2021 Bay Area Housing Market Forecast – California exodus cause a housing market crash?

Welcome to our first Bay Area Housing Market Update of 2021! We are very excited to share with you the housing market data for the month of December. As we are very surprised, the month of December has been very busy, but also there are a lot of rumors about a 2021 housing market crash, and whether it’s caused by this California exodus, so I would love to share these data and statistics with you to see if this is really going to happen in 2021. On top of that, I thought what’s better than showing you the actual case studies and the offers that we have made during the month of December, so you can see the competitiveness on the market for different areas and different asset types as well. As always, I welcome your new ideas of what you would like me to share, so I can continue to produce more relevant educational videos for all of you. Thank you so much for reading, and I hope you enjoy it! The video version can be found here.

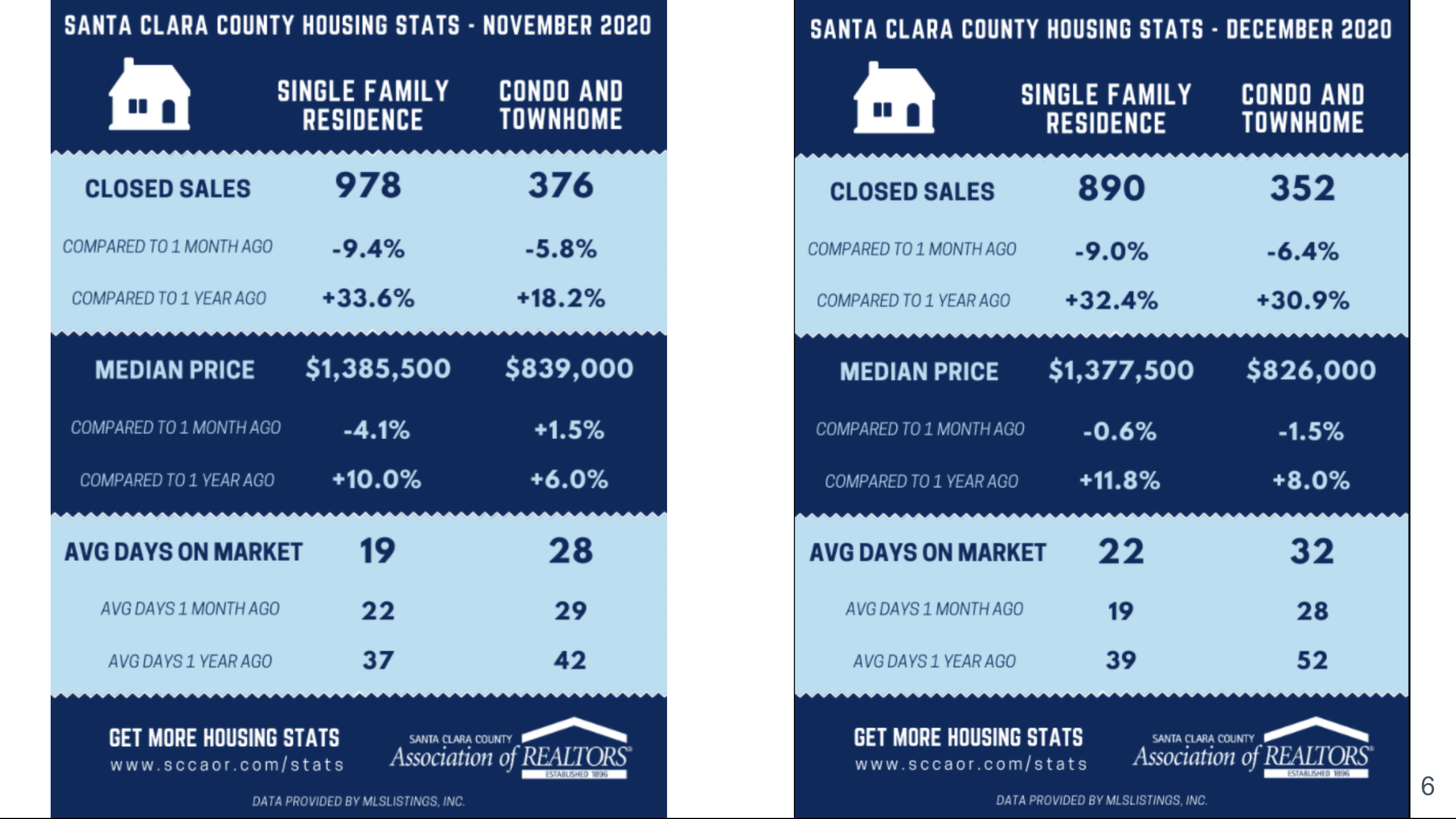

Let me go ahead and take a look at the Bay Area housing market statistic here. As you can see here in Santa Clara County for single-family homes, the number of sales in December compared to November. In November, we had fewer sales compared to October, and then in December, we had even fewer sales compared to November. The same thing happened to condos and townhomes also, however, we actually had more sales compared to a year ago in 2019, and the median sales price went up to 1.385 million and came down slightly by 0.6% compared to November to 1.377 million. Typically, it’s pretty common in December because of a slower market, although for us, we really didn’t see that. I think the activity was way more active compared to December 2019, and therefore you see that the single-family price has gone up 11.8% compared to 2019, and for condos, it did go up by 8% compared to 2019. If you look at the days on the market now, we are still right around 19 days versus 22 days in December, it’s slightly more but it really is not that much. Compared to a year ago, we definitely have dropped quite a bit. Of course, for condos and townhomes, we are still seeing that the number is a little bit higher in terms of days on the market for Santa Clara County.

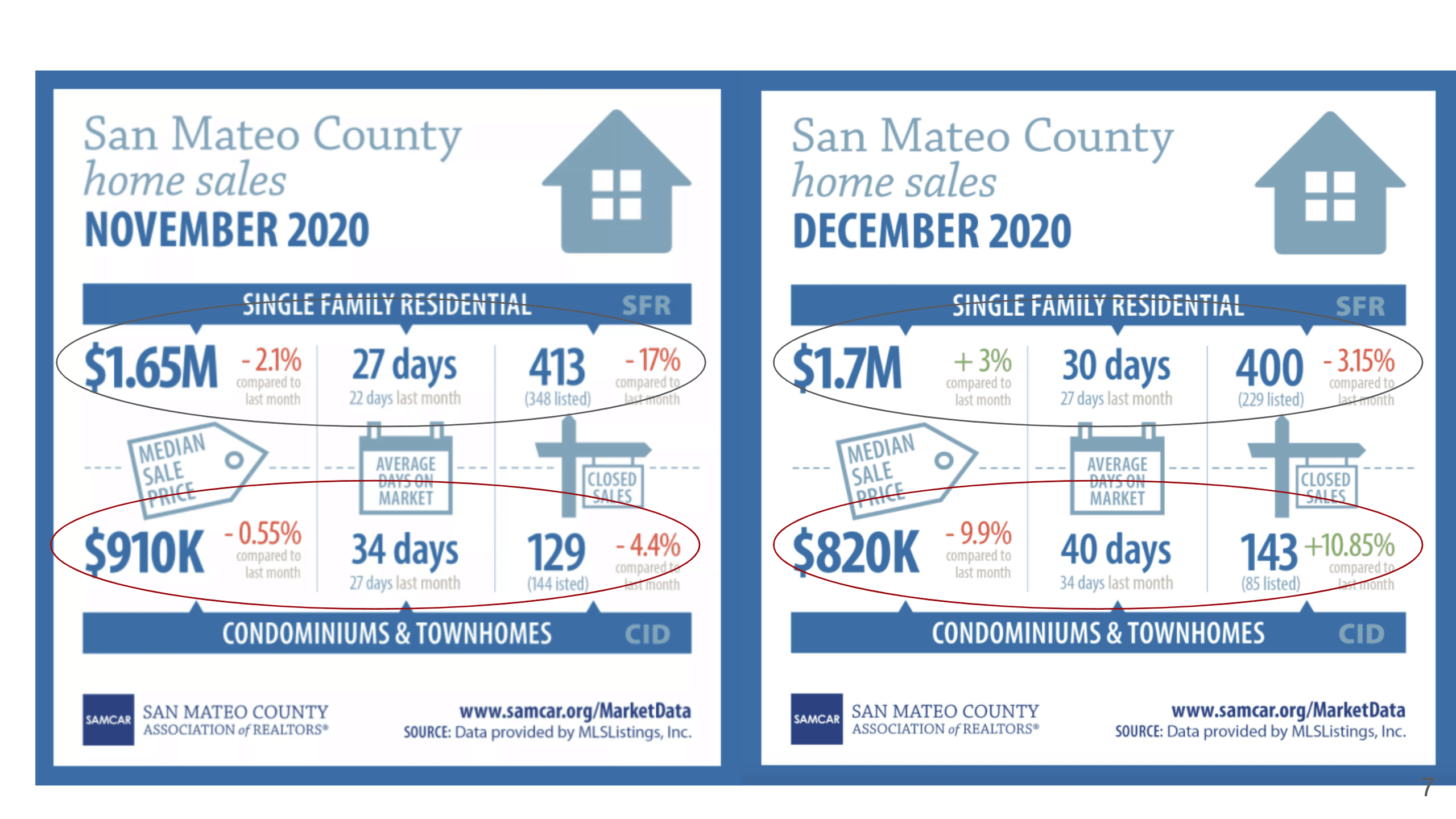

What about San Mateo County? As you know, we’ve been talking about this for quite a few months now, in San Mateo County we have seen a little bit of a decrease in pricing, but very interestingly, last month in December it actually went up 3% compared to November, so the price had gone up a little bit. Properties stayed on the market for about 30 days instead of 27 days, which was definitely a little bit longer. We also see that we have a 3.15% less list property. For the condominiums, the price did drop quite a bit. Again, condominiums and townhouses definitely got hit a lot harder no matter which county you’re in, so you see that the price has gone down 9.9% for condominiums and townhomes, and they also stay on the market a lot longer. There were more properties actually closed in the month of December, but at the same time, the price still had gone down. So we’re gonna take a look at the statistics later to give you a sense of why the condos market has gone down, and also whether it’s a good time to actually come in and buy the condominiums down now.

