How Supply Chain Blockage Could Affect Real Estate Prices – October Housing Market Update

Welcome everybody to our Bay Area Housing Market Townhall. Today, we will go over Bay Area housing inventory and market trends, looking at the mortgage rate trends, and your purchasing power. We’re now 18 months into this COVID pandemic, so let’s look at the economic side effects of this pandemic. Also, we have the eviction moratorium that’s expired in California. So what kind of renters protection programs are still out there? Then, of course, we have to talk about multifamily investments, rental rates, cap rates, and trends. Watch the video version here.

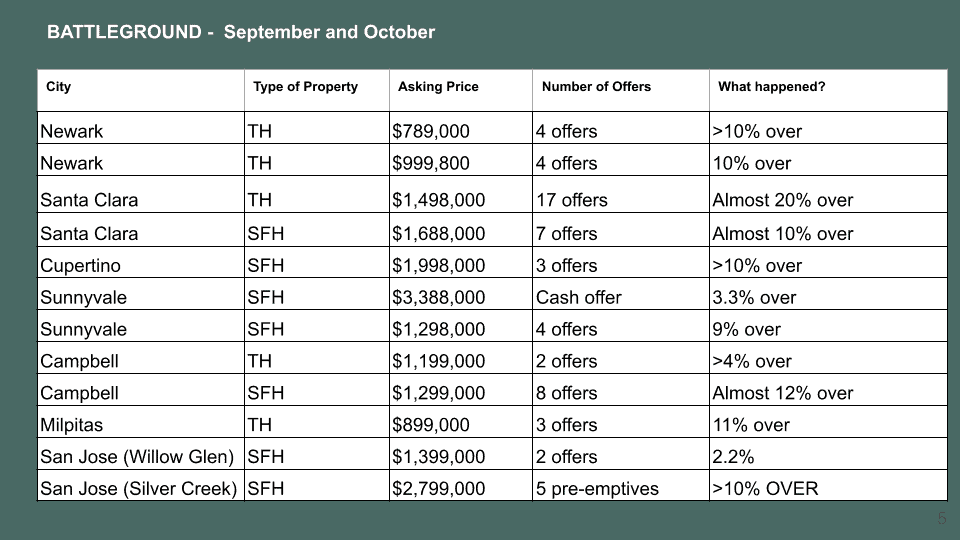

As always, we want to show you what’s been going on. We’ve talked about the summer being a little slower and then in September, a lot of kids have gone back to school, the markets typically come back a little bit. If you look at Newark, the townhouses still have multiple offers. Pretty much everyone has multiple offers and everything has sold over the asking price. In Newark, which is in the East Bay Area, four offers still got about 10% over the asking price. The ones that were asking $999,000, $800,000 had gone over a million-dollar.

In Santa Clara, Cupertino, and Sunnyvale, they’re still really hot. Cash offers have gone over 10 to 20%. As you see, a lot of these offers were about 10% over, besides the cash offer for a close to $3.4 million property. It went only about 3.3% over.

Then in Campbell, the price point is slightly lower at $1.2, $1.3 million. For single-family, $1.3 million is hard to find in Campbell. That’s why they got eight offers and it went about 12% over the asking price and the townhouse went about 4% over the asking price. In Milpitas, there are three offers for this townhouse and it went 11% over. Then the San Jose Willow Glen, which is more on the west side, and the Silver Creek more on the southeast side, even these high price point properties, before the offer deadline, got five preemptive offers and still went 10% over the asking price.

I just wanted to show you how competitive it is still out there. Although if you go back to a couple of months before, around the April-May timeframe, you’ll see the number of offers, a lot of them were double digits. Over here is a little bit more of single-digits, less than 10 offers besides the one in Santa Clara. That would give you a little bit of good reference when it’s your turn to make offers.

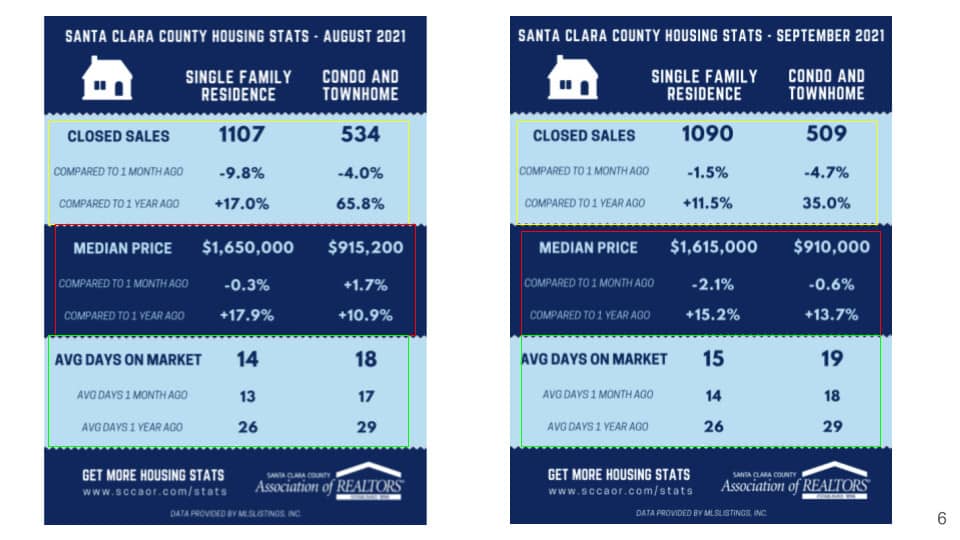

Let’s look at Santa Clara County housing stats. Let’s compare August and September. In August as you see, for single-family closed sales, we went down a little bit compared to a month ago. And if you look at last month, it also went down from July. So we’ve been going down in terms of the number of close sales, but it’s still up about 11.5%. The same thing for condos has continued to go down since July. We are down another 4.7%, But it’s 35% more than a year ago.

In terms of the median price in Santa Clara County, it’s $1.65 million. It did come down a little bit from 2.1% last month to 1.615%. Also, the condo townhomes came down to $910,000. But again, both of the prices have gone up double digits since last year.

Then let’s look at the days on the market. The days on market have gone up a little bit from last month. As you can see from July, it was about 13 days, August was 14, and now September is 15 days. So you see the market has slowed down a little bit. And it’s pretty normal as we see that towards the end of the year that days on the market go up slightly.

The same thing for the condo and townhome market but it still has gone down quite significantly compared to the exact time frame from last year.

