Part 2 – 2021 Bay Area Housing Market | Residential and Multifamily Mortgage Rates & Foreclosures

Welcome back to the February Bay Area Housing Market Update Part 2! We talked about Bay Area housing market statistics and economic market updates in part 1, if you haven’t seen it, check it out here! In this part, we are excited to have a discussion over mortgage trends and foreclosure activities with two mortgage industry leaders – Wes Iseley representing the residential side, and Jeff Burns representing the commercial side.

Wes Iseley‘s experience ranges from directing large firms with Wall Street experience to developing growing companies into industry leaders. Wes is currently the Senior Managing Director of Carrington Investment Services. He is responsible for all external transactions and manages key business relationships and strategic alliances for the Carrington family of companies. He is a board member of the California Mortgage Banker’s, the MBA Independent Mortgage Banker’s and the acting Chairmen of the National Association of Mortgage Servicer’s (NMSA).

Jeff Burns, Senior Managing Director, is responsible for new loan origination in California and the western United States. He specializes in multifamily financing for Fannie Mae, Freddie Mac, and other capital sources. Mr. Burns currently serves on the board of directors of the California Mortgage Bankers Association and formerly served on the Freddie Mac Advisory Council. He is also a member of the Urban Land Institute and the Bay Area Mortgage Association.

Let’s see what they think of the mortgage trends and foreclosure activities! Watch the video version here.

Wes: I’ll jump in and see what Jeff thinks. I’m looking at the residential side, especially like rates because two things are driving these home sales – low rates and inventory. The 10-year rate right now is 1.14% up from August. Lenders out there aren’t lowering the rates, because they can’t keep up with the volume they have, so if you lowered your rates even more, there’d be even more backlog and underwriting. So, you know, there’s room in there as the 10-year probably increases. There’s a blog out there from Les Parker, it’s called the Spotlight blog, which has some great overviews. The big concern there is that the economy is popping back up, but the fear from some of the economists is if the stimulus package overcooks the economy, then inflation’s going to increase, and that’s going to be not a 2021 problem but 2022. That’s where I think the fear of some of the interest rate projections comes from. I think you’re fine this year on interest rates, but Bank of America came out today and was quoted saying that the fear again of inflation hitting in 2022 would impact rates.

Jeff: I think the same fundamentals are at play in the multi-family world. We’ve had really low rates through the pandemic, and as Wes mentioned, the 10-year’s up now, but lender spreads are still pretty hefty. I primarily finance apartments through Fannie Mae and Freddie Mac, but you’re still looking at rates in the low threes, and so people are set. Then you see a lot of apartments where you’ve got tenants that are struggling to pay their rent on time, so you’re seeing cash flows drop in certain sub-markets around the Bay Area. However, price expectations of sellers, as Helen mentioned earlier, really haven’t changed, so what we’ve seen as cap rates actually drop because they want the same price on a lower NOI, a lower cash flow on the property. If you can get a 10-year fixed-rate loan in the low threes, what we’re seeing is that more buyers of properties over 50 units where you start getting institutional money, there’s a ton of that money out there, and they’ve got to get it out, so we’re seeing people buy it at crazy prices, but inventory is still really tight, and rates are low, and that’s keeping the pressure on pricing. One other point to follow up on what Wes said about inflation. I think we’re geared up for a stretch run here of a lot of stimulus, a lot of central banks, you know, the fed keeping rates low. I think you’re really gonna see asset prices rise over the next 5-7 years, and even outpacing probably consumer inflation. I just saw somebody ask a question about debt service coverage ratios. Typically, we’re seeing those on acquisition loans, where there’s fresh equity coming in, at 1.25%, and for cash out refinances 1.3% or a little higher as kind of your max leverage points.

Helen: Yeah, we do notice that some of the debt service coverage ratio has increased. For those who don’t understand, that’s more for the commercial loan side. They need to make sure that the Net Operating Income for the building can cover at least 1.25% of their annual debt services.

