When will inventory come back? – November Bay Area Housing Market Update

Welcome to the November Bay Area Housing Market Update! We are so excited today to share a lot of data with you about our housing market, about what happens after the election, and also we just heard that the vaccine is coming out soon, so what will happen if the vaccine comes out? We will share some of the local news first, and then we’re going to go into the United States housing market, what we’re doing and what is the forecast by different organizations. Watch the video here!

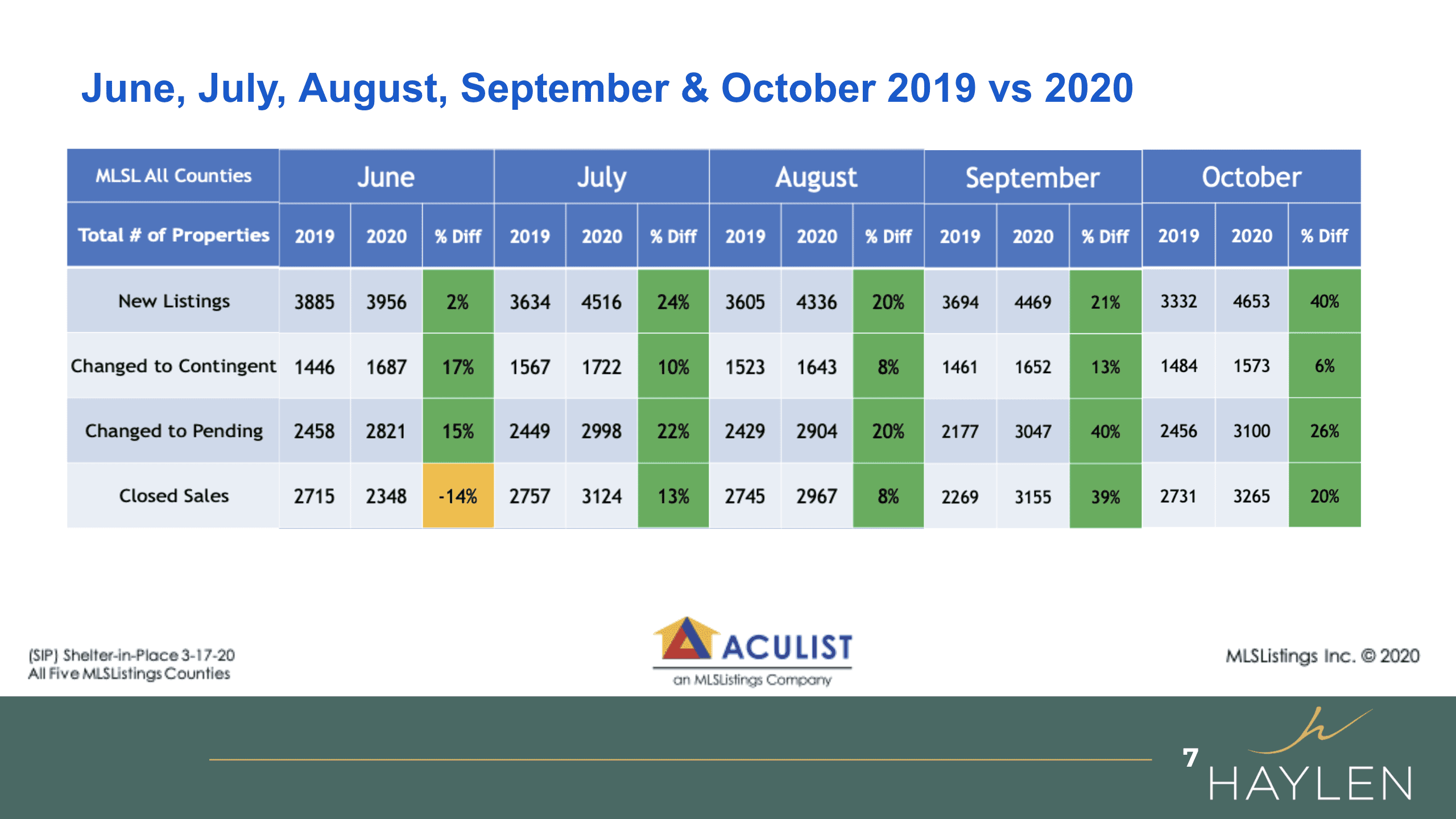

These are all the aggregate numbers from the five counties in the Bay Area. We have been stacking up this chart since May, and the numbers from May used to be all red, but now it’s been positive numbers all the way through to October. As you see that the number of new listings has increased 40% compared to last year, and we continue to have more properties that went under contract, and also more properties had closed as well compared to the last year.