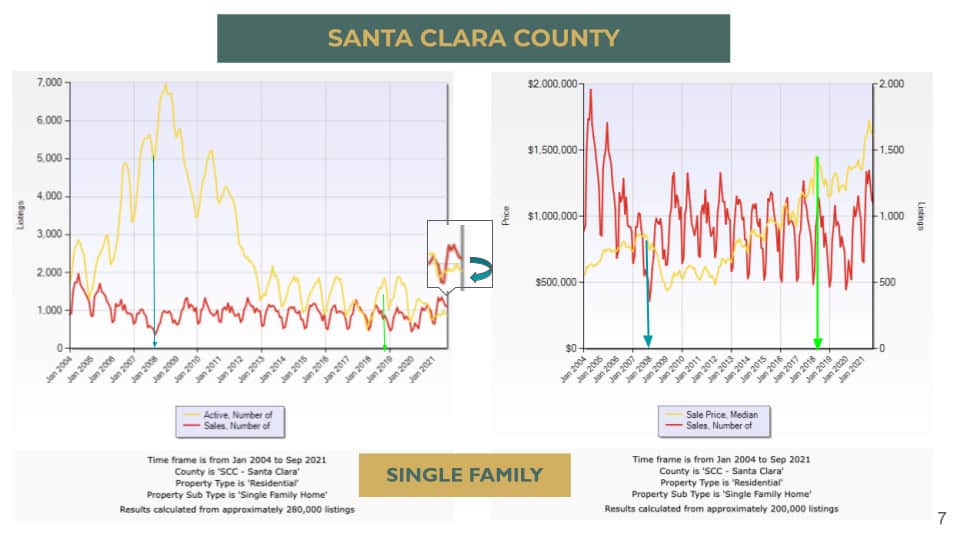

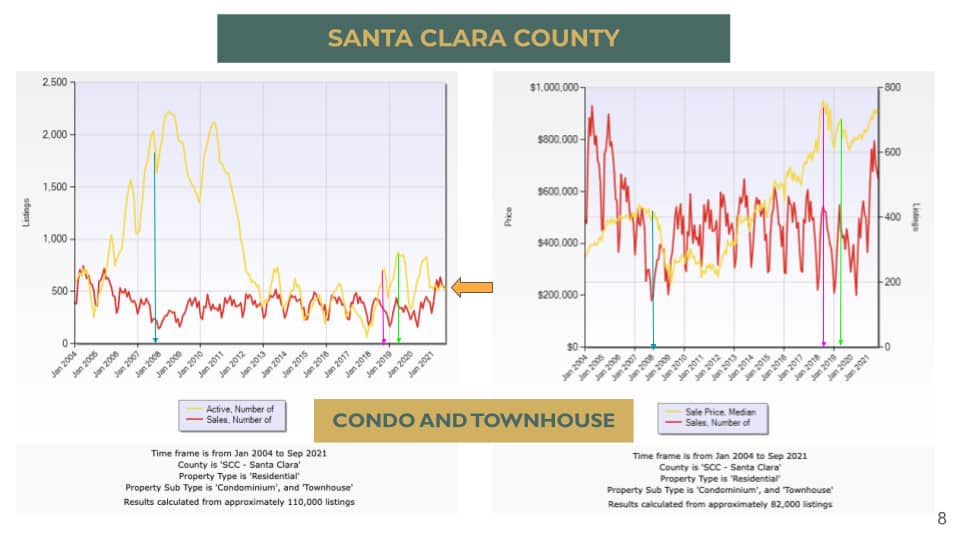

Now, I thought of sharing these charts with you guys. This is quite interesting. If I pull all the data, the number of active sales and the number sold since 2004, as you can see the inventory, the yellow line, has fluctuated quite a bit. But then, the number of sales has stayed pretty consistent.

So, we can see this large inventory here, honestly, at that time, between 2007 to 2011/2012, that time, I would say that 90% of even my sales at the time were all short sell or foreclosure. There was that much inventory on the market. And then, of course, it has dropped quite a bit since then. Now what’s interesting is that you’ll see it has gone down quite a bit. The inventory now is like less than 1,000 listings in Santa Clara County. Before, we had as many as 7,000 listings.

Now, in this other chart that we’re looking at, we still have the number of sales, but it’s the same pattern as these red lines right here. However, we are comparing now the median sales price here. As you see, this is where the price started to drop quite significantly. If you look at this chart, comparing the same period, in this chart, you see these huge differences between the number of active listings and the number sold.

The same thing if you look at another point which is around 2018 to 2019, you see that the price has gone down. The same thing there is quite a bit of difference between the number of active listings and the number of sold listings. But more interestingly is that as of September 30, the number of sales has gone above the number of active listings. This shows you why the price has gone up quite a bit.

When you have so many active listings, the price would come down. But when you have more people buying than the listings on the market, that’s when the pricing would continue to go up. I think this would be quite important to look at. If you’re wondering, will the price start to drop now? This is an indicator where you see that the demand is still really strong over here.

What’s interesting is that in the condo market, we’re seeing a pretty similar pattern here. The same thing around 2008; you see this big difference here and the price started to drop. But what I thought is interesting is that besides another drop in 2018, there’s also one more drop around the 2010-2020 timeframe where the price has dropped again.

As you remember when the pandemic just started, a lot of people were staying away from the condos and townhomes. So the price drop here is probably closer to more like the beginning of the pandemic. For the townhomes and condos, they have a little bit more pricing fluctuations.

Then you will look at the same thing here: the number of sales versus the number of active listings. We don’t have any gap here anymore for condos and townhomes. As we see, the pricing for the condos and townhomes is probably going to continue to stay pretty strong.

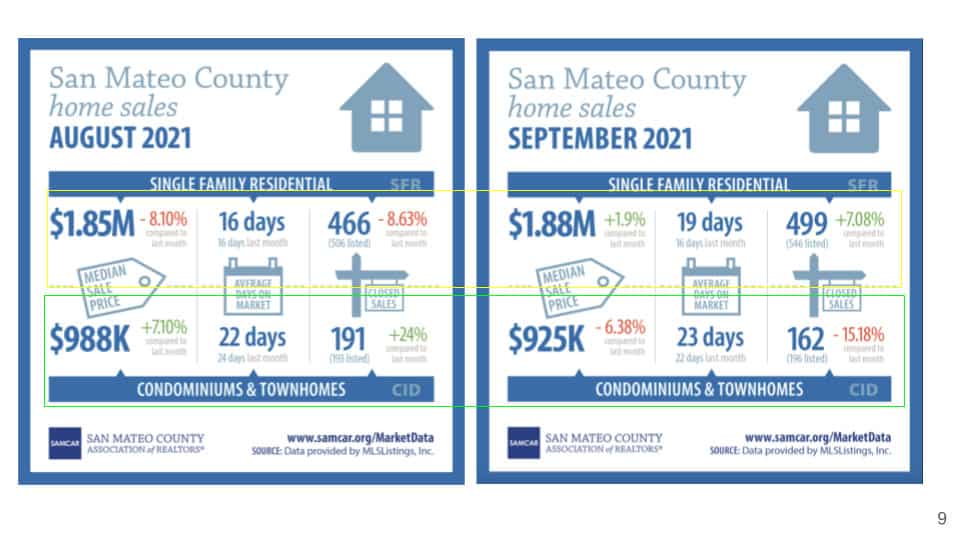

If we look at San Mateo County, the median price is even higher. It is $1.8 million now. It has gone up 1.9% from last month, although last year we had a little drop. The number of days on the market is a little bit longer. It’s 19 days on the market. Then we have a little bit more sellsó7.08% more sellsócompared to last month.

If we look at condos and townhomes, the price dropped a little bit. We kind of flip-flopped. Last month, the price for the condo and townhome went up. But then this month, the price for the condo and townhome came down a little bit; they stayed on the market slightly longer, and had fewer sells as well for the month of September. If you look at both Santa Clara County and San Mateo County, their days on the market stayed a little bit longer.