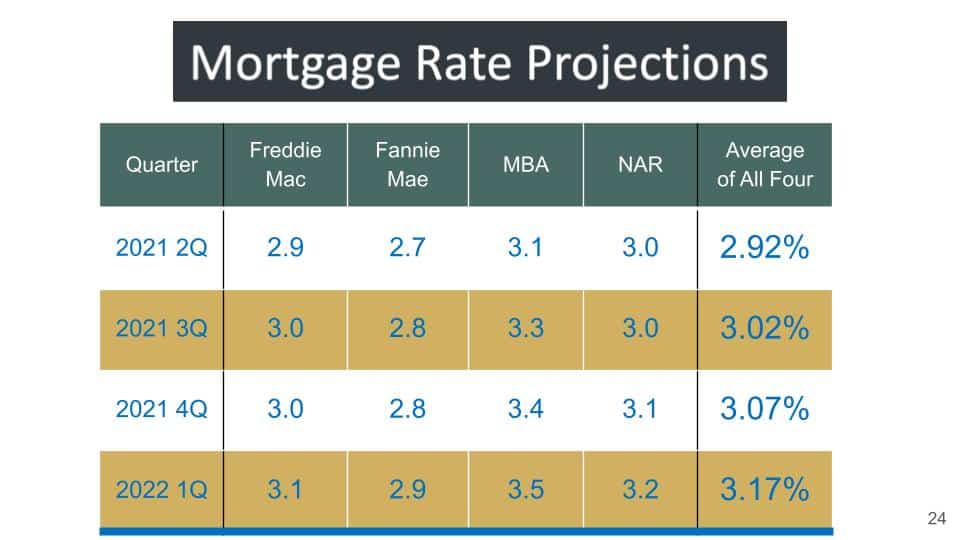

It’s interesting because you guys both talked about how low the rate is and obviously we also know that the rate cannot stay this low forever. We’ve been trying to keep updated regarding the mortgage rate projections by Freddie Mac, Fannie Mae, NBA, and also NAR. They all basically project that 2Q is probably going to be the lowest, and then it’s going to start inching up. In 2022 1Q, they’re expecting about 3.17% on average of the four organizations. Do you guys think that’s probably where we’re heading towards as well?

Wes: I think the unknown is still the inflation – how it will impact us in 2022. So as I said, in 2021 we’re going to enjoy low rates, and even with that inflation, if you’re still sub four, those are still low rates for the residential side.

Jeff: Same with us too, I mean, I’ve been talking at various conferences for the last 8 years about rates going up, and I have been wrong the whole 8 years, so I hesitate to make any forward-looking predictions because of my track record isn’t great.

Helen: I said the same thing since, I think, 2014. I was like – well we’re supposed to be going into 5% next year, and then it hasn’t gotten there yet. But I agree with you, I’ve been saying that as well, and who would have thought that our rate would actually come down below 3%. It’s pretty incredible.

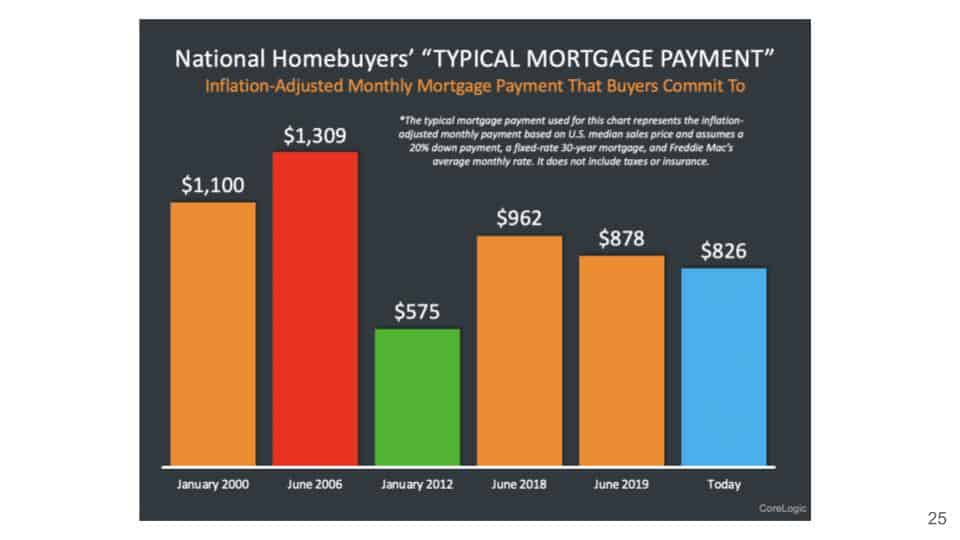

This chart also shows exactly why our housing market is going crazy. If you really adjusted these monthly mortgage payments according to the inflation, then we are paying less than back in 2000 and 2006. In 2012, of course, because the price was so low, but looking at the interest rate, this is the reason why so many people are jumping into the housing market and buying homes right now.