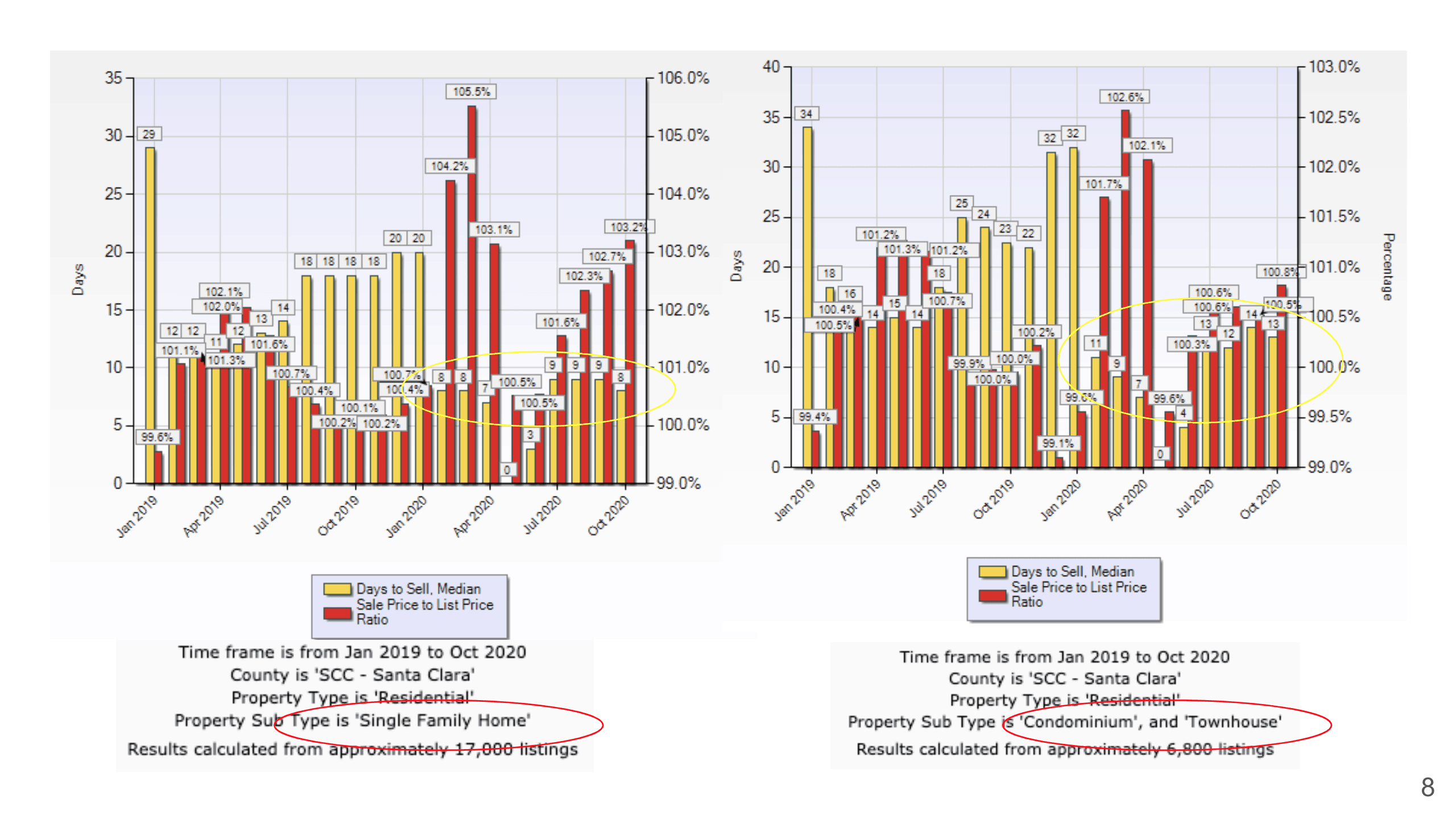

If we look at this chart we are comparing the single-family homes and condominiums in Santa Clara County. If you look at this yellow circle here in the first chart, we’re comparing the number of days being sold. If you look at single-family, this is all under 10 days. It stays on the market for 10 days only. However, condominiums and townhomes do tend to stay a little bit longer nowadays. For this reason, I think I’ve been mentioning quite a bit for the past few episodes, that people have shifted the way they live, and the way they want to buy their homes. They are really looking for a single-family more these days. Also, if you look at last year, we all experienced a slow down on the market last year, but as soon as January started, we actually saw a huge increase in the competitiveness of all these listings. This is the same for both single-family and condominiums. Last year for the condo, you see that it was hovering around 99% to 100%, but at the beginning of the year, pre-COVID, it had jumped up to 102.6% for condo and single-family was 105.5%. But of course, COVID happened, and the shelter-in-place happened, as you see in May everything dropped to zero because we stopped counting days on the market at the time, we weren’t really open for people to go look at homes. But after May, we opened and although we’re not as aggressive as pre-COVID back in February and March, in single-family you still see that they all started going back up again, and the average is about 103.2% in terms of the offer price over the asking price. And then the condo, again, it’s not as aggressive. It’s right around 100.8%. It is not below the asking price, but it’s not too much over the asking price either.

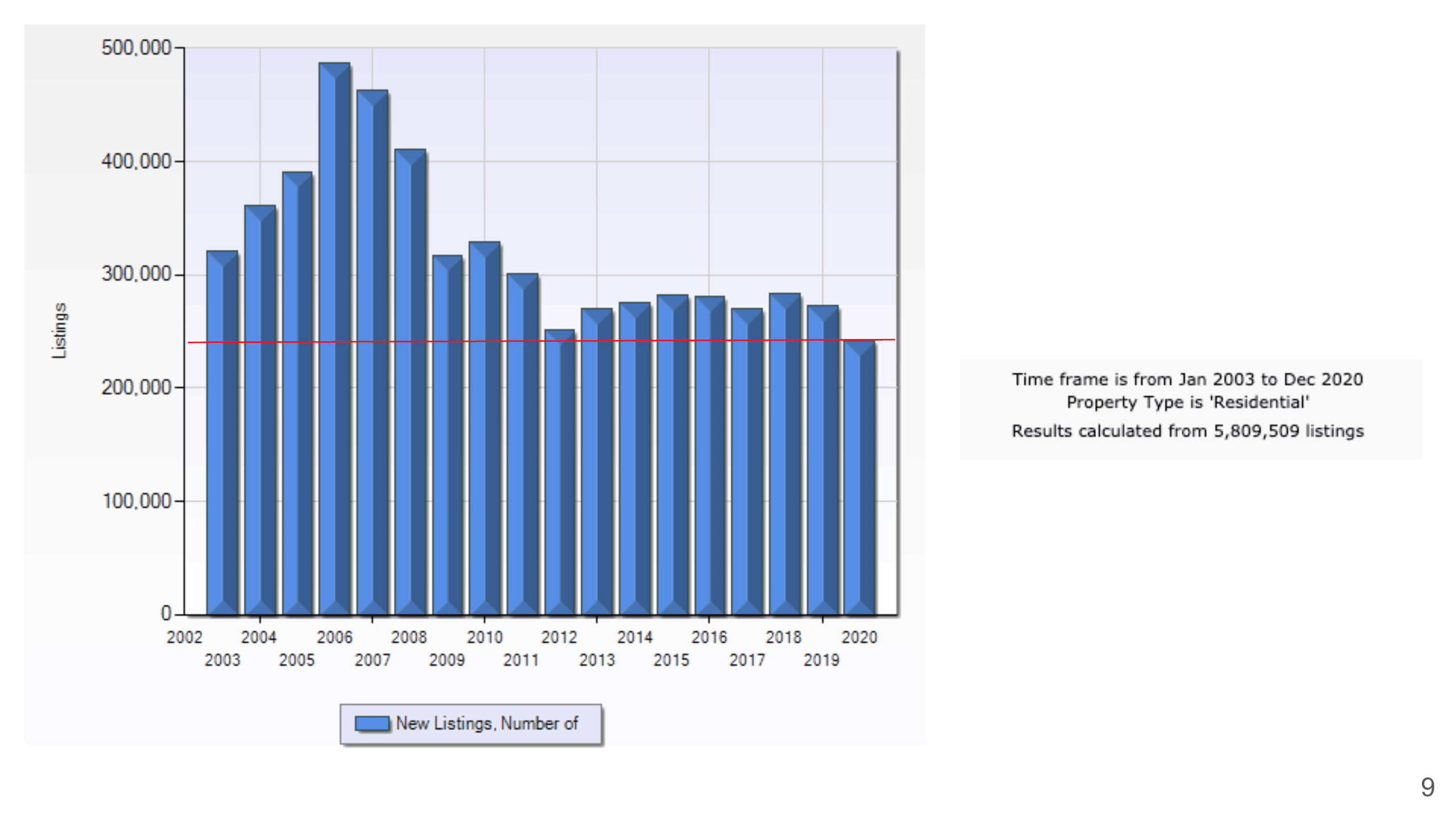

And here I thought it would be fun to share with you guys is that you see all these numbers of new listings historically since 2003. So this is 17 years of data, and we have still historically low compared to other years. 2012 is probably one of the lower ones, but as you see like 2006, 2007, and 2008 we have quite a bit of inventory on the market but right now we are definitely a lot less than before.