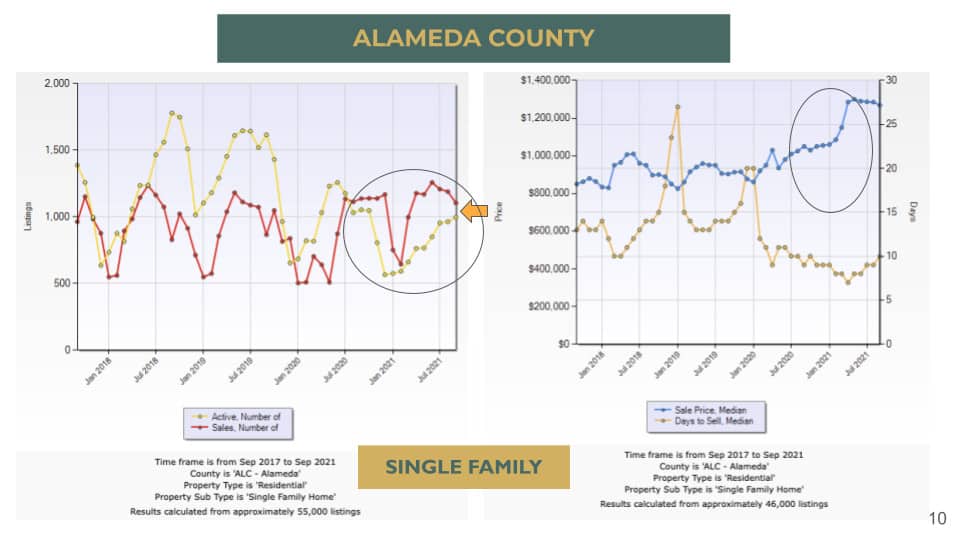

What about Alameda County? In Alameda County, you will notice that the number of sells has been more than the number of active listings on the market. You can see why we have had this crazy price increase since last year. It’s because we have so much demand in Alameda County. I’m sure a lot of people who live in Alameda county have seen that effect as well.

We talked during the pandemic special about how a lot of people are moving a little bit away from the peninsula. They are moving more towards a suburban area. And Alameda County has a lot of areas that have increased in pricing where we didn’t expect that to happen before. So we see this increase in pricing by looking at the number of sells versus the number of active listings.

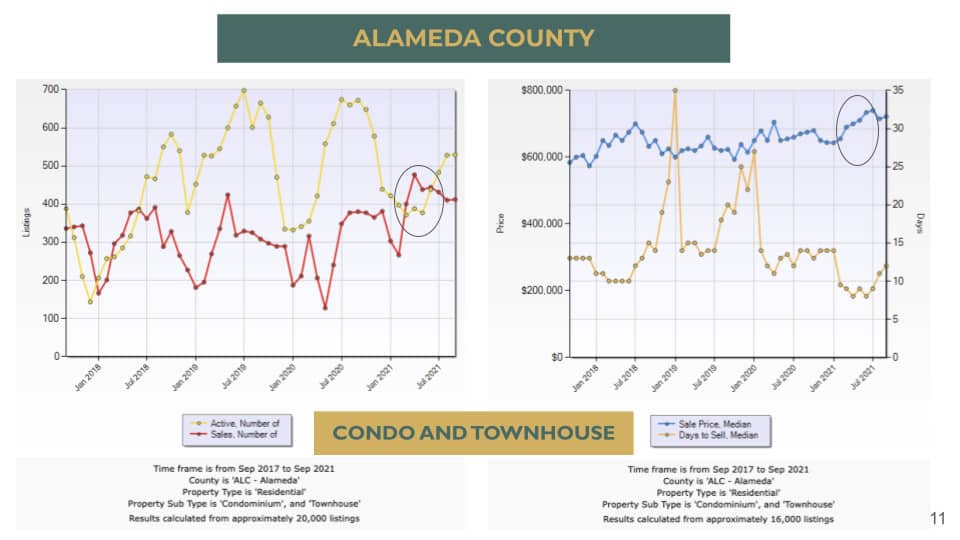

If you look at condos and townhomes, again, we see a number of cells versus the number of active listings. And that’s why we see these pricing increase as well in Alameda County.

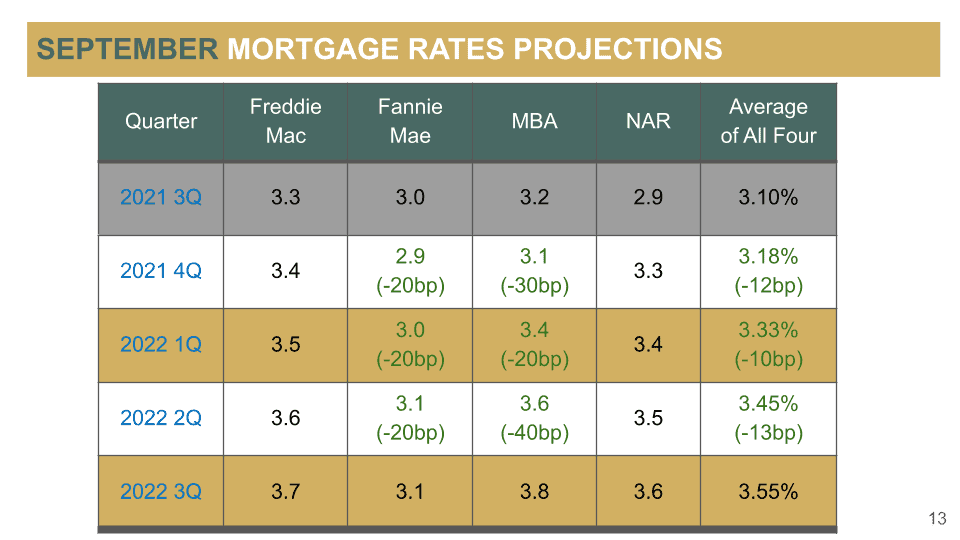

Let’s take a look at the mortgage loan update and see what’s going on. Now, Q3, 2021 is officially over. We know that Freddie Mac/Fannie Mae Mortgage Bankers Association and National Association of Realtors had these projections of our mortgage rate at 3.1%. I would say that that was pretty close to what it was. But then, their Q4 projections for Fannie Mae and Mortgage Bankers Association, have adjusted lower again.

Now instead of the 3.1% that they projected, they now say that it’s going to be 2.9%. For the Mortgage Bankers Association Association, it has come down to 3.1%. So the average of all four is 3.18%. Their projection dropped by about 12 basis points. And the same thing for Q1 2022. It has dropped another 10 basis points to 3.33%. 2022, Q2 is 3.45%. The rates are going up; it’s just that their projections have come down compared to two months ago.

Then they also now are projecting that Q3 2022 is going to be at about 3.55%. We are looking at it compared to this quarter. We’re just going up by about 37 basis points only.

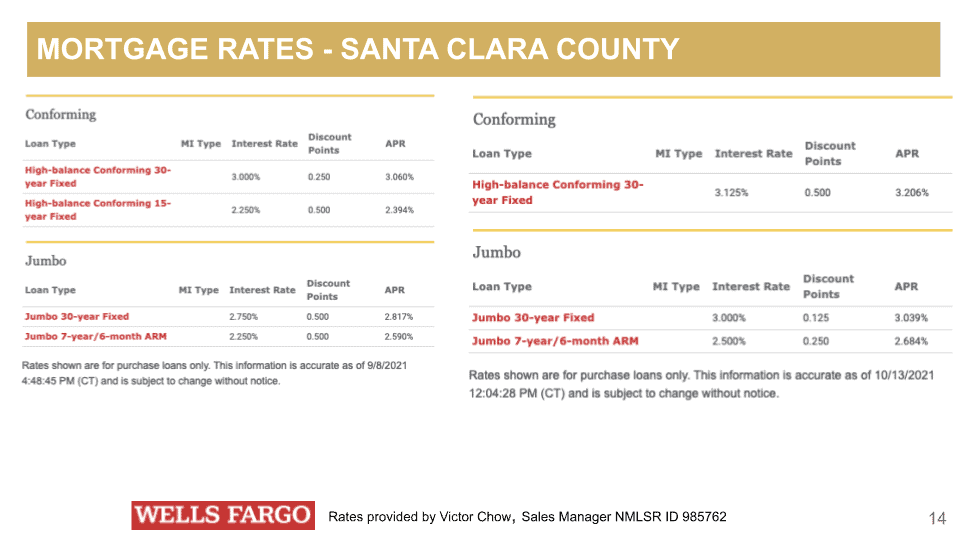

Now, to verify whether that projection is correct, Wells Fargo has been very generous to share with us their mortgage rate. And last month for a jumbo loan, their interest rate for 30 years fixed was about 2.75% and the high balance at 3%. This month, it’s 3.125% for conforming, 30 years fixed, and 3% for jumbo loan. And I thought it was pretty amazing that jumbo loan is cheaper in terms of interest rate compared to high-balance conforming, 30 years fixed.