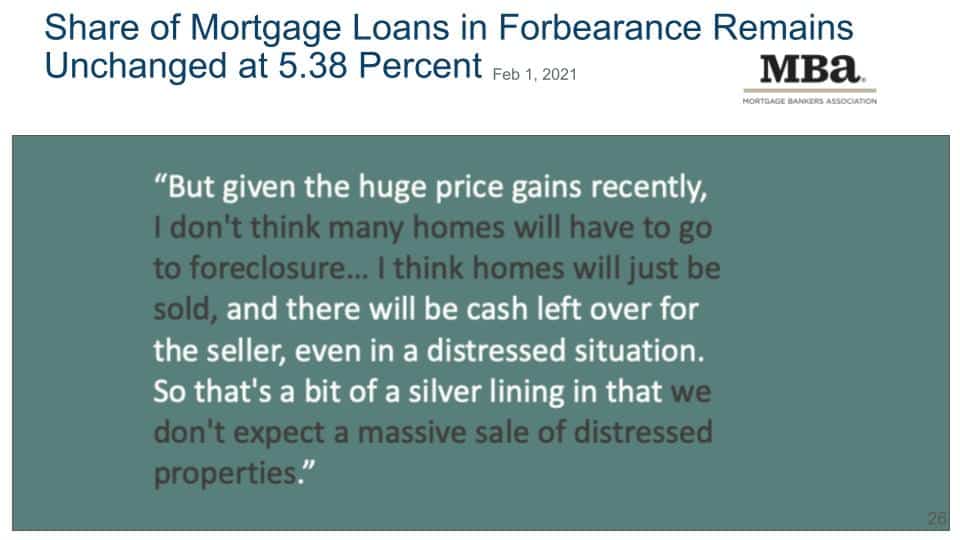

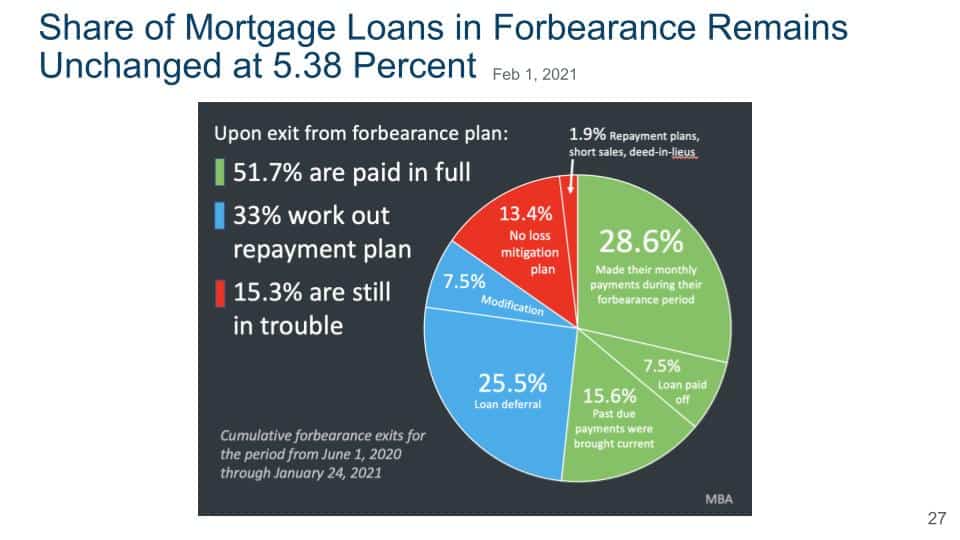

In terms of forbearance, of course, one of the biggest topics is regarding the mortgage loans in forbearance. It has remained unchanged at 5.38%, and Lawrence Yun from the National Association of Realtors says: “But given the huge price gains recently, I don’t think many homes will have to go to foreclosure… I think homes will just be sold, and there will be cash left over for the seller, even in a distressed situation. So that’s a bit of a silver lining in that we don’t expect a massive sale of distressed properties.”

Here is another chart showing the mortgage loan in forbearance, and I know Wes you had some thoughts on that as well, but I thought this is really interesting that it’s showing 51.7% are paid in full, and 33% have a workout repayment plan, while 15.3% are still in trouble. This is the data from the Mortgage Bankers Association, is this what you’re seeing as well?

Wes: You made a really good point, Helen. I was going to bring up that so we have 560,000 customers that we service, so we understand credit sensitive assets. But very different from the last crisis, because people have equity. When we’re looking at prepayments, it’s amazing that people are resolving their issue, if they have one, by selling their house and taking that equity. I think that people thought that it was going to be inventory at the end after the foreclosure moratorium. There’s going to be less inventory because people are going to sell their houses. I think the only thing you’re going to see is pop on that, so I think you made an excellent point on that. Out of the forbearances that we have, we kind of follow what the NBA and Black Knight puts out. We still have 14% of the people that are in forbearance that continue to make their payments. I agree with you that the ones that are going to be the problems still are going to have problems after that, that’s why it’s kind of flatten out that curve of people coming in, and flattening out of people exiting. It’s kind of status quo right now, so I hope we’re going to work hard to help resolve these customers.