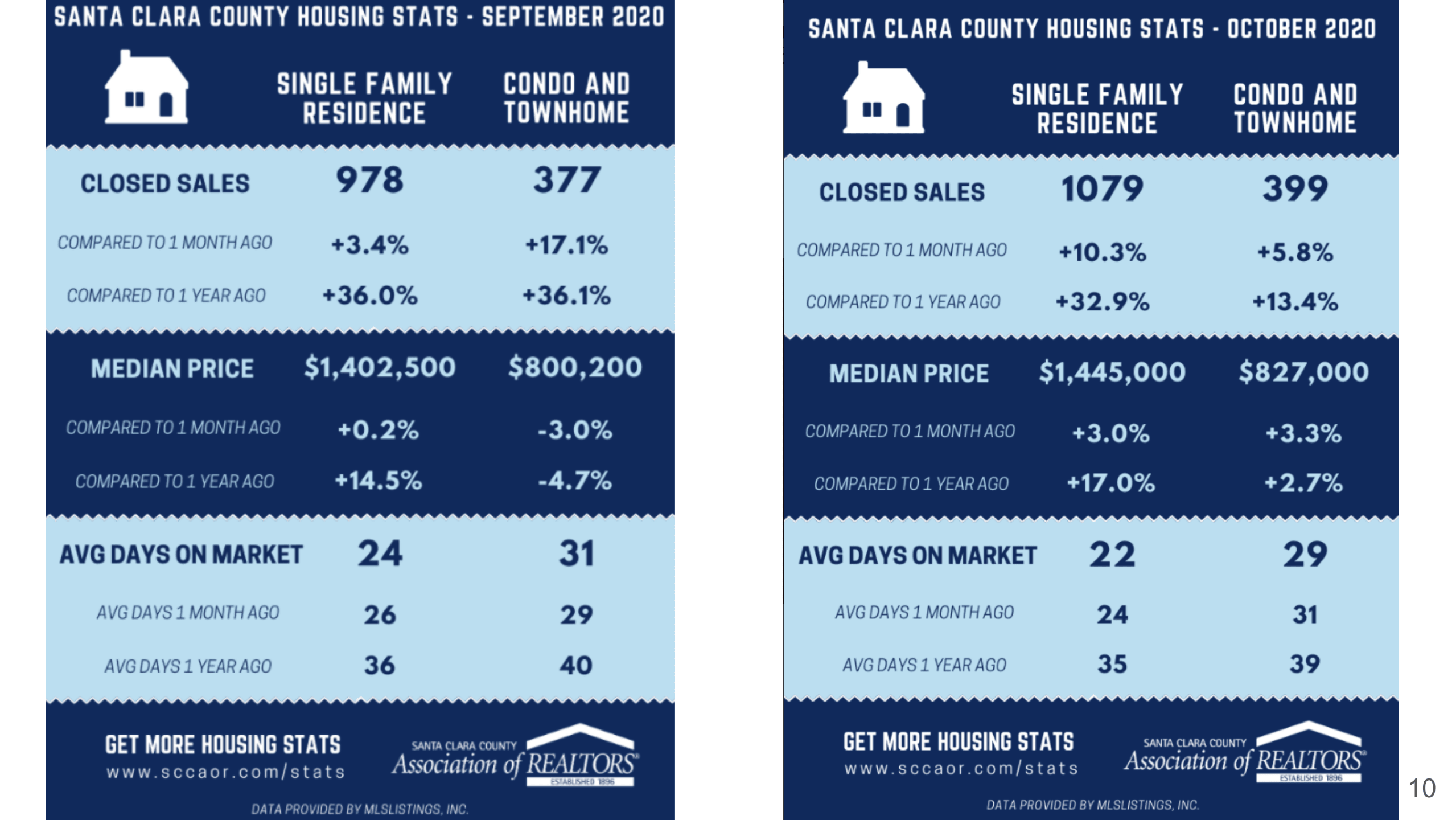

Now, here let’s compare Santa Clara County data. We have our numbers from September 2020 compared to October 2020. September we were saying that the close sales have gone up, and compared to last month, we still have gone up more again for single-family, as well as for condo and townhomes, the number of close sales has gone up, not to mention it has gone up quite a bit compared to 2019 – 32.9% for the month of October and also condo was about 13.4% compared to last year October. The median price continued to go up, and for Santa Clara County now our median price is at 1.445 million. It is 17% more than last year, while the condo and townhouse are about 2.7% percent more than last year.

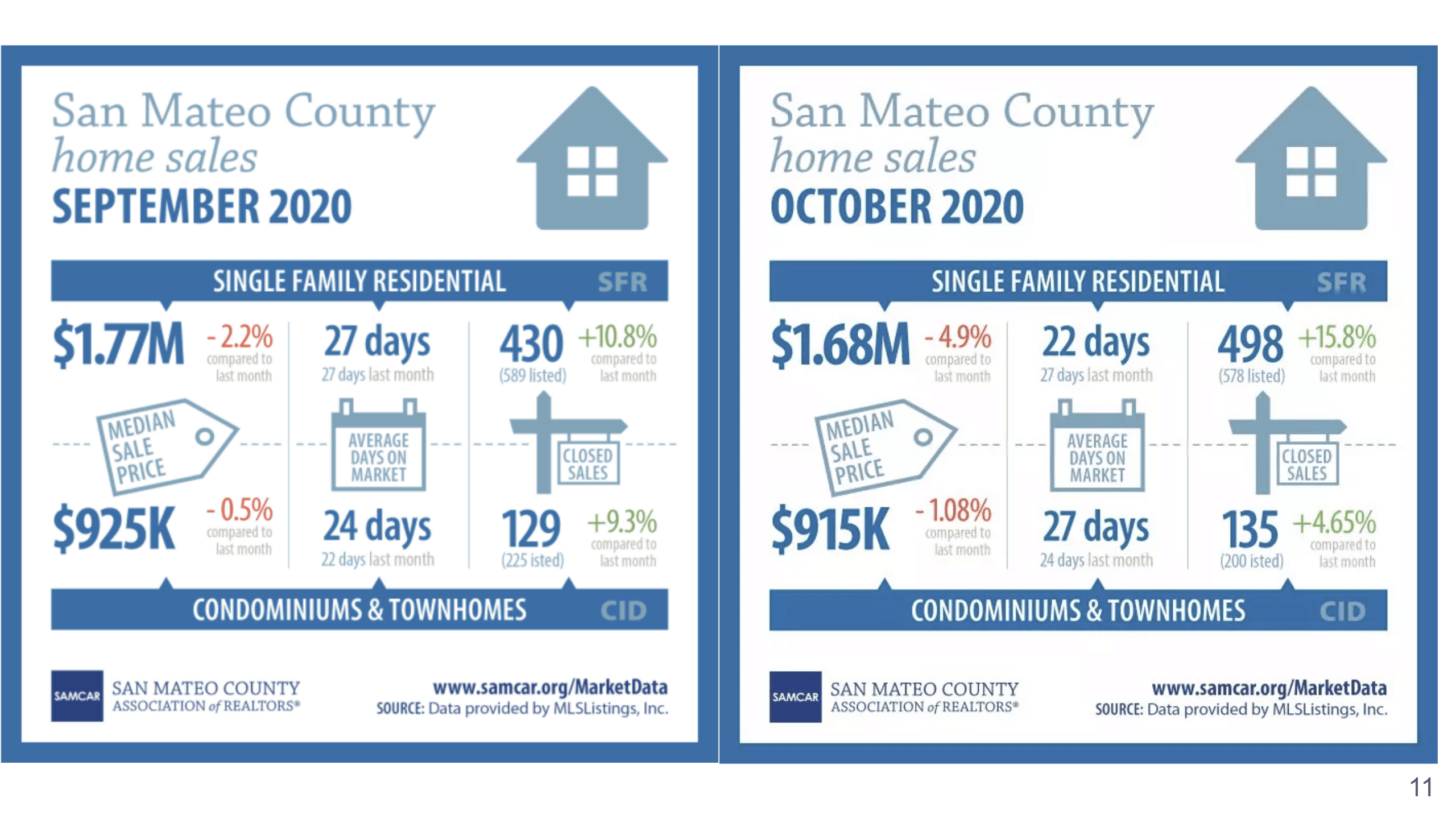

San Mateo County is a little different though. In San Mateo County, you’ll see that since last month we’ve been seeing a dip in the price. Single-family residence here, the median price last month was 1.77 million and then again this month we dropped a little bit to 1.68 million, which is about 4.9% percent. They are still selling fast though, about 22 days on the market. They do have more closed sales, which was about 16% more compared to last month. The same thing for condominiums, the price has come down. I thought it’s quite interesting, especially if I share with you the next slide.