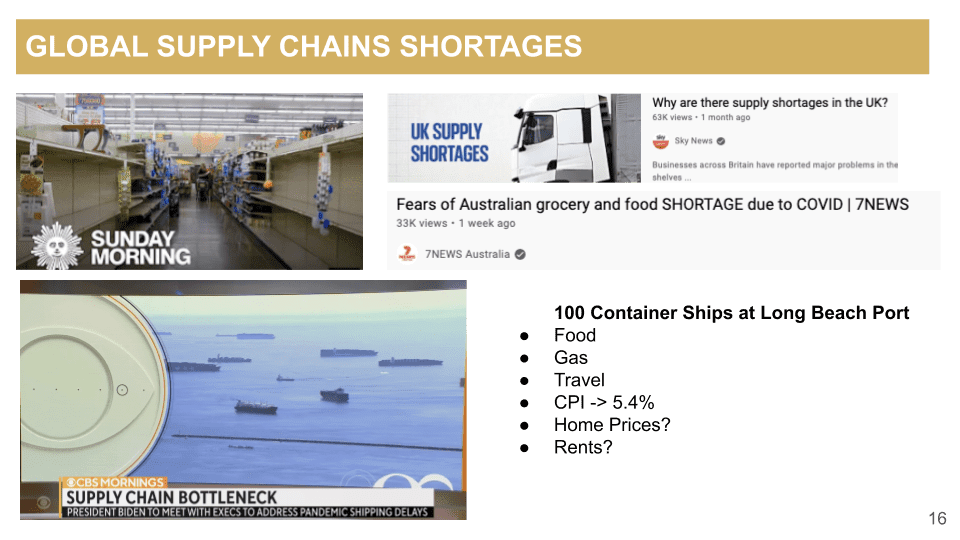

Now, in terms of the macro housing market update, this month, so many news channels have been talking about supply chain shortages. And this does not only happen in the United States. I don’t know if a lot of you have seen this. I don’t know, Tyler, do you see it in your market as well?

Tyler: Yes, we’re seeing it personally and professionally. We’re doing two major capital expenditure projects on two different properties, total repositions, and we’re having major issues with materials and labor from all vantage points. We’re also finishing our basement at our home and we’re waiting on materials. So I think we’re all feeling it. We’re looking at six months to receive the furniture. We’re redoing a clubhouse on one of our properties, and we’re looking at three and a half months. It’s pretty interesting.

Helen: As a matter of fact, I started my kitchen remodeling project, the planning side of it, and the appliances were ordered in May. Today, we finally got the last piece of our appliances, and then the cabinets are going to take 10 weeks. So we’re not going to get them until December.

Tyler: We’re all dealing with it. It’s crazy.

Helen: You see that a lot of remodeling projects are just sitting there, taking forever. However, what I want to touch on later is if you want to do remodeling, you better do it now because the shortage is not just here in the United States. It’s in the UK, Australia, Asia, all over. It’s global. They all have supply chain shortages.

You’ll see that in Long Beach, at the port, they said they have almost 100 container ships just sitting there not able to come in. There are a lot of reasons why we have these supply chain shortages. You might say, “Why are you talking about supply chain shortages? What is there to do with real estate?”

Everything is related to each other. When we have supply chain shortages, this affects all the costs, food, gas, travel. Our CPI is already 5.4%, but that doesn’t even include our home prices and rents. So we have to take a look at all of that and what kind of effect it’s going to have on our housing market as well.

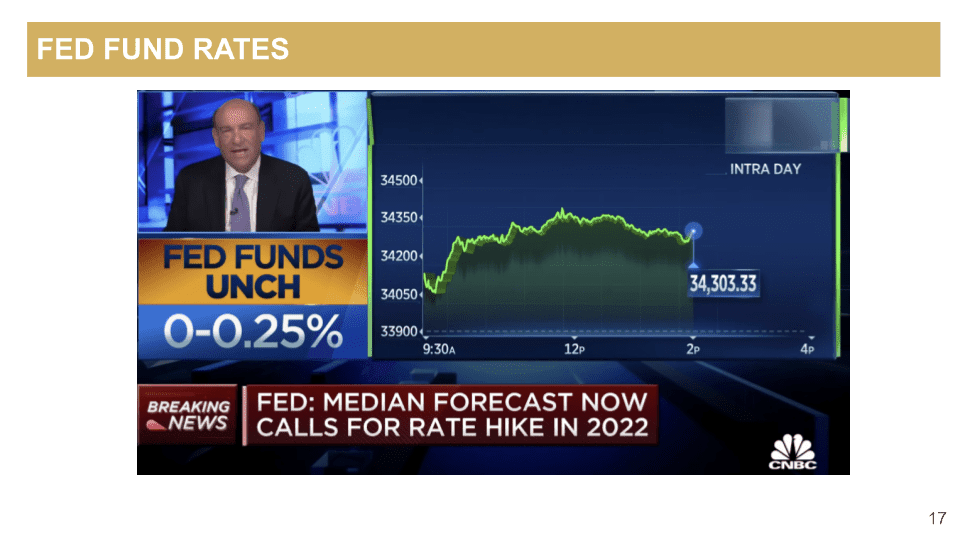

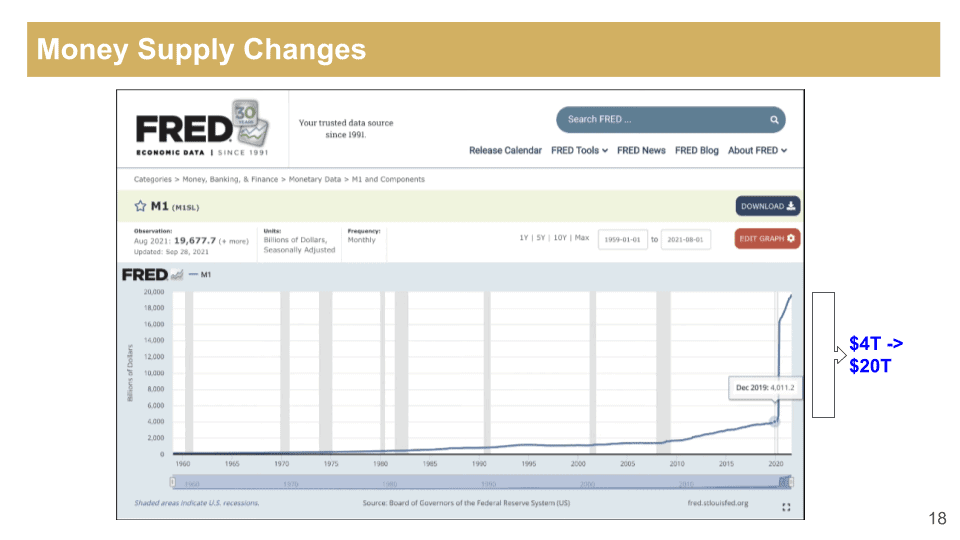

On top of that, federal funds have decided not to change their federal fund rates, so it stays there. However, they are forecasting that they’re going to have a rate hike in 2022. One of the reasons is that we have these money supply issues. You have probably heard a lot about inflation. One of the main reasons why we’re going to have inflation is that before 2020, we had $4 trillion of the money supply. Now, we have $20 trillion. That’s a lot of money that just appears out of nowhere.