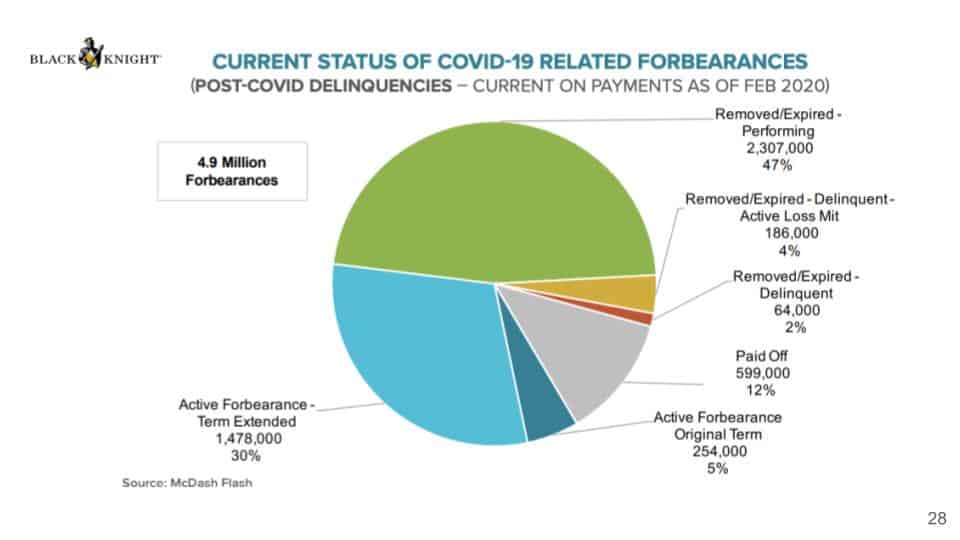

Helen: It’s interesting that you mentioned Black Knight because that’s my next slide. From Black Knight reports, what they’re showing here is that out of the 4.9 million forbearances actually 2.3 million had been removed from these forbearance plans, and they are performing now. Although there are 4% that is active loss mitigation, and there’s still another 2% delinquent, but 12% have been paid off. The active forbearance with the original terms is 5%, and then there are 30% of them with extended terms. I mean, it is still significant that they are still in active forbearance, but I think it’s just a little bit more comforting to see that we have 47% actually performing now.

Jeff: I would say, too, on the multi-family side. Fannie Mae and Freddie Mac have offered forbearance to owners of multi-family properties that have their loans on it. Typically, it’s a 120 day or up to 120 day forbearance period, and then you’ve got 12 months after that to add those payments back on top. When this whole thing rolled out, as a company we service over 100 billion dollars in multi-family loans, and we were scrambling about how many people are going to be banging down our doors to not make their payments. It turned out to be very very few, I mean, I think the initial CARES act provided the enhanced unemployment benefits, and some of the direct payments. We really didn’t see rent rolls decline in the early days of the pandemic. Where we’ve seen rent rolls deteriorate has been over the last several months, because the stimulus ran out, and they’ve been negotiating various packages. The one just passed has 25 billion in rental relief that’s getting out to the states. Obviously, in typical government fashion, it’s taking a lot longer than what they said it would to get in the hands of landlords. But most properties we’re not seeing distressed sales in multi-family except in very few cases. Now, it’s a topic for a whole nother webinar, but if you got into strip centers and hospitality, there’s real trouble there, and probably more trouble to come. But as far as residential real estate goes, it’s not been too big of a problem.

