October 2020 – Bay Area Housing Market Effects Amid Mortgage Forbearance, Elections & US Economy

Welcome to the October Bay Area Housing Market Update! This month, we unpacked a ton of statistics to answer some of the most common questions regarding housing market effects caused by Mortgage Forbearance, Elections as well as the US Economy. Watch the video recording here!

For this episode of Bay Area Housing Townhall, we also invited Nathan Donato-Weinstein, Economic Development Officer of the City of San Jose, to talk about the city’s plan to facilitate opportunities and economic growth amid COVID-19. You can find the full webinar recording here.

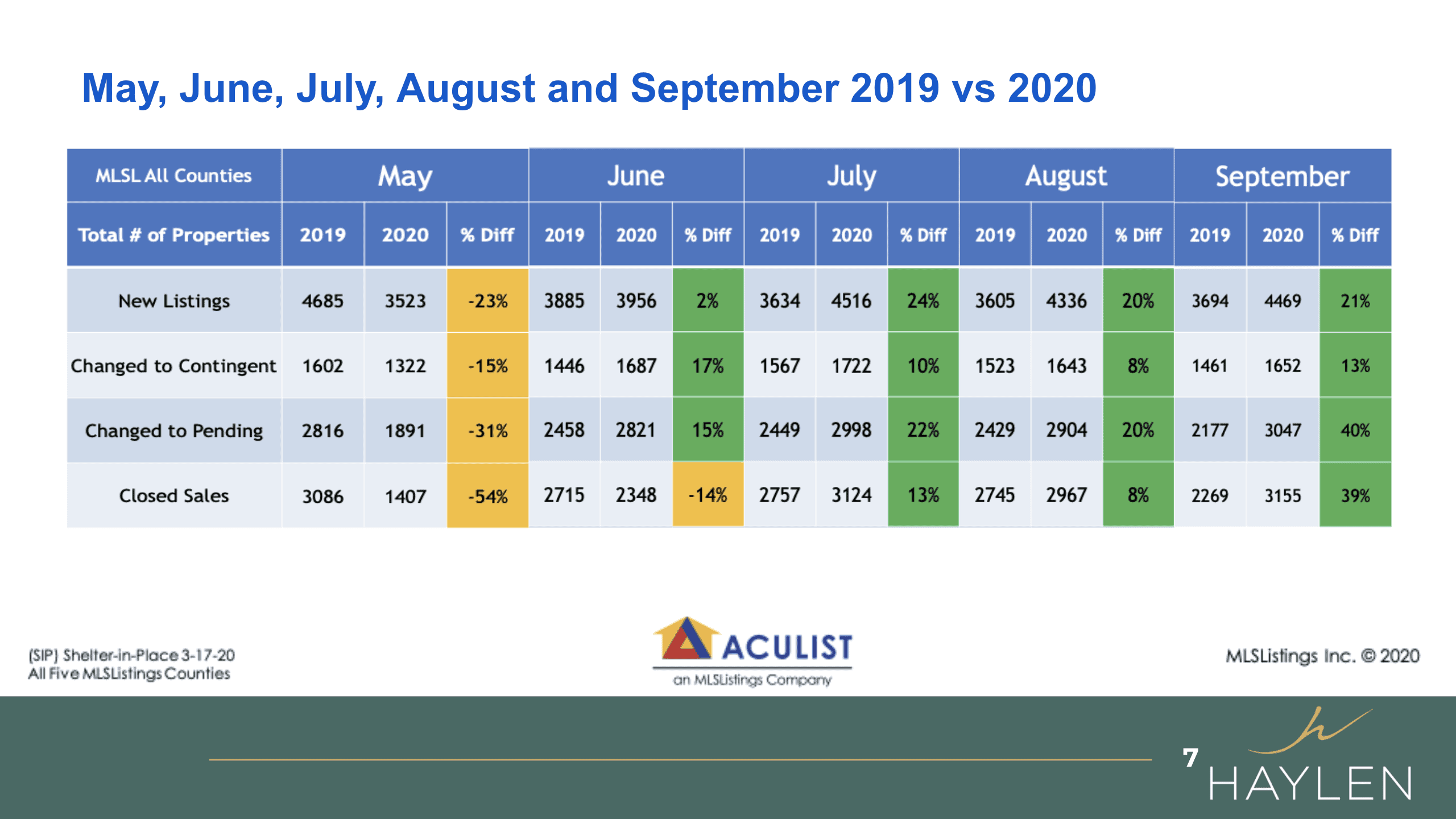

Let’s start to talk about our state of the market. I had spent hours preparing these slides today, and I wanted to show you guys here, I kept stacking it on, you guys probably have seen this before, but as you see, we are doing really well. We continue to add more new listings, and for the month of September, you see that we also have more close sales compared to 2019. These are numbers from all five counties in the Bay Area.

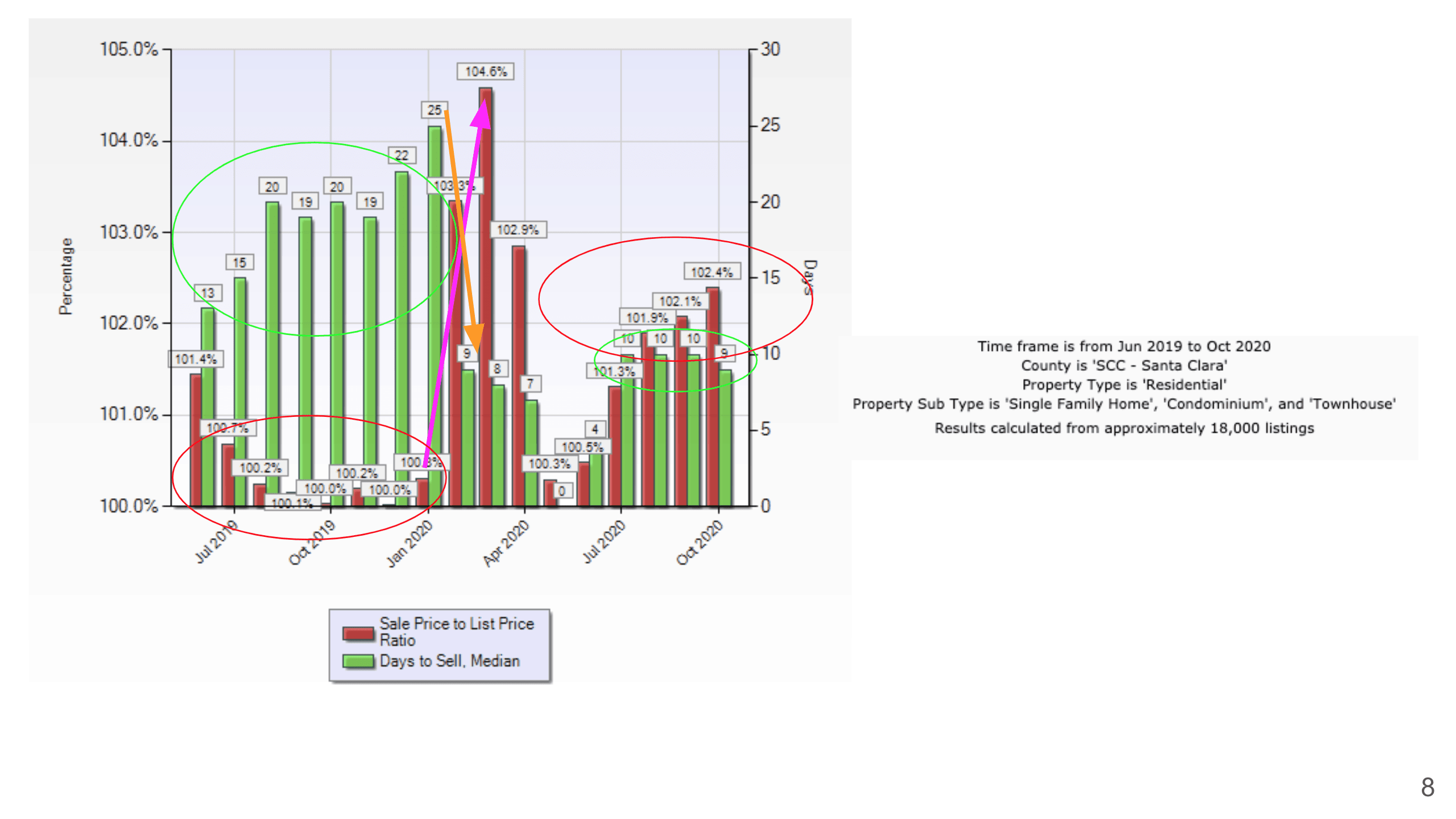

Now if we look at this chart, it is for San Clara County from June 2019 to October 2020 with all the residential properties. As you see that the green represents the median number of days on the market. You see that last year it stayed on the market much longer, almost double the number of days for this year. If you look at how people are offering, how competitive the market is. Last year was not as competitive as this year, and this year we definitely have more competition, more multiple offers. In the following slides, we’re going to explain to you why this has been happening. One thing I thought extremely interesting is that if you look at this part how the offer price over the sold price had jumped up so much in January, February, and March 2020, so people really, even before COVID, have already started buying and they have come out very aggressively. We’re gonna take a look at why this is happening.

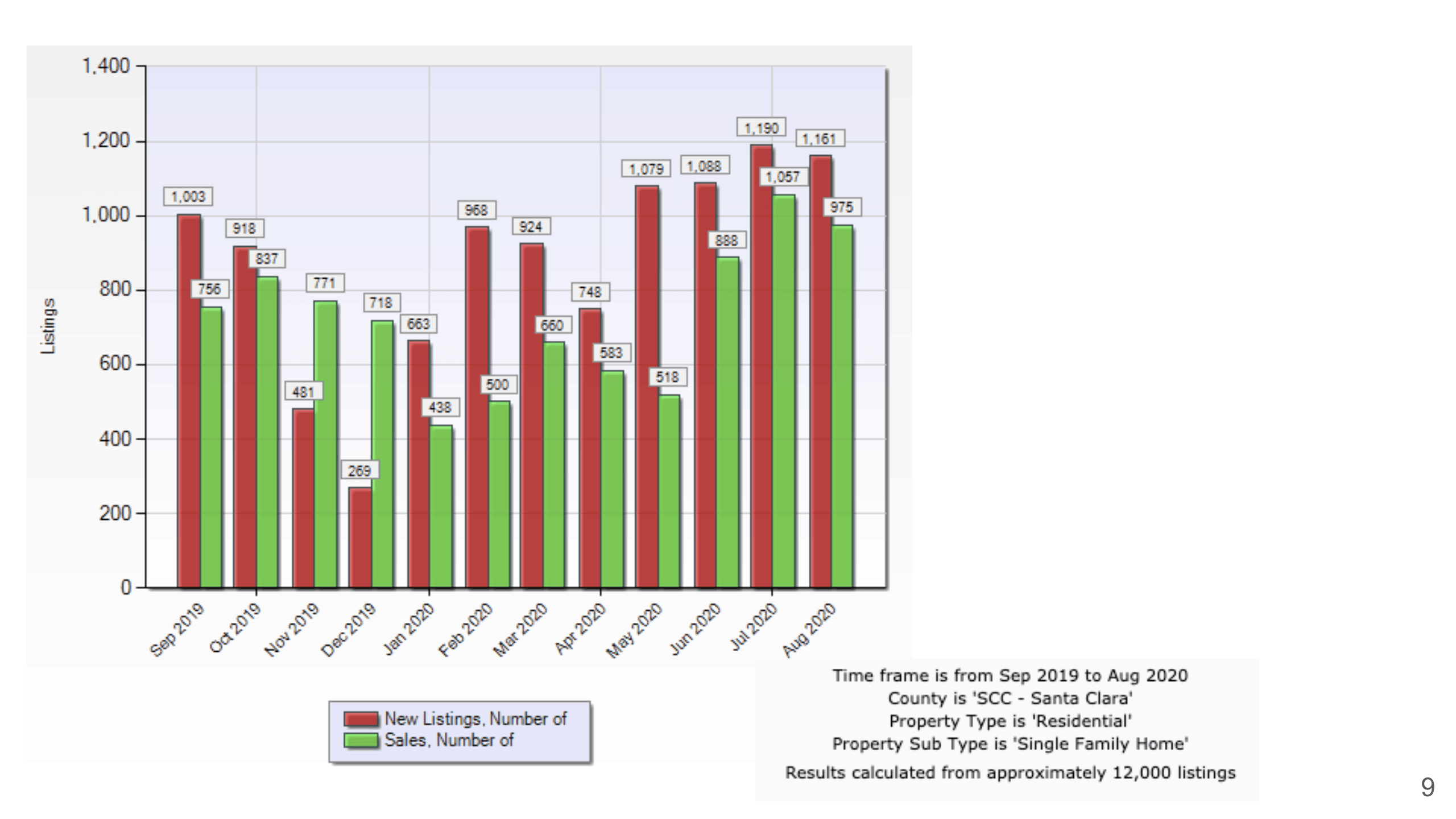

So here is another chart where we’re going to look at the number of sales and the number of new listings. We definitely have a lot more new listings and also we have a very strong number of sales in Santa Clara county.