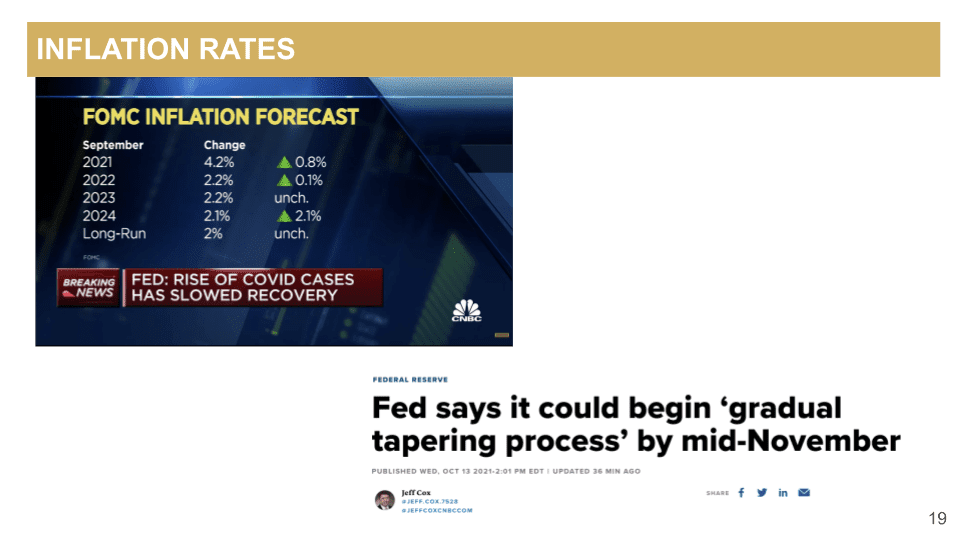

What are you going to do with all that money? They already said that inflation is going to be quite drastic at 4.2%. Even though they said that their forecast for 2022 is about 2.2% to 2.1% long-term, it is still higher than what they would like to see. Again, this does not count the housing costs. I’m sure when you go to the supermarket to buy stuff, or even when you’re remodeling, you didn’t see only a 2% increase in those prices. It’s way more than that. The labor costs, everything is way more than that.

The federal government said that they’re going to start gradually tapering this process by mid-November. What does that mean? It means that they are going to increase the rate in the near future. When they increase the Fed rates, it’s not directly affecting the mortgage rates, but it will cause the mortgage rate to increase.

Luckily, from our projections, it doesn’t seem like it’s going to happen in the next four quarters. But again, remember that projections can change. Almost every month, when I do these kinds of projections, I always come back to say, “They changed the projections again.” Although it wasn’t that big of a difference, they can still change.

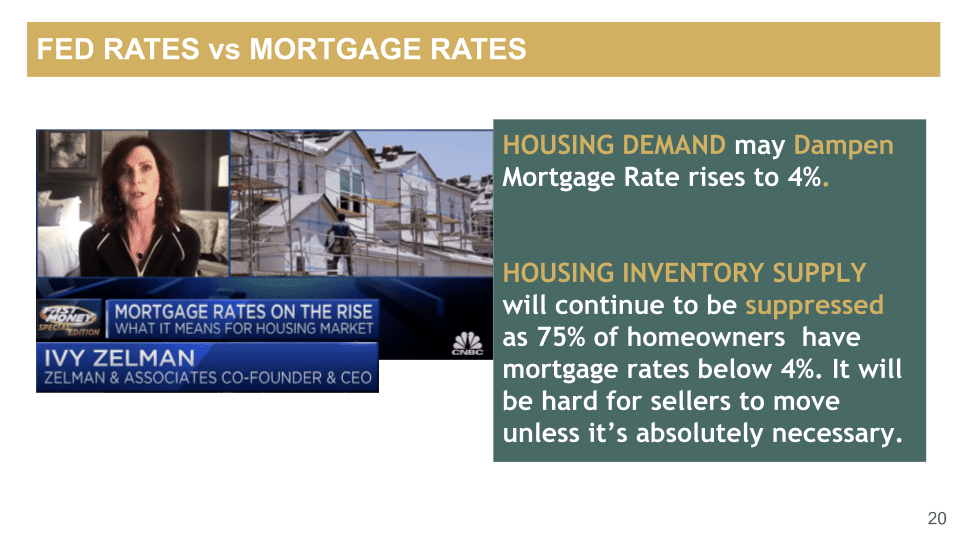

Let’s say that the mortgage rate rises to 4%, then the housing demand is going to be dampened, especially for jumbo loans. You are going to see that big difference in terms of the demand. However, 75% of the homeowners have a mortgage rate of less than 4%. If the mortuary rises to 4%, what do you think about these sellers? Do they want to move? If they don’t need to move, they probably don’t want to move and sell their property. That means we’re also going to have a housing supply shortage again.

We’re going to have lower demand, but we’re also going to have a lower supply. So this is going to affect quite a bit. For this reason, I don’t think the price is going to drop like crazy, I think it’s probably not going to affect it. I think that it’s still going to go up moderately, instead of right now we see 15% from last year. It’s still going to continue to go up. It’s just that the mortgage rate is going to go up and then you’re going to have less supply in the future.

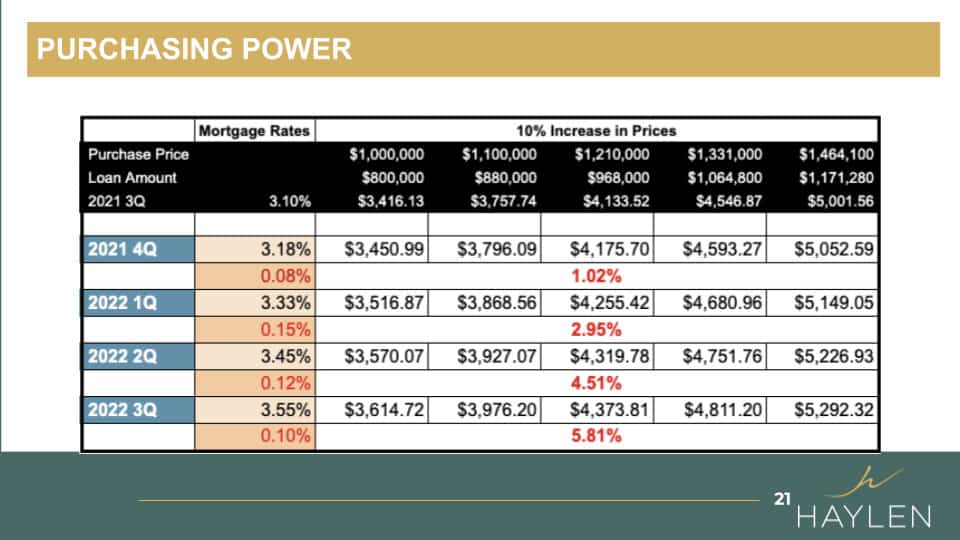

This chart is showing everybody the purchasing power – what it means if there’s just a 10% increase in prices. Here’s a look at the purchase price every 10% and assuming the loan amount is 80% of your purchase price. These are the rates according to the projections right now. We have already passed Q3. If you had bought something at $1 million, your monthly payments are about $3,416. If the market has gone up 10%, then you’re going to be paying about $3,757 instead.

