2022 Housing Market Predictions – November Bay Area Housing Market Updates

Welcome everybody to our 25th episode of the Bay Area Housing Market Townhall. You can watch the video version of this episode here.

There is so much going on. I want to go over different county’s housing market conditions compared to last month; and since we are in November now, we probably want to know about the housing price prediction for next year, the Mortgage Rate Projections, and also, we have news talking about the inflation rate at 6.2%. How is it going to affect our mortgage rate? And also, the biggest news of the month – the Zillow iBuyer Flop! What are their fundamental mistakes during this whole iBUYER phenomenon? Also, what is the best value increase – which is the return on investment strategy? So, hopefully, today, you guys will be able to learn something from this webinar.

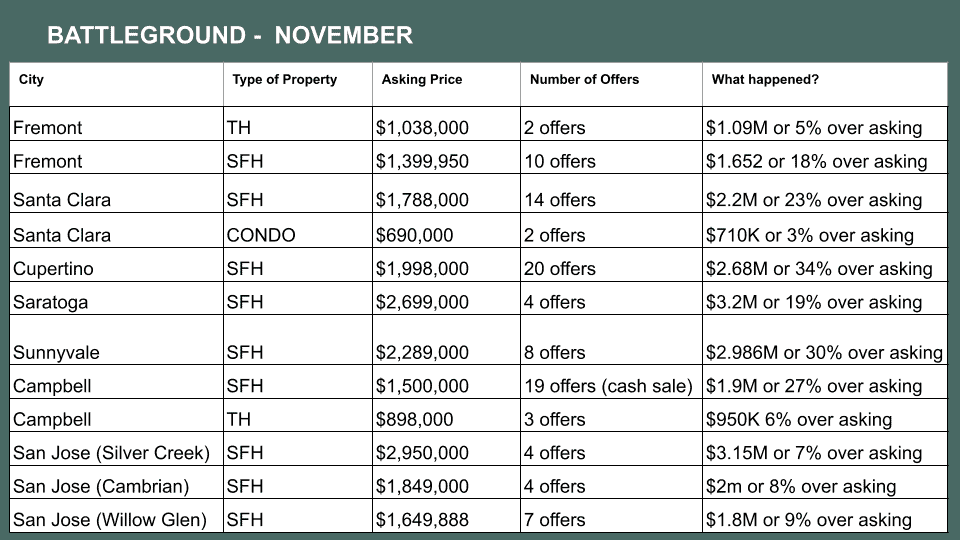

Let us take a look at what has been going on with all these offers. I know it is November. A lot of these are kind of like the October/November time frame as we talked about last time. The summer did slow down; but as soon as the school started, people came back. I remember last month when we showed a lot of single-digit offers. Now, this month you see there are a lot more double-digit offers, number of offers, and it has gone quite a bit over the asking price as well. No matter if it is East Bay or South Bay, single-family or townhome; but you do see that townhomes, condos, are not as popular still. The single-family are still really popular, especially the ones that are in a better school area, and they are still going over 18%-20% over the asking price.

There is definitely still a lot of competition out there. If you are in the market, I know it can get pretty frustrating, but just be patient, listen to your realtors advising you on the offer situation. When your realtors are making an offer, they need to have really good communication with the listing agent and One Tip – really important! and I think a lot of buyers agents don’t realize how important this is! As a listing agent, one thing they want to look at is a very well-written offer – meaning your contract should be written correctly, shouldn’t have a lot of mistakes because when you have a lot of mistakes that means that the listing agent will have to counter you on all the terms and also, they want to know that you have reviewed all the disclosures and also all the inspection reports. It would be very well worth it if everything is signed upfront and I know because every time you make an offer, it is going to be writing, I do not know, 5, 6, or 7 offers and you don’t want to be signing all these disclosure packages every single time; but be prepared if you are close to the winning bid, you should have all those signed upfront. Having a good relationship with the listing agent can make a big difference. Also, communication is really important. We have a buyer’s agent just submit the offer without saying anything, without explaining anything, and have a really bad written offer, even they are, maybe the top three, we would much rather work with another agent who really knows what they are doing and negotiate with them instead and see if we can get a better price from their buyers. So, just make sure that if you are making an offer for your buyers or if you are working with a realtor, make sure the offer is written correctly and accurately.