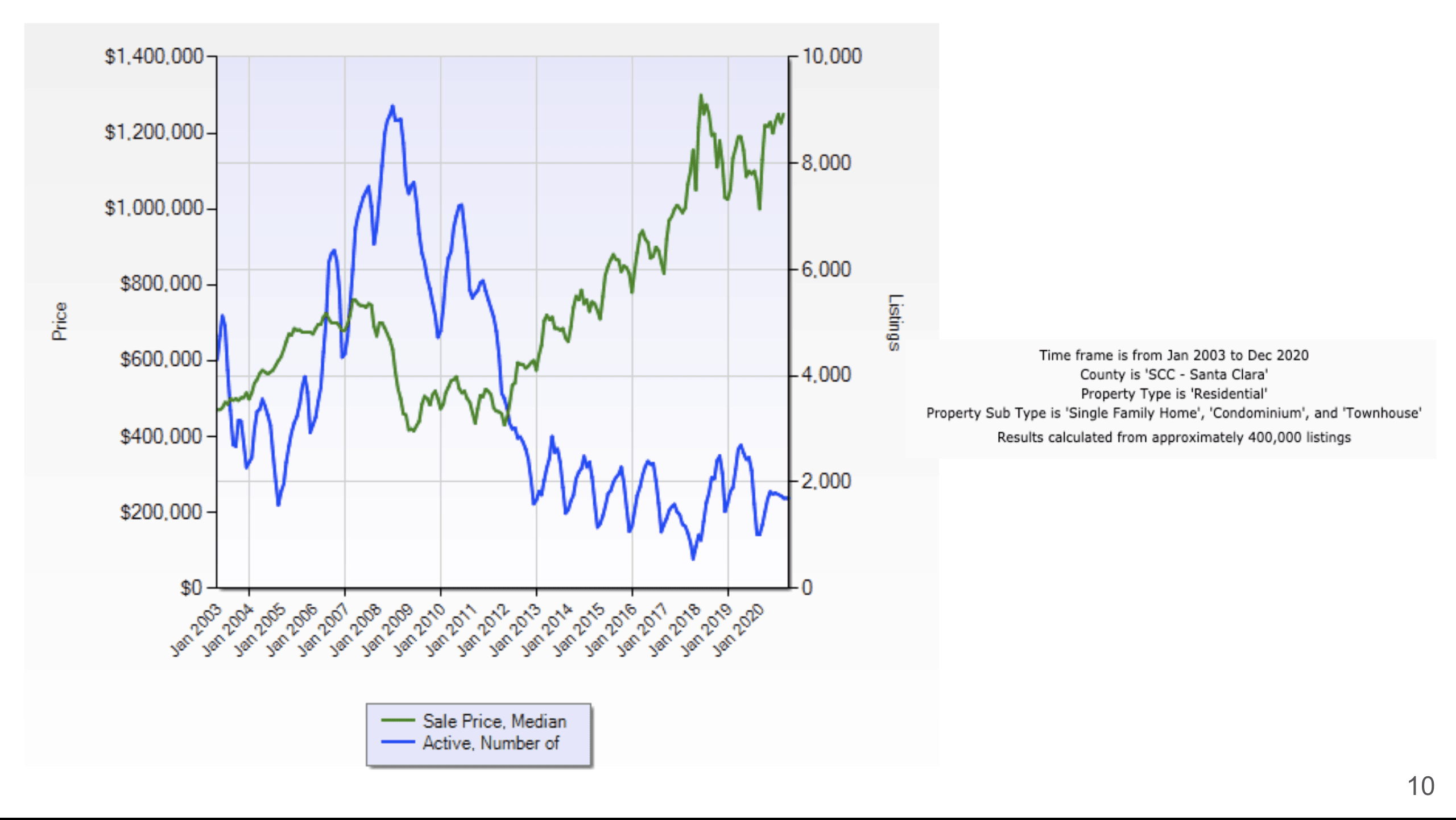

This chart is showing us all the median sales price versus the number of active listings. So the green line here is showing the median sales price. Starting from 2003, it has been going up and we have gone through some, you know, downturn over here in 2009, but as you see that around 2013 we have already come back to the previous peak, and since then it has gone above and beyond. Then the active number of listings though, as you see, actually has gone down. Our supply is really at a historic low right now. We have so many people who need to buy, but we don’t have enough listings to sell. That’s why the market has been pushing the prices up because it’s simple – supply and demand. When you have a very low supply, your price is going to go up.

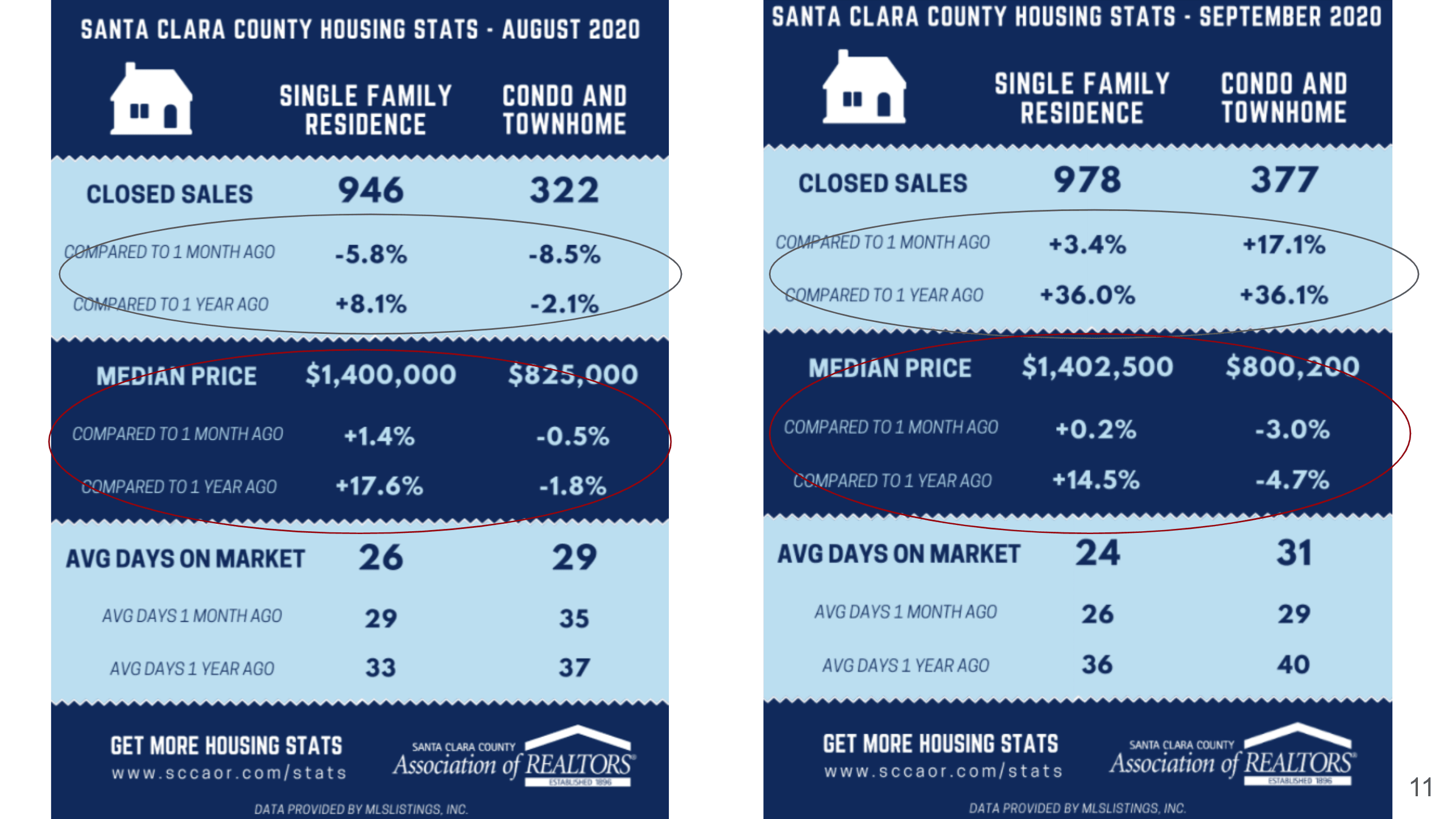

Here is a chart comparing last month and this month’s number, where you see the single-family residence in Santa Clara County (this is provided by Santa Clara County Association Realtors), we have more close sales compared to last month, and compared to last year we have 36% more. The right side is talking about the condos and we have 36% more closed sales for condos as well. The medium sales price is hitting 1.4 million dollars for single family, and $800,000 for condos. The price had gone up for the single family, but you’ll see that the condors actually have come down. We’ve been explaining to a lot of our clients that because of this shelter in place, people spend so much time inside the house, and now you really do need a much bigger space. Also, people want their own space and less common areas, so that’s why we noticed a huge shift of our buyers looking for a single family compared to condos these days.

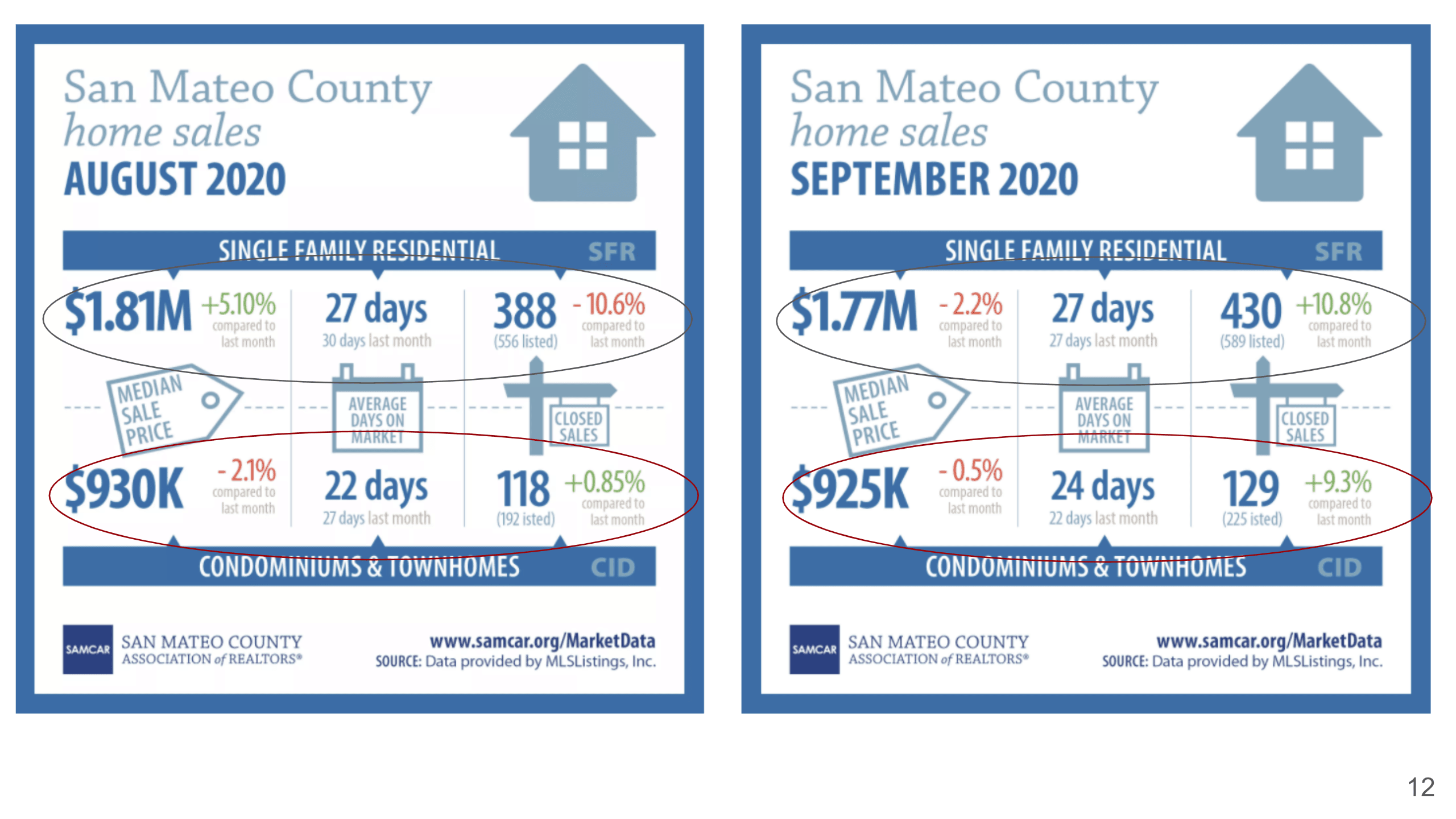

Now San Mateo County here, you’ll see that actually, the price has gone down. In August the median sales price was $1.81 million, but in September it had gone down to $1.77 million. However, they still have very strong sales – they have a lot of close sales, 430 in September compared to 388 in August for single-family residents. The price for the condos has come down as well, the days on the market are slightly higher, but there are still more condos that have been sold compared to August.