And this is an eight basis point increase. It doesn’t mean that the monthly mortgage payment is going to go up by eight basis points. It’s actually gone up 102 basis points. Then if you wait two more quarters, based on their projections of 3.33%, then your monthly payment, compared to Q3, will be about 2.95%. Then if you wait another quarter, you’re going to be paying 4.51% more. Then Q3 of 2022 if you wait again, it will be 5.81% more compared to what you’re paying here.

Then this does not count the price increase and it’s assuming that you’re paying the same price. If you look at this column, if you’re paying $1 million, you’re paying 5.81% more compared to Q3, but I did not account for if the price has gone up by let’s say $100,000, how much more that is. I just want to give everybody a reference.

It’s one thing that a realtor just wants us to buy properties because they want to sell. I wanted you to look at it a little bit long-term in terms of if there’s a lot of people buying properties based on the monthly payments, they can lock this for 30 years. It’s like what we’re saying right now: if the interest rate goes up, the sellers don’t have to sell. They will just hold on to it because the interest rate is too high for them to move anyway. So think about it a little bit more before you make that decision, whether you want to get out of the market or not.

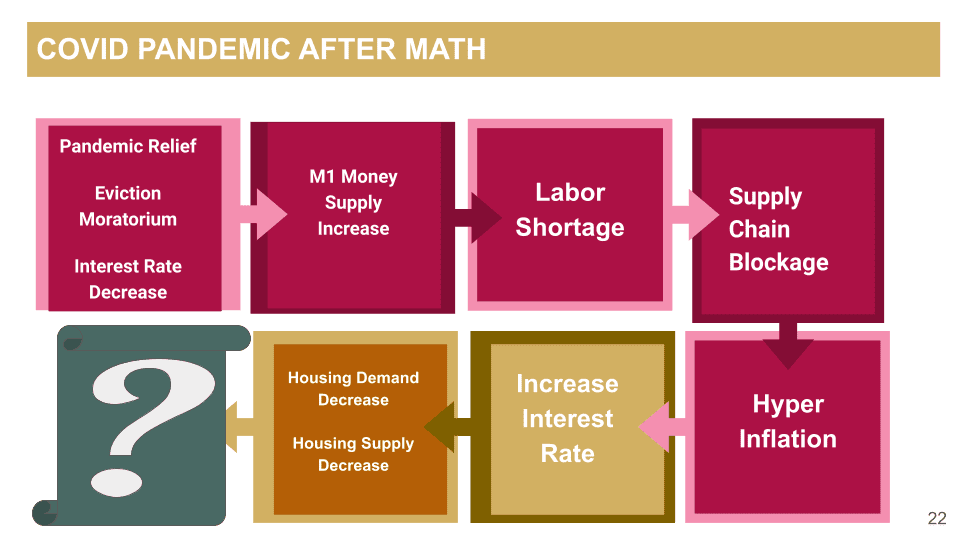

Now, we want to talk about the aftermath. We’ll cover a lot about what’s going on with a pandemic relief. We had the eviction moratorium and the interest rate decrease because of the COVID pandemic. This is what we have seen, which caused the money supply to go up significantly. On top of that, we have a labor shortage and the labor cost is also going up. Now we have supply chain blockage.

One thing about the supply chain blockage and why all these container ships are stuck at the port is the labor shortage. We talked a little bit about this two months ago. A lot of these benefits have caused a lot of people not to go back to work. And then, of course, also there are some job losses, and a lot of women and elderly people have decided to completely get out of the workforce because they have to stay at home to watch the kids or they’re just too worried about their health conditions.

So we have this labor shortage that caused the supply chain blockage, which also caused this hyperinflation. To tackle that, now the Fed, sooner or later, is going to start increasing the Fed rate and cause the mortgage rate to go up, which means the demand for housing might decrease and also the housing supply is going to decrease.

What does it mean? I don’t know. Tyler, do you know?

Tyler: All I can say is that you are a gem, Helen because there’s so much going on and you’re asking me what the numbers look like in my market? While the numbers are a little bit different, everything is interrelated in this global economy. It’s complicated, but we’ve got to be able to read the tea leaves. There’s a lot going on here. I think that we’ve got to be bold. We’ve got to move in some direction. We can’t just be flat-footed, but there’s a lot here.

Helen: I agree with you. One thing that we know for sure is that inflation is going to happen and then the interest rate is going to increase. I think those are the two that we kind of know for sure. In terms of where the price is going to go, we don’t know. We cannot tell you, “We think it’s going to increase another 10%.” Nobody can tell you that.

Tyler: If you look at the weight of money, I was talking to Dr. Peter Lindemann recently on my podcast, and he’s a world-renowned economist. He was talking about this weight of money and if you think about it, it’s unprecedented. The amount of capital injection that we just saw in the monetary supply across the globe has never happened before. And that money’s got to go somewhere. Where’s it going?

Currently, we’re seeing it going into assets. And, of course, in real estate, the housing market but all the other asset classes as well, you’re starting to see that inflation felt. We’re seeing that in real-time and cap rates and all these other things you were just describing beautifully. So I think there’s a lot to be said about that. I would imagine we’re going to see continued asset inflation as well. What does that mean for your strategy?

Helen: Absolutely. I think that’s why real estate is so important and everything is related. On top of that, I want to talk a little bit about multifamily, especially because today, we are talking about syndication. Yesterday, we also had a multifamily panel. We had Marco Cugia from CoStar, Joshua Howard from California Apartment Association, and Aaron Frederick from Colliers, who’s our multifamily broker.

We were talking about, “Well, the eviction moratorium expired. California had a lot of regulations. With this expired, a lot of people worry that landlords are going to just start evicting all the tenants.

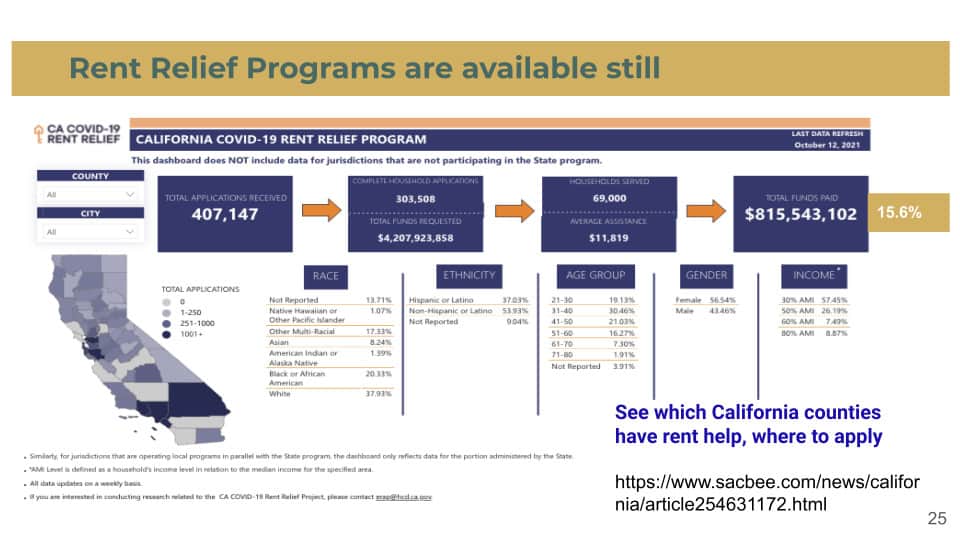

Just to let you guys know, there are still a lot of different tenant protection programs in different counties. Feel free to use this website link. This is where you can find out a lot of different counties, you have different links in there, and see what kind of programs they have to offer tenants and also landlords.