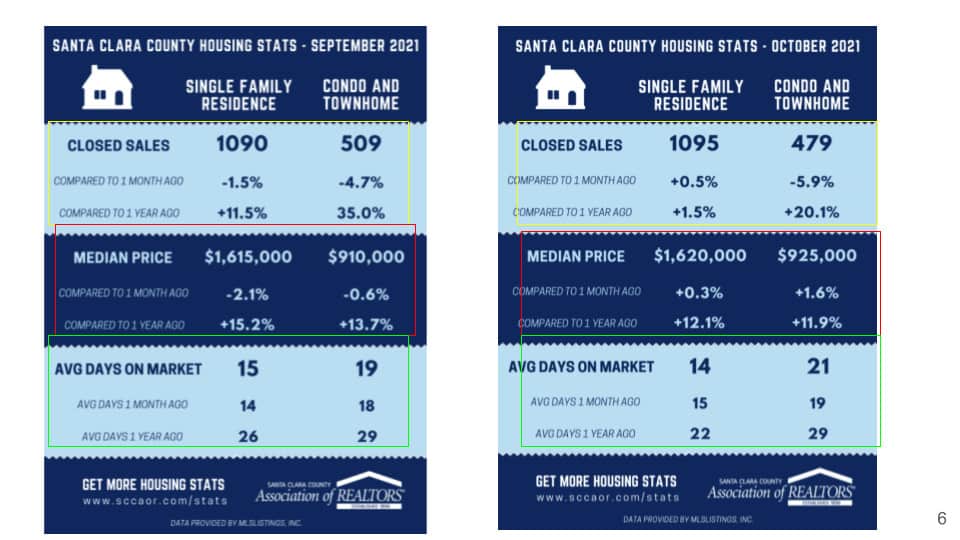

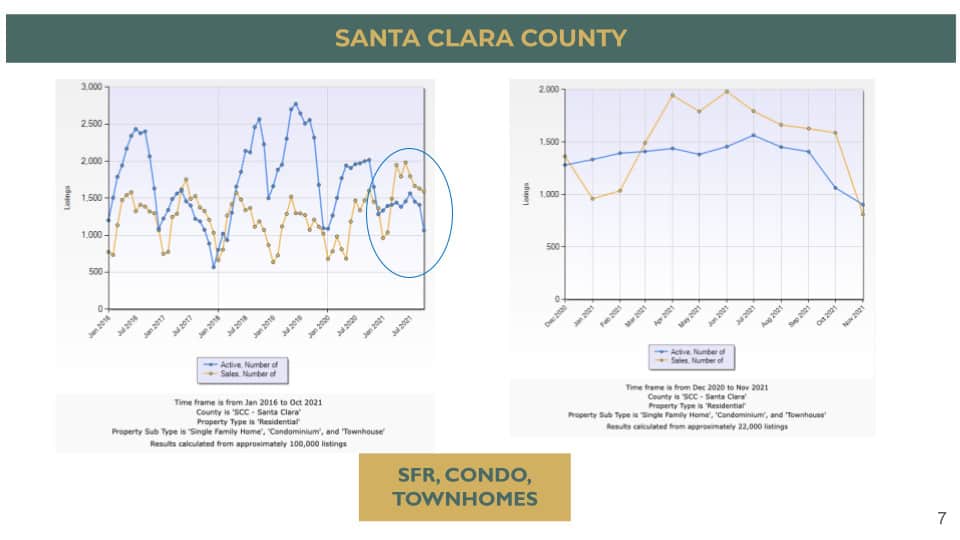

What is going on in Santa Clara County? Now, in Santa Clara County, we look at the October and September numbers. We have slightly more, pretty much the same, 5 units more, for this month; and then, condo and townhome has a little bit less compared to single-family. But then, compared to a year ago, we did have a little bit more and especially for condo and townhomes, and in terms of the median price, though is still going up and is still double-digit from last year, for both single-family and also condo and townhome. But then, compared to a month ago, it didn’t have too big of a difference, but the average days on the market are also pretty consistent as well compared to last month. It is staying at about 2 weeks’ time for the single-family and 3 weeks for the condos.

Now, in terms of the price here, for Santa Clara County, as we see that this is a chart where we show the number of sales versus the number of active listings. If you look back in 2016 and throughout, most of the time we have more active listings, right? But look at what happened. This is, I think, one question that so many people always ask: why does the price keep going up so much when it’s already so expensive? and we kept talking about, it is the supply, it is the supply. Well! There are 2 things; supply and also interest rate. So, this supply, as you see, the number of active versus the number of sales, they are a lot more. Whatever comes on the market is pretty much sold. So, that’s why we noticed that the price had been going up so much.

If we just stretch this out. If we compare and see, now from 2020 to this month, November 2021, what do you see is that the number of cells went down a little bit and it looks like it is starting to go back up. So, we know that the activity is starting to slow down actually in November, and you can ask a lot of realtors out there and we definitely see a number of buyers are slowing down.