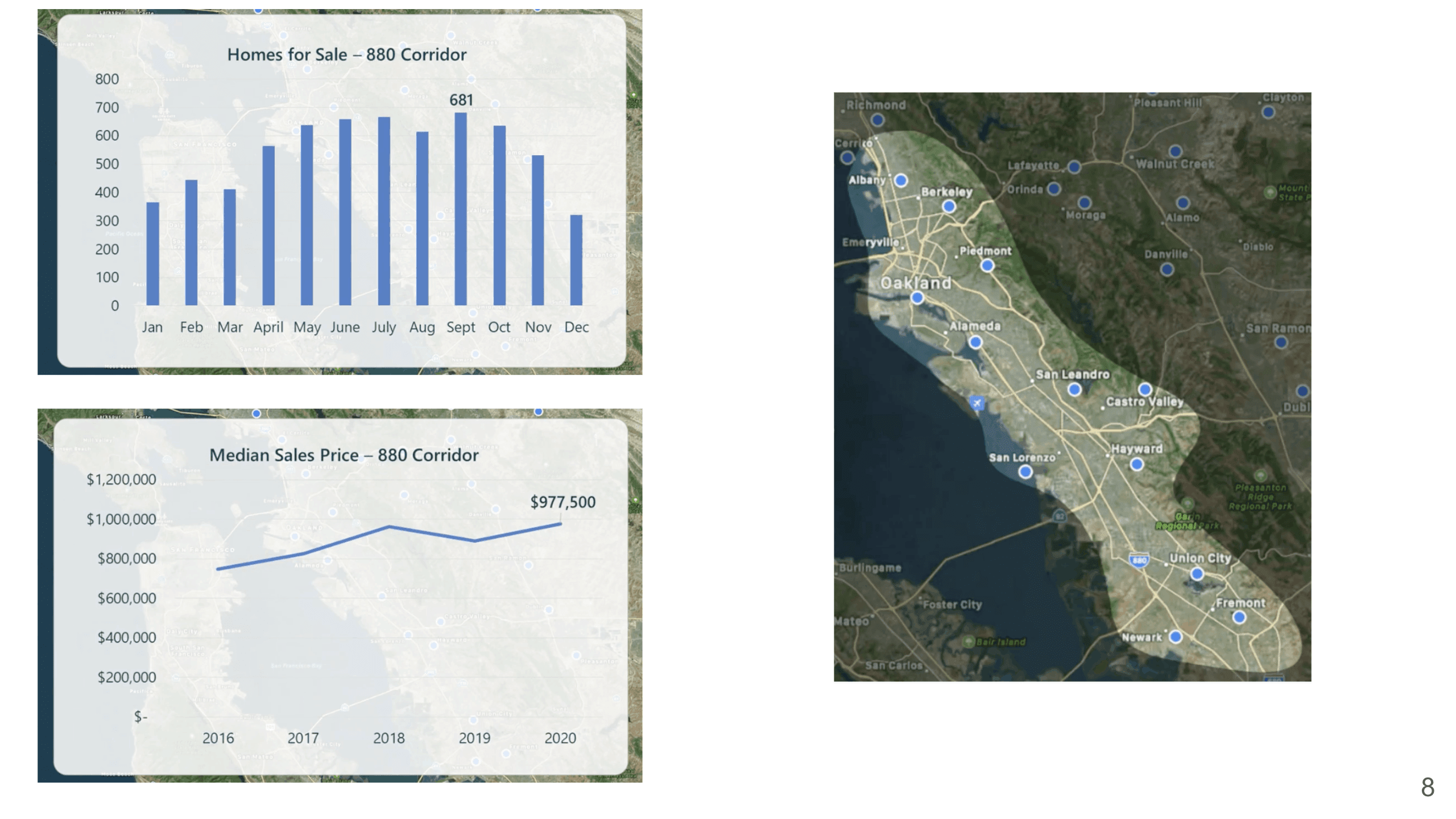

These are the East Bay markets and the 880 corridor, such as Union City, Fremont, Newark, all the way up to Berkeley. You see that home sales have dropped, you know, for December, of course, it had very few home sales. I don’t know if you guys have been looking at the inventory, but every single buyer we’ve talked to, they all told us that – my gosh there’s nothing to see. It’s true that the inventory is very low, and the price has still continued to go up. As you see that in 2016, it was less than $800,000, now it’s almost inching up to close to a million dollars for the median sales price.

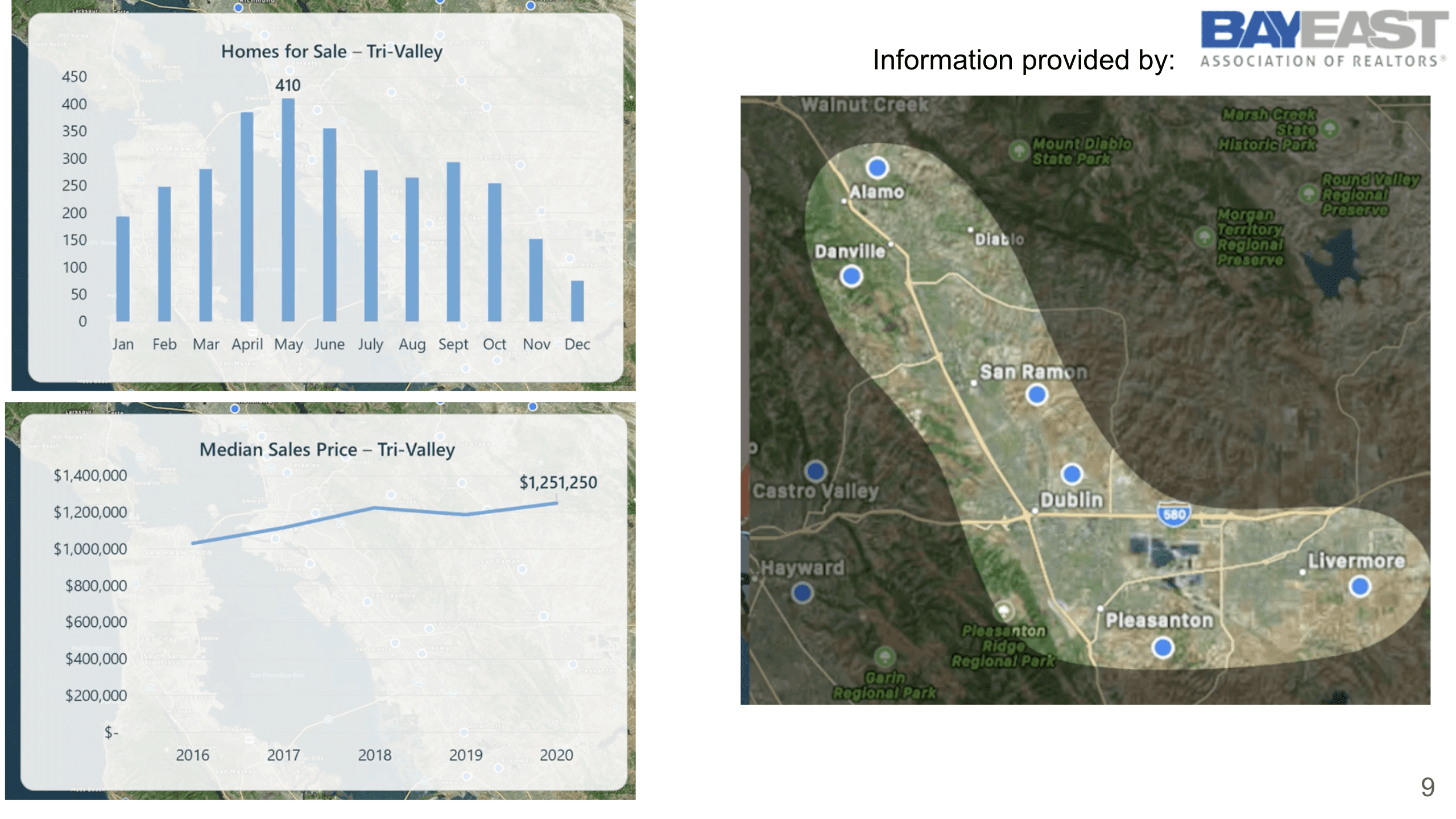

In terms of Tri-Valley, the same situation that the home for sale peaked in May, and then the number of sales just kept going down, especially because, as you could tell, it was during the COVID pandemic, so a lot of sellers are actually holding back and not wanting to put properties on the market. However, the pricing has gone up to 1.251 million.

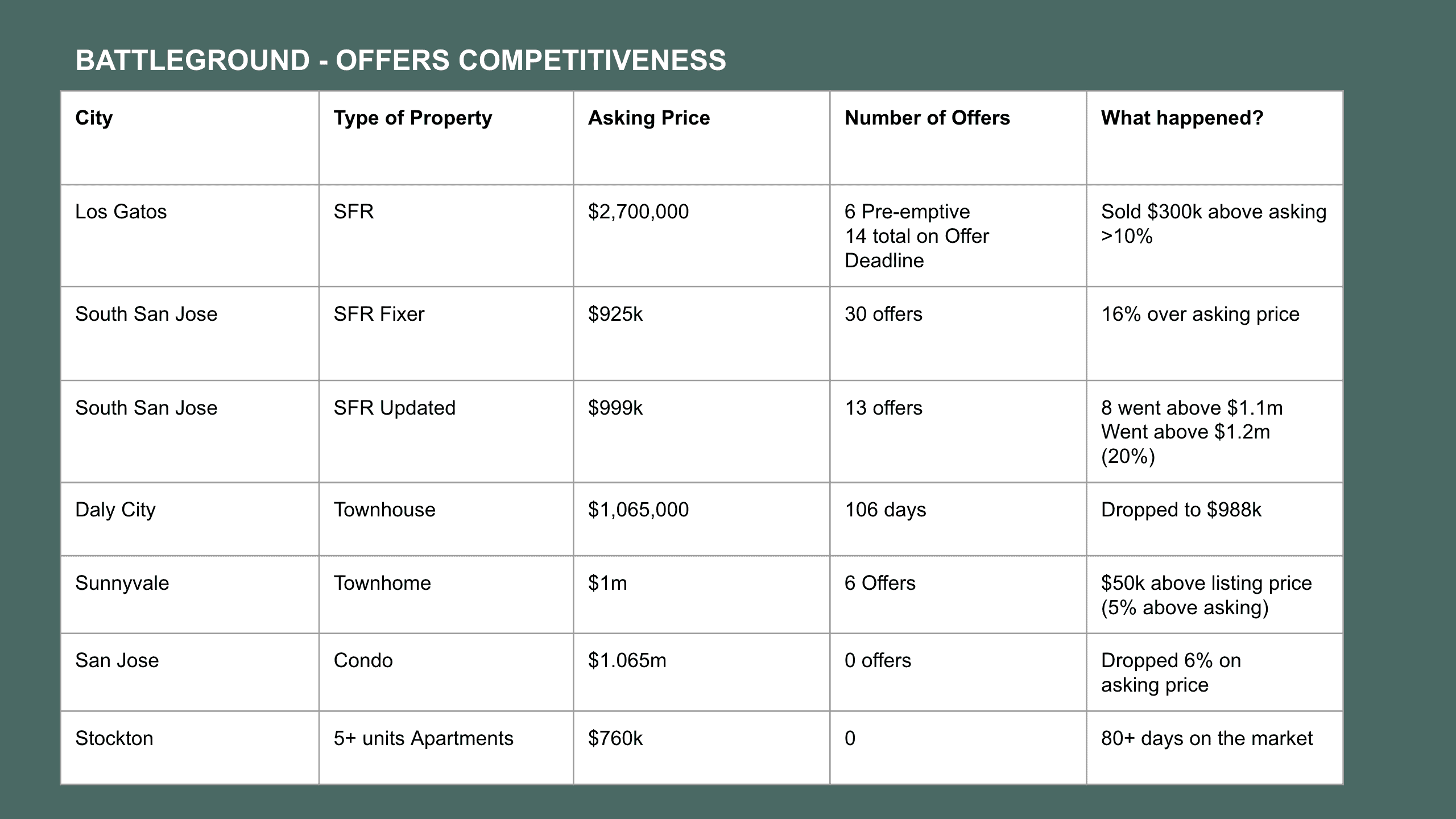

Now, what is happening on the battleground? What kind of offers have we been making? As you see here, in Los Gatos, we have made an offer for a single family with a asking price of 2.7 million dollars. There were six preemptive offers, meaning that people just did not want to wait for the offer deadline, they just jumped in with an offer. In the end, sellers decided to wait and the 14 total offers were made on the offer deadline, and it was sold $300,000 dollars over the asking price, which is over 10%. A fixer in South San Jose, its asking price was $925,000. It got 30 offers – this was literally during the Christmas break – and in the end, it went 16% over asking price. Another updated one, asking price $999,000, they got 13 offers. As you see, fixers are very popular, I mean, updated homes still have a lot of offers. It actually went 20% over asking price, and 8 out of the 13 offers went above 1.1 million. As you can see, South San Jose didn’t have this kind of competition in 2019 or 2018, but now you definitely see a lot of competition even in the South San Jose area. Now, in Daly City, there is a townhouse that’s asking 1.065 million, stayed on the market for 106 days, eventually dropped the price to $988,000, no offer. Sunnyvale townhome asking one million dollars, they did get 6 offers, so it’s still competitive because of the location. It went over $50,000 dollars above the listing price, which is just about 5%. You could tell how the difference is between a single-family and townhouse. A condo in San Jose, asking price was 1.065 million, it didn’t get any offer, as a matter of fact, they dropped the price by 6%, and it’s still on the market. Then there is a 5+ units apartment in Central Valley Stockton, asking price of $760,000, didn’t get any offer, and it’s been on the market for 80+ days.

So what is going on with this market? You know, the market has been so hot, there are still people who are able to sell properties. Actually, I wonder if the real estate practice has been permanently changed. One of the big things, of course, is the open house. There are no more open houses, which used to be the way to sell homes – you want to do open houses, you want to attract a lot of people coming into the house – but now, you don’t need to do open houses, and you can still sell a home with that many offers. As a matter of fact, in my eyes, without the open houses, it’s actually safer for the homeowners – you don’t have to worry about random people just walking into your home. Trust me, when we used to do open houses and a lot of people came in, we had to have two, three, or even four agents to be at the open house, just so that we can keep an eye on everybody to make sure they’re not stealing anything. So it is safer for the homeowners as well as the real estate agents, as you know, it can be pretty dangerous for somebody who just sits at an open house with no one around. Also, buyers really get the best representation from the real estate agents, really understanding and walking through the property by themselves, and looking at everything carefully. So as a matter of fact, I do believe that this really should be the way to go, and this is going to be a way to elevate the real estate standard to make sure that buyers are being represented the right way by our real estate agents.

