Mortgage Rates Since Last Peak – December Housing Market Part 2

Welcome to part 2 of the December Bay Area Housing Market Updates! If you haven’t, please read part 1 here. You can also watch the video recording of this episode here.

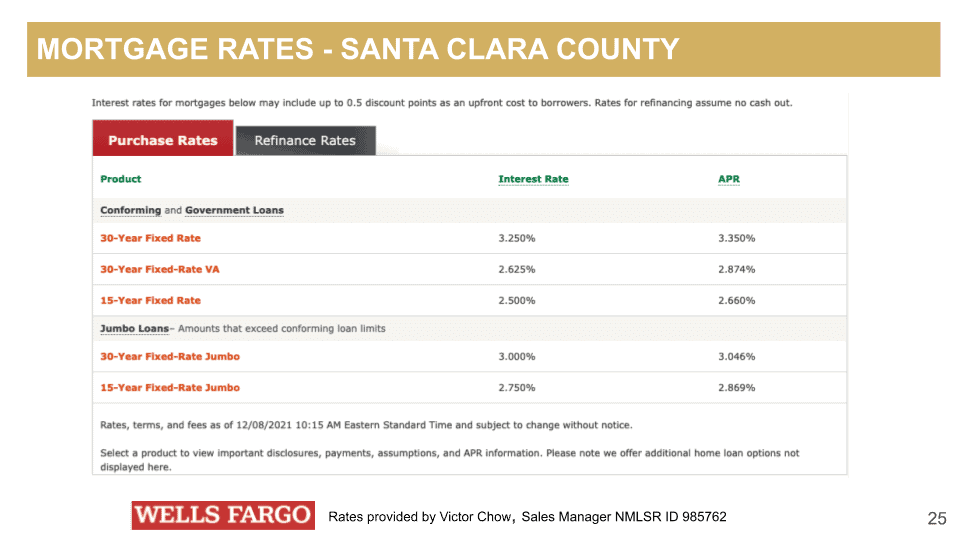

The mortgage rate for 30 years fixed Jumbo on Dec. 8 was 3% versus conforming 30 years fixed is 3.25%, so the larger the loan, you are actually getting a better rate at 3%. This was just pulled early today, December 8th.

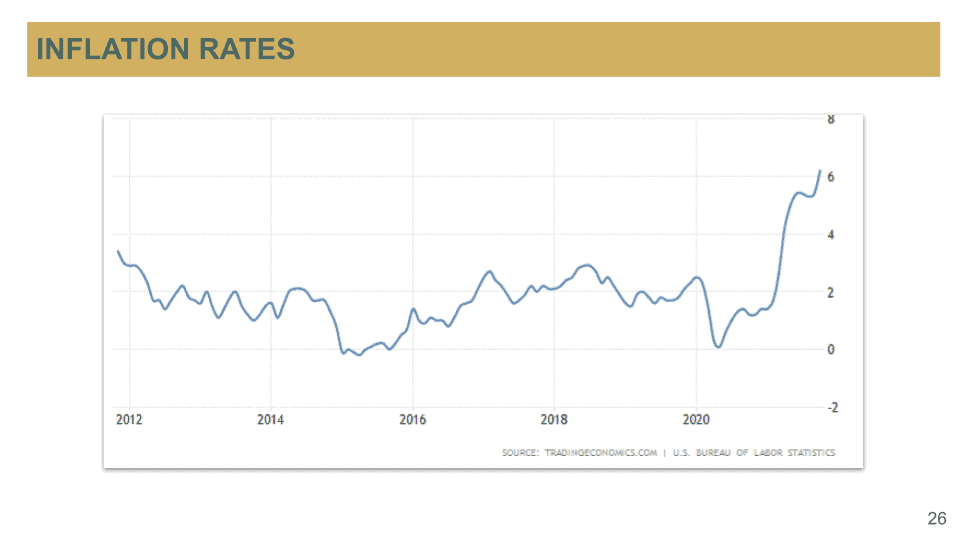

As we talked about last month that we are expecting the inflation rate to go up, even more, we already have seen the inflation rate has gone up. But, what does that mean? If you refer back to the November housing market update, these inflation rates can actually affect the mortgage rates in the future as well. So, we do expect the mortgage rates to continue to go up.