A lot of our buyers are talking about what they want to buy next year. Just want to remind you guys that during the wintertime, right now, it is a good time to buy because you have less competition. I cannot tell you how many times we remind our clients to look for properties during this time, in the wintertime – fourth quarter, because there are so many fewer people competing with you. Now is a really good time, during the holidays, as long as you are not traveling. So, hopefully, you can take advantage of this holiday season and go out and find the perfect home for you.

What about San Mateo County? If you look at San Mateo County, the single-family pricing also has gone up, from 1.88 to 1.91 this month compared to last month; and it actually came down slightly, it is two days less on the market, and we have fewer sales, slightly fewer sales, compared to last month. As for the condo and townhomes, the prices actually have come down a little bit by 3.24%, stayed on the market pretty much the same, just one day difference, and also have an almost very similar number of units sold. But then, if you look at August, September, and compared to August, we had much less, like 15% less compared to August.

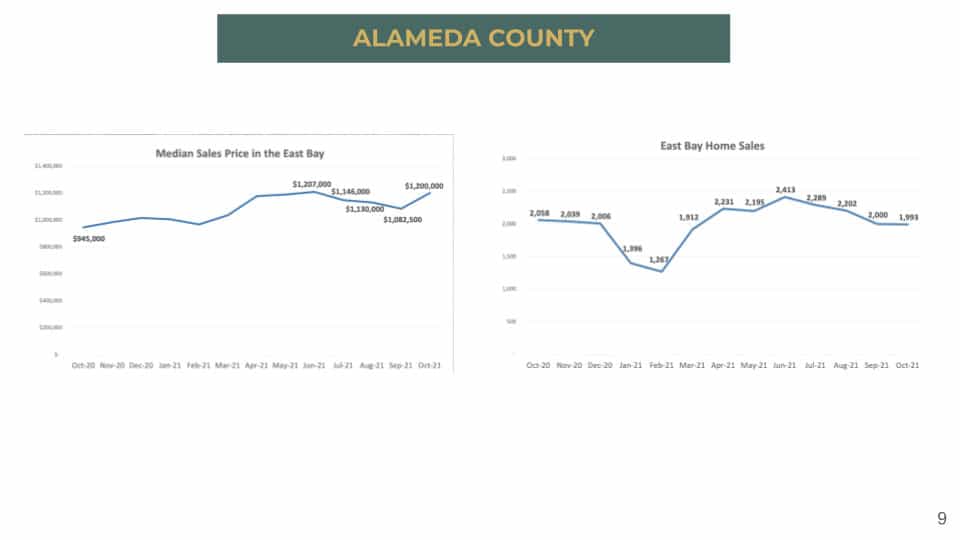

In terms of Alameda County, the pricing had gone up quite a bit in October. Let’s go back to the Summer. It is summertime – Again, I think we talked about this over and over again is that the misconception about summertime is very hot, you can get a really good price. I mean for the seller during the summer, but actually, summertime is a slower season of the year, the second slower season after the fourth quarter in November and December. So, as you see here, the price has gone down a little bit; but then as soon as the school started, the price had gone up again.

In terms of the number of units sold, it was quite a bit and then, it has gone down a little bit compared to the summertime.