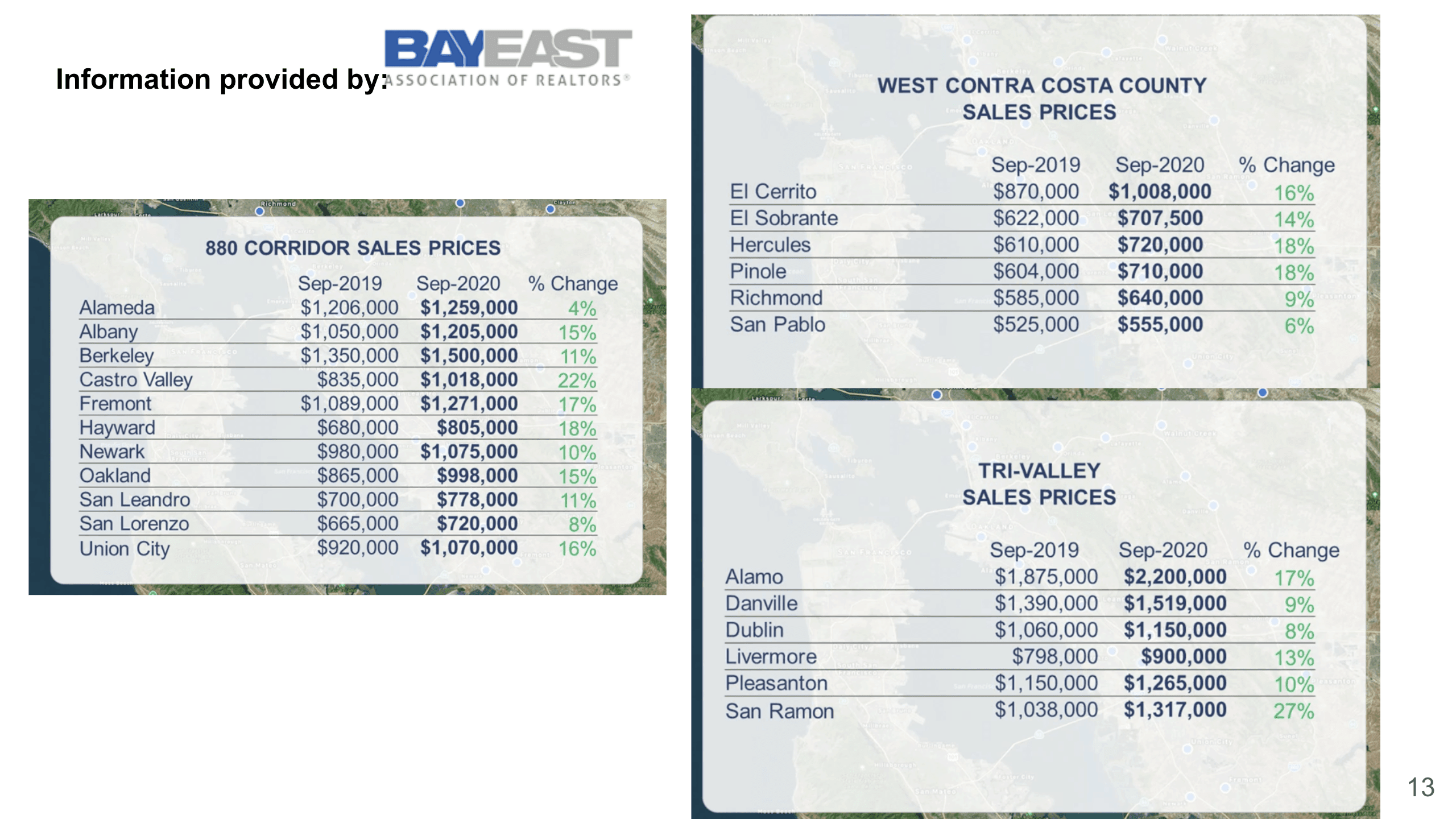

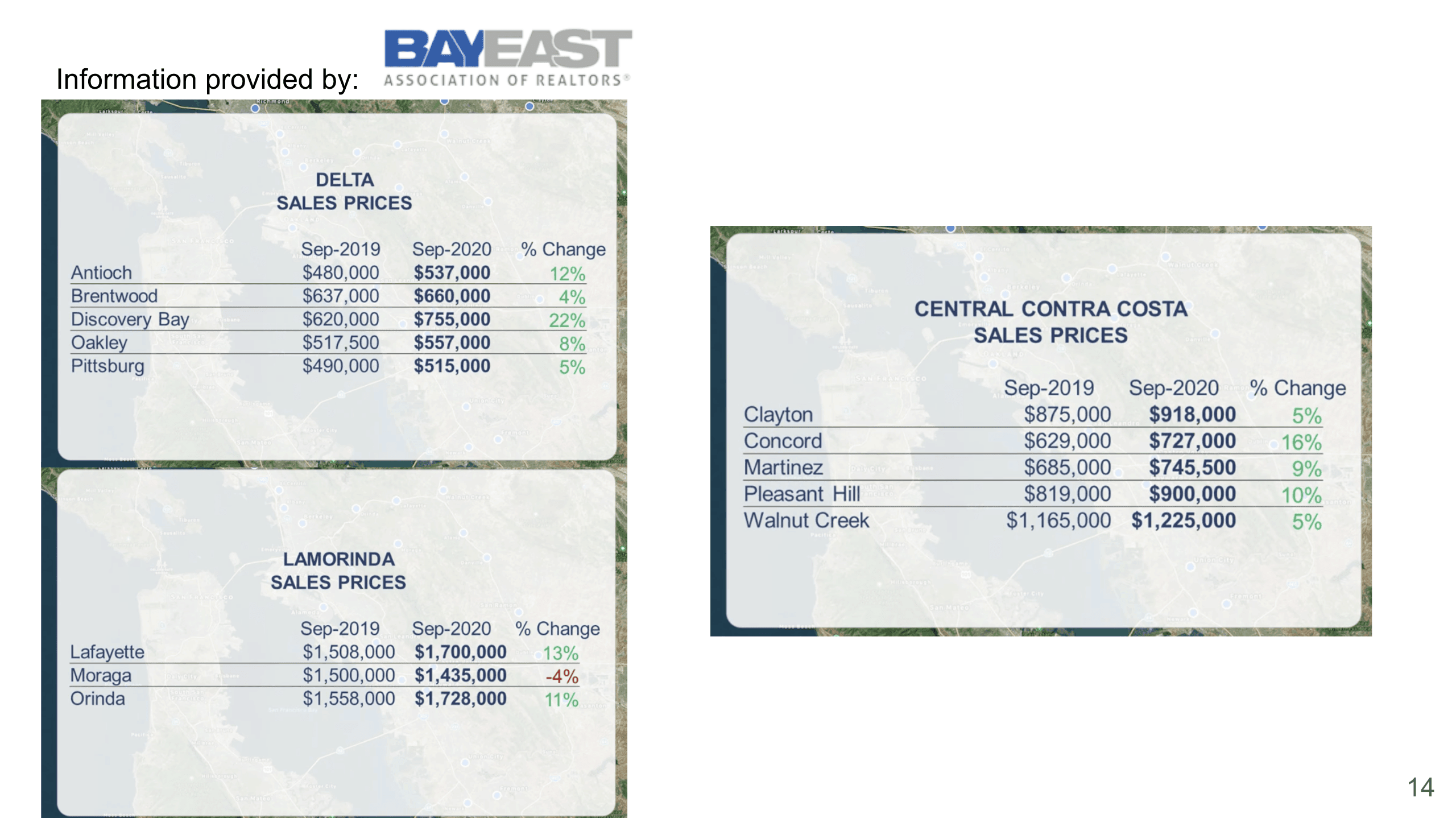

This one is provided by Bay East Association Realtors, and it covers numerous areas, so I’m not going to go over every single city here. But as you can see that compared to 2019, you see all green numbers, these are all increase in the sales price, so you see that they are all going up quite a bit since last year.

Same thing all the way from the more inland and also the North Bay Area. Most of the sales price had gone up as well besides Moraga, which is the only one that has come down slightly.

Now, what about the economic market updates? What’s gonna happen? So many clients, so many buyers, and even sellers are asking us – what do you think about the market? You know, do you think that the market is gonna come down? I heard rumors that it’s gonna crash because of the election, because of the forbearance. So I want to answer some of these questions through these slides.

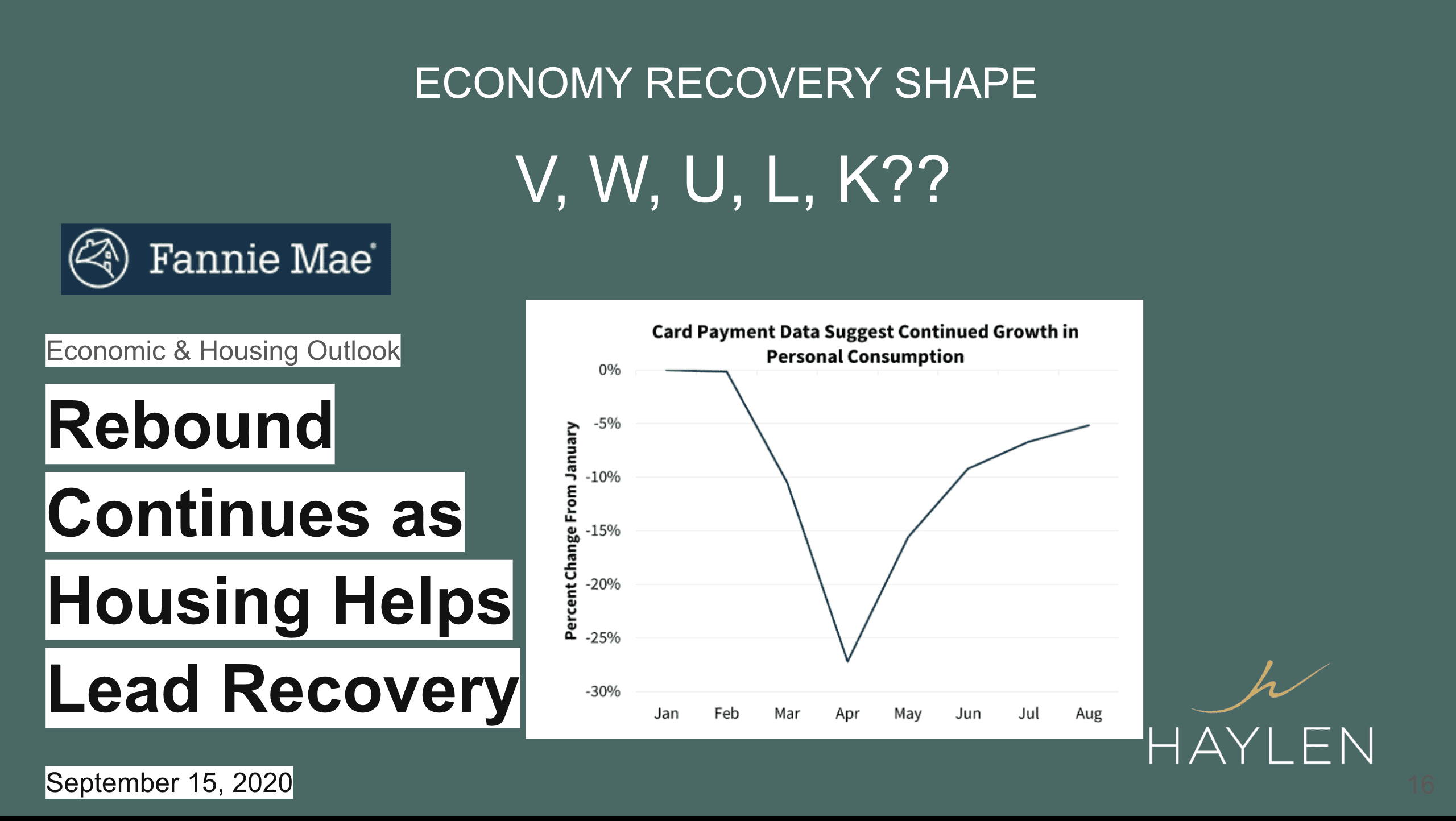

One of the most interesting things is that, since the beginning, all these economists and you hear a lot on youtube videos, they’ve been trying to predict what kind of recovery shape we’re going to be in. Are we going to be in a V shape, W shape, U shape, L shape, and now politicians are talking about K shape. As you see here, Fannie Mae, which was actually awarded as the most accurate forecaster, had said that this is more of a V-shaped recovery.