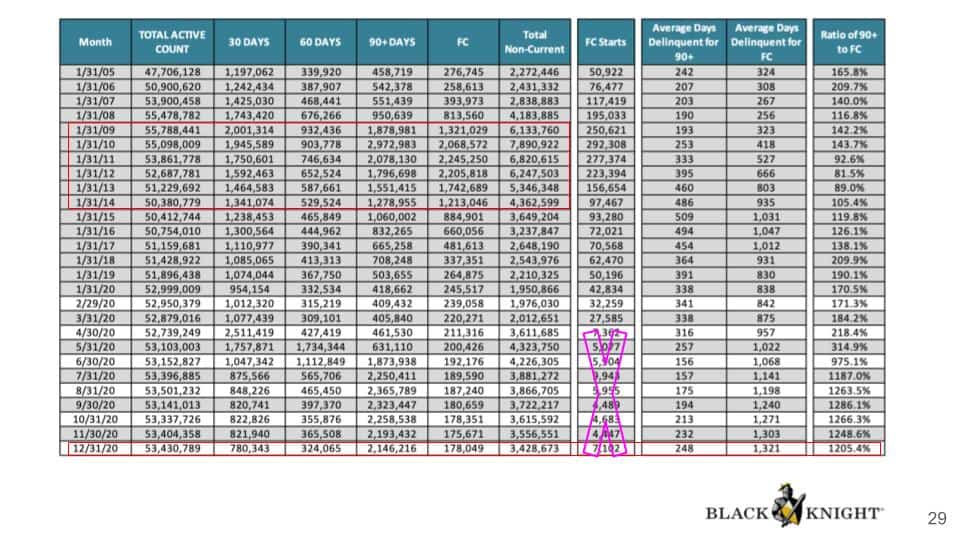

Helen: I absolutely agree with you, actually, I do have some slides about those other asset types as well at the end. This is another data to show that right now as of December 31st, we have about a total of 3.4 million non-current loans. I’m going to say let’s not look at the foreclosure stats, obviously, we have forbearance right now, these are not the numbers. But if you look at compared to 2009 to 2014, you know, total non-current we have 3.4 million, but over here we are at 6 million or 7 million, and in 2014 we have 4.3 million. If you look at the number that way, you see we’re not really as bad as in the previous recession, it’s really not even close to this 7.89 million in total non-current. I’m looking at this data, it just doesn’t show me that there is going to be a wave of huge foreclosure that is out of the ordinary compared to any other years.

Wes: Yeah, the credit quality compared to 2008-2009 is far superior, then you have equity. The underwriting guidelines back then with the stated income for resi rocking to be fraud, that’s non existent. You actually have good credit quality with people experiencing problems that forbearance is helping out with.

Helen: I remember those days, I actually started my real estate career in 2005, and at that time I was a mortgage loan broker. I remember I was like – wow, stated income, stated assets, you really just need to tell the underwriter this is how much I make, you don’t need to prove anything. We used to have a joke back then saying – long you can breathe, you can get a loan.

Jeff: Well, to that point, one of my top clients is Shea Properties and Shea Homes. They’re both in the apartment business and in the single family business. I never forget them telling me a story back then that they’d have somebody go in to rent an apartment, and wouldn’t qualify. Then they would go across the street to the sales center and end up walking out with a new home. You know, that tells you how much things were on their head.

Helen: Totally, it is definitely very different back then. I watch youtube videos all the time and I want to know what other people are talking about. My feed is just filled with housing market crash and foreclosure waves, that’s why I started doing all this research because I’ve gone through the 2008 recession at that time. I understood why we had this massive foreclosure crisis, a lot of people literally just gave up because it’s an investment decision – I didn’t put any money down, I’ll just let it go, right? At the time you can get a loan with no down payment, so in a sense, you’re not really losing much. But right now, it’s very different because at least in the Bay Area, most of the homes have at least 20% down or equity in it, so I just don’t see how people would just give up their home that easily.

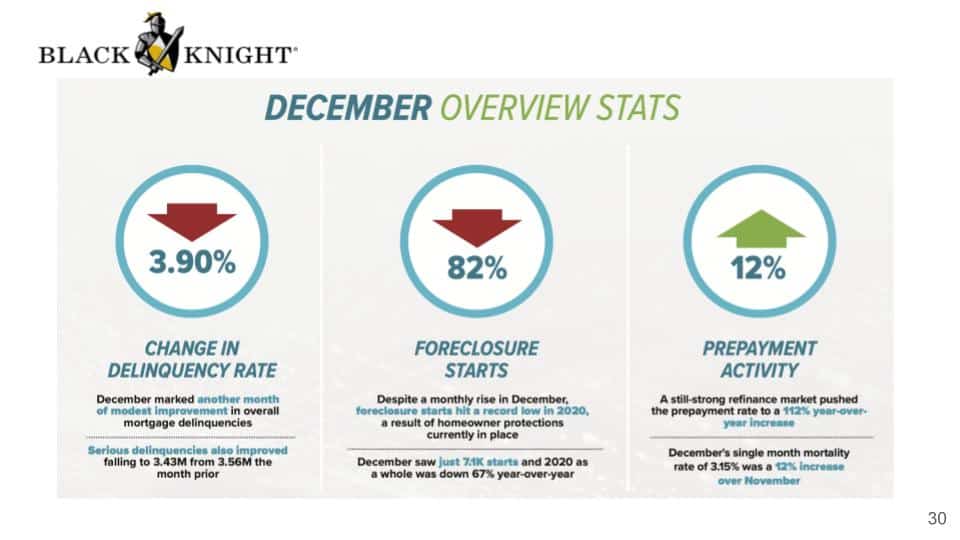

Here is a little bit of a summary. Basically, it says the delinquency rate had dropped by 3.9%. Because of the moratorium, there are no foreclosure starts. The prepayment activity actually went up by 12%. One of the reasons is also because the rate has gone down, so a lot of people are refinancing and that’s considered part of prepayment activity.