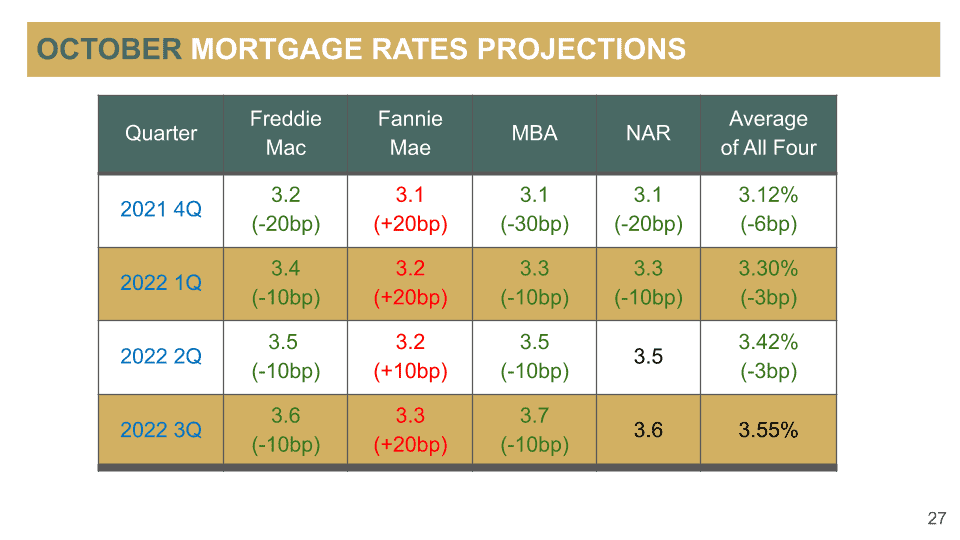

Good thing is that this month or November, I should say the November mortgage rates projection is staying the same as the October mortgage rate projections. That is the good news but the bad news is that it is trending up, so basically, the projection is still saying that the rate is going to continue to go up. It is not too much we are talking about 3%-3.12% to about 3.5% but then remember for the last few months that we had adjusted their projections. I should say they have adjusted their projections, so depends on what the Fed is going to do with the Fed rate. They can potentially adjust their projection as well. I just want to remind everybody to think about that because when you look at the inflation rate, it is going to go up. It is likely that the Fed rate is going to increase as well and which in turn can affect the mortgages rate as well.

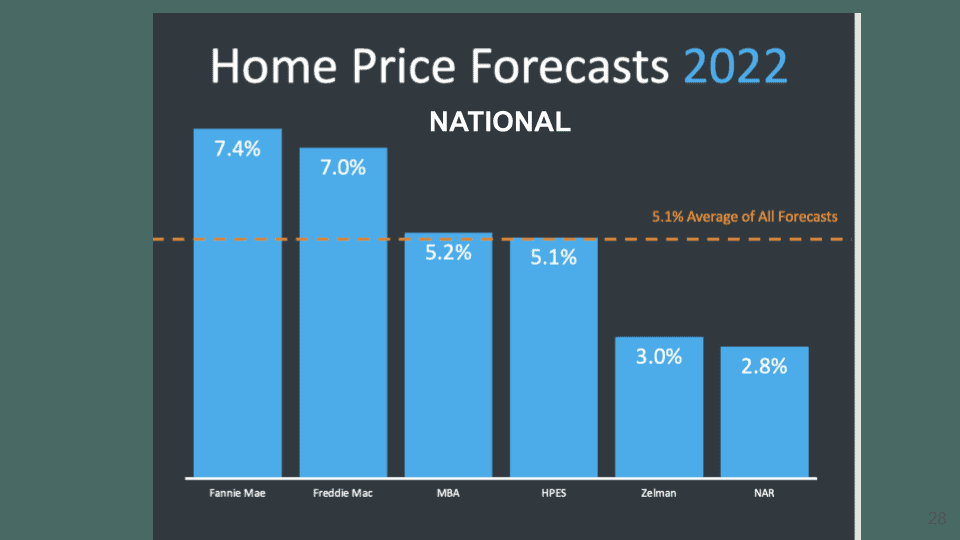

What about a Home Price Forecast? Nationally, Fannie Mae, Freddie Mac, Mortgage Bankers Association, HPES, Zelman, NAR are still expecting the home price continues to go up. It is not going to be double digits but it is still going to be a pretty healthy appreciation.