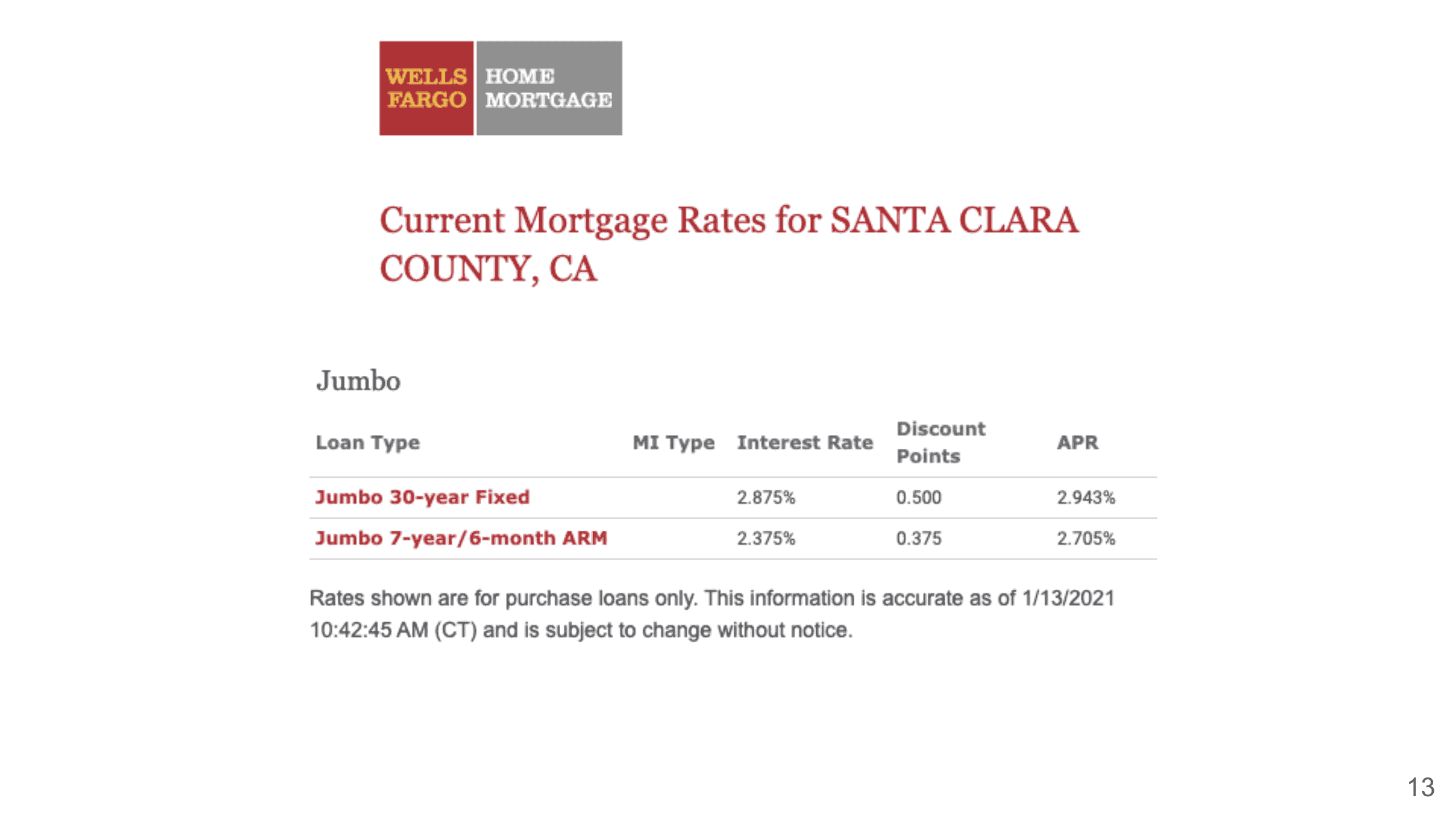

Now, let’s look at residential loans. This is the mortgage rate for today. Wells Fargo has shared that the interest rate for jumbo 30 years is 2.875%. We’ve been seeing this rate for a couple of months now, but it’s still holding up pretty strong.

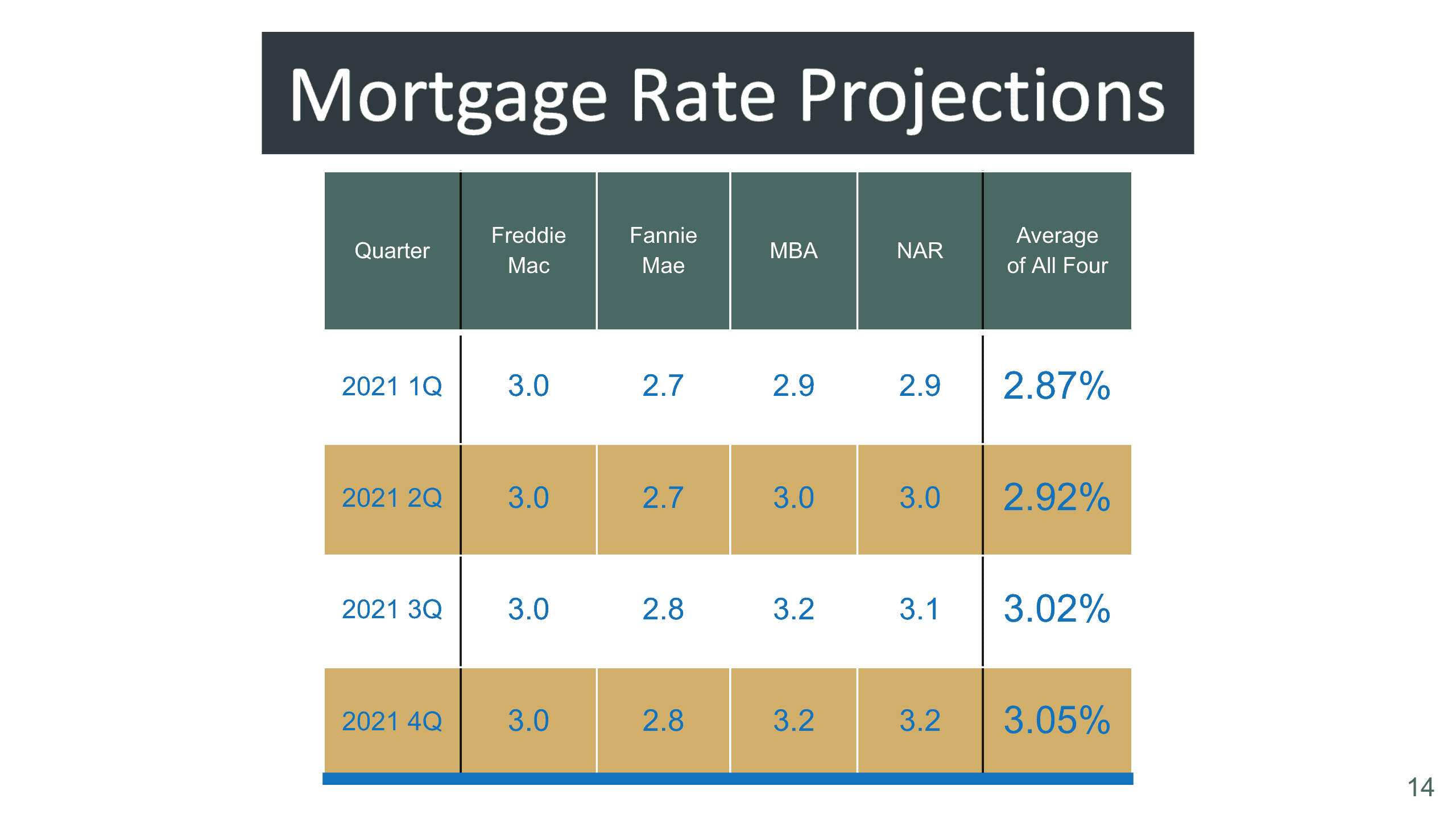

These are the mortgage rate projections by different agencies. Again, they did change a little bit, if you notice that now they have projections all the way to 4Q. The past few ones that I shared with you were only projected up to 2Q 2021. Freddie Mac has the same rate across the board. Fannie Mae believes that 3Q and 4Q are going to inch up slightly. The Mortgage Banking Association believes that it is going to actually inch up a little bit starting 2Q, and then go up to 3.2 starting 3Q 2021. The National Association of Realtors predicts the same thing, it seems like it’s inching up to 3.2 by 4Q 2021. I think most agencies are predicting that the mortgage rate is going to go up, but may not be going up that dramatically.

Now, I know a lot of people are really asking again about the housing crash in 2021. If you type in this term, you see a bunch of videos about housing crashes, and then they talk about the California exodus – everybody is leaving California. So I really want to touch on a couple of these things during this housing market update.

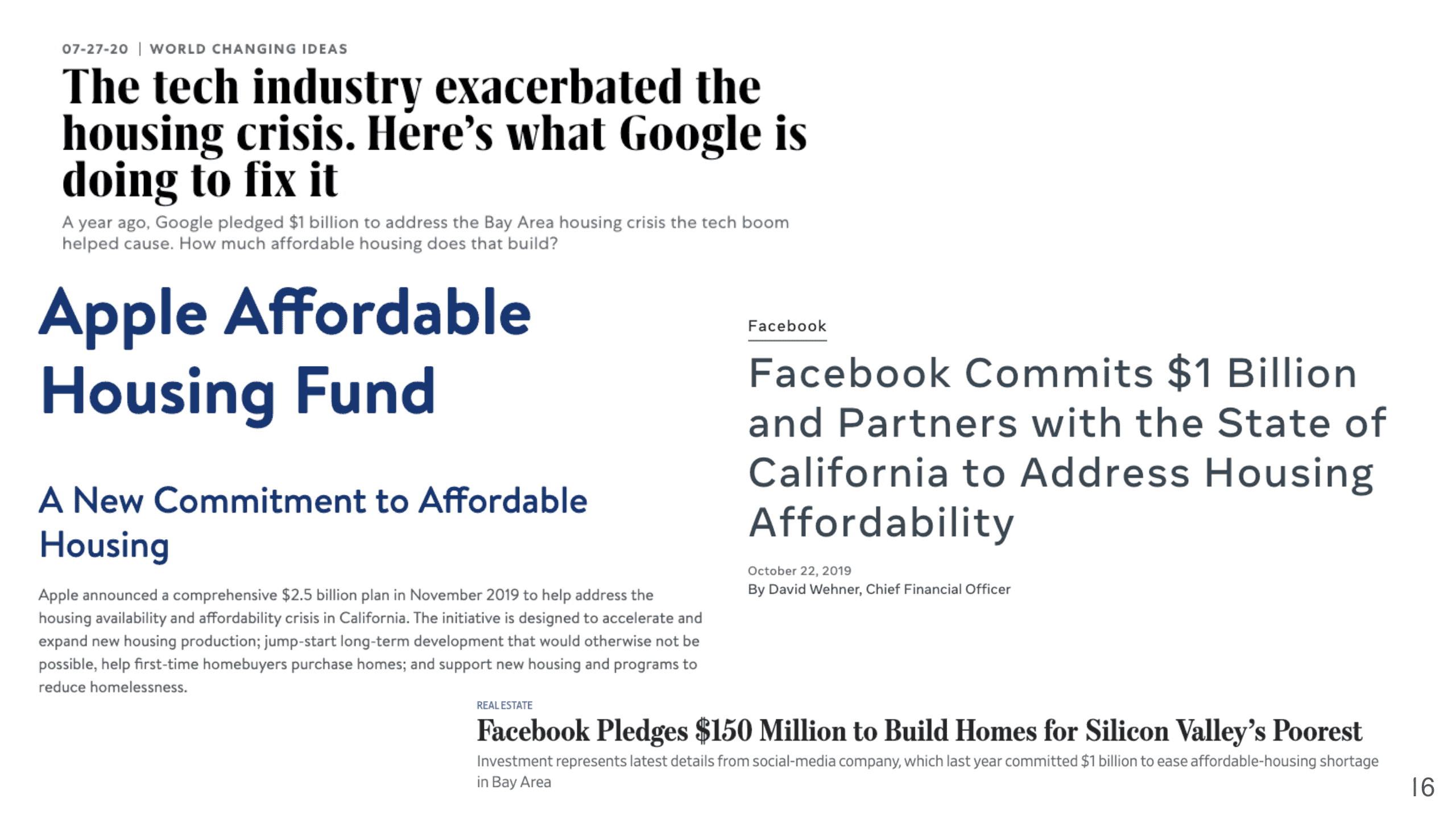

Obviously, Oracle just decided to move, so that was big news, another tech giant had moved out of California. But don’t forget that we still do have a lot of other tech giants in this area, and Oracle actually has been talking about leaving California for a while now. Google had already committed to invest one billion dollars to address the Bay Area housing crisis, and Apple also committed to a 2.5 billion dollar plan. Facebook committed a billion dollars to address housing affordability, and then recently they pledged another 150 million dollars to build homes for Silicon Valley’s poorest. Why I’m sharing this is because these major employers, these tech giants, have invested so much in the Bay Area, so we still have a lot of very strong companies here. Yes, we do have some companies leaving, but really if you look percentage-wise, it’s still not that much. Although I absolutely admit that there are a lot of people and a lot of companies moving and considering moving, I think the biggest question is that will this really affect the housing market. So let’s keep looking at other information that I want to share with you guys.