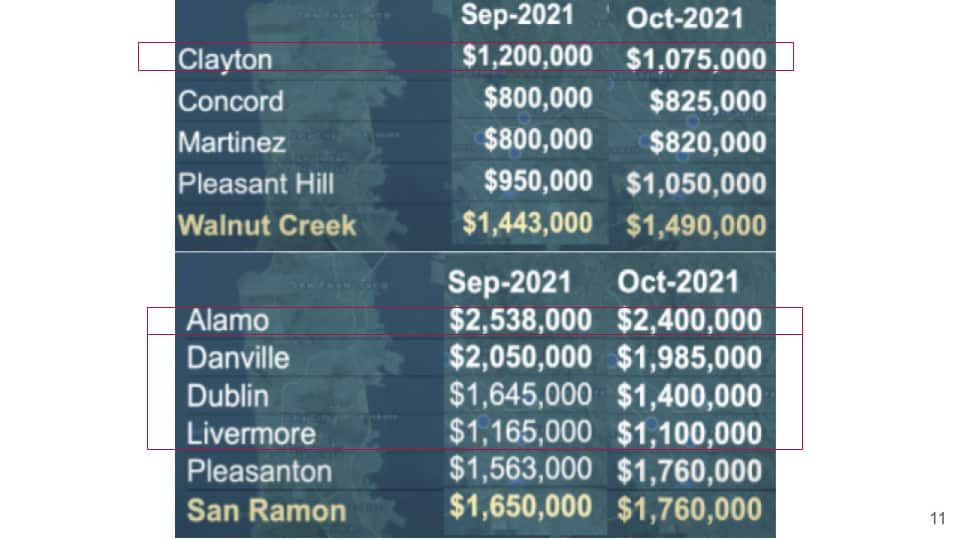

If we look at the cities in Alameda County, you will see that there are just a handful of some of the cities that had gone down in pricing compared to last month. So, it’s the City of Alameda came down by 15,000, Hayward came down by about $22,000, and San Leandro, San Lorenzo, and Union City also came down slightly as well compared to last month.

As for these other cities, Clayton, Alamo, Denville, Dublin, and Livermore; they also had come down on their median sales price; but all the other ones, pretty much everyone else, had gone up in pricing compared to last month still and especially if you look at Pleasanton, it has gone up almost $200,000 compared to September.

Because we just lift the travel restrictions, we started to see and hear a lot more foreign buyers coming to ask about buying properties again over here and CNBC also reported that “Real-estate brokers brace for ’flood’ of wealthy buyers from overseas as travel restrictions lift.” Just to let you guys know from first-hand experiences that we definitely starting to hear more foreign buyers asking about buying properties here.

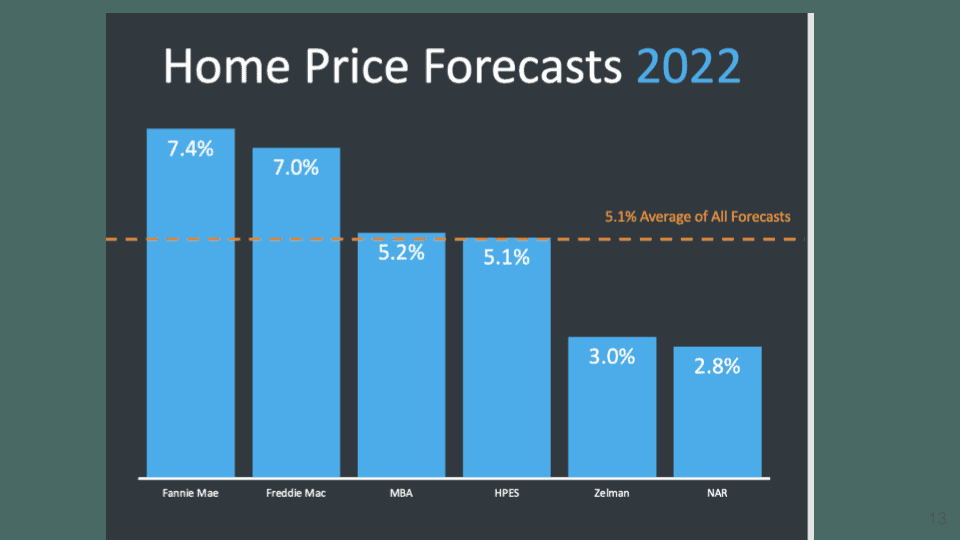

With that said, if you want to know about the home pricing forecast, in 2021 as you see that Fannie Mae, National Association Realtors, Freddie Mac, Zelman, and Mortgage Bankers Association, all had predicted 2021 home prices is going to go up in double-digits which we have seen just now from the previous charts. They are pretty accurate about that.

Now, what about 2022, this is their forecast: Fannie Mae at 7.4%, Freddie Mac is 7%, Mortgage Bankers Association of 5.2% and HPES at 5.1%, Zelman at 3%, and NAR at 2.8%. Although they are much more conservative compared to their last year’s forecast of 2021 number, it is still going up, so they are all expecting the pricing is going to go up still, for 2022. I know a lot of people have been talking about again market crash and because of a lot of different scenarios, they worry about foreclosures. They worry because the price has gone up so much, there is no way it is sustainable, but most of the organizations are still predicting that the pricing is going to go up. One of the main reasons, of course, is because of the inflation as well, the supply is still low, and also about the mortgage rates.