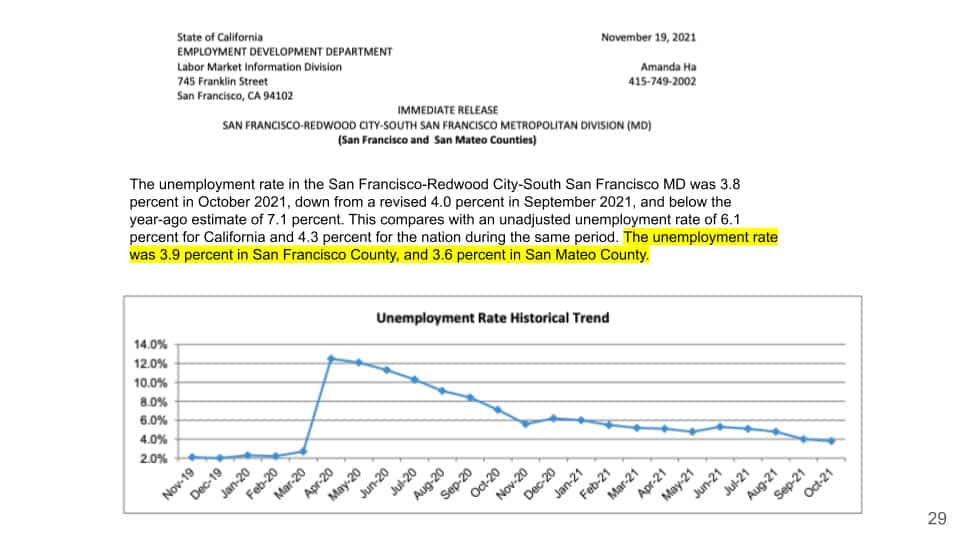

In terms of in our Bay Area, this report just came out on November 19 from the EDD, Employment Development Department, and they had shown that San Francisco County, their unemployment rate is at 3.9% and San Mateo County is at 3.6%, understanding that national is at about 4.2% currently, so we are below the national unemployment rate right now.

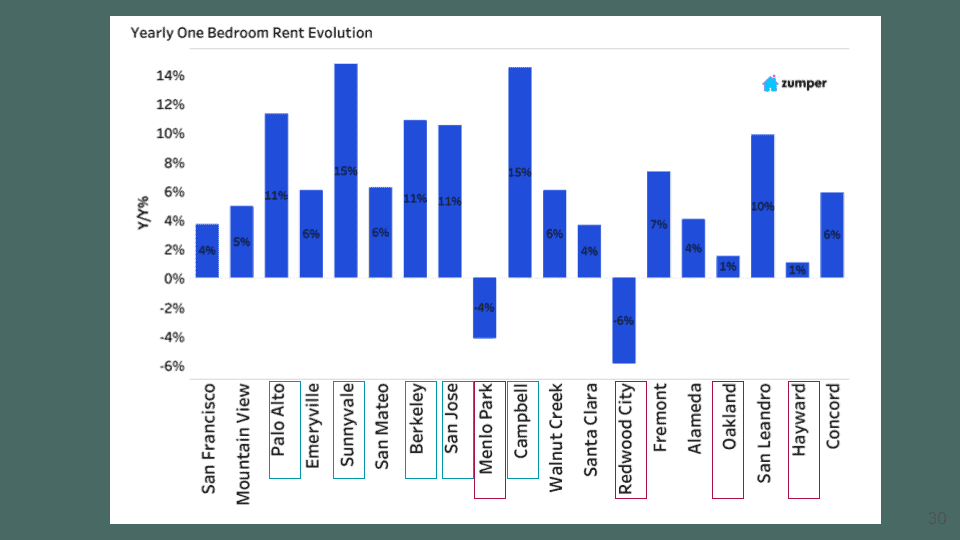

I also want to look at the rental situation. The one-bedroom rents currently as we see that we actually had some good news here. Because, if you look at Palo Alto, Sunnyvale, Berkeley, San Jose, Campbell that had gone up quite significantly, double digits in terms of their rental rates compared to last year. Of course, last year has gone down but then it seems like we have a healthy return on their rental rates. The most is at Sunnyvale and also Campbell at 15% then Palo Alto, Berkeley, and San Jose at 11%. But the losers on the market right now is Menlo Park and Redwood City. Redwood City lost 6% compared to last year, Menlo Park reduced 4% from last year, while Oakland and Hayward only went up about 1%.