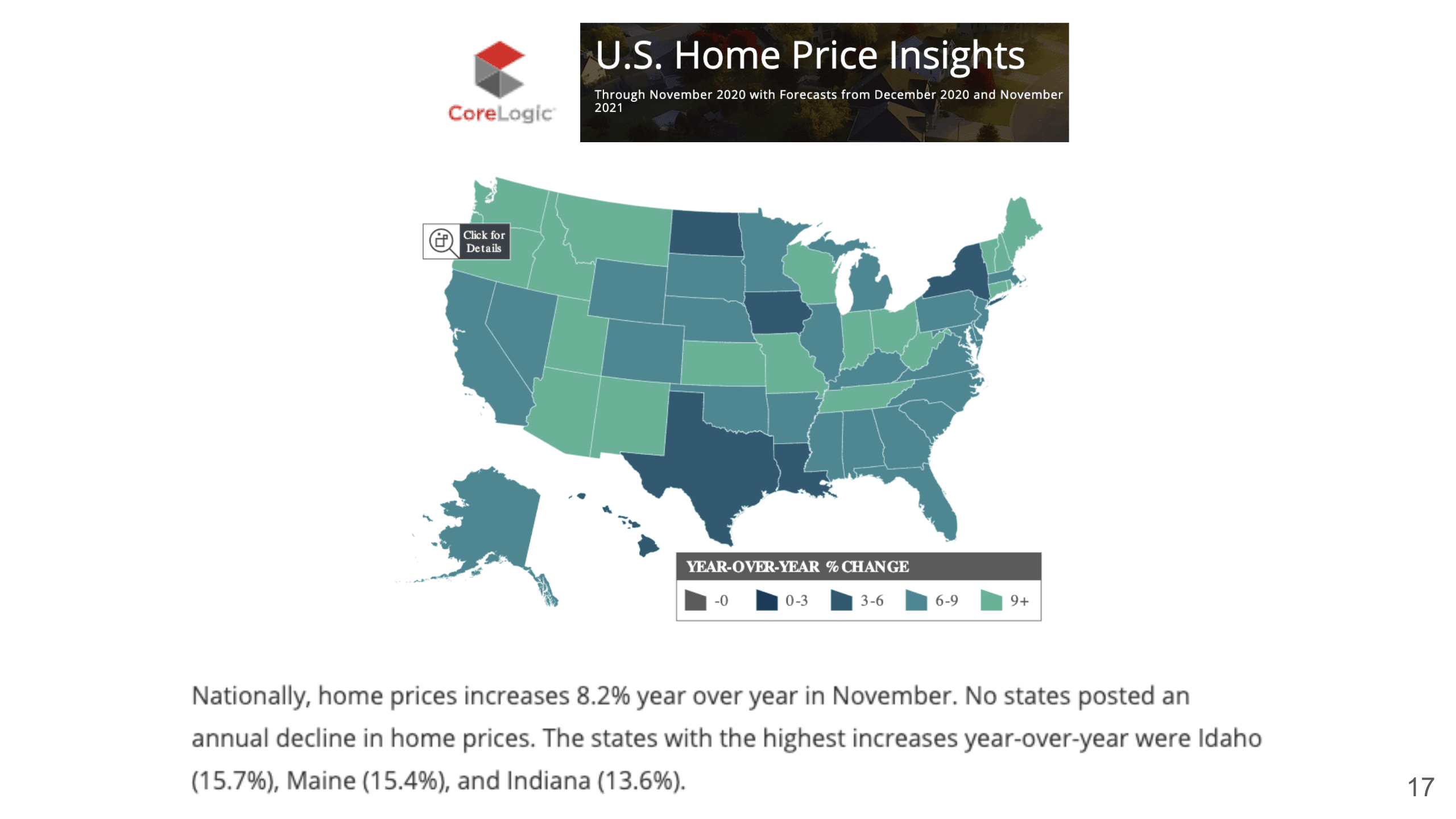

This is from CoreLogic that talks about home price increases year over year in different states. Surprisingly, there’s not one state that has negative change, meaning all the states within the whole United States will have a positive increase in the house prices.

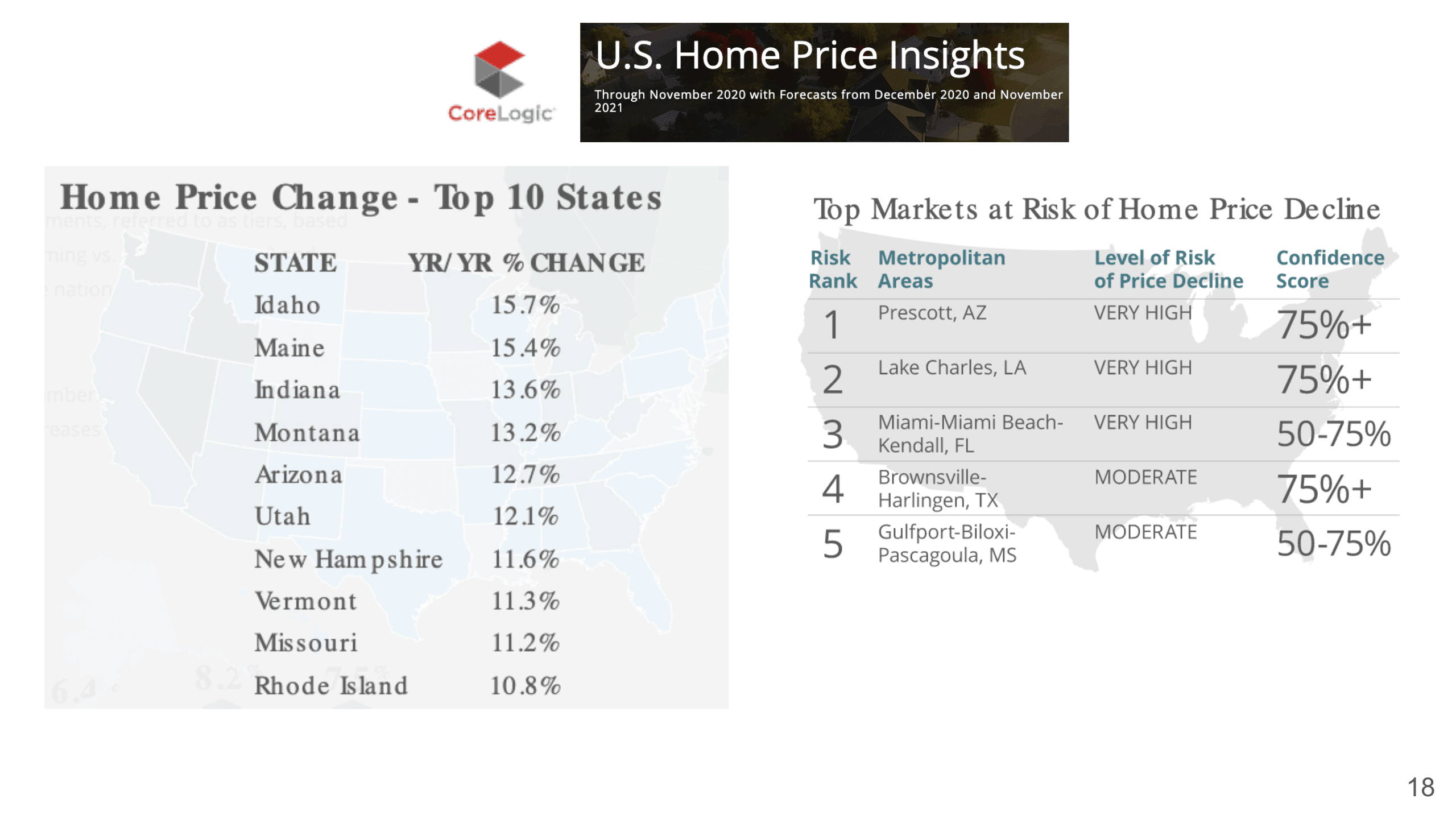

Now, these are the top 10 states with the biggest housing price change – Idaho, Maine, Indiana, Montana, Arizona, Utah, New Hampshire, Vermont, Missouri, and Rhode Island. The list on the right includes the top markets where CoreLogic considers to have a risk of home price decline. They are Prescott (AZ), Lake Charles (LA), Miami (FL), Brownsville (TX), and Gulfport (MS). We repeat this over and over again that it really depends on the area. Even in the United States in general we’re doing great, but we have to look at each market individually.

When we talk about housing crashes, of course, there’s a lot of economic data, but at the end of the day, foreclosure would be one of the biggest things that can cause a housing crash, which happened in 2008. Now the thing is when we look at national homeowner equity, meaning how many homeowners had increased their equity. It averages about 10.8% in 3Q 2020. The year over year change was increased by a trillion dollars total. And the percentage of homes with negative equity actually went down 18.3%, meaning there are fewer people who owe more on the property than the property’s worth. So this went down 366,000 homes in the entire country.

So Americans are really sitting on tremendous equity right now. 42.1% of all the homes are owned free and clear, and 58.7% of all the homes in America have at least 60% equity in them. The average equity of mortgaged homes is $177,000. I mean, I think this chart says a lot. Tons of equity means that if they really cannot afford to pay for the mortgage anymore, they are at the risk of being foreclosed, they can also put it out on the market and sell it to get the best price possible, because typically, you get your property foreclosed is because you cannot sell it on the market, so with the equity that a lot of homeowners still have, it actually makes it easier to sell. Another thing is that, go back to renters versus owners, this is talking about the average equity of a mortgage home, and if you still decide to rent, you are missing out on building your equity, and $177,000 equity is a lot.