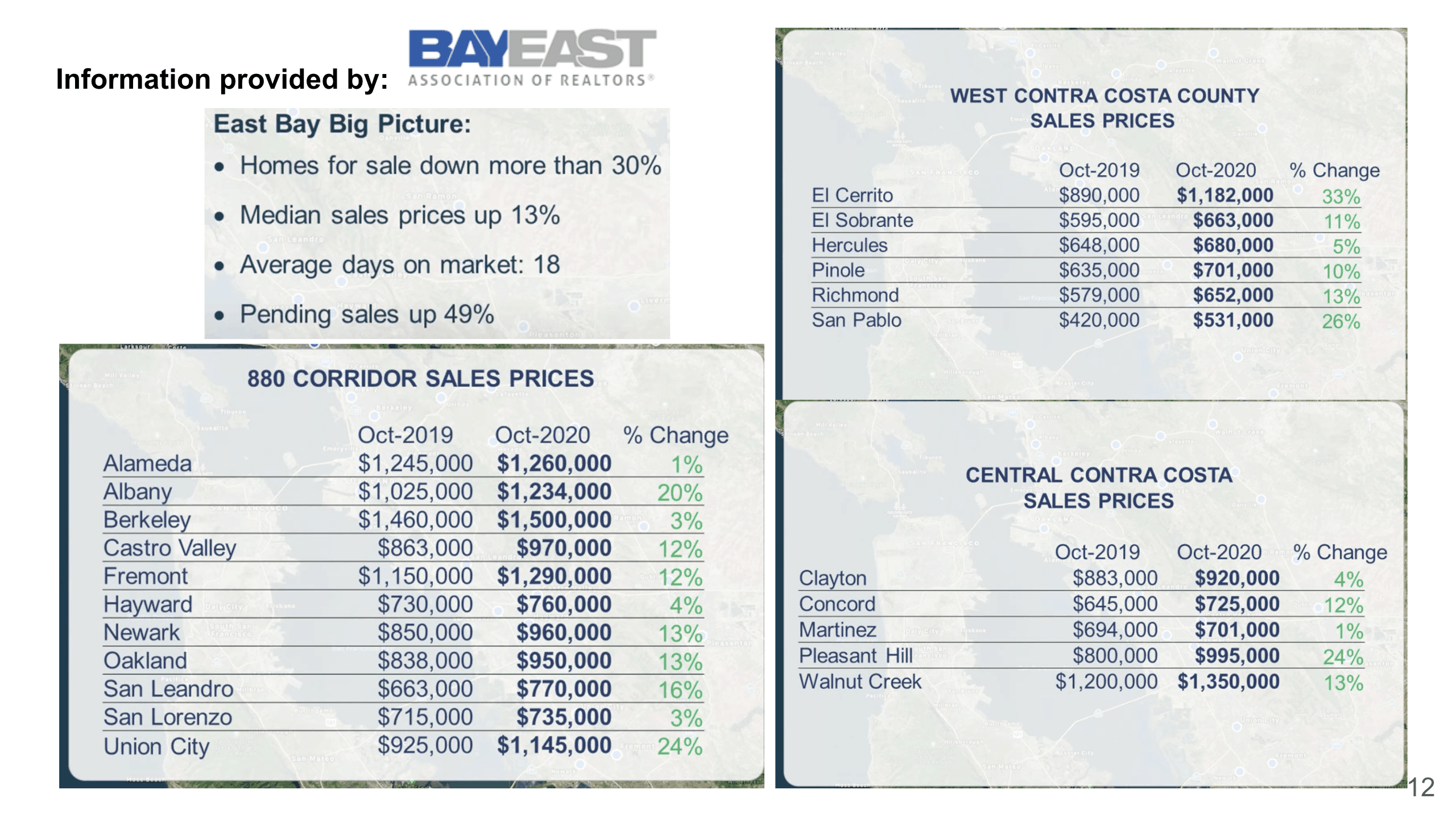

This is all the East Bay counties’ data, and you will see that there is quite a bit of difference. Now, a big picture for the east bay is that the home for sale is down more than 30%, but the median sales price is up 13%, and the average days on the market is 18 days, the pending sales have gone up 49%. If you look at the 880 Corridor, everything is green and they have gone up so much. Albany had gone up 20%, Union City had gone up 24%. Here is West Contra Costa County, if you look at El Cerrito 33%, San Pablo 26%. Central Contra Costa has gone up quite a bit as well, a lot of them have gone up like double digits besides Martinez and Clayton, they only went up about 1% and 4% respectively.

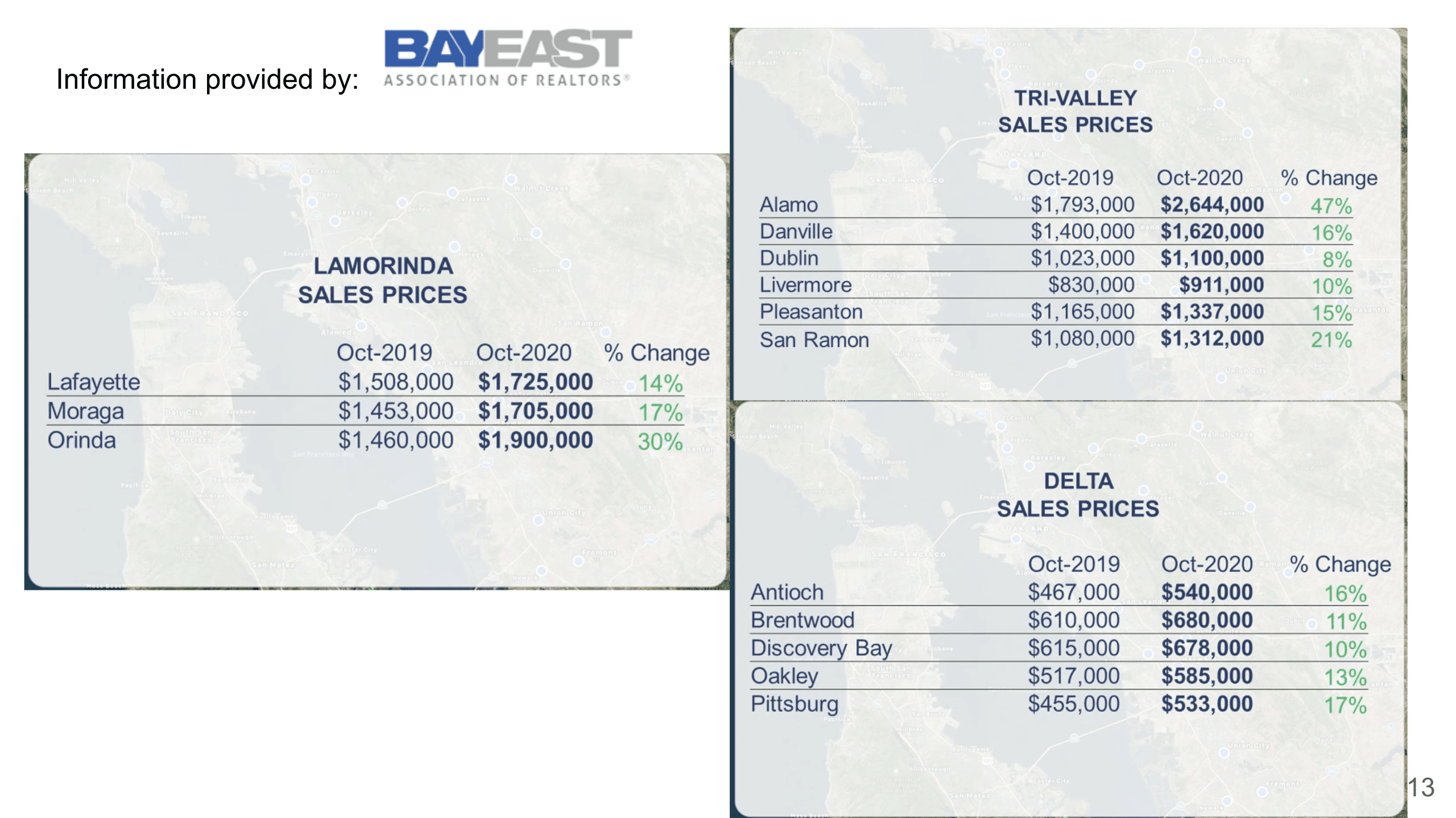

If you look at Lamorinda, it has gone up 14% to 30%. Tri-Valley went up from 8% to 47% for Alamo. Also, here we see the Antioch, Brentwood, Discovery Bay, Oakley, and Pittsburgh all went up double digits as well.