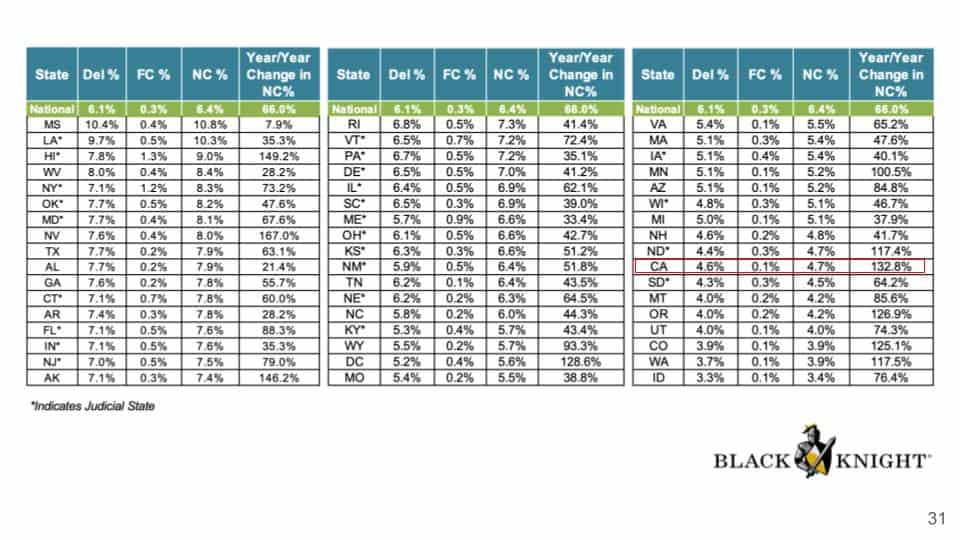

If you want to know where California is ranked compared to anywhere else, we constantly get this question all the time from our clients, so I would show them. Actually, I did this chart a few months ago as well. As you see that in California, we have just 4.6% delinquency, foreclosure percentage is 0.1%, non-current is 4.7%. We are not one of the top 10 markets where Mississippi, Louisiana, Hawaii are getting a much bigger hit in terms of these delinquencies.

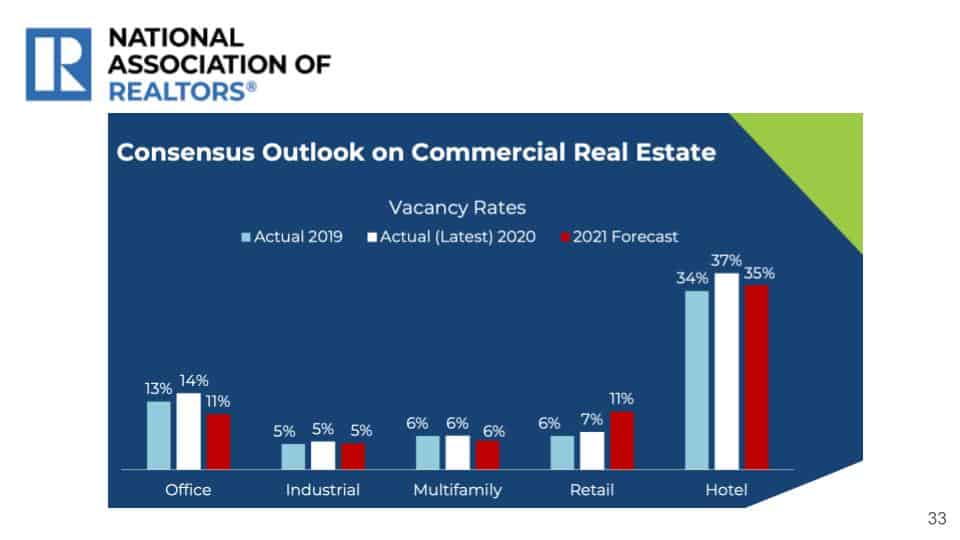

All right, and then the commercial real estate market. Just like what Jeff was saying. Look at the vacancy rates for hotels is at 34% in 2019, and 2020 is about 37%. The forecast for 2021 is 35%. For retail, it’s expected to be about 11% this year. Multifamily we’re staying pretty consistent as well as industrial. So out of the commercial markets, industrial and multi-family probably doing relatively well, and office – I’m a little surprised with this number, which is through NAR. I do see a lot of vacancy in offices, don’t get me wrong, they have leases, but I’m saying there are people who are not continuing their lease anymore, or they completely moved out. Do you see any situation in the offices?

Jeff: I think that office number might be a little misleading because I don’t know if it takes into account the spaces that are coming on the market as sublease space. You might have a building that’s 90% occupied in terms of signed leases, but, especially in the urban cores, San Francisco there is a ton of empty sublease space available. I’m not sure that’s getting captured in these numbers, and, you know, that’s always an early trouble sign in that sector, because either people are going to walk from those leases if they can’t rent them, or the landlord’s going to have to get involved if the gap between the current pay lease and what the sublease market will yield is too big of a gap. I don’t know, I’m a little skeptical of that projection.