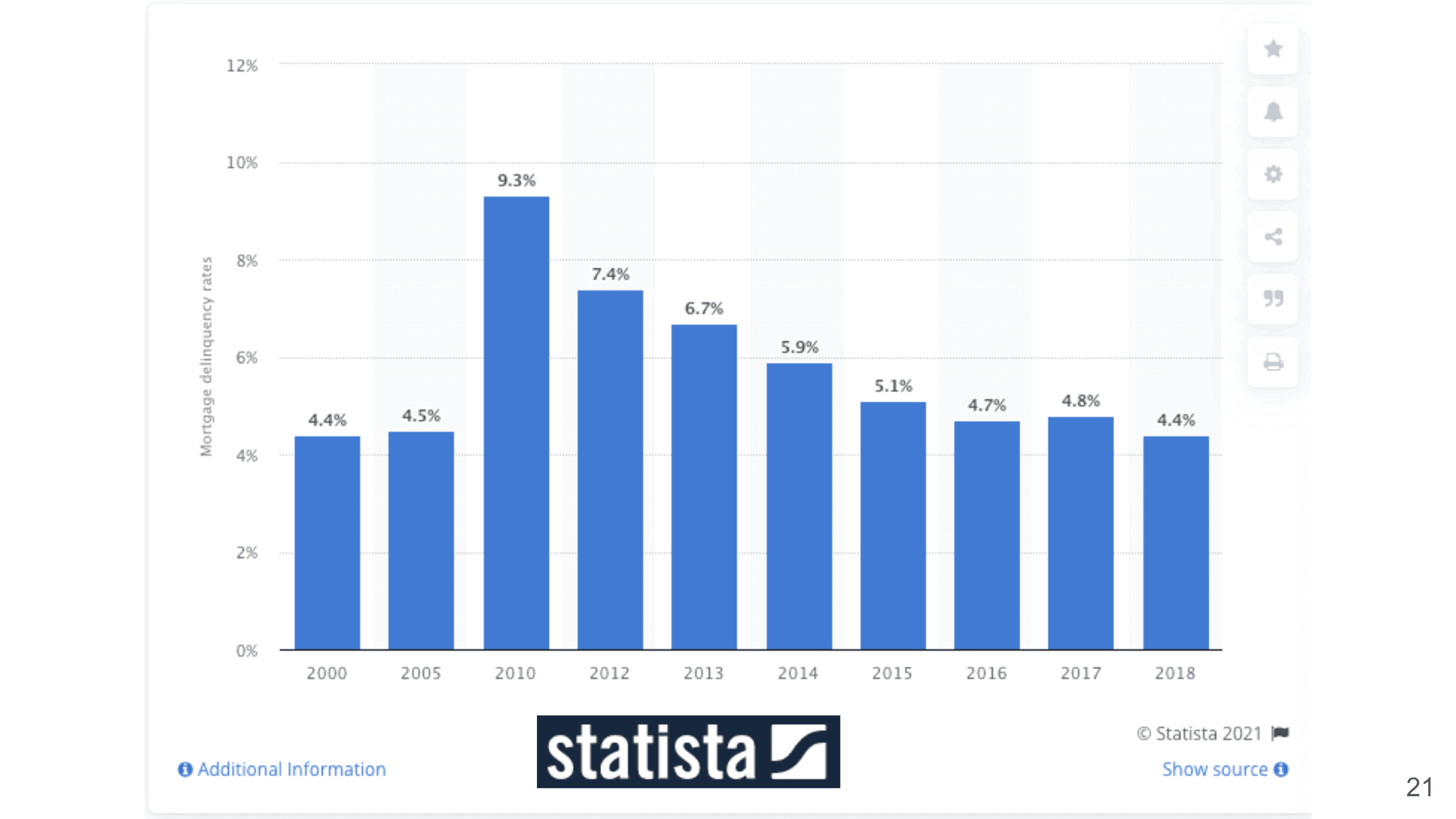

Also, I want to show you the percentage of delinquency. Back in 2010, that was the time during the recessions, it was 9.3%. Then, as you see, when the market was doing much better, it went down to 4.4%.

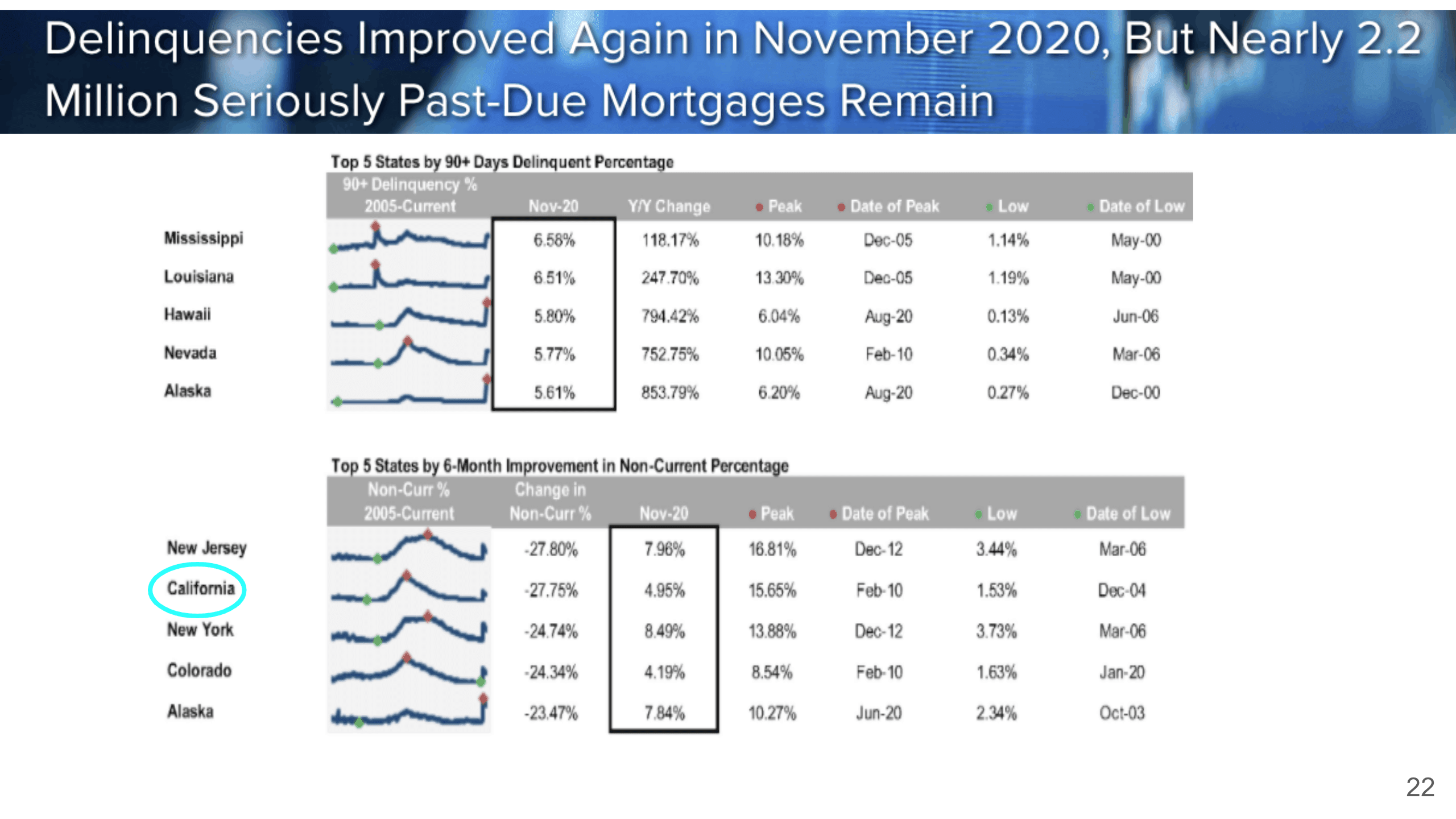

The reason why I’m sharing this with you is that delinquencies did improve in November 2020. There are still 2.2 million seriously past due mortgage remains, but if you look at the number here, these are the 90+ days delinquency. These are the top five states that have the worst delinquency with 90+ days, and they are Mississippi, Louisiana, Hawaii, Nevada, and Alaska. They are at about 5.61% to 6.58%, nothing close to the 9% that we were just looking at earlier. Of course, again, California is not one of them. At the bottom chart, you see that the top five states by six-month improvement in non-current percentage. California is within the top five, so we are down to 4.95%. This is, again, we’re talking about the Bay Area California market so we just don’t see that foreclosure is going to be a factor to cause a housing crash here in 2021.

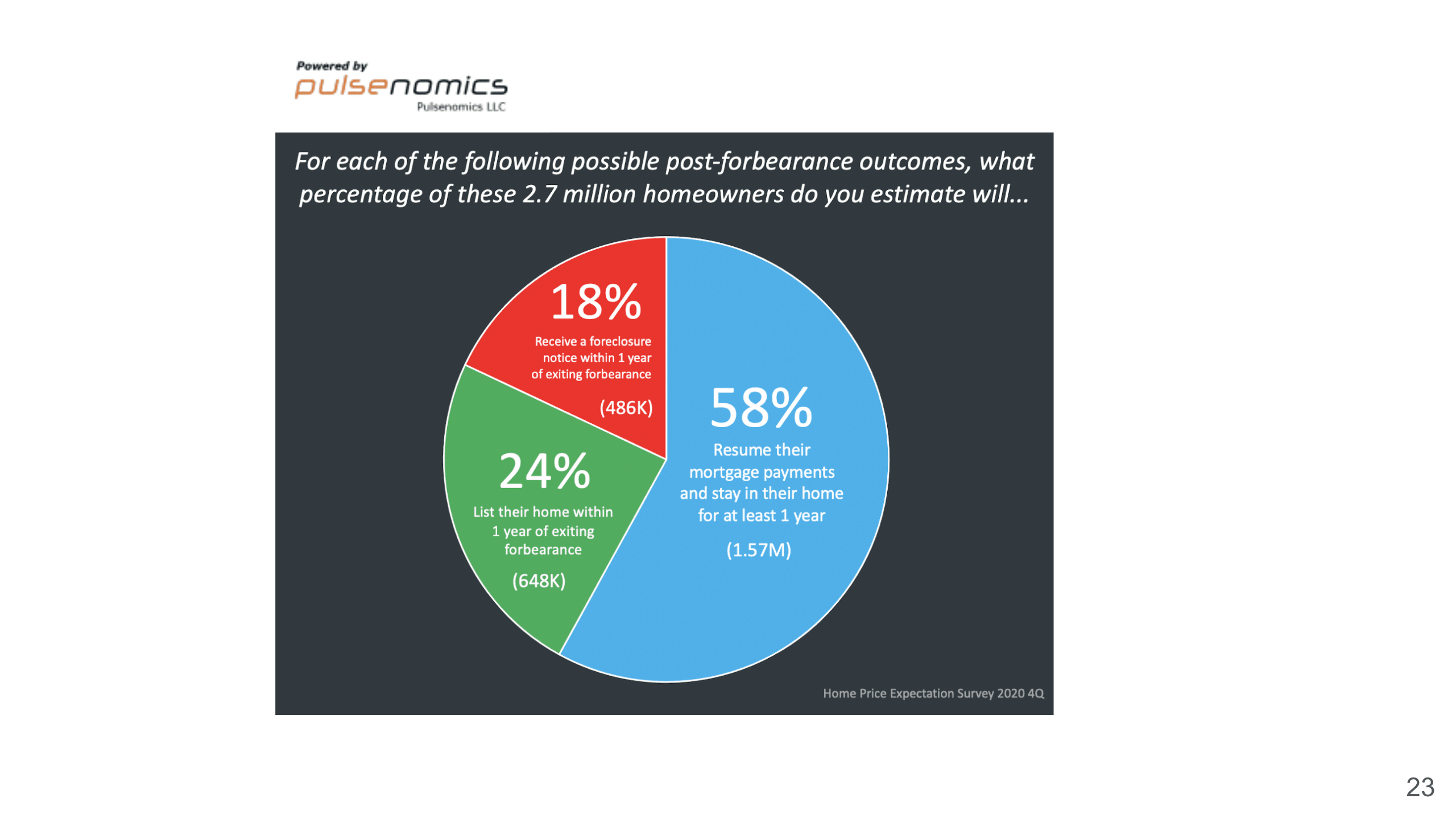

This is a survey asking about the forbearance outcome – what percentage of these 2.7 million homeowners you estimate will actually resume their mortgage payments? And that’s 58% from this survey.