As I mentioned, East Bay has gone up quite a bit. We can really see that people are moving away from the more expensive areas. Even us, on the ground we talk to our clients and a lot of them say, you know, we are working in San Francisco, we’re working in the Peninsula, but I think East Bay is more affordable because we don’t have to go to work as much now, we are able to work from home. So they would much rather pay less money for bigger homes than being in the Peninsula. After looking at those statistics, you could definitely see that migration.

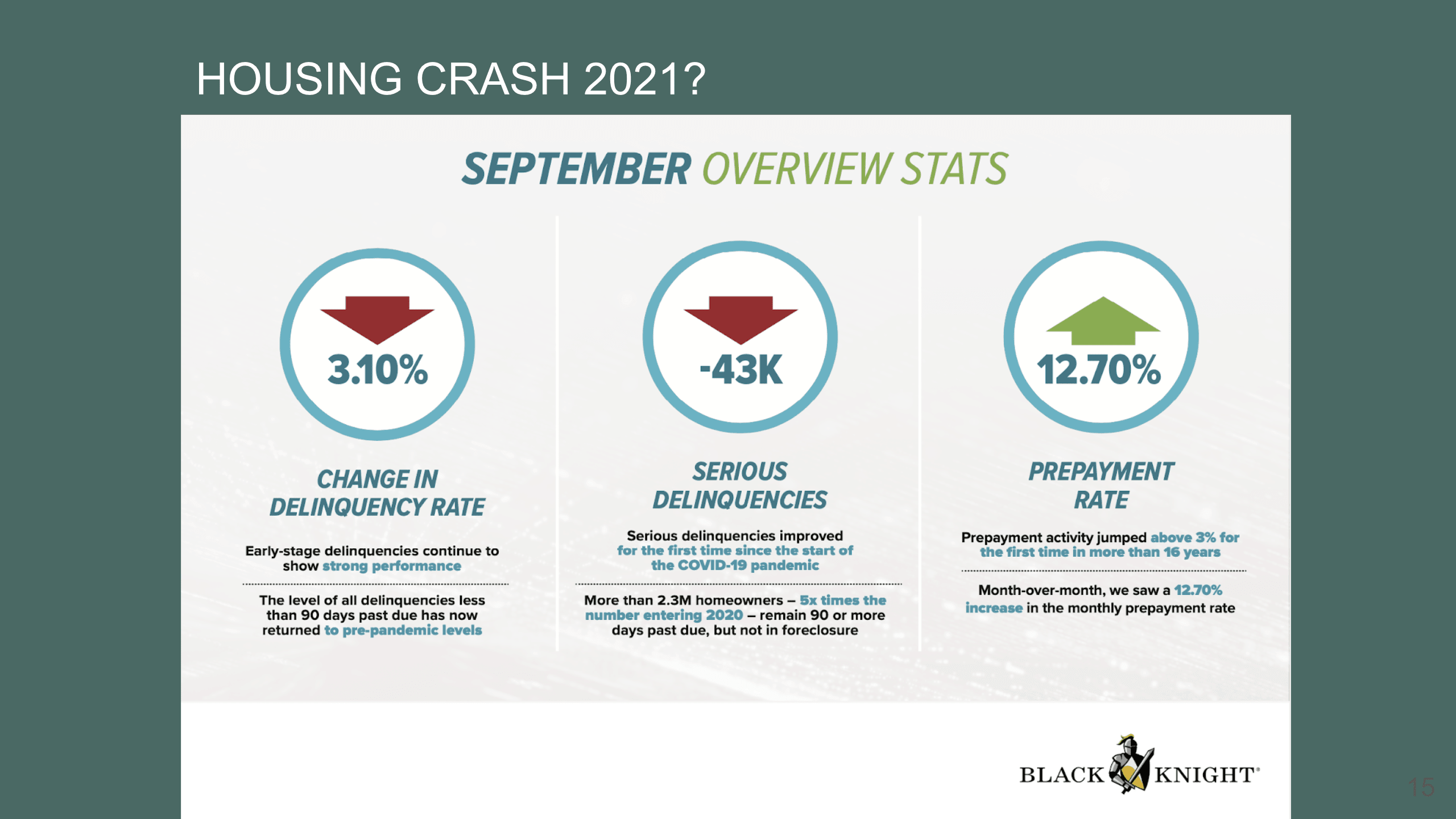

Regarding the mortgage loan, a lot of people have been talking – are we going to have a housing crisis in 2021? So let’s take a look at some of these mortgage loan statistics. The delinquency rate has actually dropped 3.1% in September and also went down 43,000 on serious delinquency, which means more than 90 days past due, and the prepayment rate actually has actually increased by 12.7%. These data are from Black Knight, I really enjoy actually looking at Black Knight reports because they provide so much statistics.

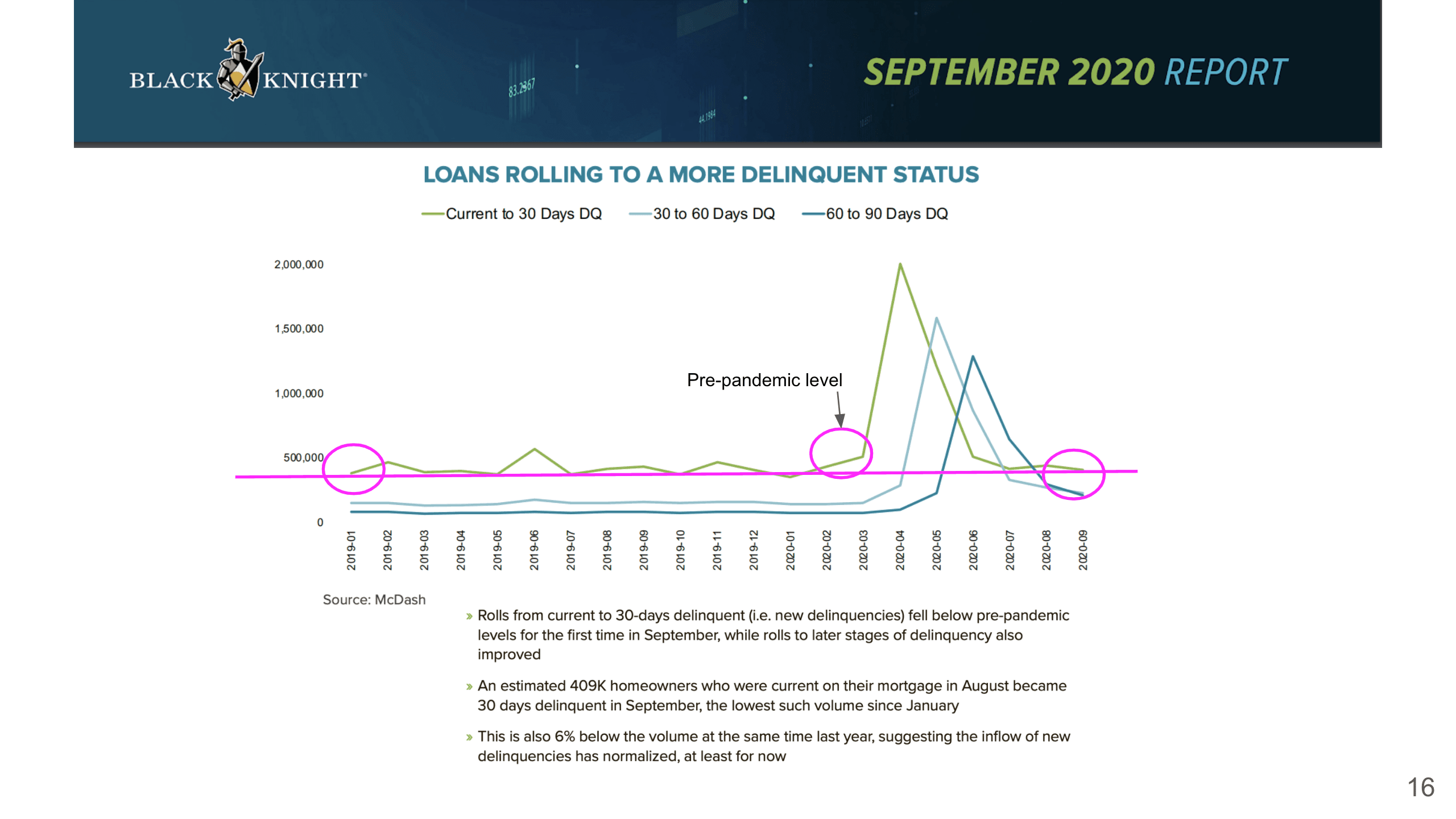

You also can see that over here in this chart, specifically, I like to look at this green line, which is talking about how many new loans have gone into delinquency, for example, to 30 days. If you look at this number here, which is in September, it actually went back down to 2019 level, pre-COVID level for sure. Also, it is even lower than in February and March. So I thought that was quite interesting where we have less new delinquency coming out on the market.