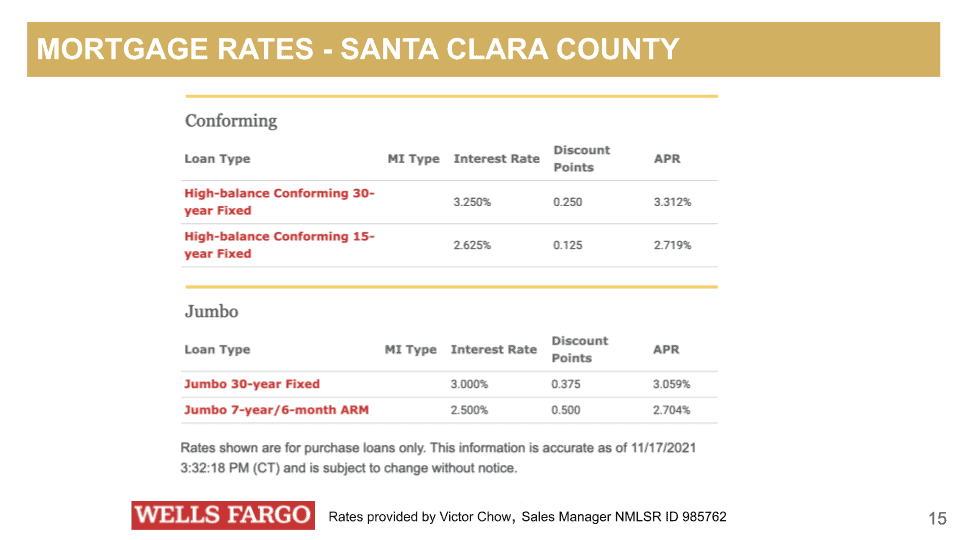

Now, of course, then, we need to talk about mortgage rates and where are they heading? Currently, just got these rates today from Victor Chow at Wells Fargo. He has shared that the High-balance Conforming 30-year Fixed today is at 3.25 and the Jumbo loan 30-year Fixed at 3% with a Discount Points of 0.375. As you can see, there is an APR as well. I just kind of wanted, in case, there is some audience here who do not know what is the difference between interest rate and APR? Why is there a difference? We always want to remind our clients that when you look at the mortgage rate, you also need to know about the APR, because the APR actually included some of the closing costs for this interest rate. So, APR actually includes the fees that you are paying for that particular interest rate. If there is a big discrepancy in instead, for example, if someone else quoted you at 2.95 but that the APR is at 3.2, you are actually paying a lot more fees to get that 2.95% interest rate. So, be sure when you ask for the mortgage rate with any of your lenders, and be sure to ask about the APR as well.

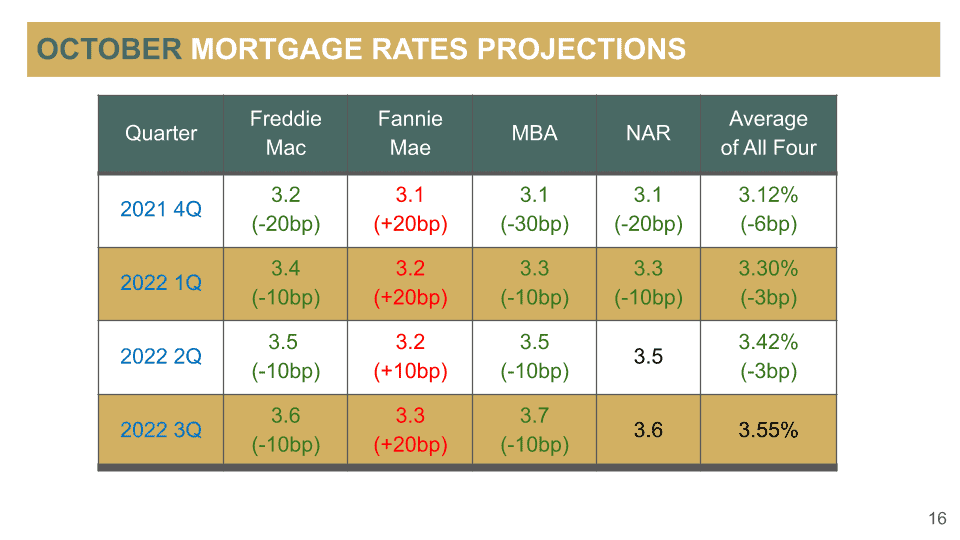

Now, we want to know where the rates are going to go, and they adjusted their prediction. However, the good news is that most of them, now, are quite consistent with each other. Last month, we saw Fannie Mae was a lot lower with their projections; but then this month, they have adjusted. Now, everybody is kind of on the same page. As you see for 2021 4Q, Freddie Mac is projecting 3.2% and Fannie Mae adjusted their projections to 3.1%, Mortgage Bankers Association 3.1%, and NAR is 3.1%; but also for 1Q, 2Q, and 3Q in 2022, you see the trend that they are all like kind of trending up to about a mid 3s and around that range, so just understanding that, I know, some of you might say that you want to wait, you can have to also adjust with, one is that the property price is going to go up and also the mortgage rate might be adjusting up as well.