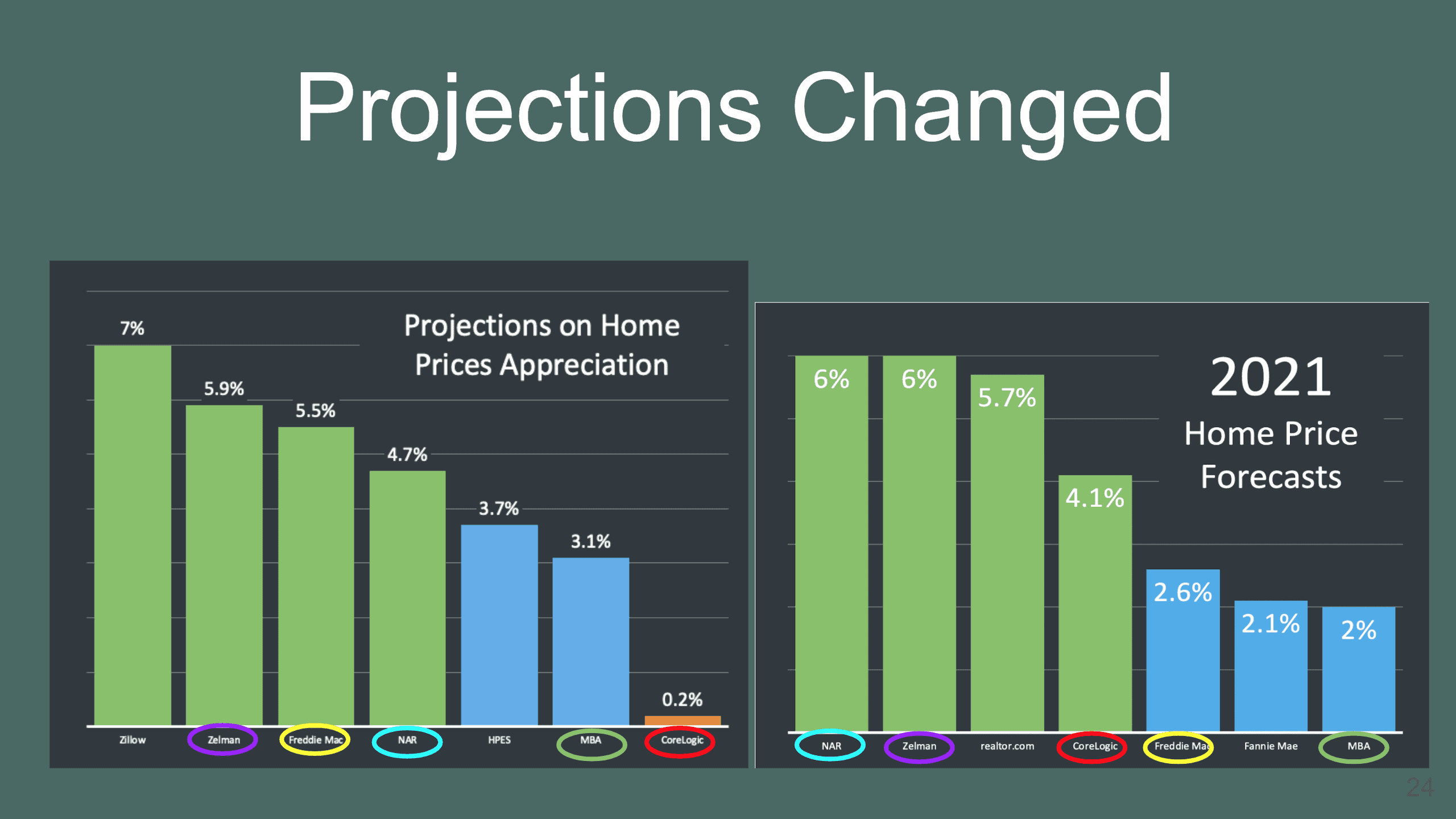

The projection on home price appreciation also changed. Last time we shared with you the projections from these organizations for 2021, and now they changed it slightly. You’ll see that Zelman had changed from 5.9% to 6%, and remember they used to predict around 3%, then went to 5.9%, and now went up again to 6%. Freddie Mac actually went from 5.5% down to 2.6%. The National Association of Realtors went from 4.7% to 6%, the Mortgage Bankers Association went from 3.1% down to 2%, and CoreLogic went from 0.2% up to 4.1%. So again, although some of them went down on their projections, all of them are still forecasting that home prices are still going to continue to go up.

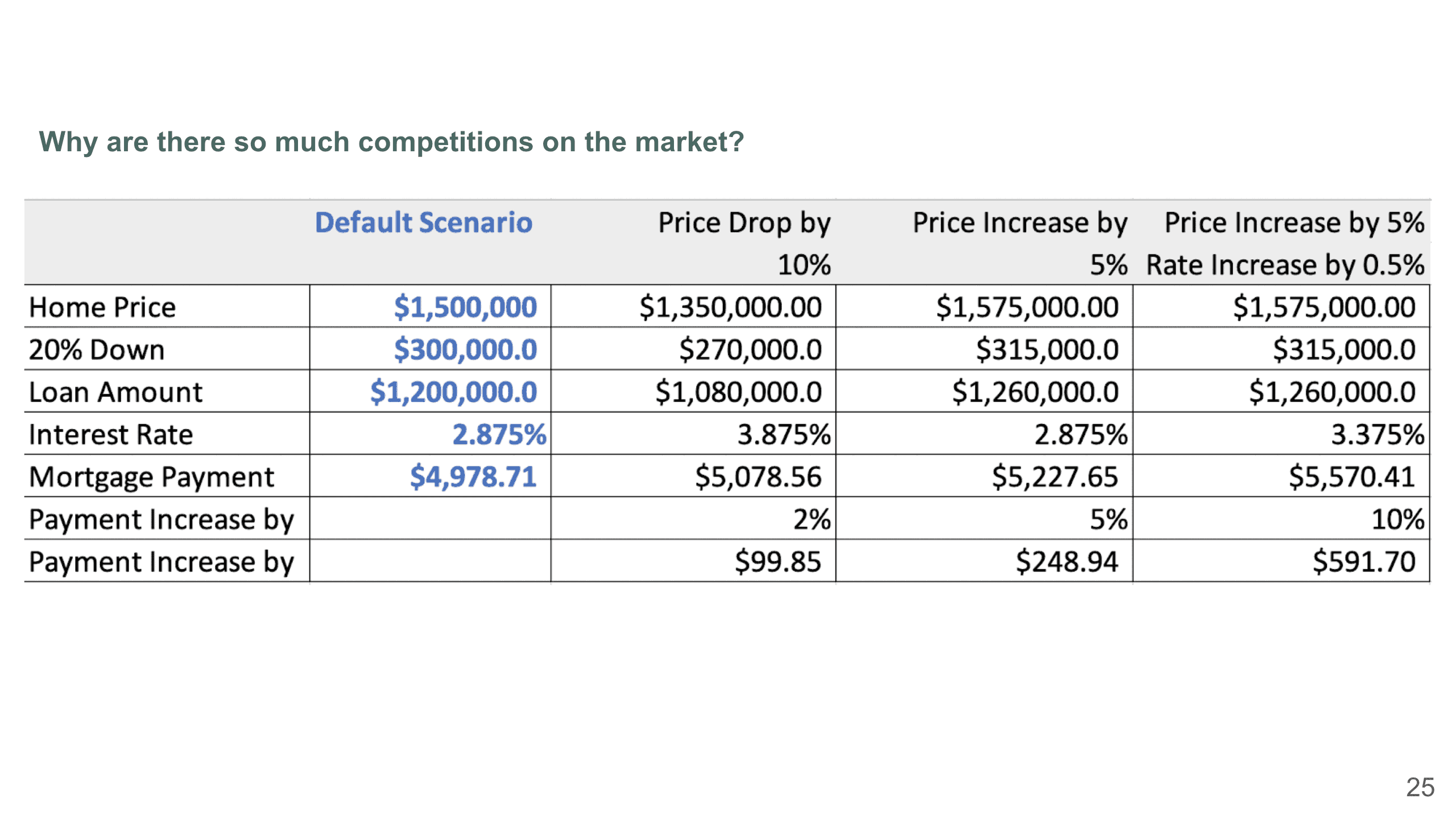

I really want to share this chart with you. Let’s do this as a default scenario – buying a 1.5 million dollar property in the Bay Area, 20% down, the loan amount is 1.2 million at a 2.875% rate. Your mortgage payments will be almost $5,000. Let’s say the housing price is going to drop by 10%, but don’t forget in 2019 the interest rate was right around 3.875% at that time, so it can go back up to that level easily, and at that time it was still a historical low. Then, your monthly payment actually will still go up slightly 2%, just because there’s a 1% increase in the monthly payment, despite a decrease in your purchase price. What about if you just wait around a little bit, and the price does increase. As you know, we saw that if you make an offer, they all go up by 10% increment or even 20%, and what will happen? The next round you get at a 1.575 million purchase price, then 20% down is $315,000. Even at the same interest rate, your monthly payment now has gone up 5% to about $5,227. Another scenario would be – Okay, I’m just going to continue to wait, and we just talked about that the pricing is probably going to continue to go up and let’s just say it went up 5% rate increased by just 0.5%, then your monthly mortgage payment will actually go up by 10%, which is $600. This is the reason why we see so much competition and why people are so aggressive, they just don’t want to wait until the price increases by 5% and the rate increases by 0.5%, that can make a big difference of $600 per month, and that’s almost $7,000 a year.

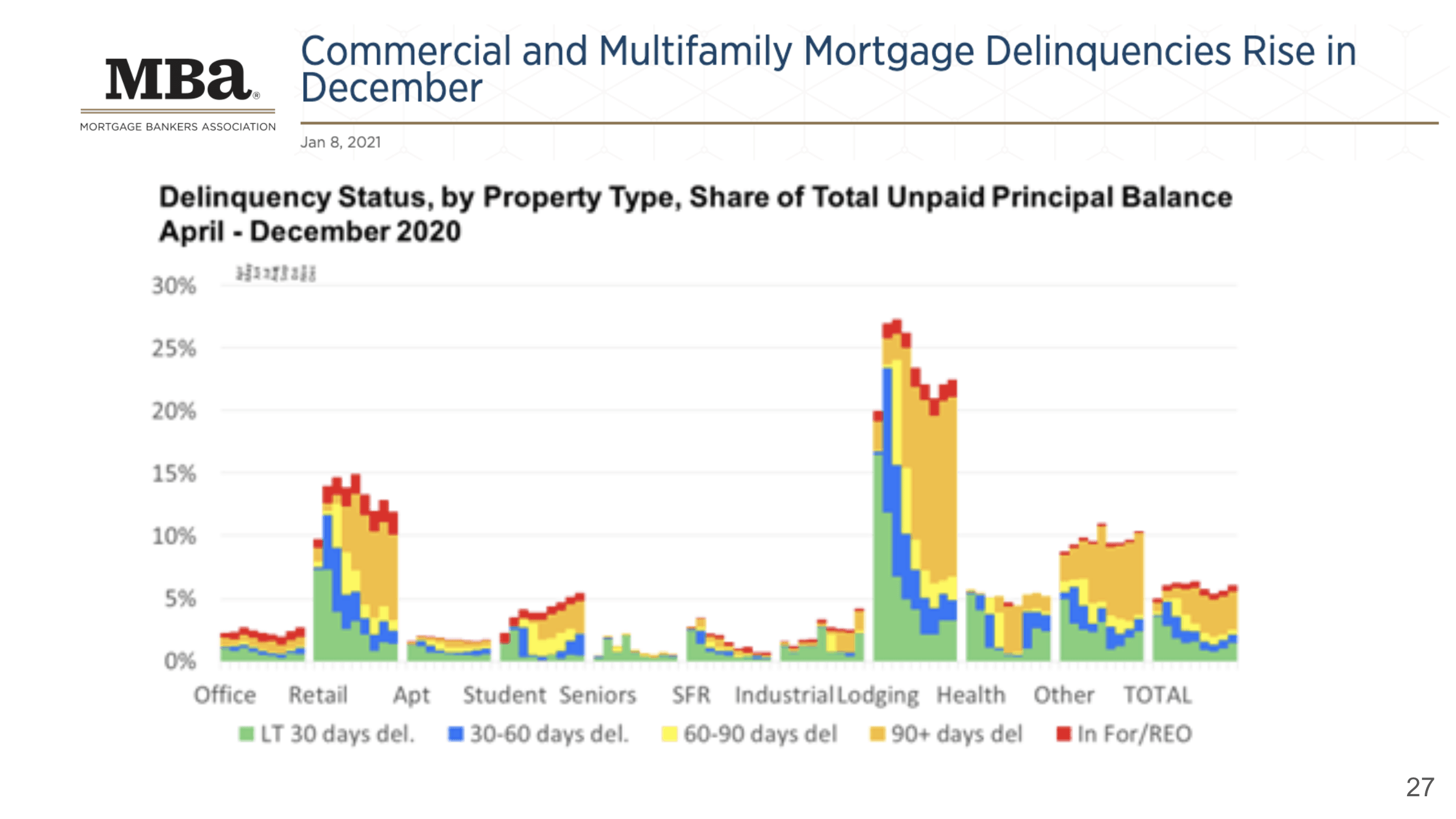

Alright, let’s take a look at multi-family market updates, and we have the commercial and multi-family mortgage delinquencies here. The good news is that we still have relatively low delinquency for apartments compared to hotels and retail.