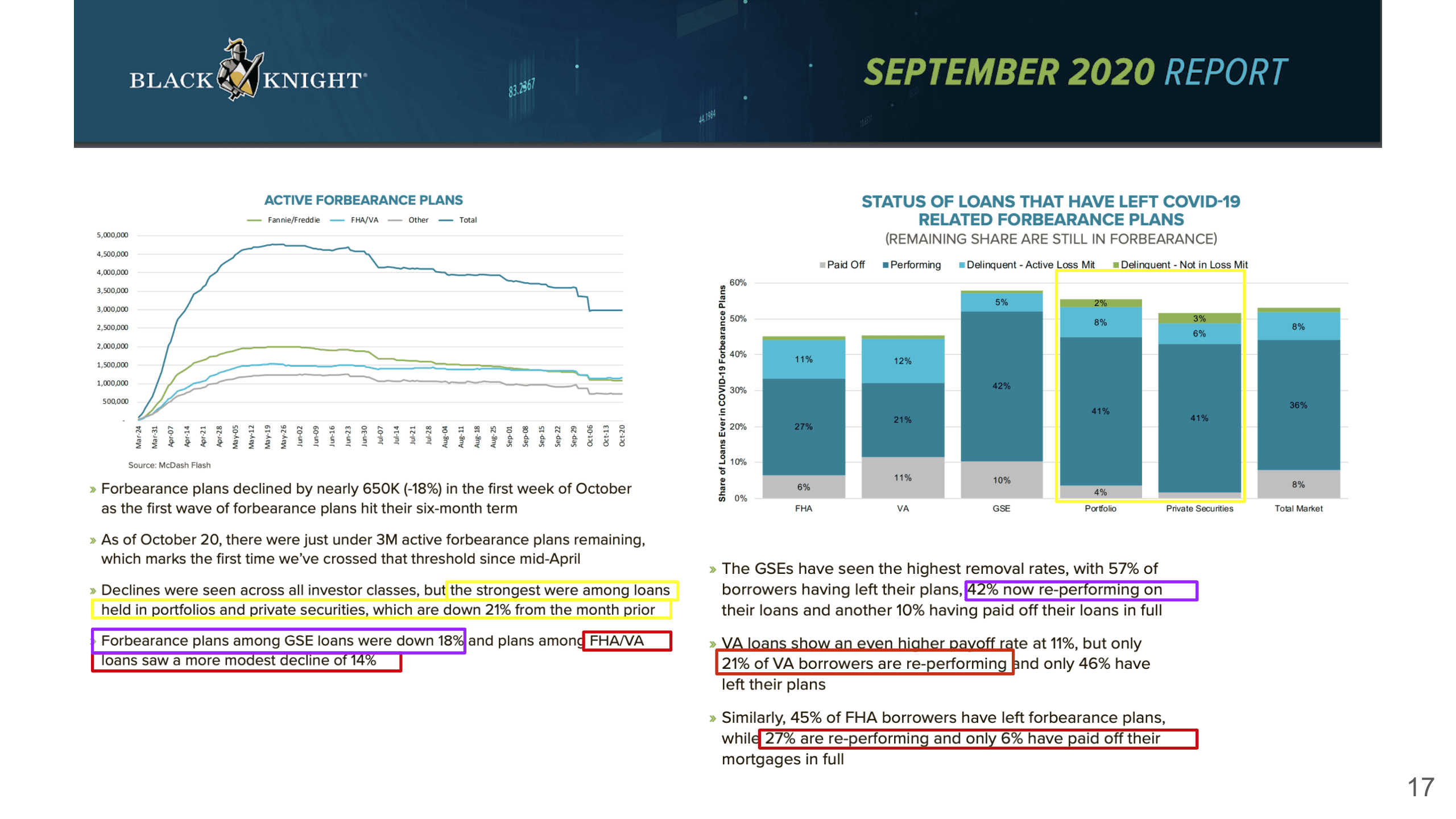

What about forbearance? Here are two charts that I want to show you regarding forbearance. This chart actually is showing us all the different loan programs. For example, what it says here is that the strongest were among loans held in portfolios and private securities, which are down 21% from the month prior. The same thing here, these darker portions here are talking about how many loans are back to payment, so they are out of the forbearance plans. For portfolio and private securities, those have 41% and came back to be really performing. Here if you look at the forbearance plans among the GSE loans, they were down 18%, and 42% have become re-performing. But if you look at FHA and VA loans, they see probably the most modest decline of 14%, so less than the portfolio and private securities, and also less than the GSE loans. Also here it says 21% of the VA borrowers are re-performing, so they are less than the portfolio and also GSE loans, and they are about 21%, and as you know a lot of VA loans are actually 0% down. And 27% for the FHA they are re-performing, and only 6% have paid off their loans, and FHA also has the 3.5% down payment program, so it is very interesting, you see that most of these lower down payment loans have the higher forbearance plans still. Again, I think if we look back to where we are in the Bay Area, we don’t have as many of these FHA and VA loan programs, so that’s why we’re not getting hit as hard.

