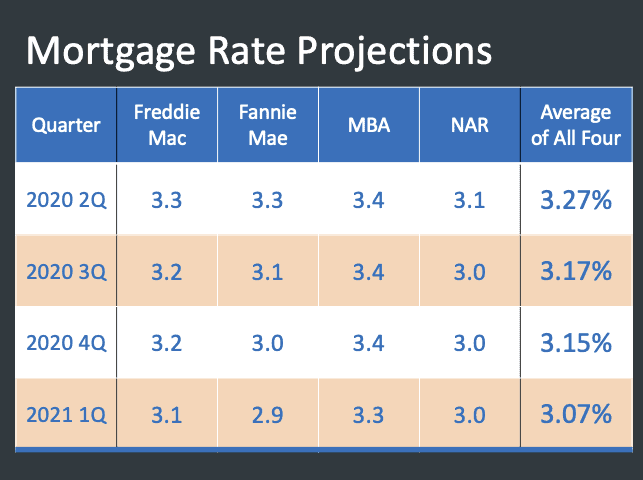

Now, I also want to share this chart with everybody, I shared this last time as well regarding the mortgage rates projections by a few of these agencies and organizations. Pretty much everybody has this prediction that the interest rate is gonna stay really low for the next four quarters until 2021. Is that what you’re seeing, Daniel, as well?

Daniel: Yeah, I’ve been reading the same thing, and a lot of people asked me about this. My general opinion is that I don’t see any reason why they should go up. I think they should stay down, the economy is still not in a great place, and I think it would be detrimental to the economy that changed the direction of the interest rates.

I do think that one factor, which I don’t really opinion how it’s going to affect things, is that we are in an election year, and I don’t know what implications that will have on interest rates, because I feel like interest rates do kind of follow consumer confidence. So I don’t know what’s going to happen with rates as a result of the election, but I will say that my expectation is that I do agree with these analyses. I think interest rates should stay at these historic lows, you know, bottom of the threes, top of the twos, kind of in that range for the 30-year fix. For the next 18 months, this is what I would agree with as well.

Helen: Yeah, and we always say that housing is really a lead indicator to bring the economy back. Right now, to be honest with you, all these small businesses are not doing so well. Like this city on the city level and the county level, they really need property tax and county transfer tax. If you don’t have housing transactions, you don’t really have these taxes. They learned from last 2008 mortgage crisis, they don’t want to repeat that again, so that’s why this time they have reacted so fast to drop the federal rate, and now the mortgage rate, of course, has been staying low as well.

Thank you so much for reading this blog, we hope this content has helped you understand the current housing market a little better. If you have any questions that you would like to discuss in detail, feel free to reach out to Helen Chong at [email protected] or schedule an appointment. Meanwhile, we will bring you the latest updates and statistics on the Bay Area housing market regularly through our social media platforms and blogs. Find us on Facebook, YouTube, LinkedIn, or Instagram!

Stay up to date on the latest real estate trends.

A Bay Area Realtor's approach to schools, neighborhoods, and long-term value for families making a move

Part 1 of HAYLEN's series on the 2026 CCIM Spring Forum in Philadelphia

You’ve got questions and we can’t wait to answer them.