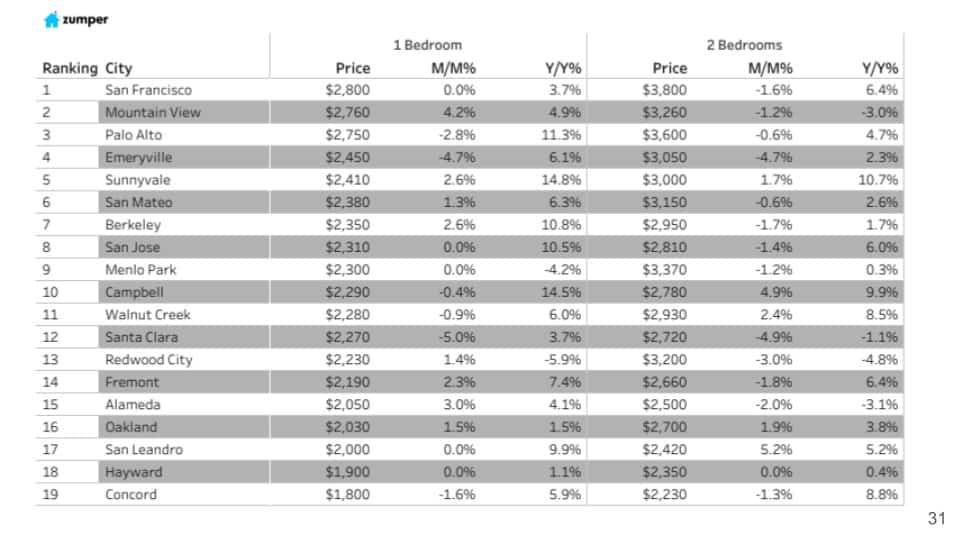

Now, this is a chart where you can see starting from most expensive, San Francisco is taking the place still at $2,800, on average for one-bedroom while two bedrooms like $3,800 and the next in line is Mountain View at $2,760 for one-bedroom and $3,260 at two bedrooms. Quite interestingly, we see that Concord is at $1,800 also had gone down 1.6%, but it did go up compared to last year for about 5.9% and then their two bedrooms is $2,230 and they are ranked 19 on this list, right now. We definitely see that the multi-family market inventory is so low. I know there are a lot of people who are still very interested and investing in multi-family because the interest rate is low right now and now, the eviction moratorium has expired, a lot of investors have a lot more confidence to come out to invest. It is just the fact that there is not a lot of inventory. I think everybody thought that a lot of apartment owners are going to sell, but they are really holding on to it. We do not see a lot of inventory on the market, unfortunately; and that if you are frustrated, do not worry, you are not the only one.