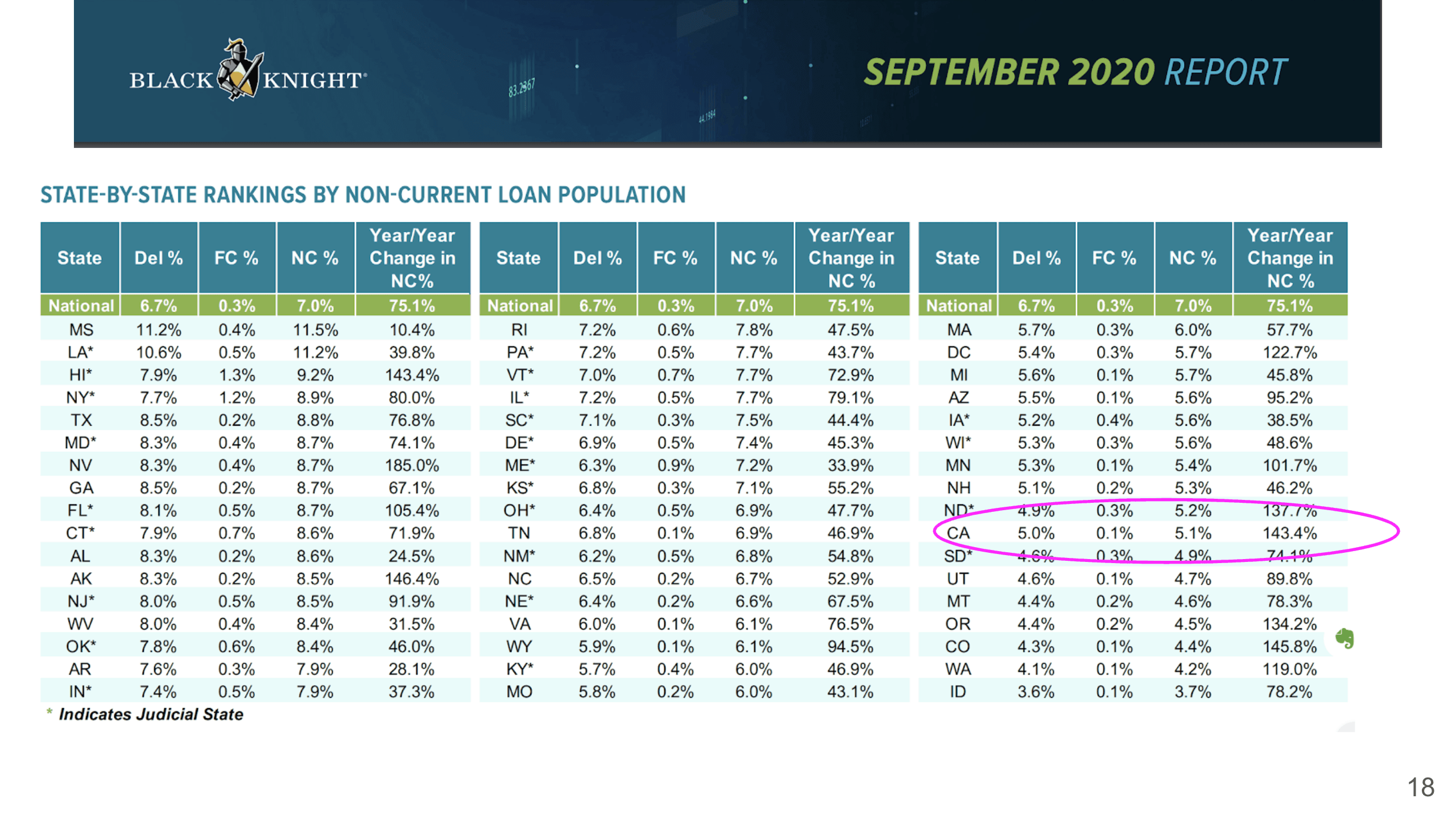

Here, again you look at the state by state rankings regarding the non-current loan population. In California, we are actually one of the lower ones. The delinquency is 5% compared to the national 6.7%, and the foreclosure percentage is 0.1% in California versus national 0.3%, so we’re below the national level, as well as this non-current percentage, which is nationally 7%, we are at 5.1%. Although we did definitely have increased quite a bit compared to before, if you compare nationally, we are much less than the national level. Again, I think if you hear a lot of news outside talking about the housing market, I just want to remind everybody to make sure that you’re looking locally, even if we’re talking about California, obviously California is huge, and there are a lot of different markets. The Bay Area market and southern California markets are still very different, so here I am just showing at a high level what the California market is doing right now.

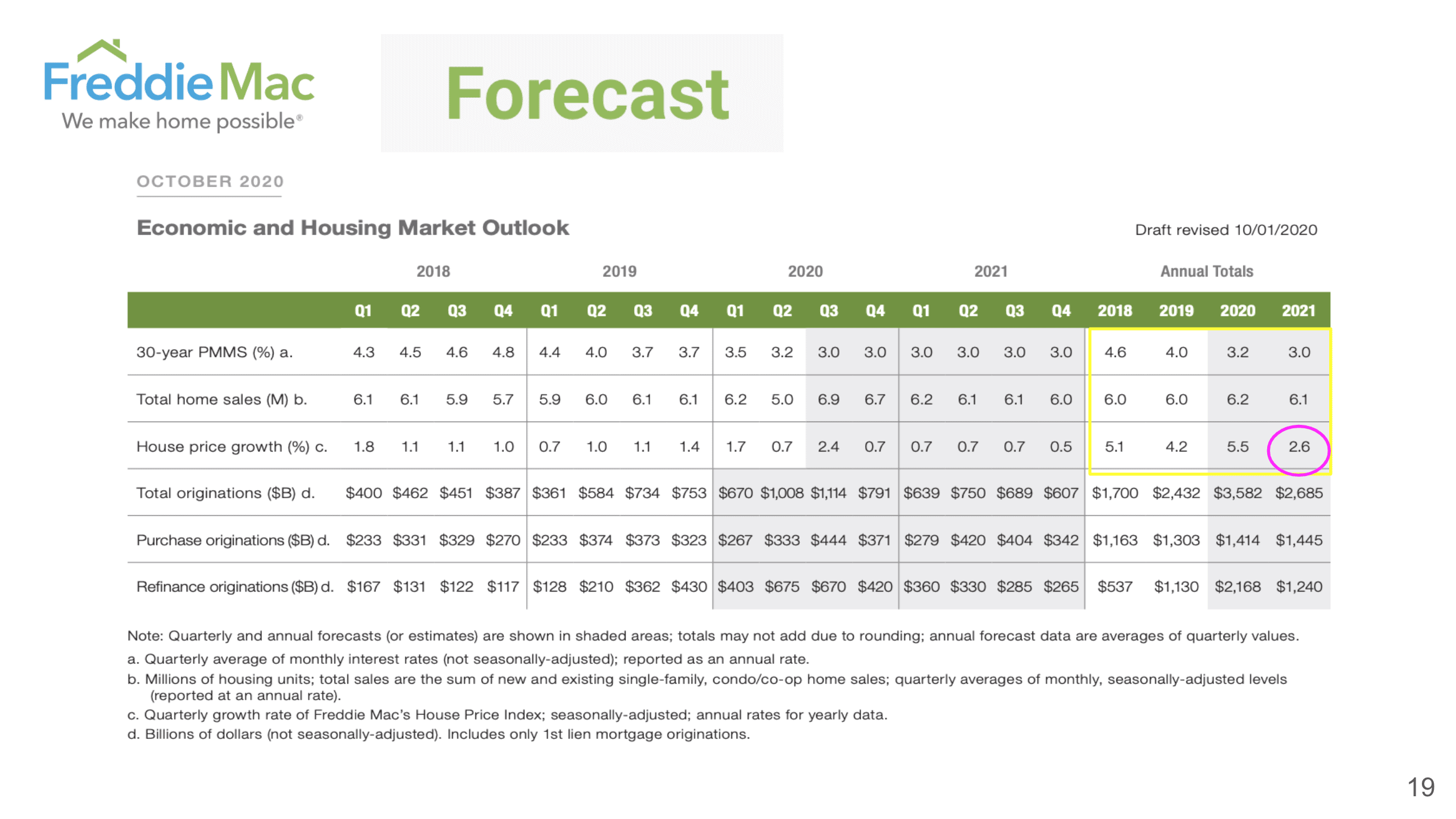

Freddie Mac has its forecast on home sales for 2020 and 2021. As you see that they are actually predicting a higher sales volume, meaning more people are coming out to buy. And they’re predicting that actually, the mortgage rate is a little bit lower than before. You see 2018 went up to 4.6%, 2019 was 4%, 2020 is going to be 3.2%, and 2021 is 3%. As for the house price growth, it was 5.1% in 2018, 4.2% in 2019, and they have adjusted to 5.5% for 2020, but 2021 is actually a little bit more moderate at 2.6%. I think a lot of people wonder if 2021 is going to be a transition period where the prices might come down slightly, to me I think it is still going to go up a little bit, and I will talk about why. But at the same time, it’s not going to be as aggressive, just like what Freddie Mac is forecasting here.