Just a couple of days ago, the chief economist for the IMF had an interview on CNBC and this is what she said:

“Our baseline assumption is based on no further stimulus. We have done the calculation, if there is a stimulus which is about the size of the CARES act, we will add about 2 percentage points to growth in 2021, which means instead of the US coming back to 2019 level in 2022, it will actually return much faster in 2021 back to the 2019 level”.

So whether we are going to get the stimulus package is a really big factor to consider in terms of how our economy is going to recover.

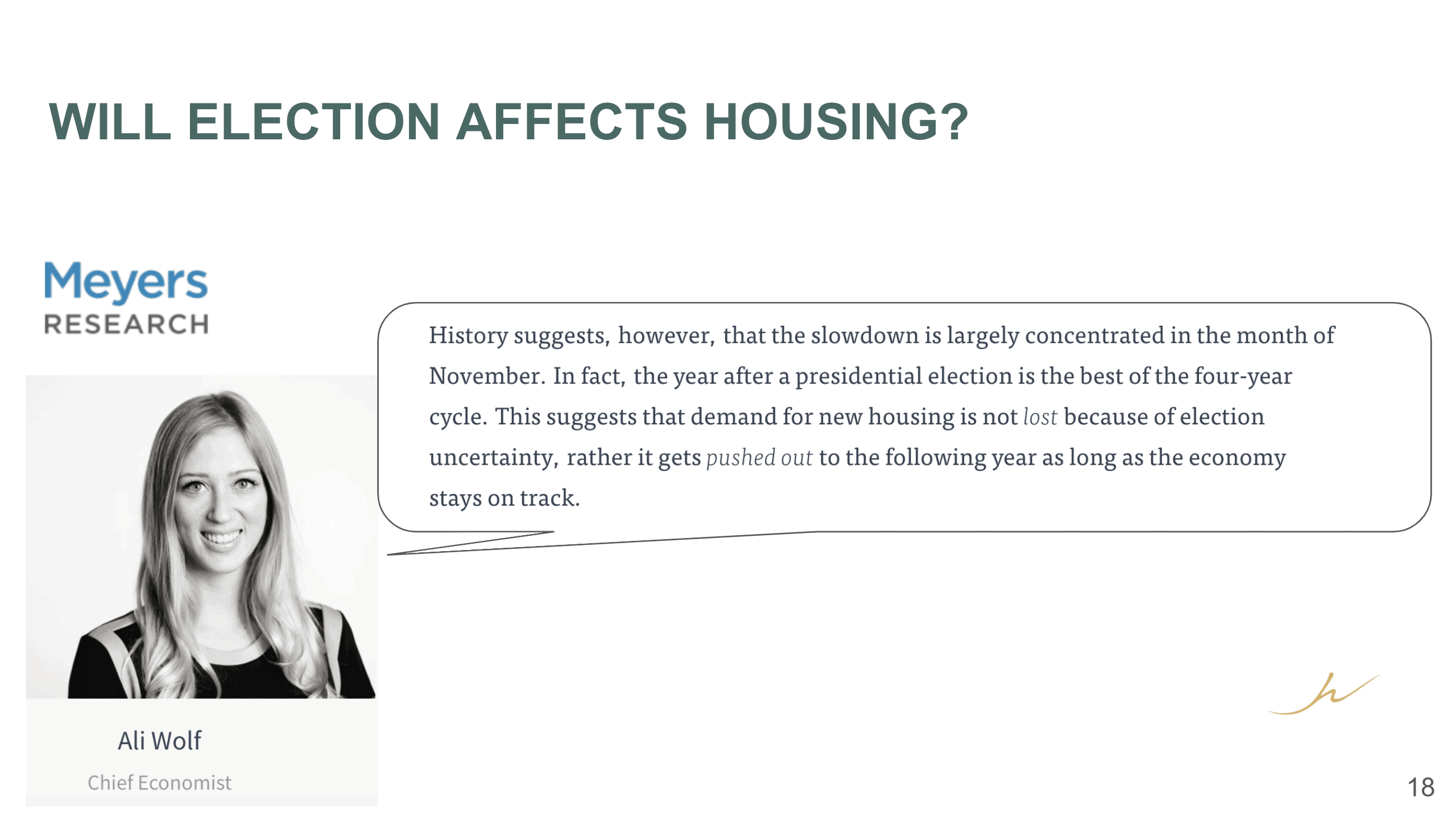

And what about the election? Is the election going to affect housing? So Ali Wolf, the chief economist from Meyers Research, said:

“History suggests, however, that the slowdown is largely concentrated in the month of November. In fact, the year after a presidential election is the best of the four-year cycle. This suggests that demand for new housing is not lost because of election uncertainty, rather it gets pushed out to the following year as long as the economy stays on track”.

She had actually talked about in this article that they had gathered all the past 50 years of data to come up with this conclusion. We see that ourselves too that almost every time if there’s an election coming up, the market slows down a little bit, and then right after the election is over, no matter who wins, the clients come back to look. It doesn’t mean that they’re not looking anymore, it’s just that a lot of buyers or sellers are just not comfortable with that uncertainty, and that’s why they’re pushing out that decision to buy or sell later.

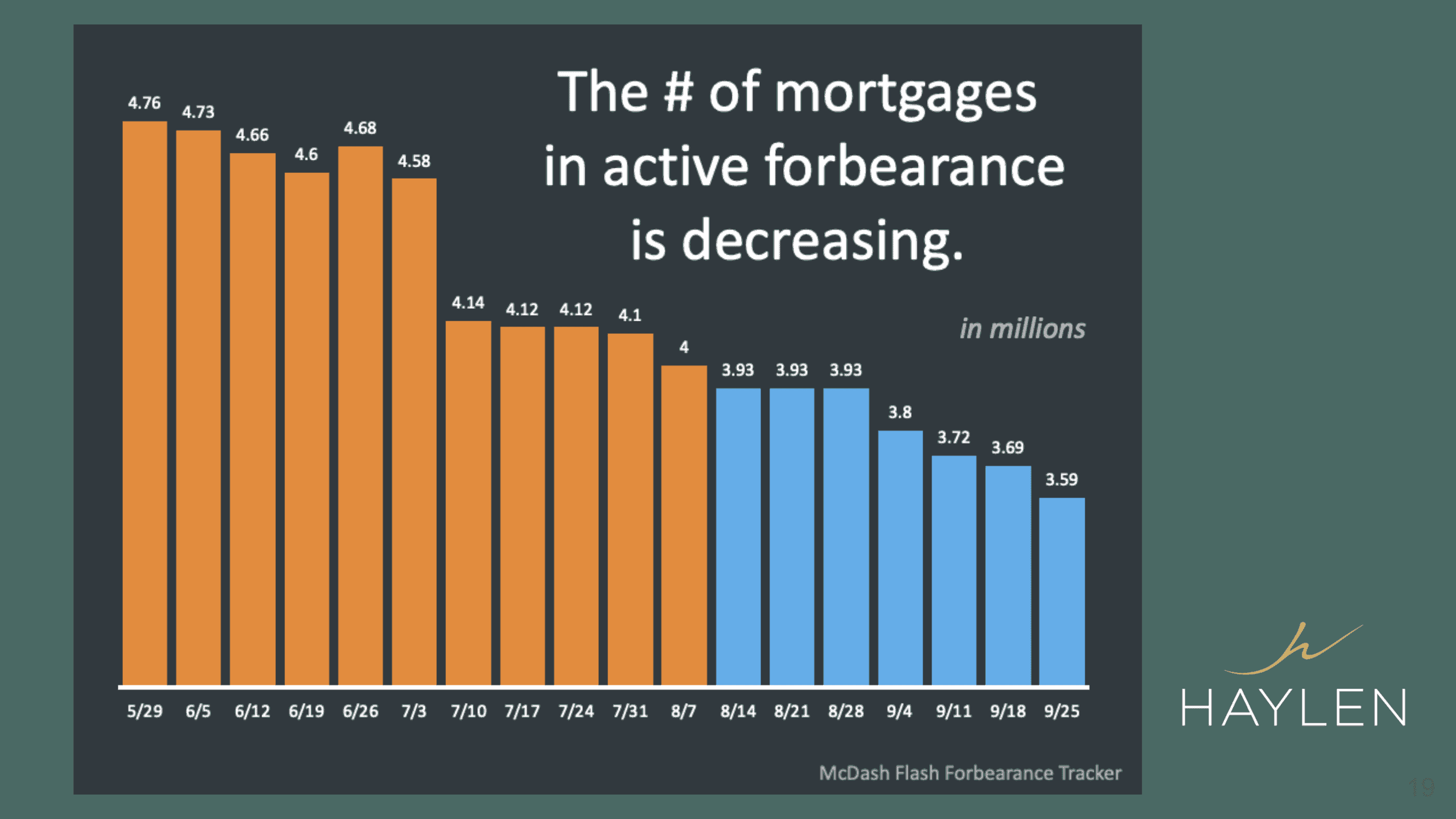

What about forbearance? As we see on this chart, the forbearance actually is decreasing right now, and we do know that some of the property owners are applying for forbearance based on, you know, they said – well it’s offered to me then I’m gonna take it just in case, just in case something happens, if it goes and it’s not coming back, or they are not making any income anymore. But we do see that the number of active forbearances is actually decreasing.