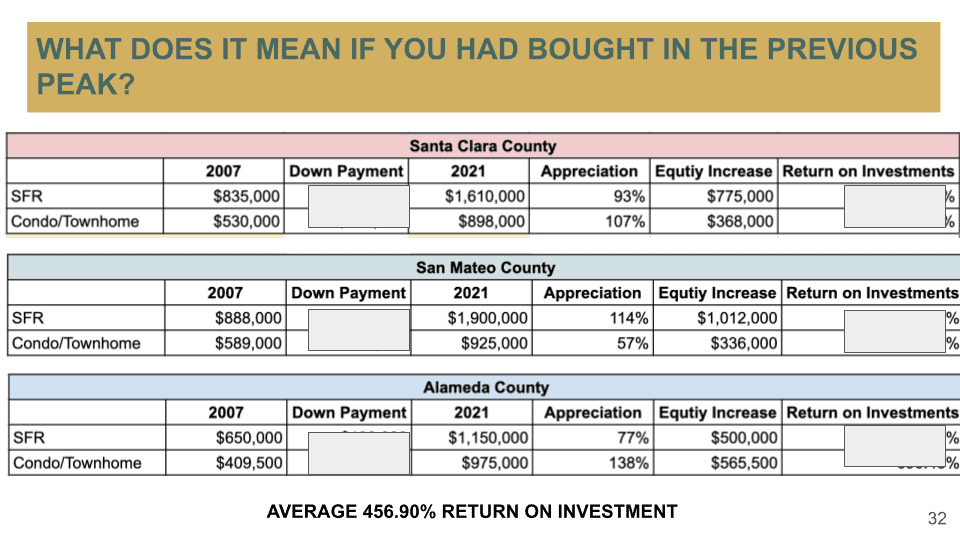

This is the chart that I want to show you. I put it in a spreadsheet format because you know we talked about the last peak right? It was in 2007 and that we want to compare to 2021. Now, if you have bought this property, I know back then you could have bought this product with 100% down, so that is even crazier but let’s just say that back then everybody was still using a 20% down. Honestly, I do not remember back in 2007 people actually put 20% down. I did so many 100% loans at the time and I have seen 105% meaning that the bank actually gave you money to buy a house and then at the time there was like state of income, state of asset, loans which means you do not need to prove your income, you do not need to prove your assets, and you just tell them how much you make and how much you have in the bank and the bank will take your word for it because they believe that all borrowers are honest at the time.

So, let’s just say that you put 20% down which is the minimum right, that means for $835,000 single-family you put $167,000 down, while condo you put $106,000 down. With the increase in the equity and all that, your appreciation is not just 93, your return-on-your investment is actually over 460%, and also even you have a condo, it’s over 300%. I think this is why real estate is so powerful because it is not just looking at the property value, you are looking at how much you invest right? Everything is based on what you have invested. So, unless this is stock then, you will be like “okay, you know, I bought this much with all cash, and then this is how much I made.” But, then with real estate, you actually can leverage and this is so powerful when you look at it this way.

The same thing for San Mateo County, their down payment is only about $177,000, everything is like less than $200,000 at the time and your return-on-investment – look at this – single-family for San Mateo, almost 570% return and then even for the condo, we talked about “Oh it’s only 57%,” but really your return-on-investment is 285% and then Alameda, again the same thing. If you look at return-on-investment 384% and 690% for condos and townhomes. This is really truly the power of real estate investments on your own home, not really buying for rental or anything like that. I have been in the business for 16 years now, still gives me goosebumps when I put somebody in the house and they are going to start building their equity in their home where they know every single month, their monthly payment is fixed and if the interest rate comes down, they will refinance.

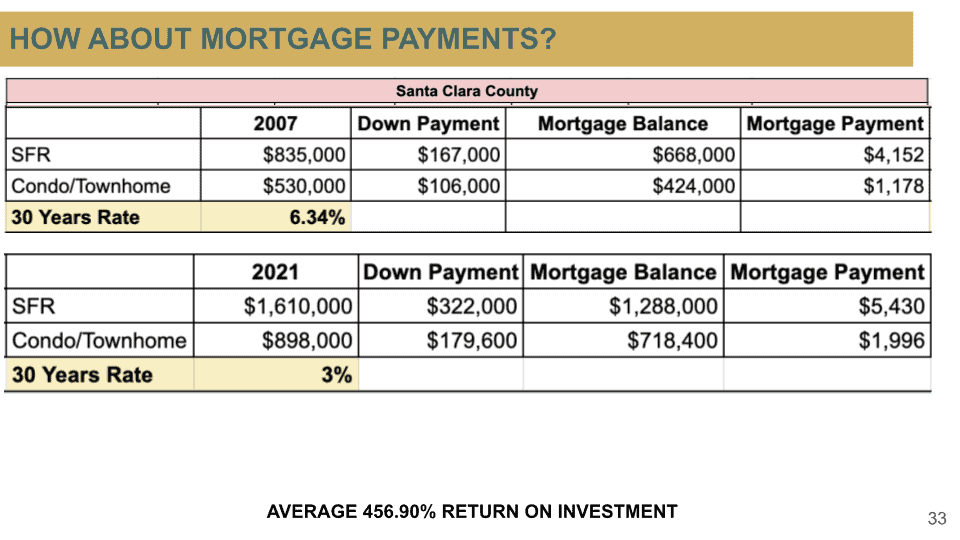

Just 2 days ago, we had done an event in Mountain View, and I just thought to ask around people, “Hey, do you know what was the mortgage rate back in 2007, 2008?” Many people said, “well, it’s higher than now.” I was like, “absolutely correct” and their answer was, “hmm, I think it was 4.5-4.75%.” They had no idea back in 2007, the mortgage rate was at 6.34%.