On top of that, in California, we have a $5.2 billion rent relief program that’s dedicated to helping landlords and tenants. But as of October 12, we only have 15.6% funded so far. There are still ways to apply for these rent relief programs so be sure to take advantage of that if you know somebody who needs that help. Just because the eviction moratorium is over doesn’t mean that you cannot apply for that.

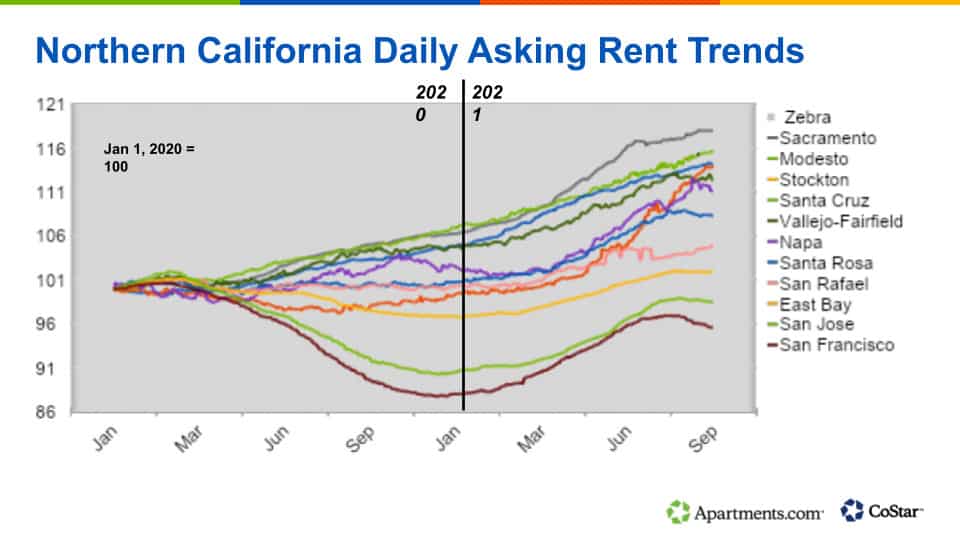

Marco Cugia from CoStar shared this chart. I thought it was very interesting. If you look at San Jose and San Francisco, the rental rates have gone down due to the COVID situation and then they’ve started to climb back up. But then as you know, around June or July, we all thought that we’re going to go back to work around September/October. So the rent kept going up. However, as soon as they said, “Never mind, nobody’s coming back until maybe next year because of the Delta variant,” you see the rate has gone down a little bit.

What I think from looking at this is that we could tell the rental rates are relying on whether the offices are going to open back up or not. Then Sacramento has been really strong. It has been going up during this whole time. Modesto is also really strong. Stockton is one that I thought is interesting; it has gone up quite a bit as well. And Santa Cruz also has been going up strong.

In a lot of these markets, as you see, the rental rates are really strong. But what we were talking about yesterday was that you hear on the news that they always talk about the mass exodus. A lot of people are leaving California; people don’t want to live here anymore. Then why are the rates still going up in that case?

I think sometimes the news makes us believe in certain things, but then we see the activities and demand within the Bay Area or within California. I just wanted to point that out.

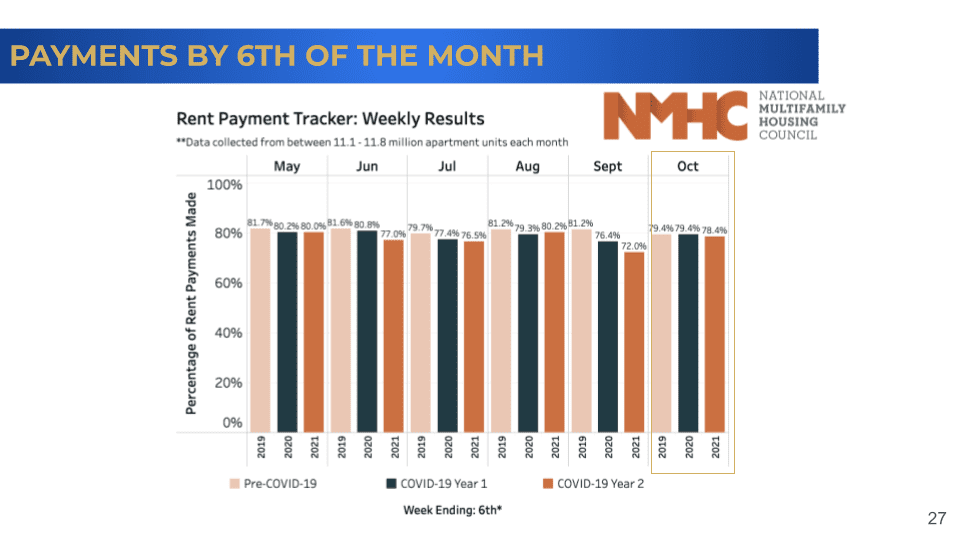

Also, I was very pleasantly surprised to look at the rent payment tracker by the National Multifamily Housing Council. As you see, in 2019, the first six days. This is usually up to the sixth of the month before they become delinquent. They collected 79.4%. But if you look at the last couple of months, it’s been low. Especially in September, it was 72% for 2021.

But we jumped back up to 78.4%. I thought this was a really good number, even though it’s still lower than August, but it is higher than July, higher than June, and slightly lower than May. So at least this is a good number to show, and this is pretty much after the eviction moratorium has expired.