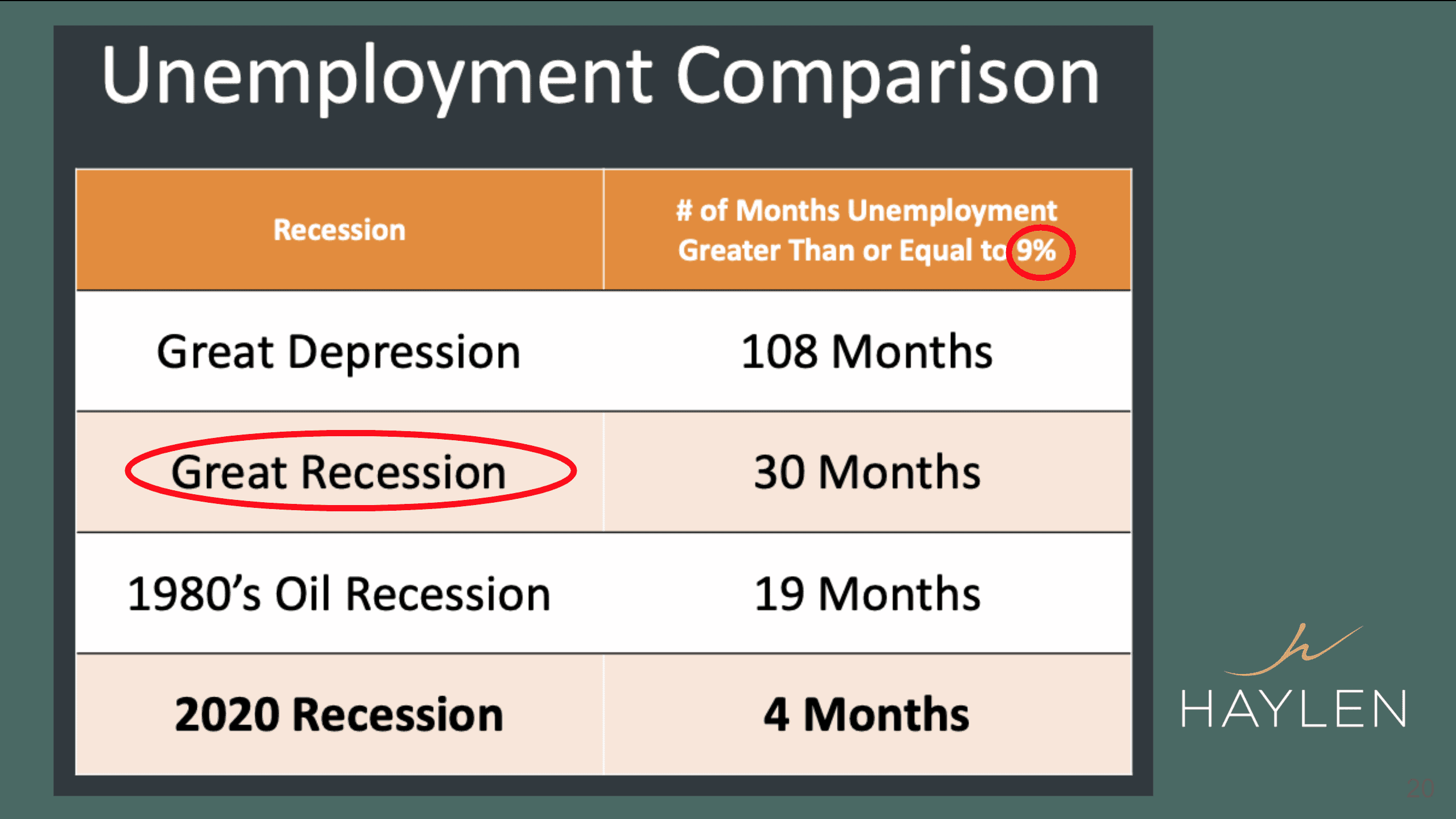

I know people are still really worried because of unemployment, and as you see here, the number of months of unemployment greater than or equal to 9% in these recessions. The Great Depression lasted about 108 months, our last recession, the Great Recession lasted about 30 months, and the 1980’s Oil Recession lasted about 19 months, and the 2020 Recession lasted about 4 months.

Many still think that a lot of people are going to file for foreclosures. I started my career in 2005, so I definitely have gone through the Great Recession at the time because of the mortgage crisis. At the time, actually, a lot of our buyers were buying with no money down or 5% down, and we even had a loan program that offers 105% of the market value. So you’re not only not putting any down payment, you’re actually getting money in order to purchase at that time.

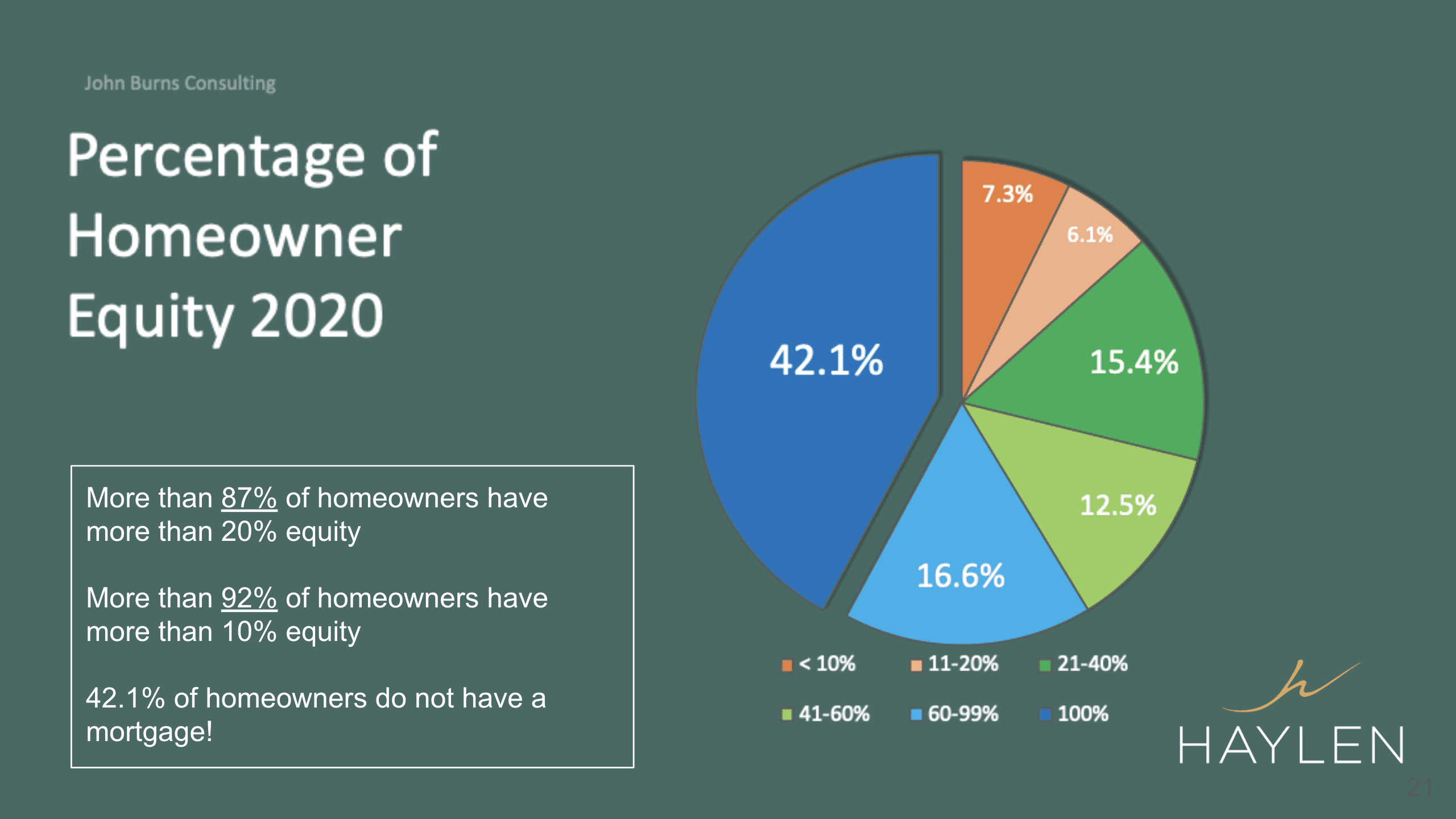

Now, look at this chart, it is talking about the percentage of homeowner equity in 2020. More than 87% of homeowners have more than 20% of equity, more than 92% of homeowners have more than 10% equity, and 42.1% of homeowners actually do not have a mortgage, which means they have 100% equity in their property.

So what does this mean? The previous recession was due to people just giving up their property, they’re going to foreclosure. However, this time even though they have filed for forbearance, firstly, the banks don’t want to take back the properties, secondly, because a lot of homeowners do have equity in their property, they can just put back on the market to sell it. That’s why we don’t think that this is going to cause a lot of foreclosures, and we do believe that because the housing market is healthy enough, a lot of homeowners will be able to either keep their property or refinance into a lower interest rate. Especially in the Bay Area, our markets are unique and a little bit different, so that’s why we really do not think that we’re going to have a high foreclosure rate.

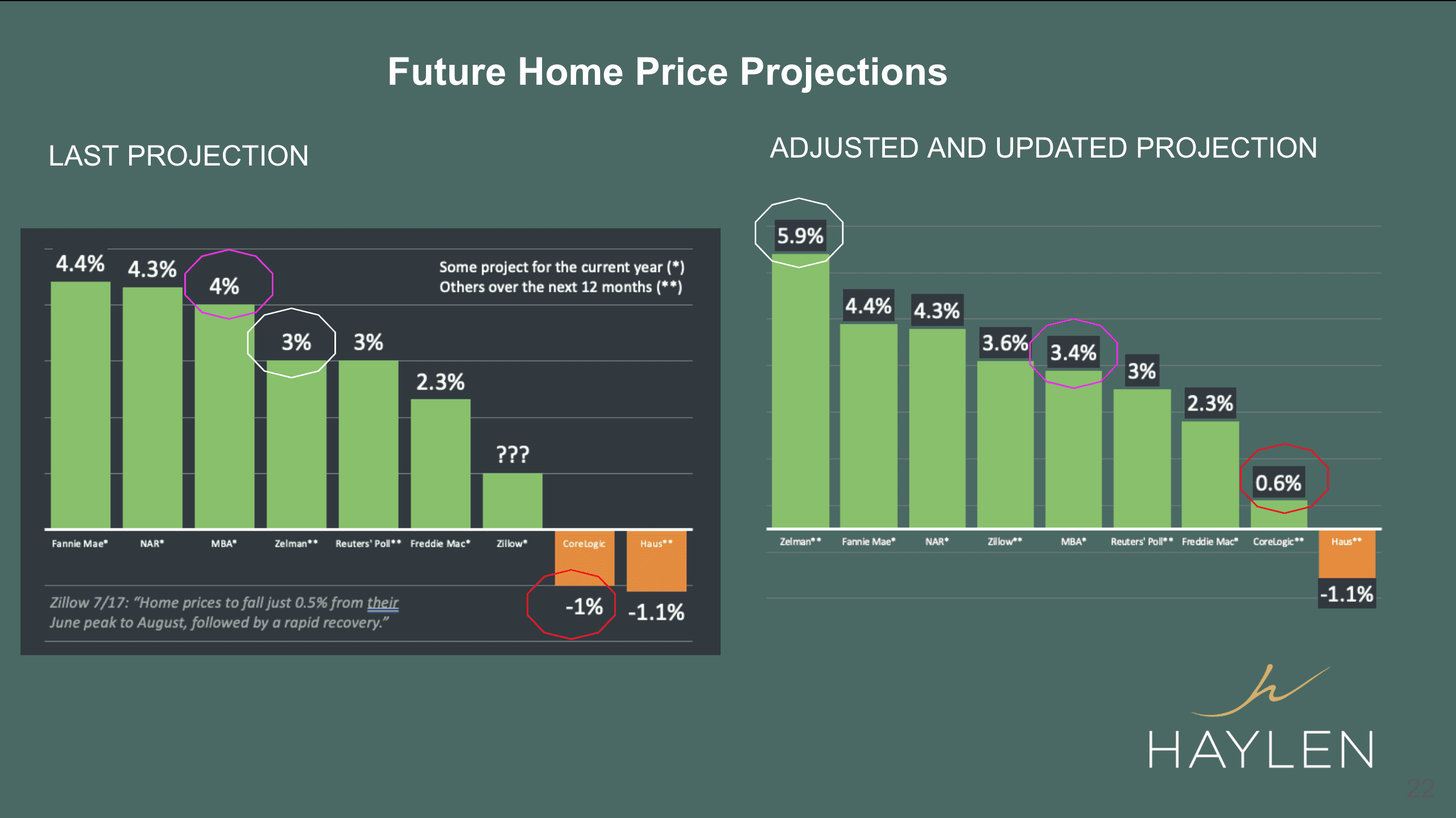

Now here, of course, that was just me talking, so I want to see what other organizations are projecting on the home prices. We have Fannie Mae, National Association Realtors, Mortgage Banking Association, etc., they have made their projection. I’m putting these two charts together because there’s one that is from the last projection and the other one is more updated. As you see that the Mortgage Banking Association used to project about a 4% increase in home prices, they did come down on their projections to 3.4%. But Zelman just adjusted their projection from 3% to 5.9%, they’re very optimistic about the economy and the housing market. Another one is CoreLogic, they went from negative 1% to actually positive 0.6% increase on the home prices projection, so that is definitely a very positive outlook.