Helen: I mean, just two days ago Salesforce Tower, they just said that all of their employees can be working from home permanently. I’m just like – oh my gosh, that’s a huge tower right there, and what is the occupancy, what are they gonna do with all their office spaces? I think we definitely have to see what’s gonna happen, although I do believe that people will still have to go back to the office. Maybe from 5 days a week down to two or three days a week instead. No matter what, especially I think if your profession involves some kind of innovation, there’s a lot of collaborative work that you just can’t really do from the computer only. I see some professions can definitely go completely remote, but at the same time, a lot of jobs in the Bay Area probably will still require you to go into the office a couple of times a week at least.

Jeff: There’s no question, and you see what’s interesting is what that impact has had on housing. Because I live in the East Bay, out in Danville, and the residential market has been red hot out here, and what it is is that people selling their small house in Palo Alto or in Santa Clara or wherever they are, and now that they’re working remote, and they know that eventually, they might only have to commute over there a couple of days a week. So there are a lot of the people I’ve met that have bought houses in my town in the last 6 months have come over from the city or the peninsula. It’ll be interesting to see what impact that has, you know, if you only need to go in two days a week, do you need as much office space as you did before? It’ll be interesting to see what the trends coming out of this are. But I think you’re right, we’re not going to a remote world out of this, we’re just not.

Wes: I’ll speak for Carrington that so we have 3,500 employees, we’re shocked at the efficiency and productivity of that. Out of those, we’re probably only going to bring back 35% of them as long as license activities can remain, which the NBA and other groups are kind of fighting for. When some of those lease terms come up in 2022, 2023, you know, we’ll review our footprint.

Helen: I think it’s more like the office space usage is going to be like – well, let’s say a lot of real estate companies, for example, they would have a 5,000 square feet office space, but then they realized that maybe most of the time it’s less than 50 of the agents will go into the office because you tend to be able to just work from home. For me, as an example, I have three children, I want to be able to work from home instead of going to the office so I can do things more efficiently. So I think this is going to be very interesting how it’s going to change, but at the same time, not eliminating this office space. It’s just that people are going to really shrink down their footprint in the office space.

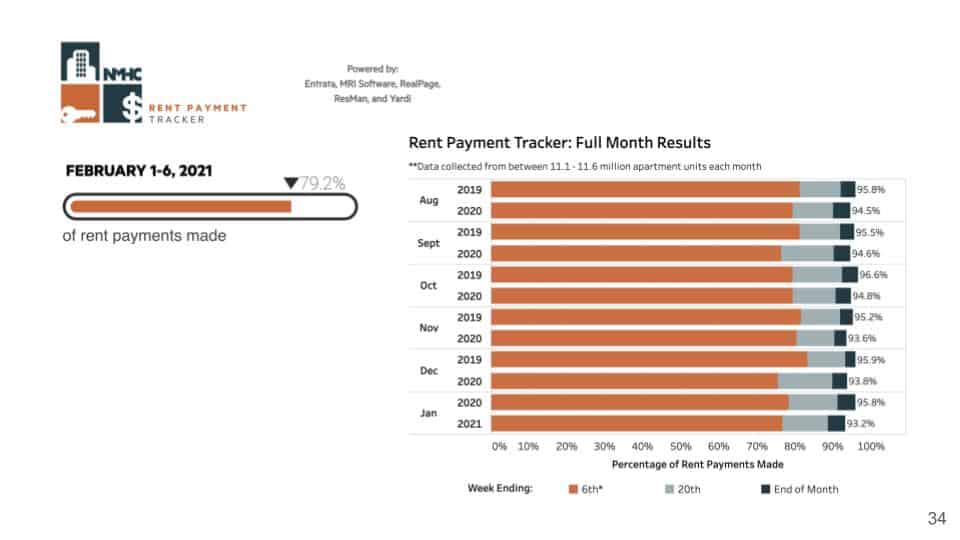

For multi-family we do this tracker every month, and in February usually the first six days we see it ranges about 79-80% on the collections. We always look at the full month because a lot of tenants actually pay after the 6th of the month and then we are at about 93.2% for January. It is lower compared to August, and relatively almost the lowest if you compare the past few months. But at the same time, we are talking about 93.2%. That’s why some of the sellers’ point to us is that – look, we are still collecting rents. Then the buyers go back – well, I don’t know how long that’s gonna last, what if after I buy it and your tenant is not gonna pay rent? Also, there’s the eviction moratorium. That’s why there is this gap between sellers and buyers that they cannot come into agreement. Is that what you’re seeing too, Jeff, when you do multi-family loans?