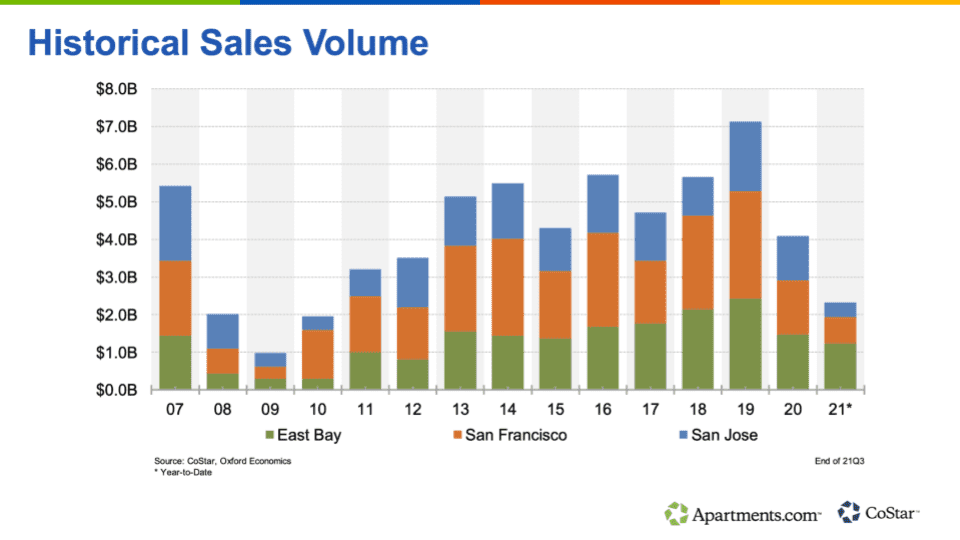

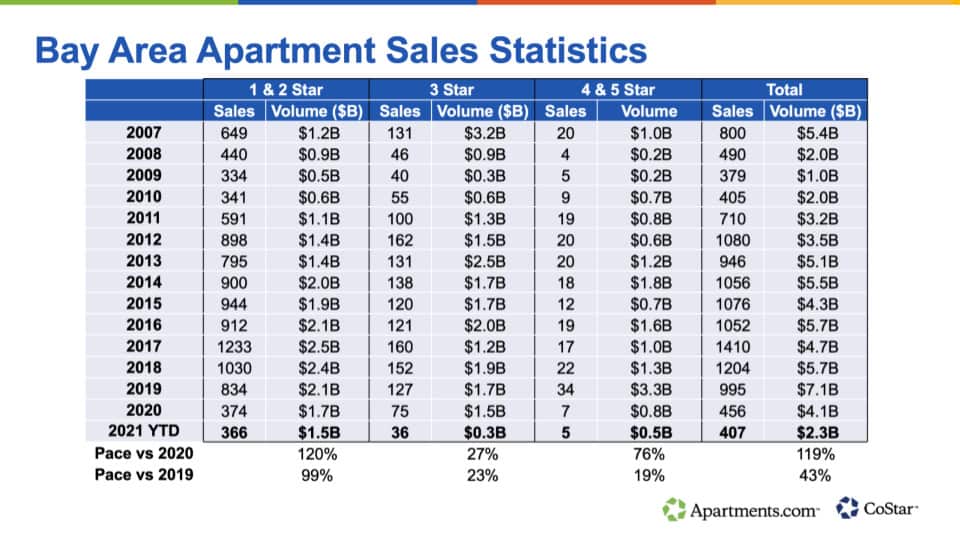

And then sales volume-wise though, I know a lot of people are talking about, “Gosh, I want to invest in multifamily. Why aren’t you sending me any listings? How come there’s nothing going on?” That’s because there’s nothing going on. The volume is so small and that’s why it’s really hard to find. It’s the same struggle that all the multifamily investors are going through right now in the Bay Area. You’re not the only one, it’s just that we have a very tight inventory right now.

This is also shown on the chart. If you look at the numbers, $7.1 billion in 2019, that was the highest. But then we are 1/3 of what we had before in 2019. That’s why you see that it’s so hard to find any multifamily to invest in right now.

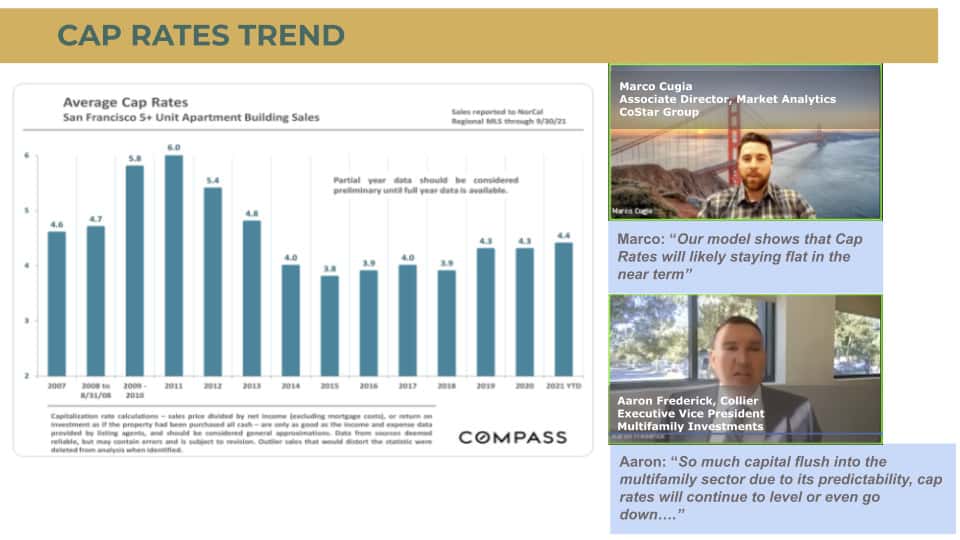

And the cap rates back in 2011 in the Bay Area were like 6% cap, but we came back up compared to 2015 3.8% to 4.4%. But where are we going to continue to go?

Marco Cugia yesterday mentioned that, he’s from CoStar, they have done some analysis as well. Their model shows that cap rates will likely stay flat in the near term. Aaron Frederick also said that because they see so much capital flush into the multifamily sector due to its predictability compared to other commercial real estate sectors, he believes that the cap rates will continue to level or even go down slightly.

So, the cap rate is pretty low, but also very interestingly, we used to get made fun of the fact that the Bay Area has such a low cap rate. But now, if you go to most of the major cities in Texas, everywhere, their cap rate is low, just as low as the Bay Area.

Tyler: Yes, we’re seeing very low cap rates across most primary and secondary markets across the US, and 4.4% isn’t too bad in comparison.

Helen: We do have somewhere it could be like 2% or 3%, but we see a lot of 3%, 3.5%. Again, when we go outside of California, we also see a lot of very low cap rates. Some of the sellers might want to sell. Hey, we need inventory. If you want to sell, this is a good time to sell because the cap rate is so low.

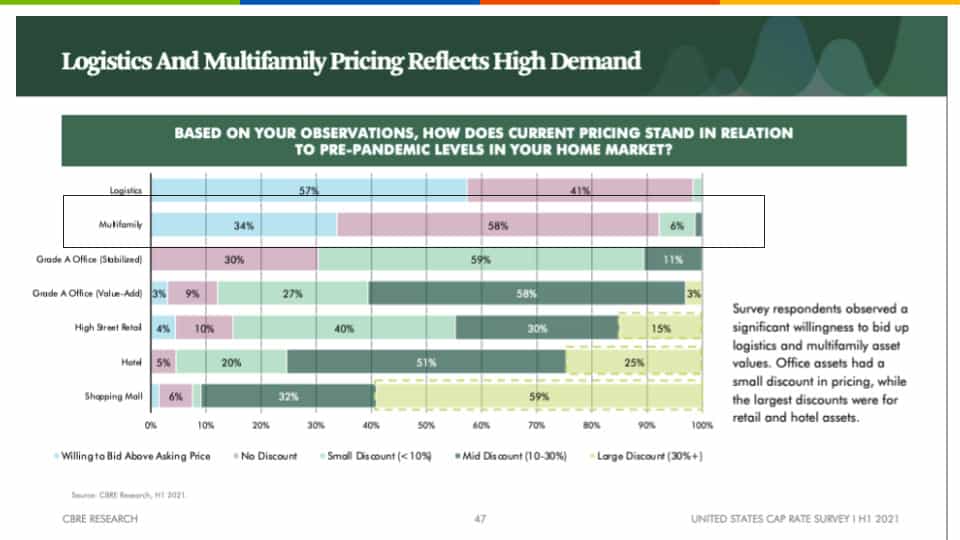

If you look at this chart from CBRE research, this is a survey to see how the current prices stand in relation to pre-pandemic levels in your home market. And 34% of them said that they’re willing to bid above the asking price, 58% no discount, and only 6% said that they would like a small discount. But it’s very little if you look at it compared to office, hotel, and retail. These ask me for a much bigger discount and also shopping malls. Logistics, which is more of the warehouse and industrial and multifamily, they’re still holding strong.

This month, we are honored to have Tyler Chesser, CCIM as our guest to share his Secrets to Invest and Form a Successful Real Estate Syndication. If you are wondering how to find investors to invest in your project, then make sure to watch this episode! As usual, if you have any comments or questions, please feel free to get in touch with us.

Stay up to date on the latest real estate trends.

A Bay Area Realtor's approach to schools, neighborhoods, and long-term value for families making a move

Part 1 of HAYLEN's series on the 2026 CCIM Spring Forum in Philadelphia

You’ve got questions and we can’t wait to answer them.