January 2021 Newsletter – Key Topics and Trends

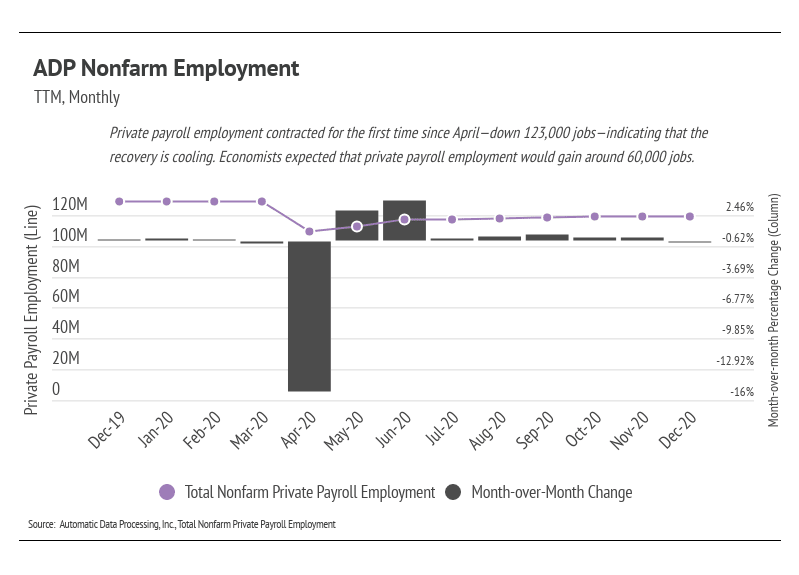

According to the ADP private payrolls, the U.S. lost 123,000 jobs in December 2020, marking the first contraction since April. Economists predicted an increase of around 60,000 jobs in December. However, they did not anticipate larger companies, especially in leisure and hospitality, laying off employees due to reimplementation of stricter COVID-19 restrictions.

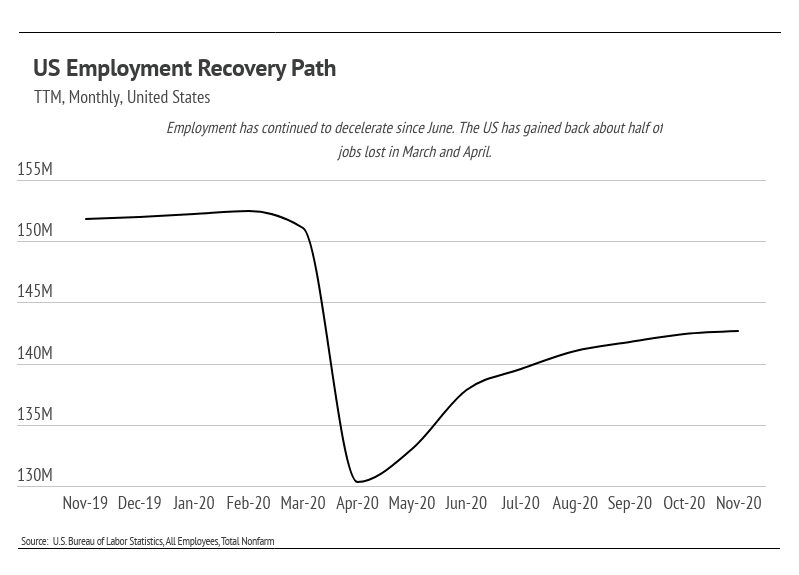

Data from the Bureau of Labor Statistics differs in the exact numbers but shows the obvious deceleration in employment growth. As time passes, more and more jobs will be permanently lost, likely with real long-term economic impact: fewer people interacting in the economy usually indicates less buying, which trickles into less production, which trickles into fewer workers needed, leading to more unemployed workers.

Job growth is one of the clearest indicators of economic health, so the December jobs contraction underscores a slowing of the recovery and the need for government stimulus. Under the incoming presidential administration, government stimulus is far more likely but will take some time to implement. With aid, businesses will be able to continue operating and will likely be able to hire significant numbers of employees back, setting the recovery back on course.

To help struggling businesses and people, the government will have to spend significant amounts of money. Heavy fiscal spending is often associated with higher inflation. Currently, inflation is around 1.2% (the Federal Reserve targets 2%), and with the expected increase in government spending, the expected inflation will rise as well. Ultimately, money today is worth more than money in the future. Not only can you buy more today, but real interest rates (inflation-adjusted interest rates) will be lower as well, making a home bought today cost less than its future price.

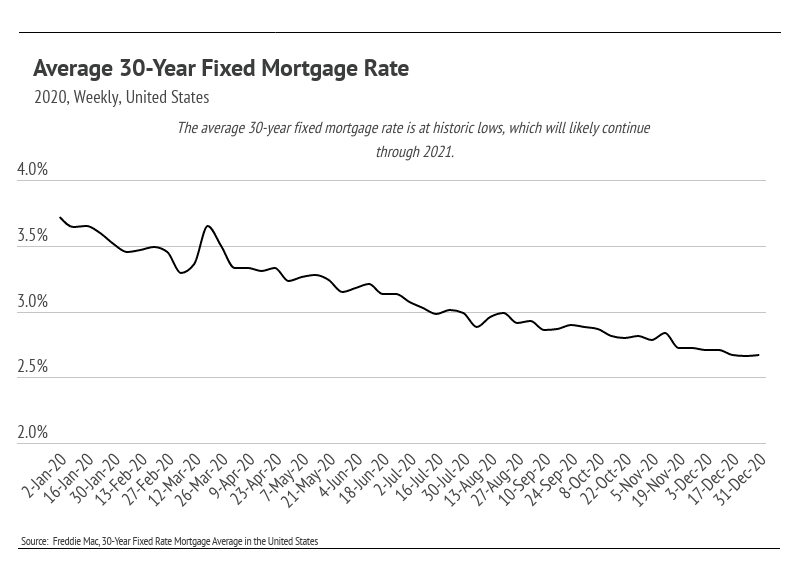

For example, the average 30-year mortgage rate is 2.67%, and if the inflation rate were 2%, the real interest rate on the mortgage would be 0.67%.

The financial circumstances on the individual level are highly variable, now more than ever. Those who have been unaffected (or even positively affected) financially are likely saving more money than ever. Strict COVID-19 restrictions have largely cut travel, dining, and entertainment expenses, allowing potential home owners to devote more of their income toward buying a home that they love. With historically low mortgage rates and an expected increase in inflation, it’s never been cheaper to finance a home.

Demand shows no sign of decline in the near term. Today, housing is one of the best investments one can make, as it has been historically.

Stay up to date on the latest real estate trends.

You’ve got questions and we can’t wait to answer them.