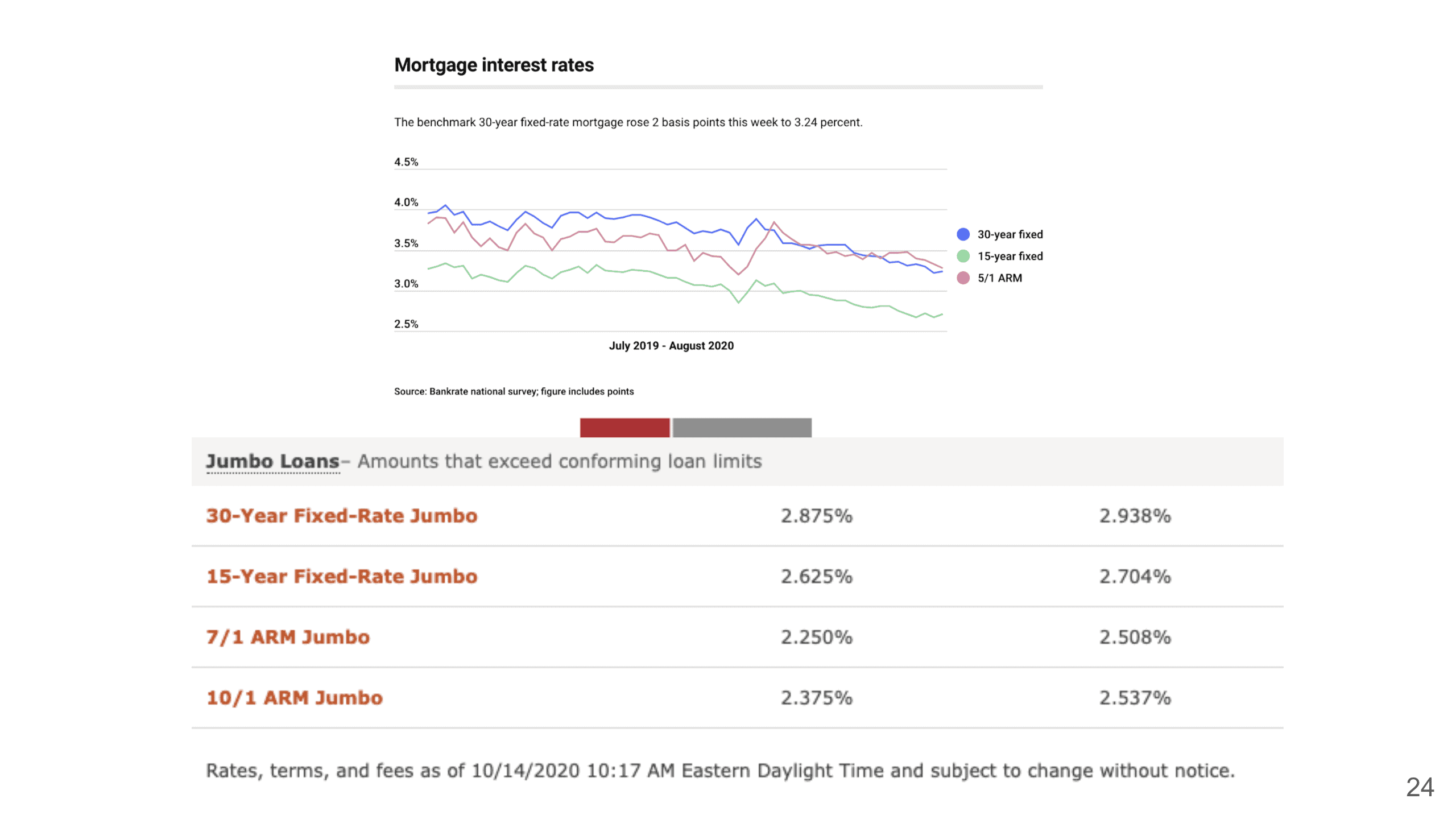

As for the mortgage market statistics, currently the 30 years fixed jumbo rate has come down to 2.875% as of today, October 14th. I remember when we first started we’re talking about 3.25%, and now it has come down to 2.875%.

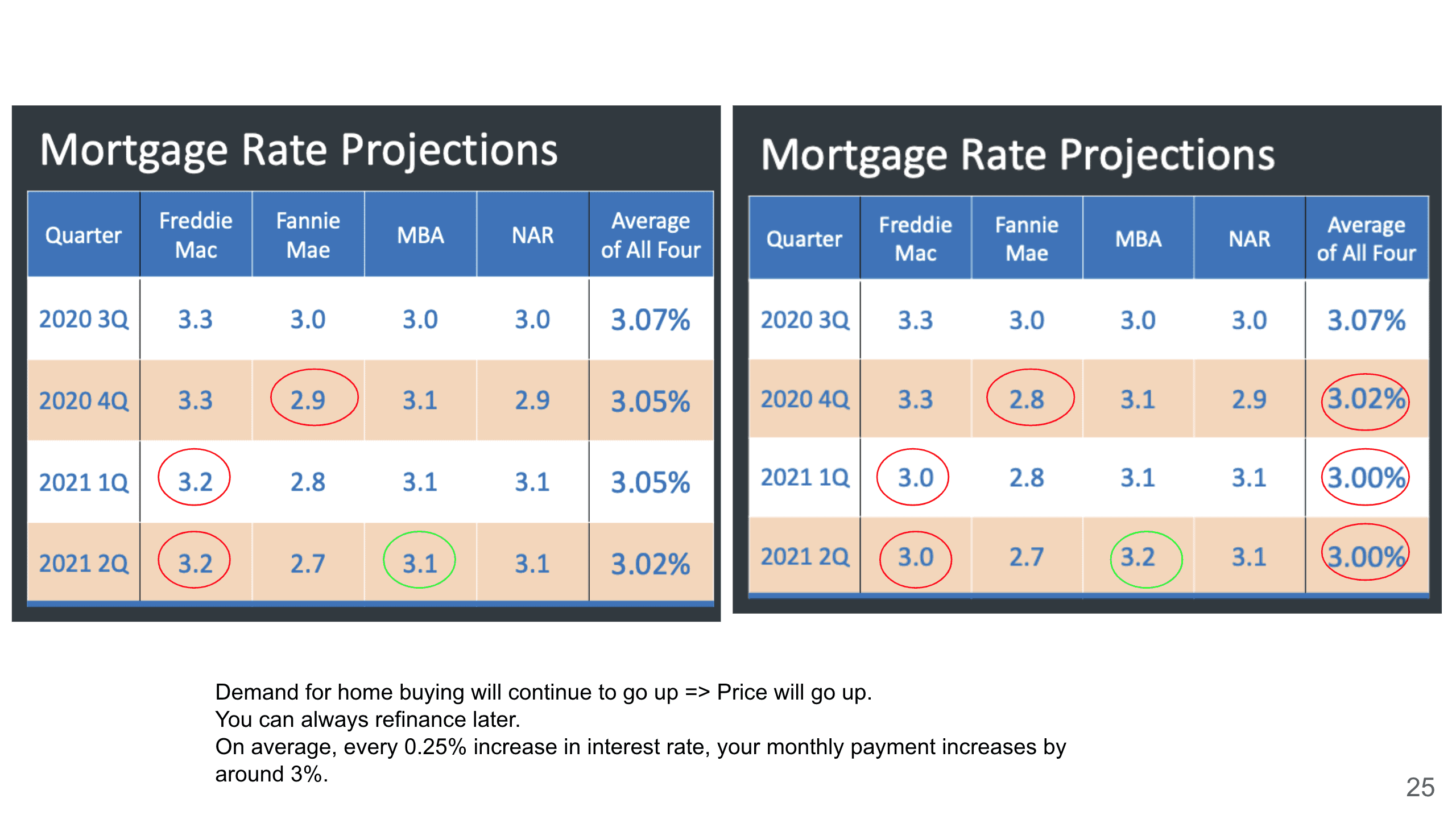

Here is the mortgage rate projection, the same thing. Freddie Mac had come down on the projection, expecting the rate to come down to 3.0% all the way through 2021 2Q. Now here’s the question, because the interest rate has come down, the demand for home buying is going to continue to go up, and then the price will go up. Now, why is it that as the interest rate comes down, there will be more demand? Because your monthly mortgage payments actually increase by around 3% for every quarter percent increase on your interest rate.

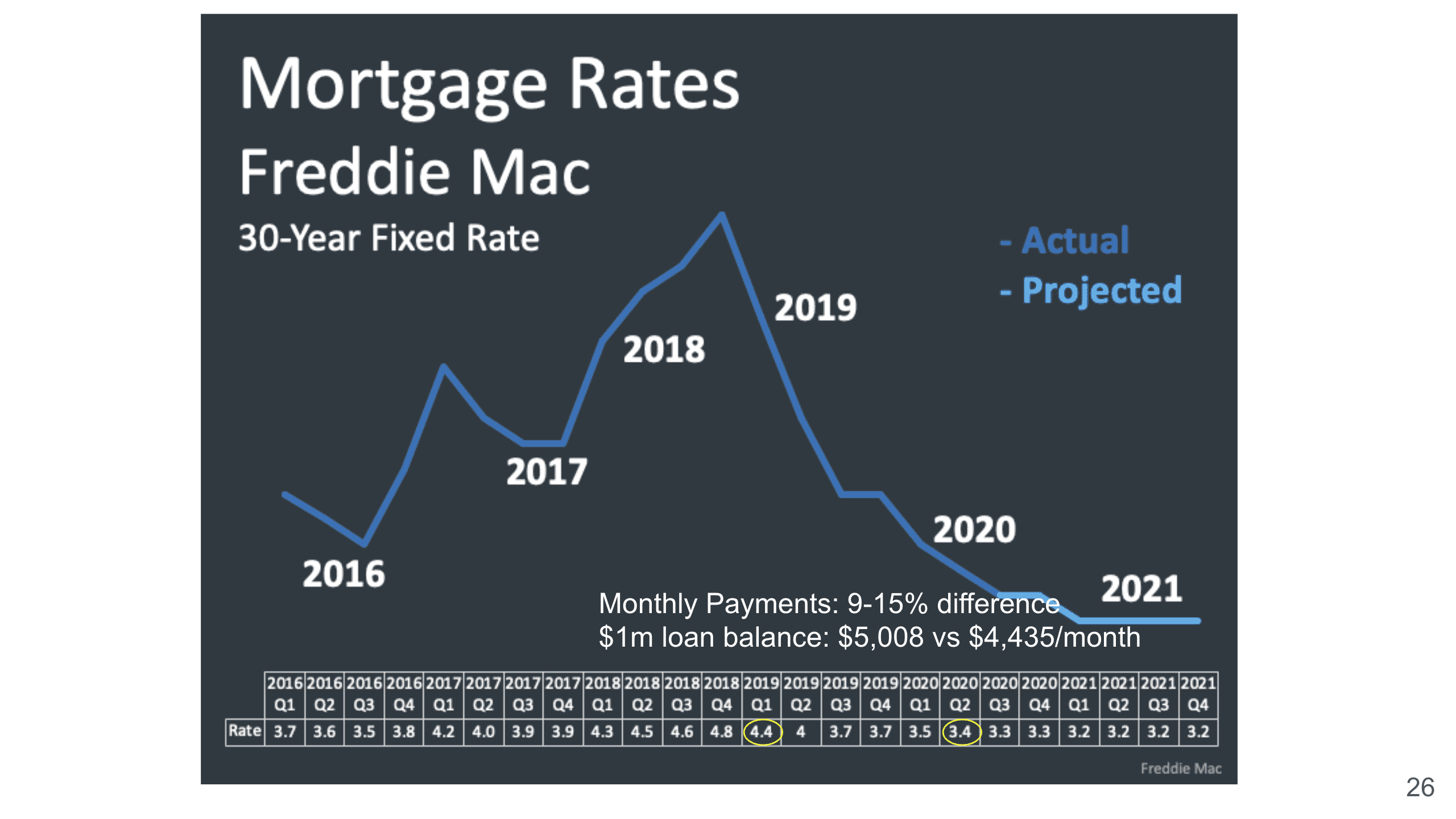

So maybe we can take a look at this chart instead. Looking at 1Q of 2019, it was at 4.4%, and then 2Q 2020 had come down to 3.4%, which was 100 basis points lower. What that means is that your monthly payment actually can make about a 9% to 15% difference depending on your loan balance. So with a one million dollar loan balance, that’s almost a $600 difference in your monthly payment. This is the reason why so many people came out to look for properties because you can’t get this kind of rate in the future, it is our historic low. I’ve never seen a rate like this, I personally just refinanced as well for my house, and now our monthly mortgage payment is so much lower than before. So I truly highly recommend that you don’t wait at home buying because I think the prices are going to continue to go up at least for the next year or so.