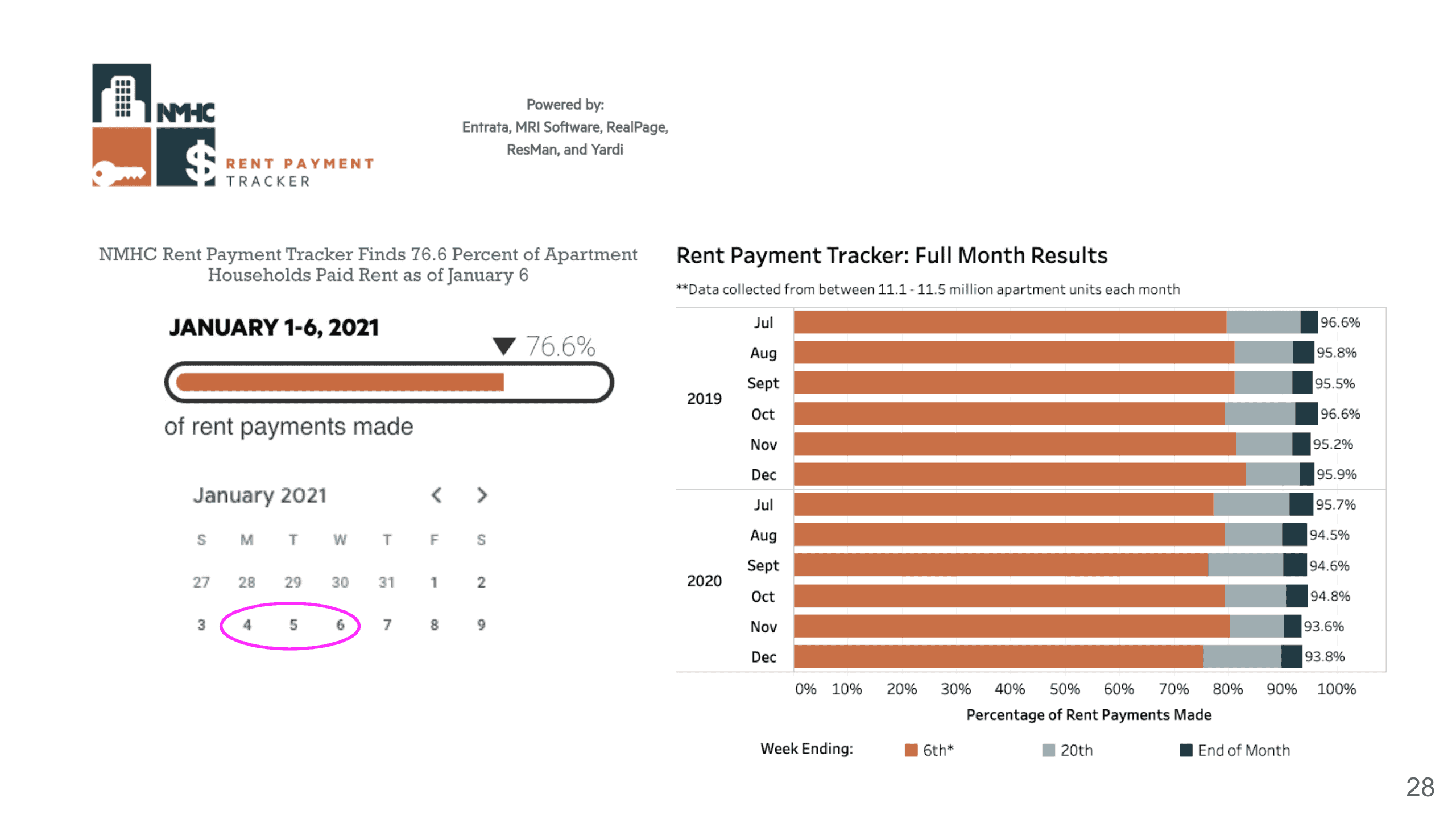

Also, this is the rent payment tracker from the National Multifamily Housing Council. In January, it is at 76.6% paid, but remember, there were only three weekdays before January 6th. Typically, if you look at the full month result, it’s actually all above 90%.

Marcus and Millichap had given some comments about different markets in the Bay Area. The vacancy in the Central Valley market is record low. The San Jose market is the market that everybody thinks will lead the comeback after the health crisis.

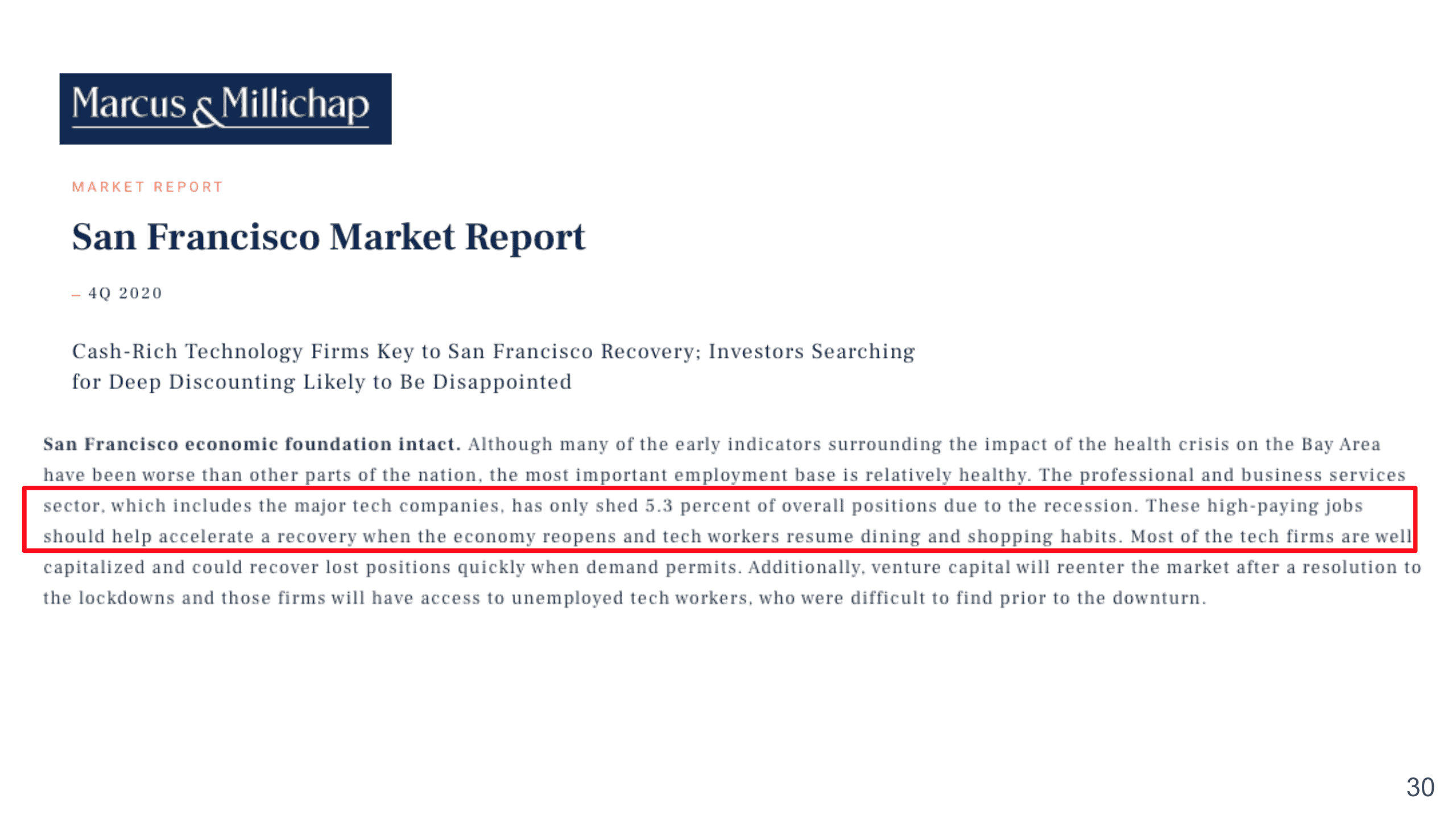

For the San Francisco market, they do believe that right now you probably can get some good deals, and even though some major tech companies have shed only 5.3% of overall positions due to recession, these high-paying jobs should help accelerate recovery when the economy reopens and tech workers resume dining and shopping habits.

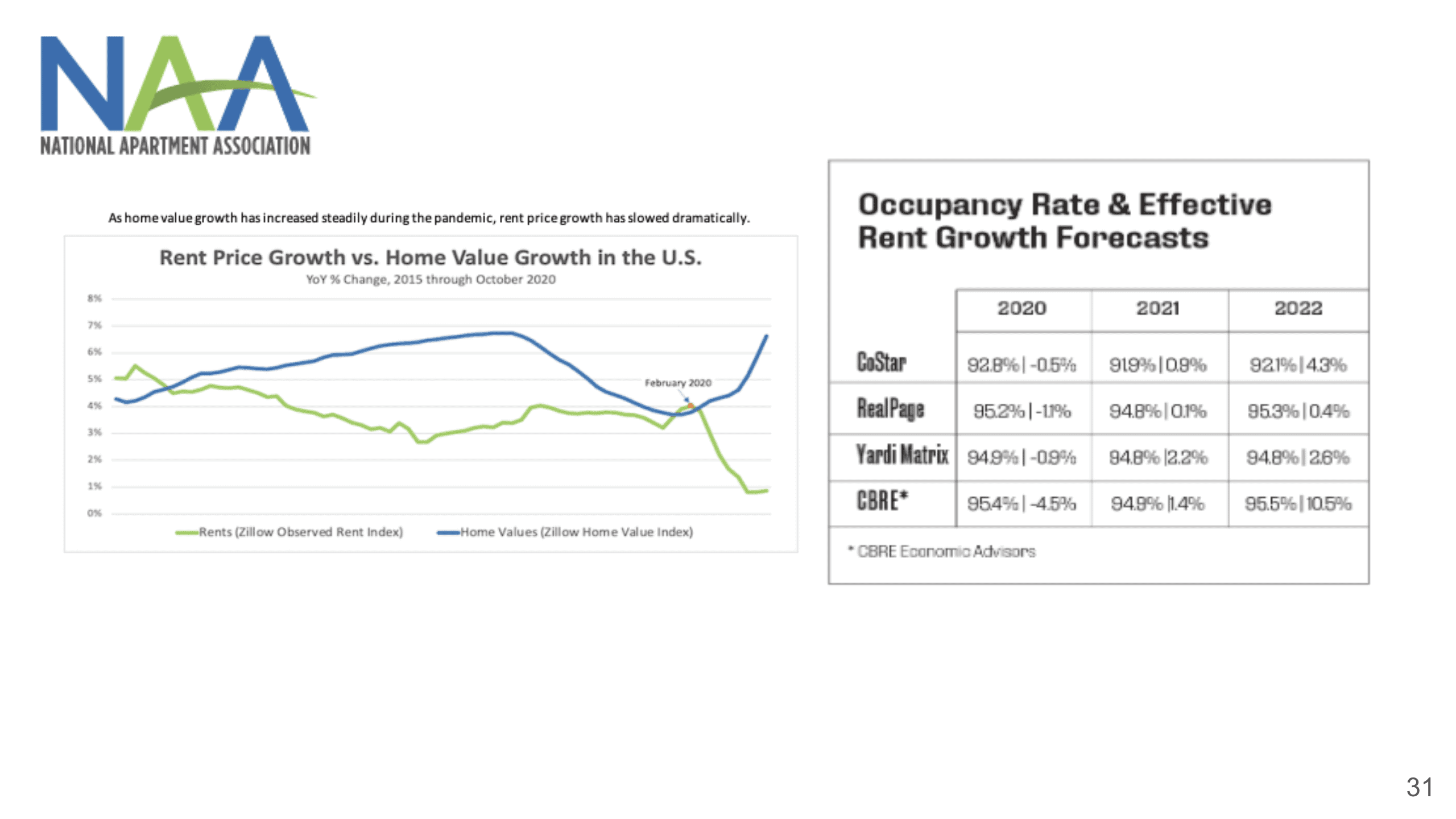

You’ll see home prices continue to go up, but rent prices have come down quite a bit. It has gone down in 2020, actually, they expect that it’s going to come back up, but a lot more conservatively.