Jeff: Yeah, I know for sure it puts pressure on buying, and then also financing these properties, when one of the things that we look closely at as a lender, you know, we get an operating statement in, and everything looks pretty rosy. Then if you dig deeper, most owners accrue the unpaid rents over time, and they don’t book it as bad debt until that tenant moves out, or it reaches a certain point where you just know you’re not going to get paid. Lenders of all stripes are really looking under the hood of these operating statements and rent rolls to say – what do we really have here in terms of cash coming in the door? We see a pretty wide variety of answers to that. Most of the difference we see is kind of like Charles Dickens’ tale of two cities. We’re seeing suburban larger unit properties collect most of their rent rolls, and we’re seeing higher rent smaller unit urban deals are the ones where when we look under the hood, there are a lot more people not making the rent payments. Also, I think there’s a more organized effort in certain cities like San Francisco of tenant rights. People are really getting the word out – hey you don’t have to pay your rent, they can’t kick you out. You know, there are groups out there really facilitating and making it easy for people to not make their rent payments. Whereas in more suburban markets you just don’t have that dynamic.

Helen: I think it is also important to emphasize that, obviously, most of the tenants are great and honest people who do want to pay their rent if they are able to. Then there is some very small percent of the tenants, the same thing for landlords, a small percentage of them, they just out there try to take advantage of you. I mean, all these tenant’s rights groups have a good intention to help the tenants, but at the same time, somehow this has been portraying the landlords to be the bad people, the greedy ones, and the tenants are the ones who are very well loved. Now we’re starting to see more and more news about these mom-and-pops landlords really struggling as well. They lost their job, and this is their only income. Not only they don’t get the income, they now have to pay for all these maintenance costs for the building. So when the legislators are proposing some of these policies, I just really hope to see them to propose something fairer for both sides.

Jeff: Helen, you’ve lived in California long enough to know that the likelihood of that is very very slim, unfortunately. You’re right though, and, you know, fortunately, the voters saw through the attempt to pass a split tax roll on commercial property, and also defeated prop 21, which would have just turned rent control on its head throughout the state. So we averted two real disastrous events right there, but certainly not out of the woods.

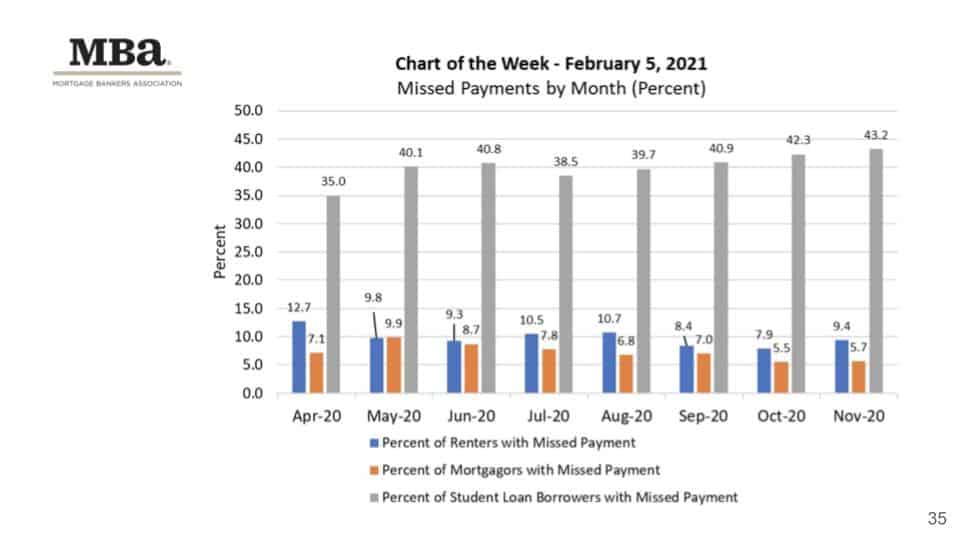

Helen: Yeah and here is a chart showing what are the missed payments by renters and by landlords as well. As you see, obviously there are more renters that are not paying, and then 5.7% of the landlords are not making the mortgage payments. But student loan borrowers are definitely hurting right now, 43.2% of them are not paying their payments. That’s all of my report for you guys and let me stop sharing right now.

In addition to the discussion, Wes Iseley and Jeff Burns also answered many questions from the audience. Watch the full video here! If you have any questions or comments, please don’t hesitate to get in touch with us.

Stay up to date on the latest real estate trends.

And what to check before upgrading your internet plan

HAYLEN, an Asian-owned, people-first real estate firm, selected to steward real estate process for J-Sei Home’s next chapter

You’ve got questions and we can’t wait to answer them.