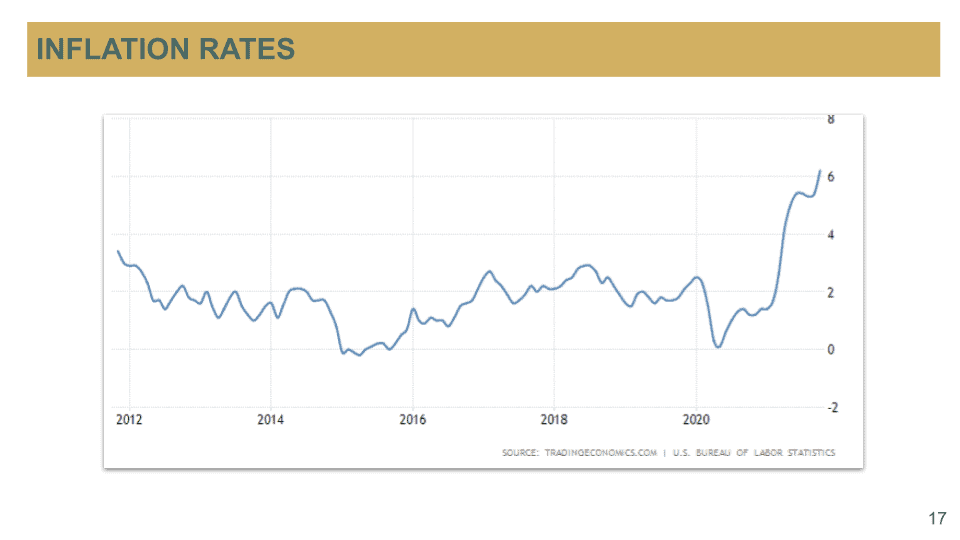

There is somewhat of a correlation between inflation rates and mortgage rates. Now, because the inflation rate that you see and you probably heard from the news is that the inflation rate has gone up to 6.2% right now and as you see that this is the highest, I think in the last 30 years. So, it is definitely something that we need to watch for, and we definitely see our gas pumps. I do not know about you guys but the other day I was trying to pump gas and I think it was over $5 for me to pump the premium gas and it was pretty darn expensive. I have never seen that before. We definitely see a lot of cost of consumer products have gone up quite a bit and then also, I do not know if you guys have already prepared for your Christmas gifts shopping; but this is a time that you probably want to start ordering your gifts.

Now, how does this inflation is going to affect the mortgage rates? Because of the Inflation pickup, Fed is more likely to raise the Fed Rates next year and because they need to slow it down a little bit and because the Fed will likely raise the interest by the middle of next year. When the Fed increases its interest rates, typically banks will do too, so when that happens, then, you will start seeing mortgage rates go up for the borrowers.

The projections for these agencies are all pretty moderate, right now; but as soon as the Fed adjusts their rates, it is very well that they might also adjust their mortgage rates projections as well.