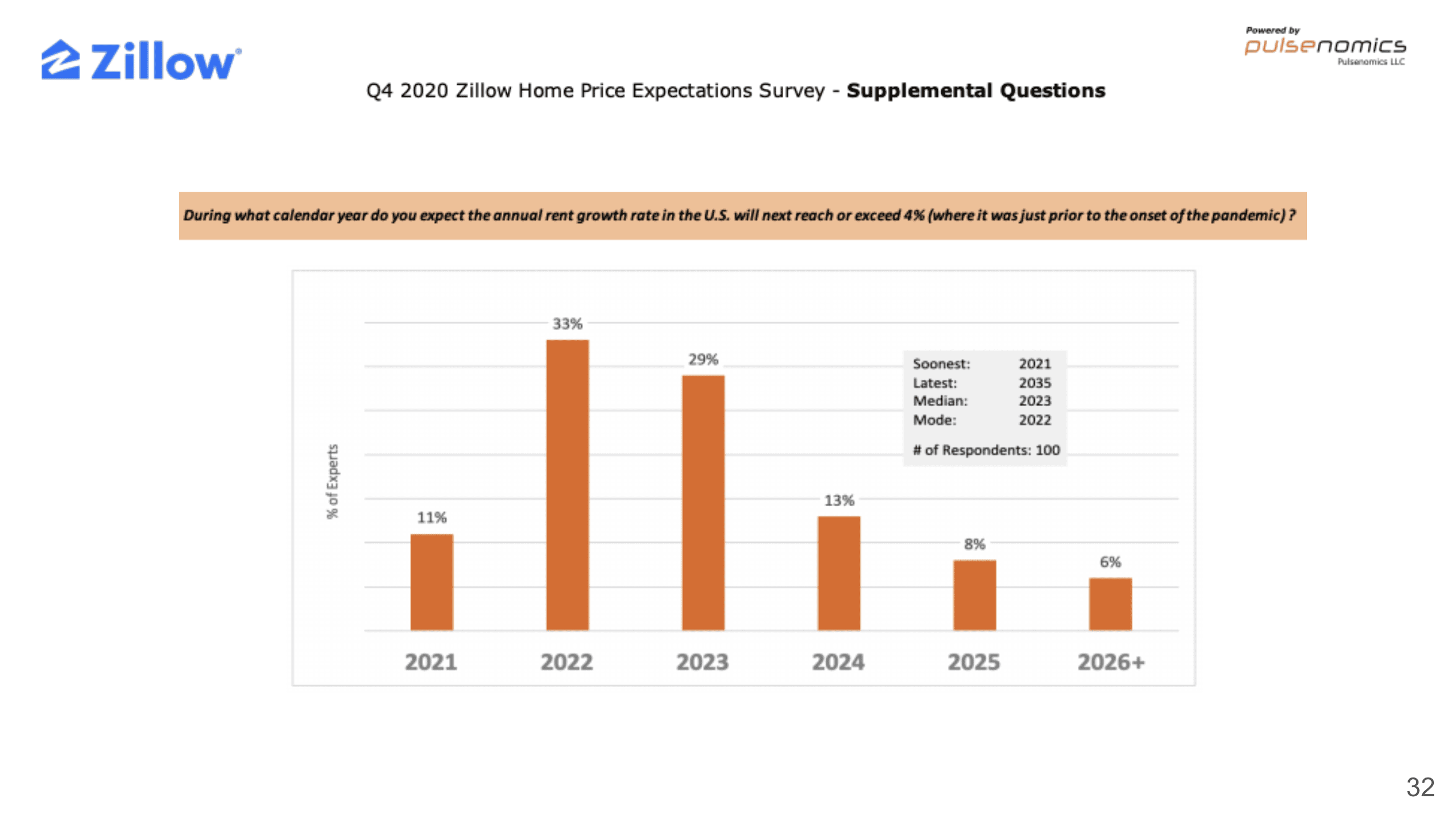

Here is another survey asking when people think that the rent price is going to come back to the normal 4% increase per year, and a lot of them believe that it will be 2022 to 2023 when the rent price is going to exceed the 4% mark.

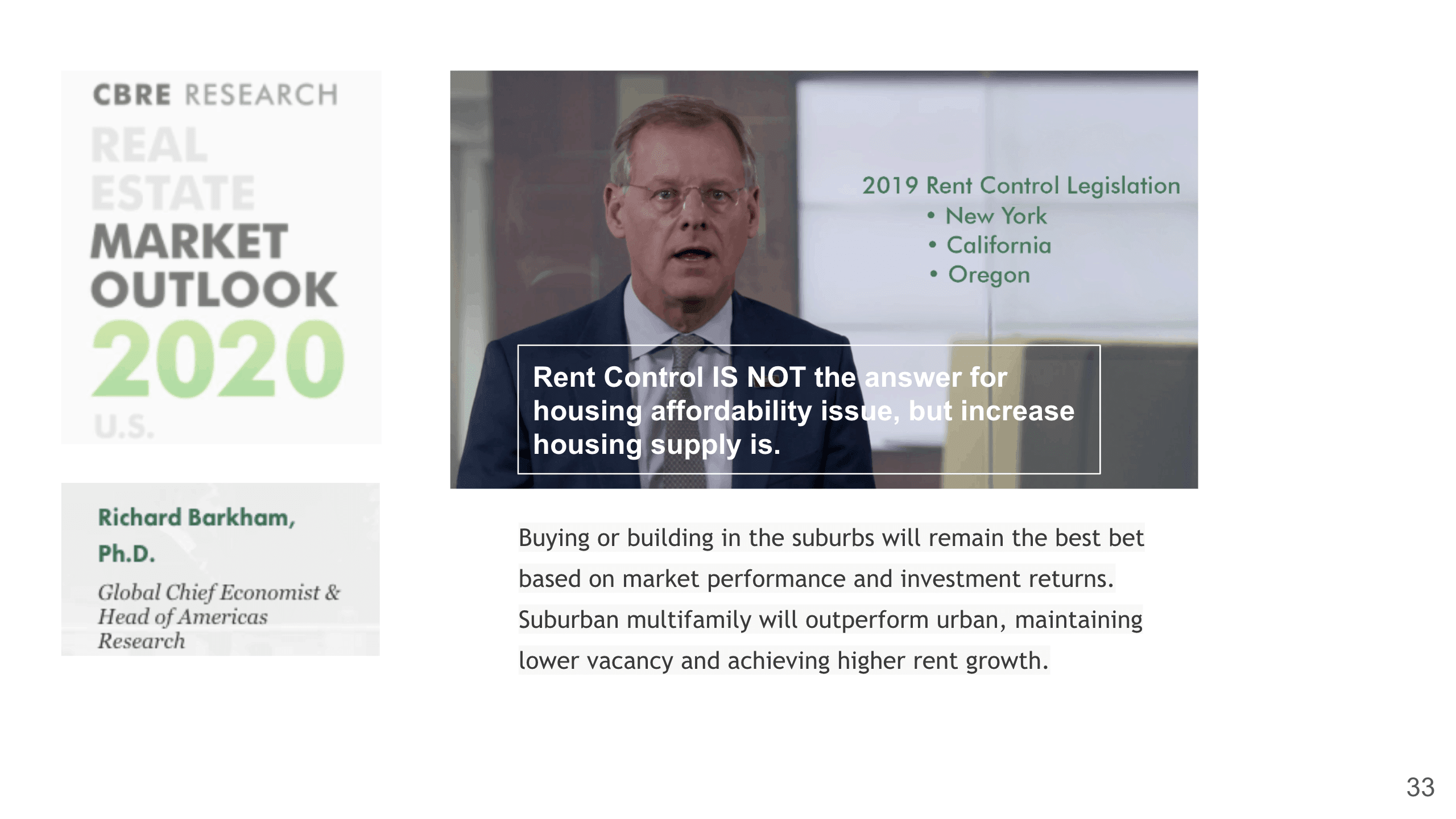

I think we talked a little bit about this regarding rent control. I truly believe that rent control is not the answer for housing affordability, it’s actually hurting. At the end of the day, it is really the housing supply. That’s why I hope that with those tech companies if they truly can commit billions of dollars to help solve this housing crisis here in California, that will be the best way to go.

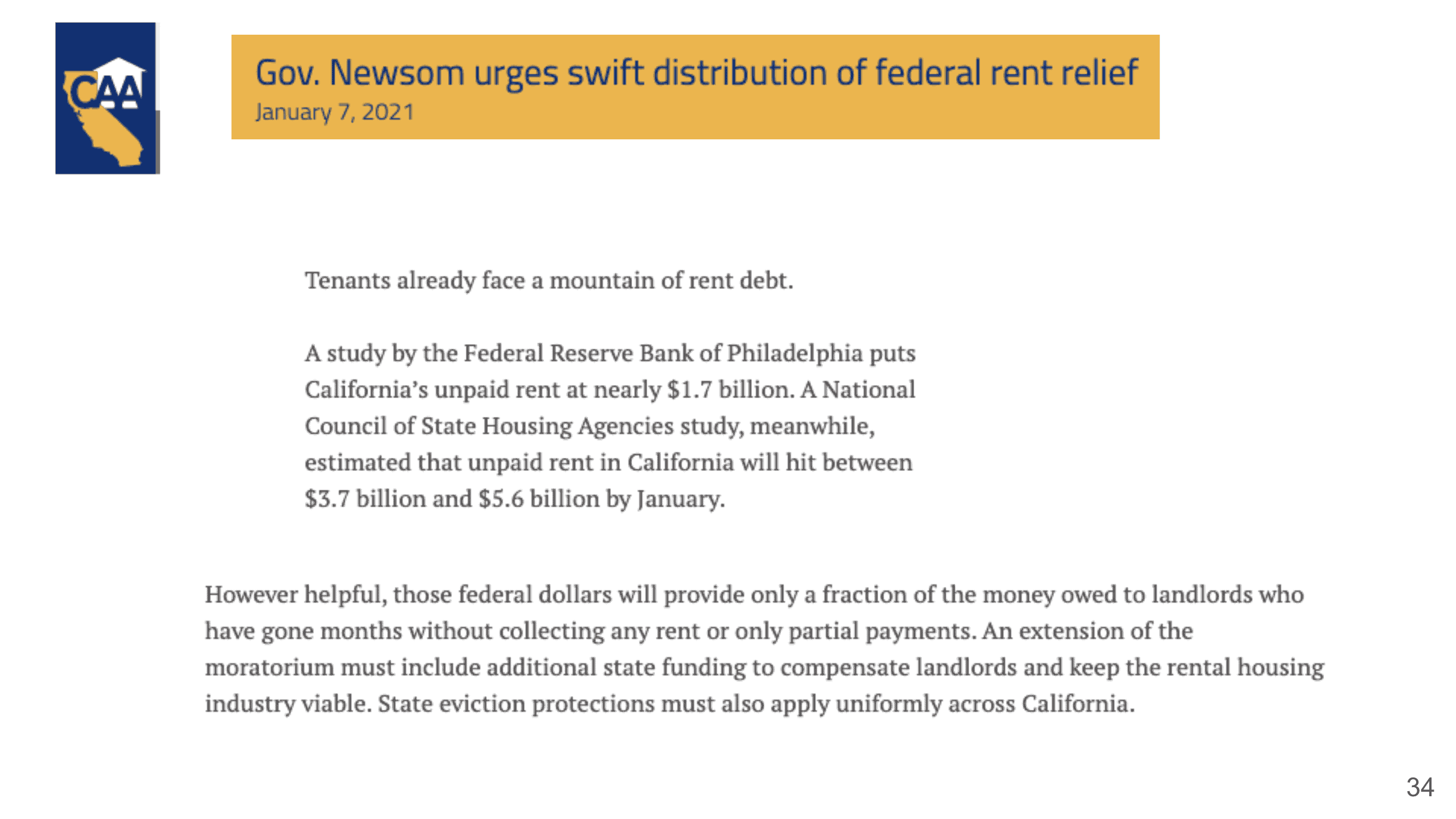

Here, as we know, we are getting this federal rent relief, and we just don’t really know where the money is going. We keep hearing that California might extend eviction moratorium, news after news about canceling rents, then what are we doing to help our landlords?

That’s why at today’s webinar, we have invited Joshua Howard, the executive vice president of the local public affairs for the California Apartment Association (CAA), to share the most updated policies and eviction moratorium status on the California Rental Housing Market. Watch the full recording here! If you have any questions or comments regarding the topic, feel free to get in touch with us!

Stay up to date on the latest real estate trends.

A Bay Area Realtor's approach to schools, neighborhoods, and long-term value for families making a move

Part 1 of HAYLEN's series on the 2026 CCIM Spring Forum in Philadelphia

You’ve got questions and we can’t wait to answer them.