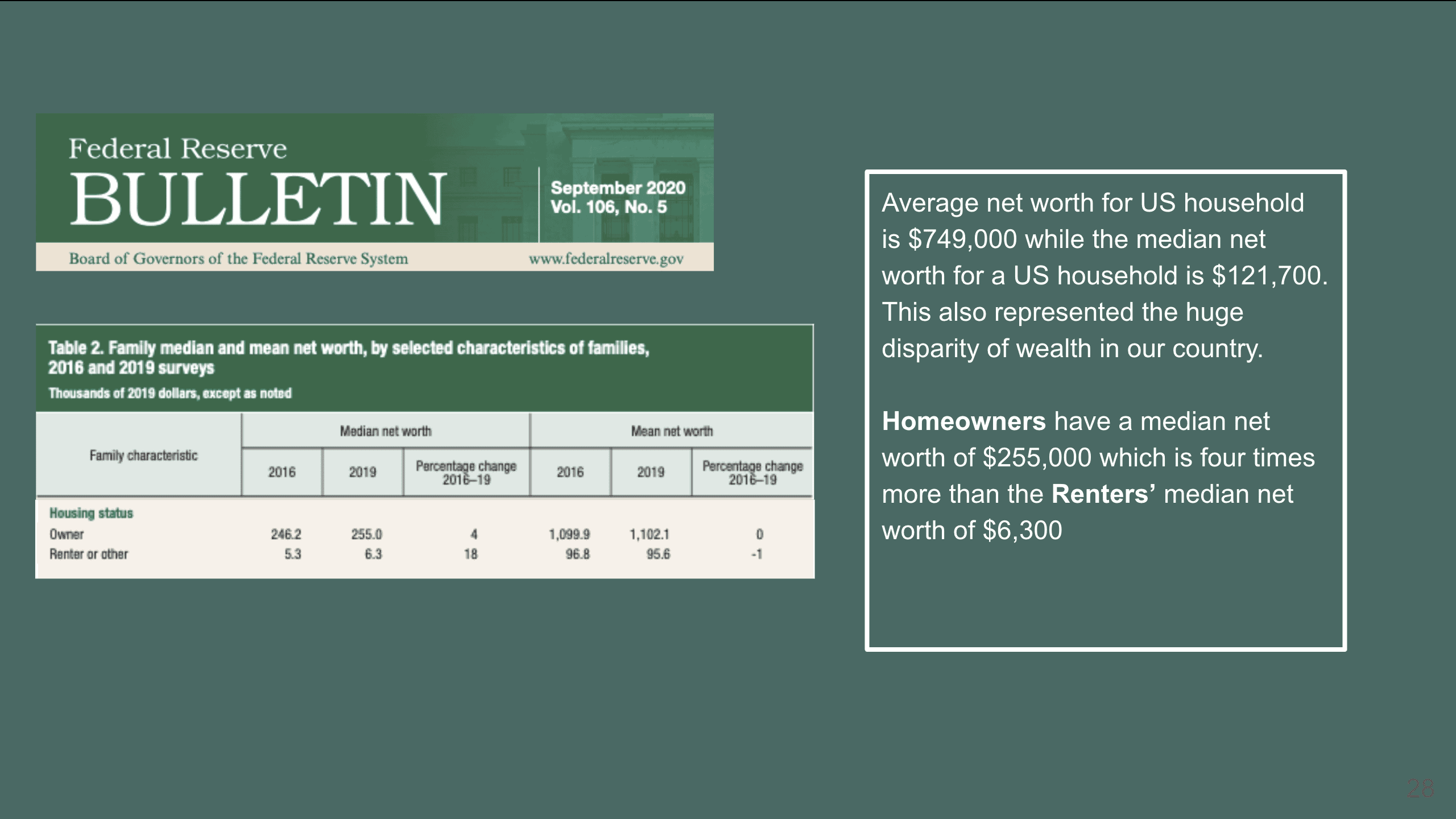

Now multifamily, I’m going to go over this really quickly, but I want to share this with you guys. Federal Reserve, for September 2020, their bulletin has shown that US households have a median net worth of about $121,700, and homeowners have a median net worth of $246,000 while renters have a median net worth of $6,300. You see homeowners have like 40 times more than renters in terms of net worth, so I highly recommend anybody to consider to be a homeowner if you can afford it.

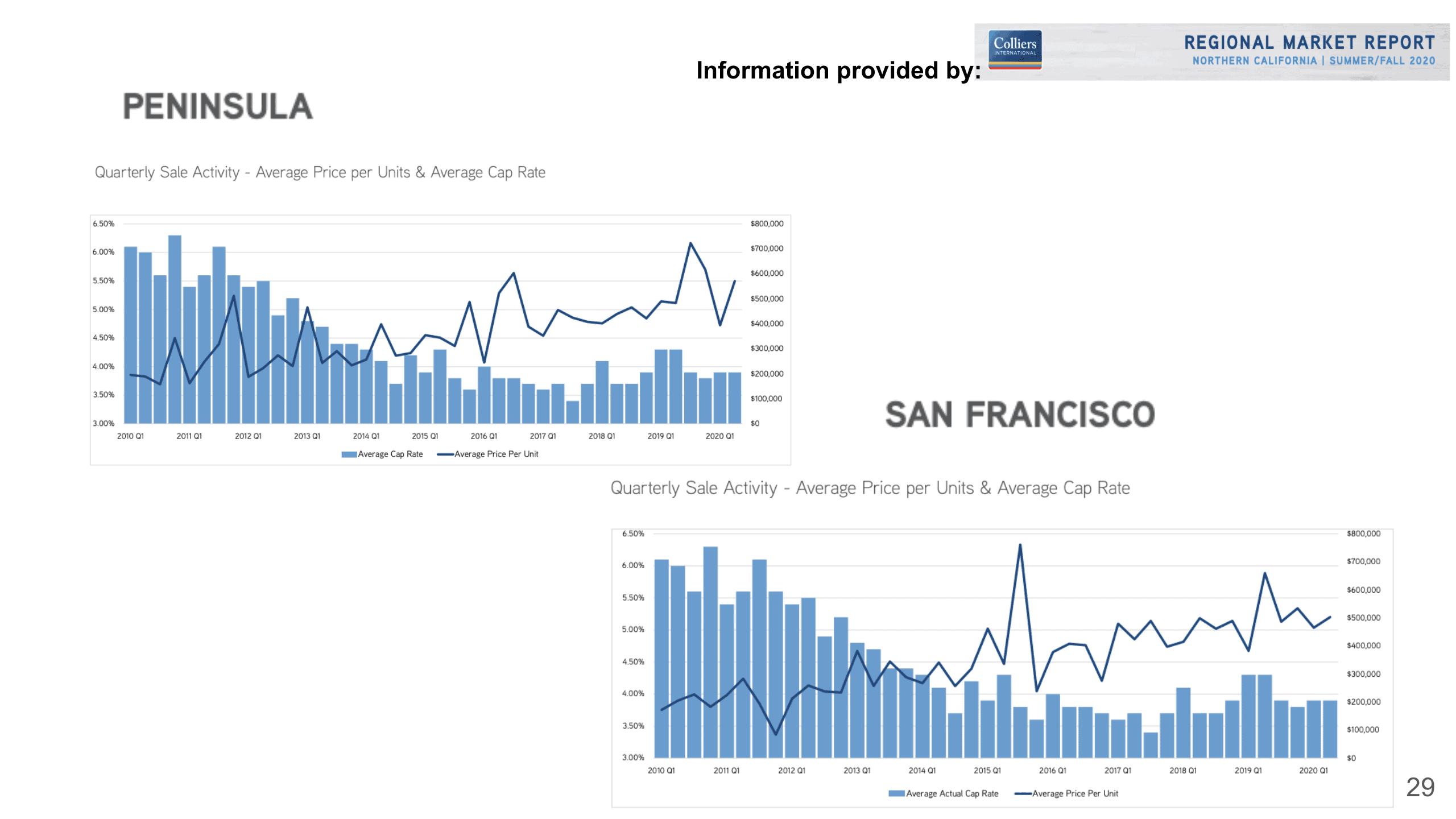

And this is the multi-family activity in the Peninsula and San Francisco. The thing that I like to look at is their cap rate. The cap rate is remaining still very strong at right below 4% for both San Francisco and the Peninsula.

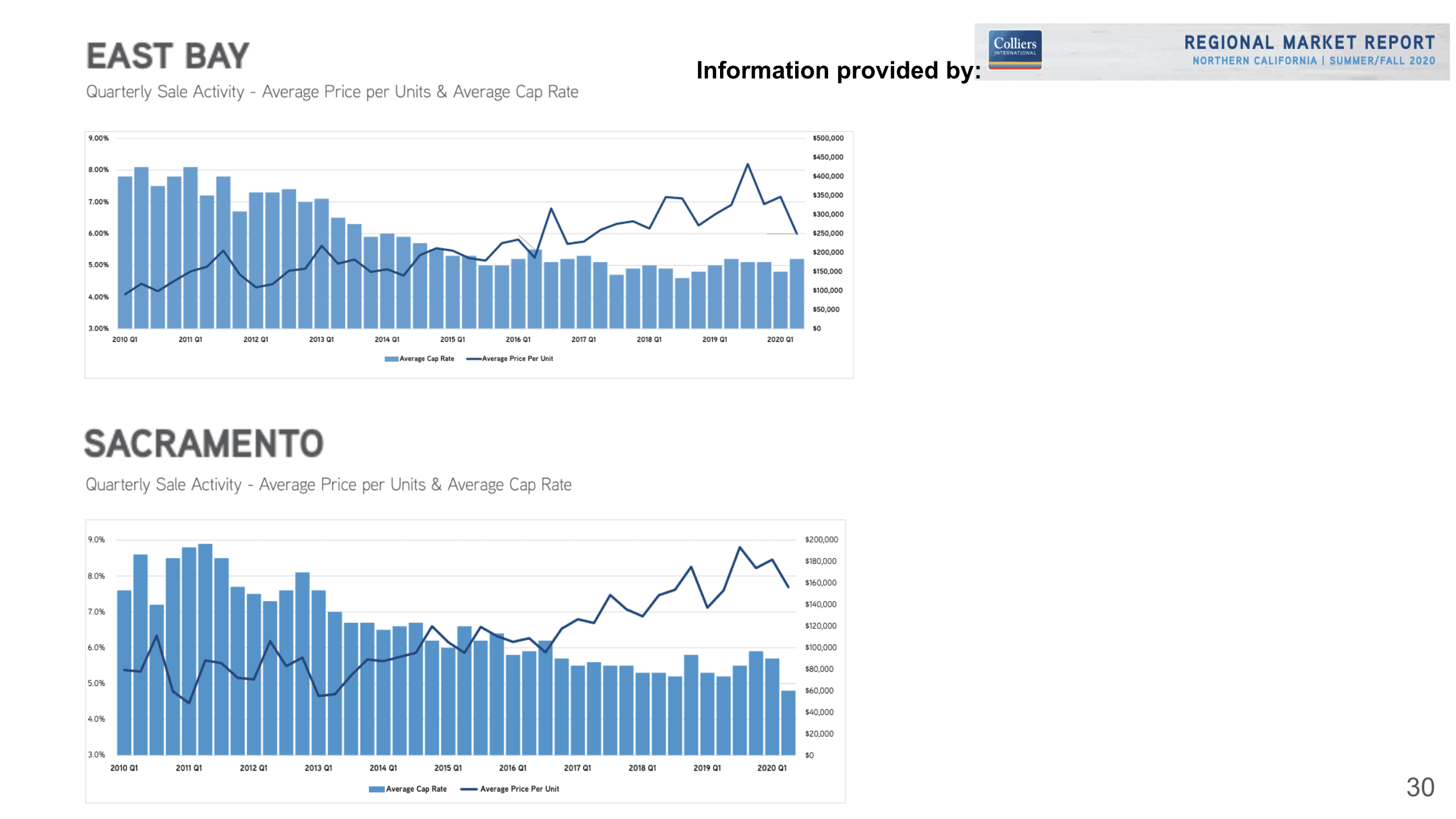

And East Bay, it is a little bit higher, which is slightly above 5% now, and then for Sacramento, it is about 5% as well, actually slightly lower than 5%.