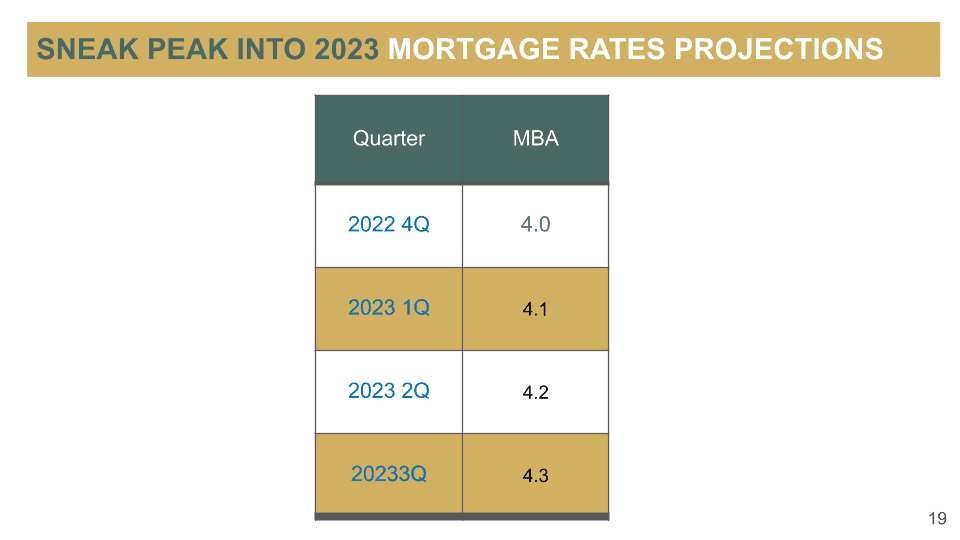

Mortgage Bankers Association – they are the only one right now that has projected all the way to 2023 3Q and 2023 3Q, they have projected up to 4.3, so it looks like they are still thinking that in 2023, it is going to be in the 4 range. Historically, it is still pretty low because I remember when I first started in real estate, it was at 6%-7% at that time, so 4% is still really low; however, it is going to be a lot more expensive. It is almost over 1% more expensive compared to this year.

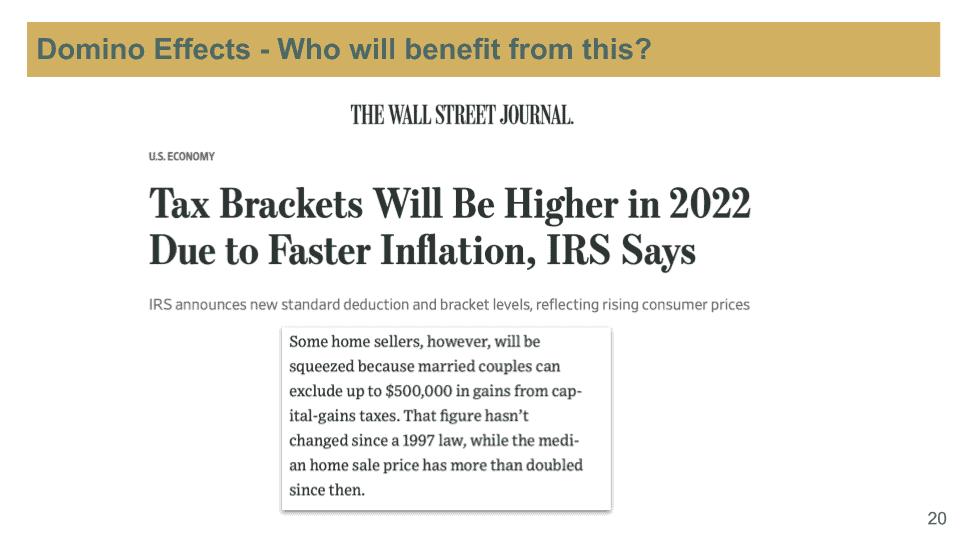

With the inflation going up and there is a domino effect, now because of that tax brackets are going to be higher in 2022, we can have a completely separate topic about this; how this inflation is going to affect our taxes? But one thing is that looks like it is going have a better, of course, effect for a lot of people because your tax brackets going up, and also some of the deductions will get to go up as well.

However, if you are a home seller, you are kind of squeezed because married couples can exclude up to $500,000 in capital gains taxes but that figure has not changed since 1997 law, while the median home prices have more than doubled since then. So, if your property has increased value for over $500,000 and anything over that, you are subject to capital gain tax. In that case some of the home sellers, one is that if they can refinance into a lower rate, then why would they want to buy another property that is a lot more expensive and on top of that, they will have to pay for the capital gain tax, so this is another reason why we are seeing such tight housing supply because a lot of sellers are just not willing to sell their properties.

