January 2023 Newsletter - Silicon Valley Local Lowdown

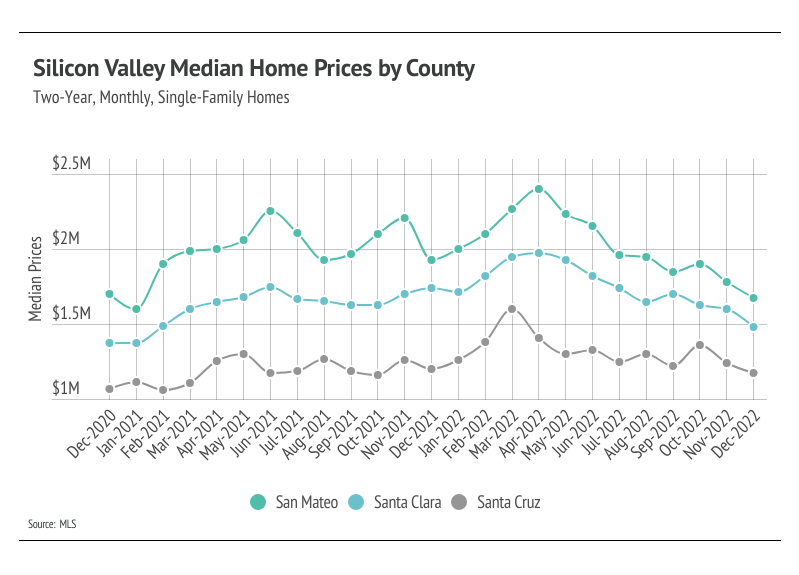

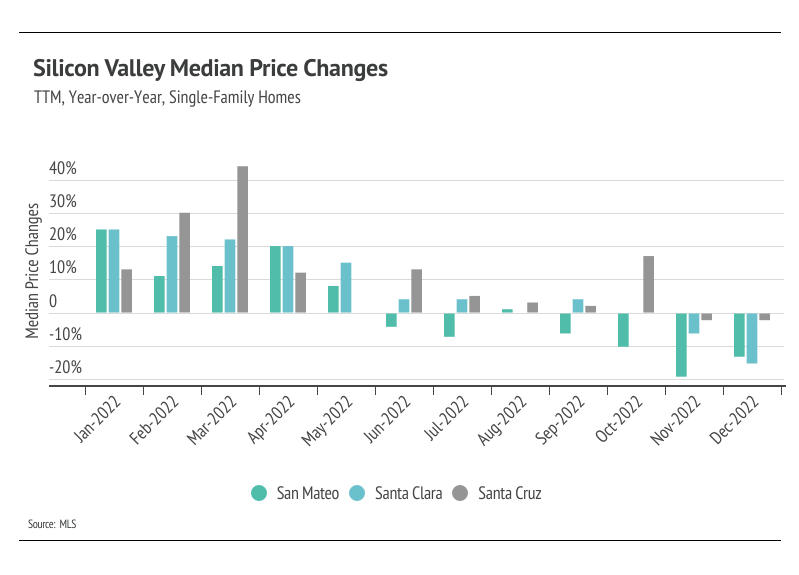

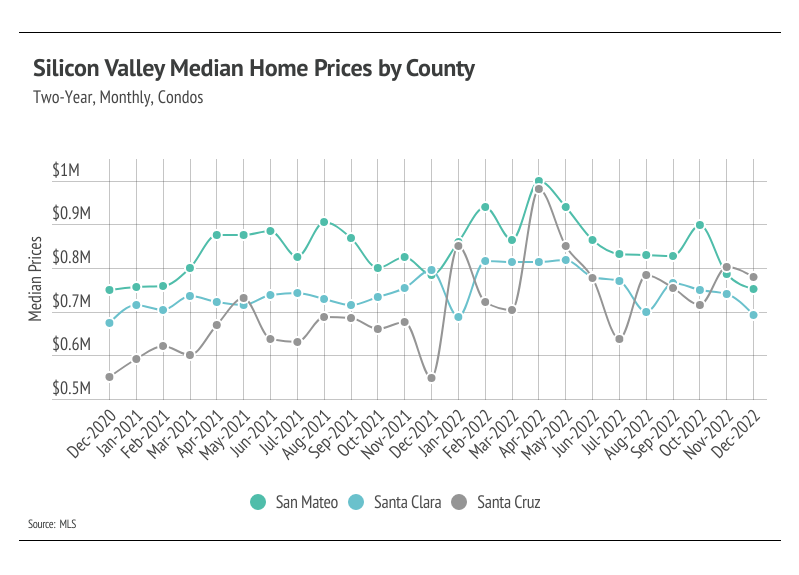

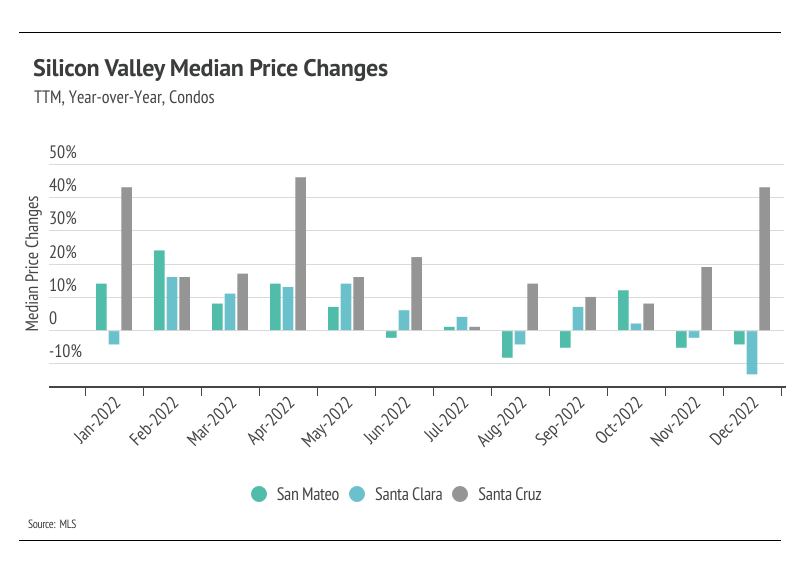

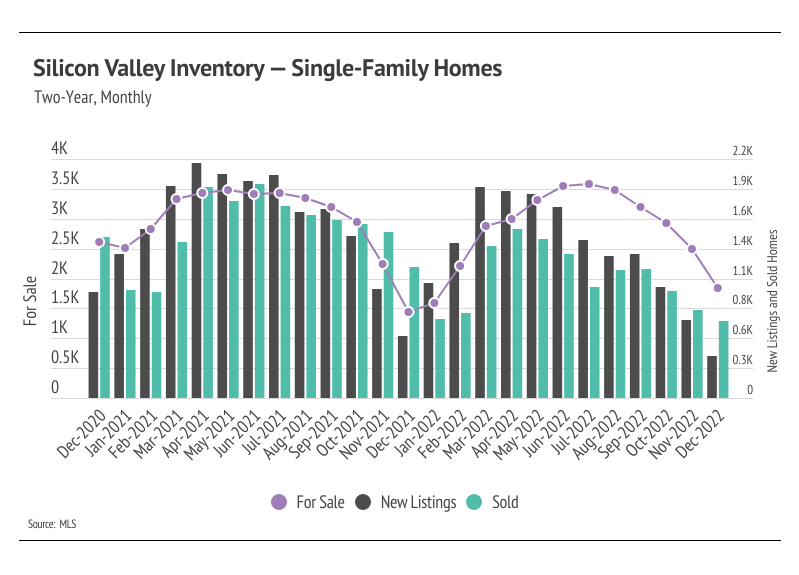

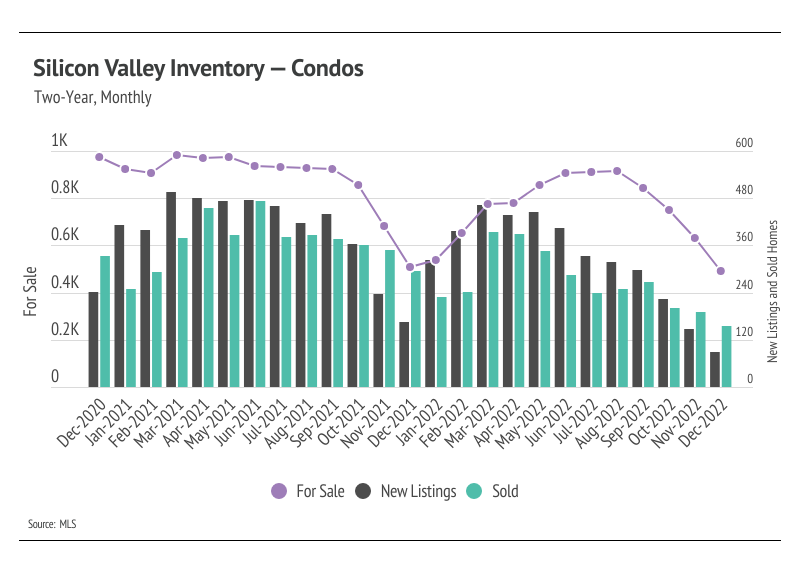

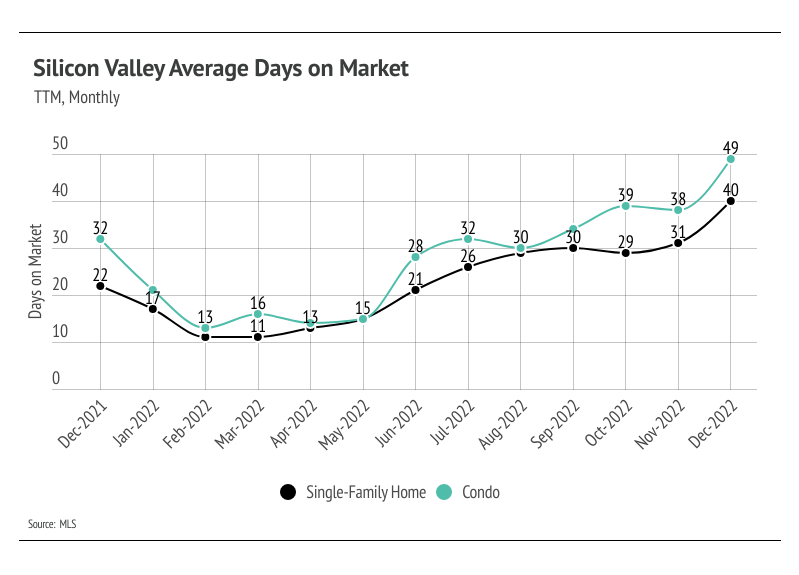

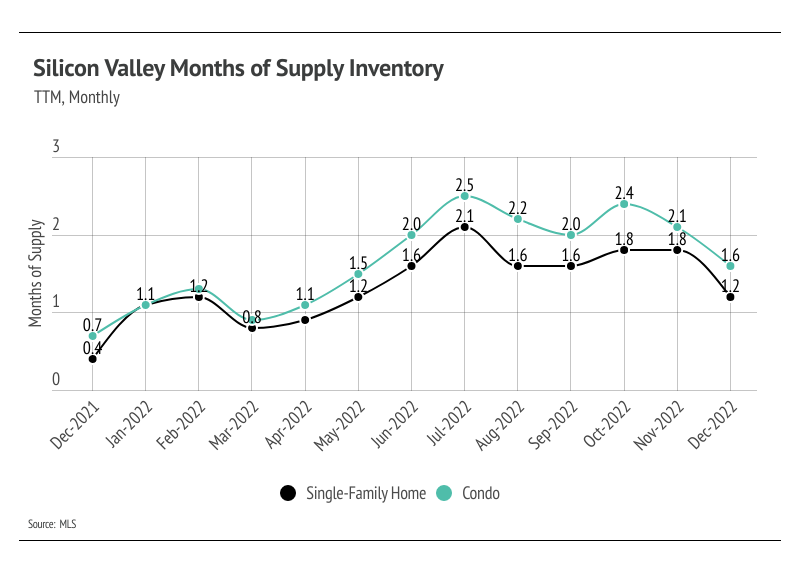

As we mentioned in the Big Story, the market has cooled for both buyers and sellers, largely because of higher interest rates. As we enter the new year, the market feels familiar — but from the era before 2020. Demand in Silicon Valley is evergreen, so we aren’t worried about matching buyers and sellers. That said, sellers likely won’t be getting multiple offers the second the home hits the market again anytime soon. To make a long story short, there is definitely less stress on the buying side of the market. Prices will most likely increase in 2023, but at a more modest rate of around 5-6%, which makes for a much healthier market than what occurred over the past three years. Single-family home and condo prices increased over the past two years, even with the declines from the peaks reached in 2022. Without any signs of interest rates dropping, we’re entering a stage of slower, longer-term growth.

Our team is committed to continuing to serve all your real estate needs while incorporating safety protocol to protect all of our loved ones.

Stay up to date on the latest real estate trends.

You’ve got questions and we can’t wait to answer them.