It was double what we have today and if just looking at the same numbers again, the mortgage payment back then on the $668,000 mortgage balance, your mortgage payment would have been $4,152 versus you having double your value and you are only paying less than a $1,300. I think this is just crazy to look at like that. If you were not in the real estate market back then you do not appreciate how low our mortgage rate is right now. I remember I had one of the investment properties I had actually 7.5% mortgage rate; 3% is almost nothing. So, be sure to take advantage of that; I mean, if you compare the mortgage payment for the condo same thing, $1,178 versus $1,996 for a $700,000 mortgage. If the mortgage rate continues to go down at least you bought it now, you can still refinance later. But, if you miss these mortgage rates, you miss it and that is it. You are not going to come back and get it again.

I know at one point, last year, we had clients who got 2.5% with like a few different discounts from the bank and that is excellent mortgage rates. If you can take advantage of that be sure to do that.

Let’s look at San Mateo County. San Mateo County is the same thing, $4,416 and then more than double the mortgage balance, you are definitely pay more but you are not paying double the mortgage payment you are paying about just 50% more which is $6,400 per month and then for a condo, it’s like $1,300 versus a $2,056 and this is about what 14 years later you are paying that little more only, it is like $700 more.

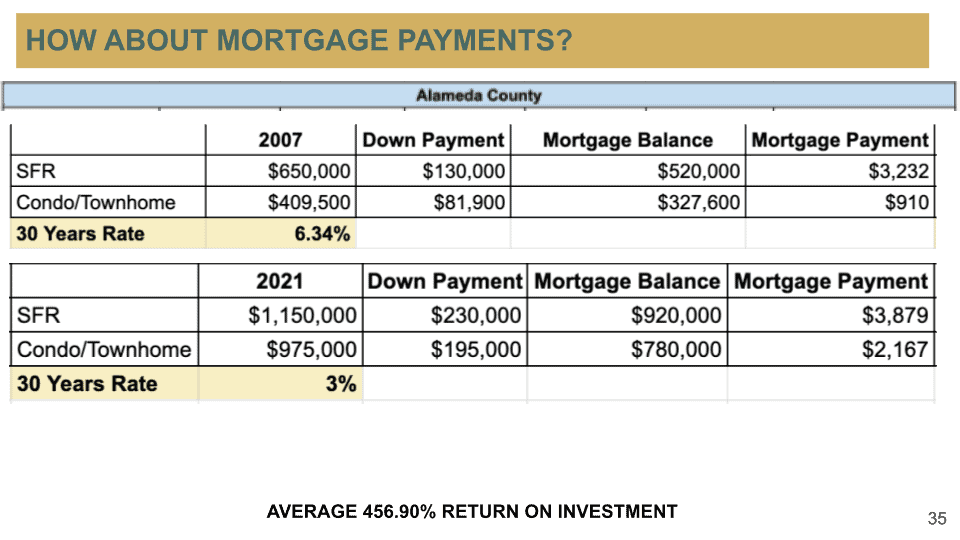

I thought this is even crazier when you look at Alameda County at 6.34% your mortgage payment would have been $3,232 and just $600 more and remember what was the appreciation for Alameda County. The return-on-investment is still several hundred percent right and but then you are only paying $600 more on your mortgage payment here and then condo/townhome this is about $1,200 more for your condo and townhomes but you get well over almost 600% return-on-investment.

Hopefully, this is interesting how these numbers work and how this might change the way you think about whether you should go into the market or not because when I hear a lot of buyers worry about, “Oh gosh! I don’t want to buy at a peak” and things like that, especially, if this is for your own family to live in. I just want to say do not time the market. I have seen too many people in my past 16 years, too many people time their market, they end up paying more just because you know like they did not take action on it. You know, I talked to someone else the other day and then they said like “we never bought, we have just been renting” and they missed out on a million to millions of equity because of that.

Hopefully, this can help change the way you think about the numbers and think about what is the right way to do, but if you are an investor, on the other hand, I am not going to tell you to just go and buy, because if you are investors, especially if you are planning on holding short term, then you have to be really careful and that would be a completely separate conversation.

Thank you for reading the December Bay Area Housing Market Updates, as usual, if you have any comments or questions, please feel free to get in touch with us, we are happy to assist you with any real estate needs.

Stay up to date on the latest real estate trends.

And what to check before upgrading your internet plan

HAYLEN, an Asian-owned, people-first real estate firm, selected to steward real estate process for J-Sei Home’s next chapter

You’ve got questions and we can’t wait to answer them.