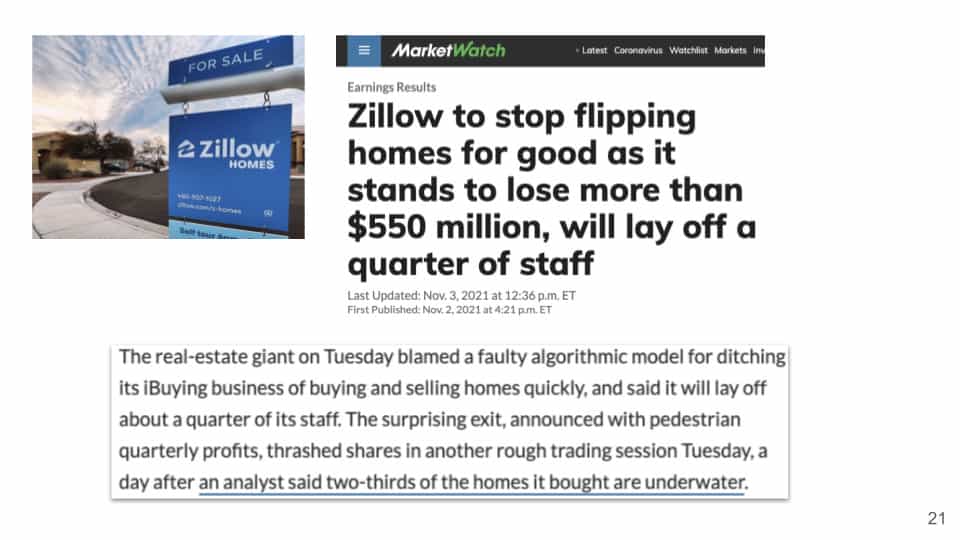

Are you guys ready to talk about Zillow? Now, this has been a really, really popular conversation in the last few weeks when the Zillow CEO came out and announced that they are going to halt iBuyer program that they had. They were really proud of it. They were talking about how easy they are going to make this home buying process. They are going to use their valuation model to purchase a home, but then they realized that they are going to lose a ton of money and on top of that, this is really unfortunate because of their decision making, they are going to be laying off 25% of their staff, so a lot of people are going to be out of work.

Now, one of the main reasons why this whole program flop is because that they blame a faulty algorithmic model for ditching its iBuyer business of buying and selling homes quickly and the surprising exit announced with pedestrian quarterly profits, threshed shares another rough trading session Tuesday, a day after an analyst said two-thirds of the home it bought are underwater. So, to understand why this did not work out is mostly because of valuation. It does not matter if you are Zillow or if you are a home buyer or if you are an investor, a flipper, evaluating a property is probably the most important thing.

Now, when you’re buying for your own primary residence that you plan on living for a long time for 10 years, there is a reason why you want to buy that home because it is for your home. I always say that home to a person for you to live in is not just a structure that you are buying, you are really buying to build memories. This is for security and for your family to grow in and give you a sense of security, give your family a place where you can always remember; however, there are a lot of investors or companies who buy and they want to flip and if they don’t do their evaluation correctly, they can make a huge mistake, especially for flippers.

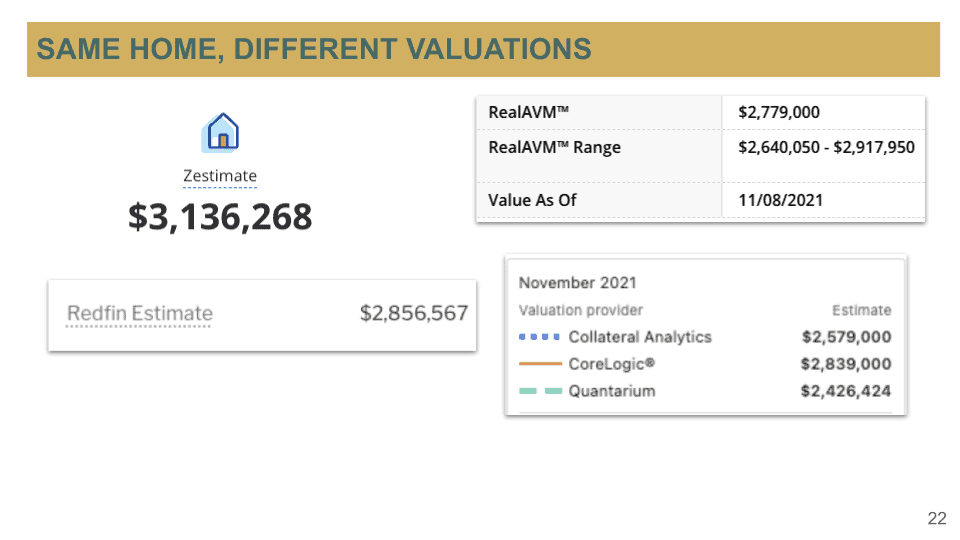

Just to give you an example. I used the same home, same address, and I put it into different websites to look at their evaluation. This estimate, which is from Zillow, they estimate at 3.1, over $3.1 million. I go to Redfin, it says 2.856 that’s almost a $200,000 difference, and that $200,000 difference can make or break an investor if they plan on flipping this property which is what Zillow was doing. And I will try another valuation model and now, for them, it is 2.779 and 3 more valuation models. We went from 2.4 to 2.839, so which one is correct? It is really hard.

I hope you enjoyed this session and please be sure to subscribe to our YouTube Channel, so you will get notified once the next episode is available. Finally, if you have any questions, please feel free to reach out to us, we are happy to assist you in any real estate needs.

Stay up to date on the latest real estate trends.

You’ve got questions and we can’t wait to answer them.