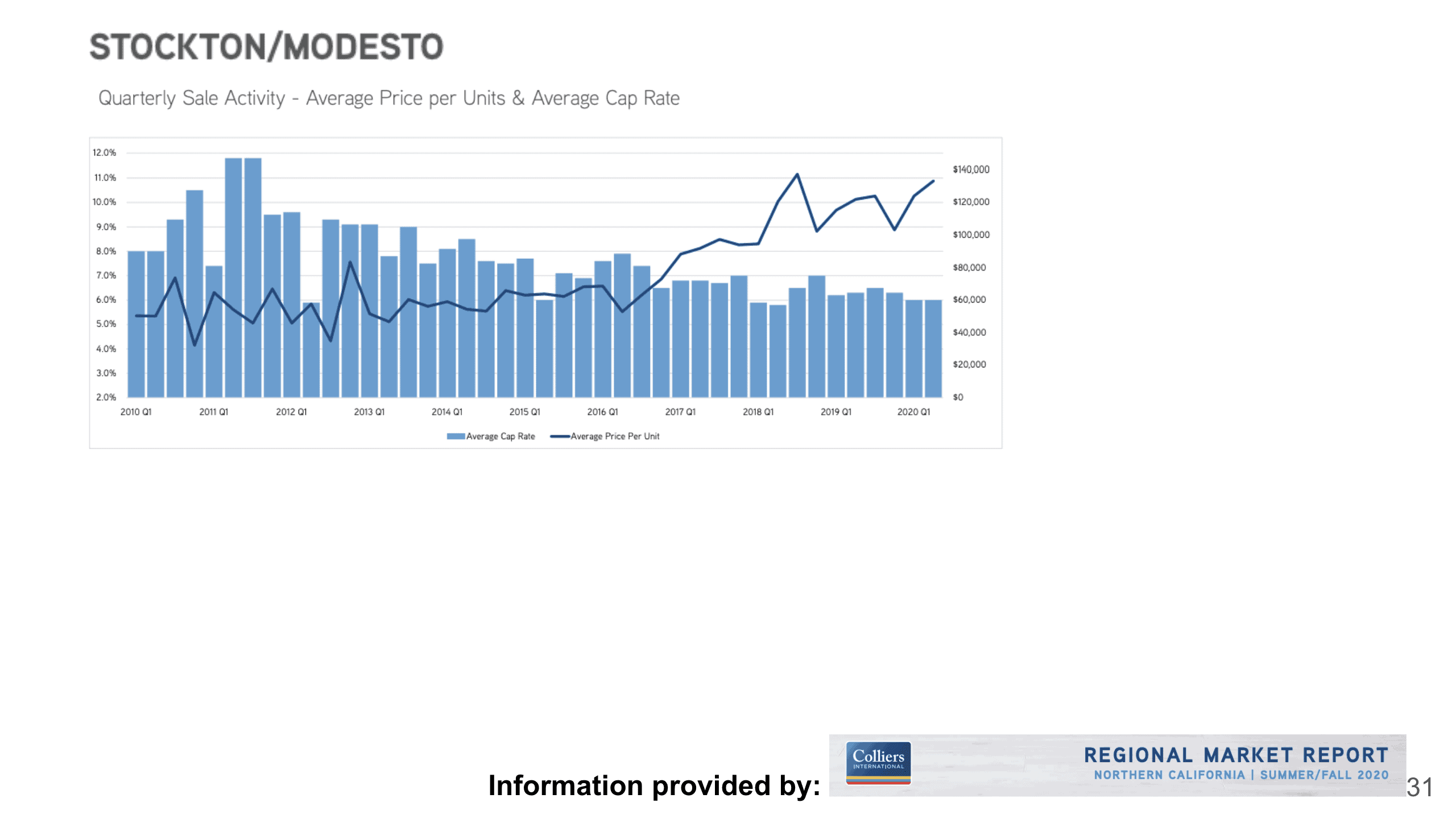

And Stockton is a market that a lot of our clients have been very interested in. As you see we actually started having our clients invest in Stockton since 2016, and you can see the per-unit price has come up from $60,000 to over $100,000, about $130,000 per unit, and their cap rate is still at about 6% currently. I know some people think that in the Bay Area you just can’t have a multi-family that has more than a 5% cap rate, but Stockton is just about one hour drive from Oakland.

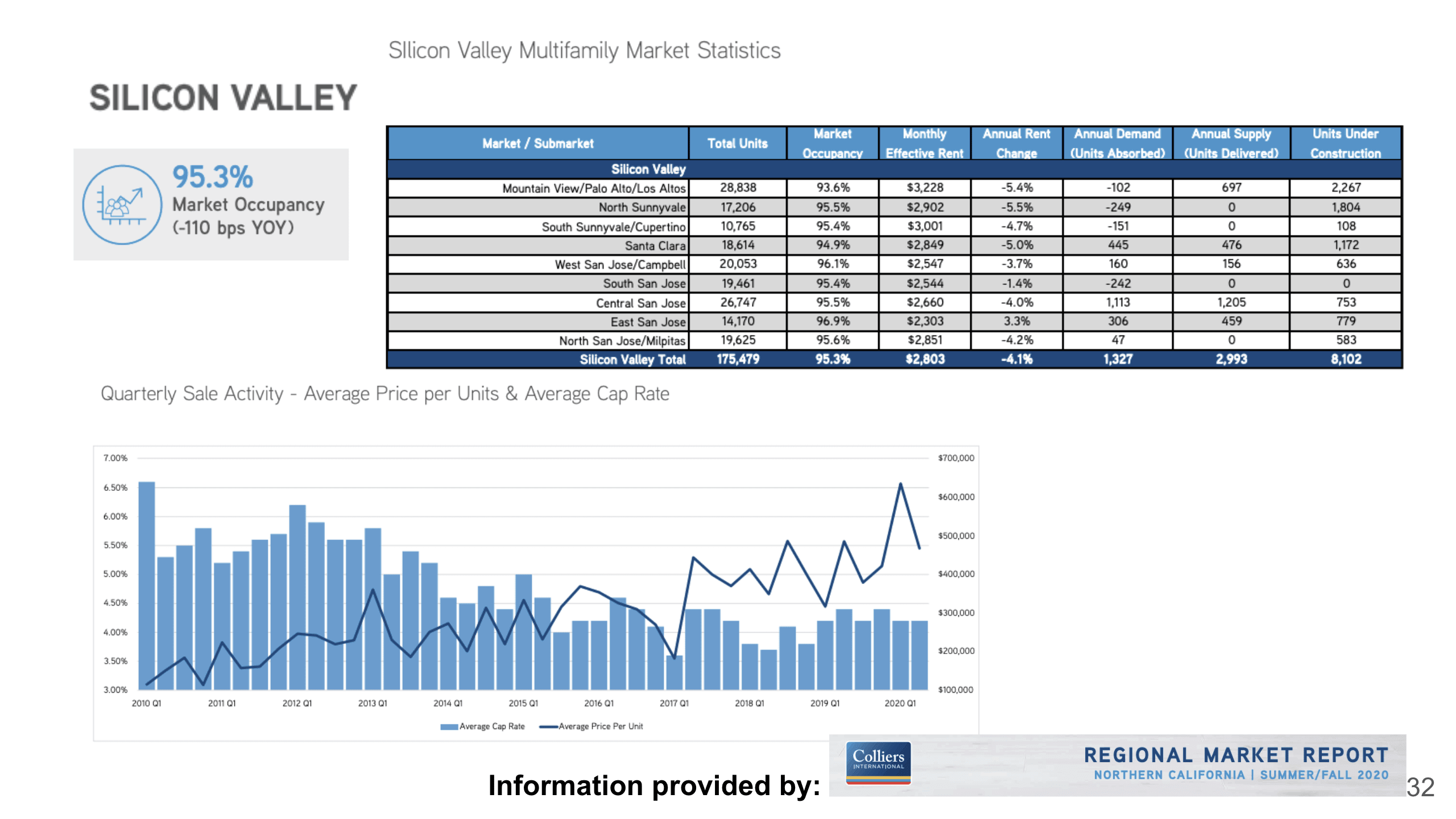

And here, let’s come down to Silicon Valley, we have a market occupancy of 95.3% and especially today we’re going to talk a lot about San Jose, so as you see that in San Jose, we still have a pretty strong occupancy rate, the rent is still pretty high, although the rent has come down slightly. The east San Jose part actually has gone up, but then other parts have come down on their rent and the cap rate is still right above 4% right now, and then the price has come down a bit. This information has been provided by Colliers, and this is their fall 2020 market report.

Lastly, I want to share this because I thought this would be a great segway to introduce Nathan and talk about San Jose.

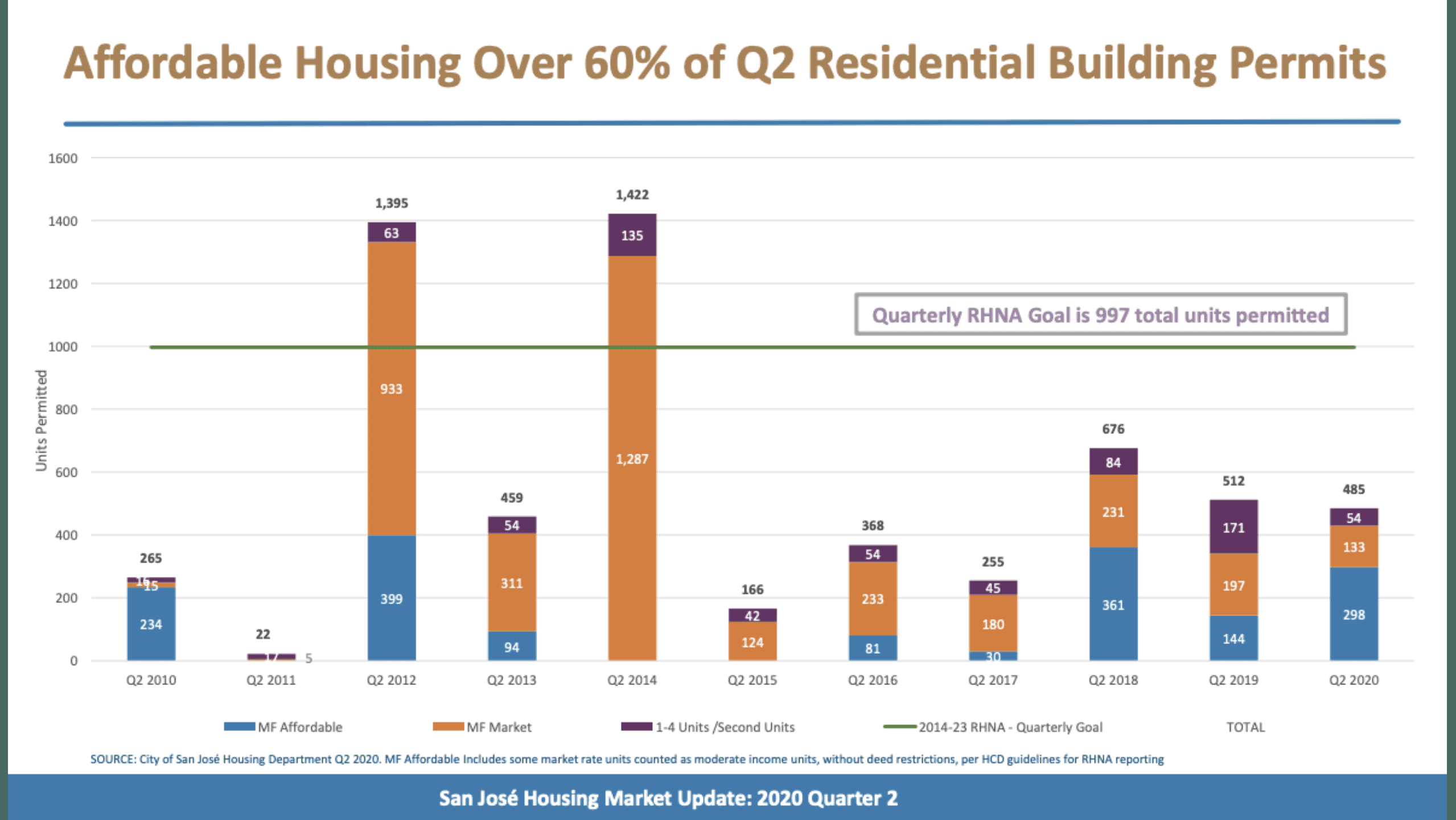

As we know, the RHNA Goal, the goals for the Bay Area region had just been adjusted to 60% of the affordable housing out of the whole 485 units, so I’m just wondering, this is one of my questions, what is the city of San Jose going to do regarding providing affordable housing?

Hear Nathan’s insights on San Jose Real Estate and Developments amid COVID-19 in the Bay Area Housing Townhall Webinar! If you have any thoughts or questions, please don’t hesitate to reach out to us, schedule an appointment now!

Stay up to date on the latest real estate trends.

Part 1 of HAYLEN's series on the 2026 CCIM Spring Forum in Philadelphia

You’ve got questions and we can’t wait to answer them.