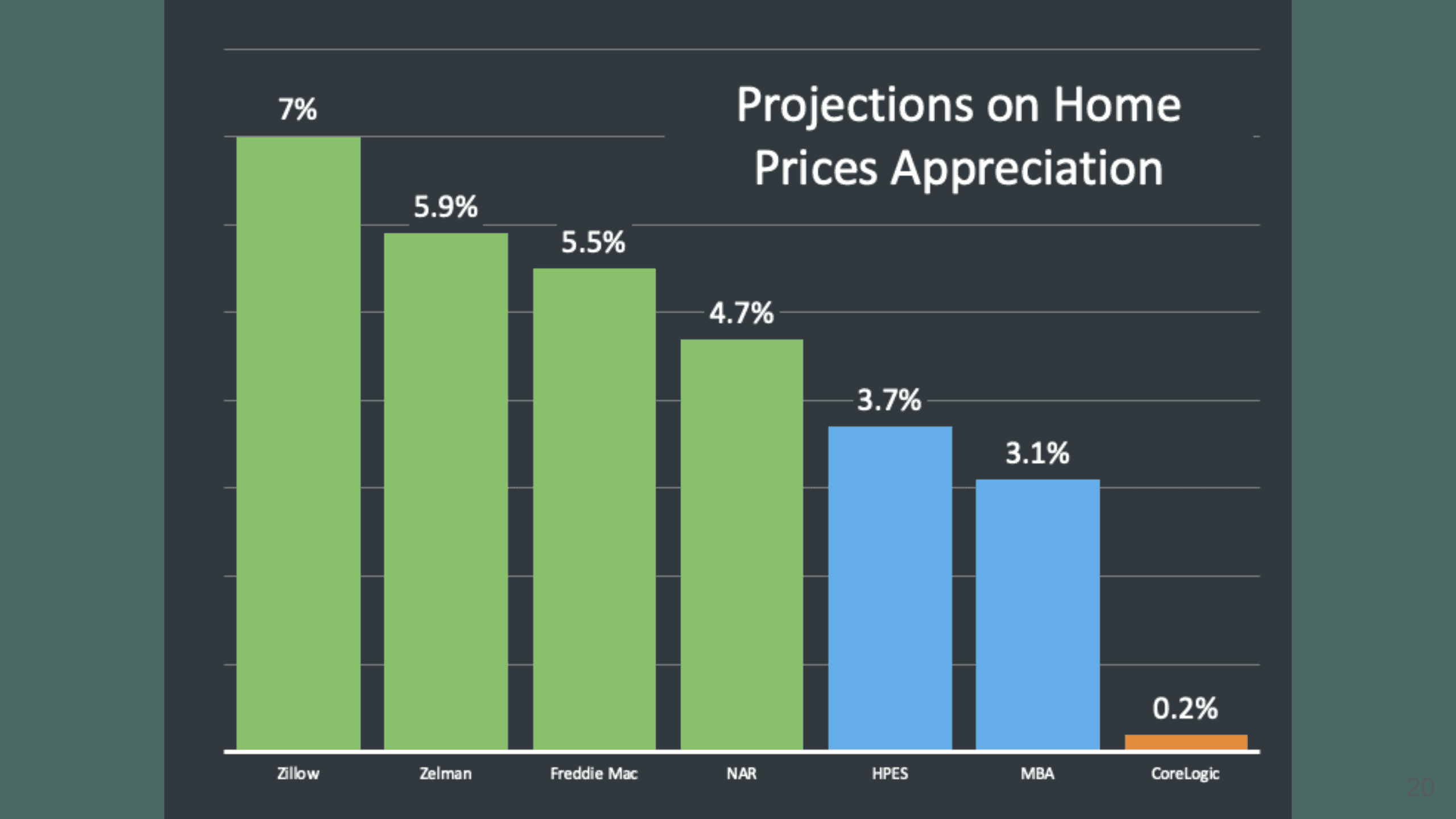

If you look at forecasts from other organizations, Zillow is forecasting 7% appreciation, Zelman is projecting 5.9%. As you remember from last month, we talked about Zelman literally doubling their projection from 3% to 5.9%. Freddie Mac is 5.5%, National Association Realtors is 4.7%, HBC 3.7%, Mortgage Bankers Association 3.1%, and CoreLogic is the most conservative at 0.2%.

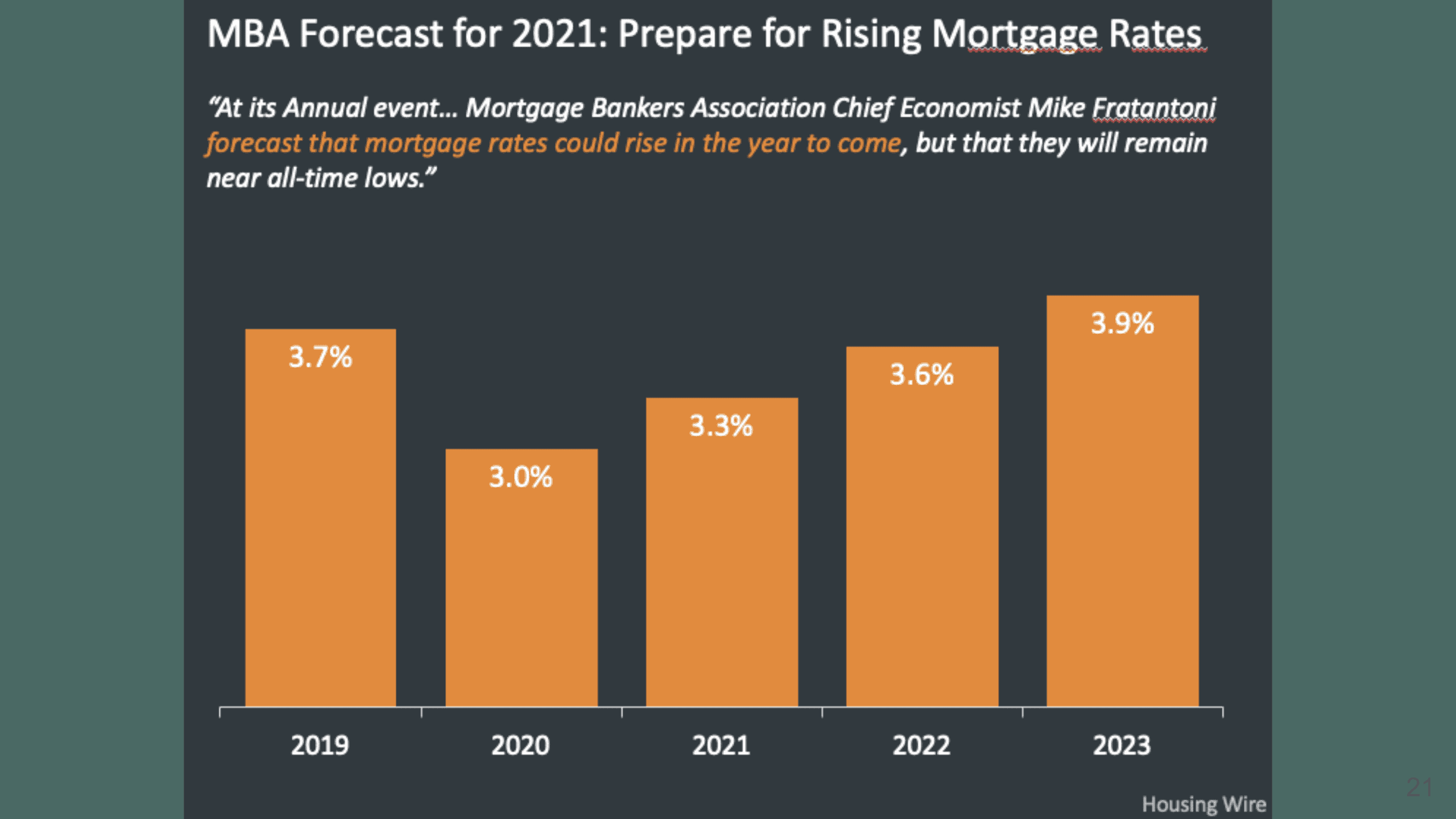

These are the mortgage rates that the Mortgage Bankers Association is forecasting. It’s going to go up a little bit – 3.3% – in 2021, 2022 is 3.6%, and 2023 is 3.9%.

What about the multi-family market? We are also very worried about the renters not paying, especially because we have the eviction moratorium going on right now.

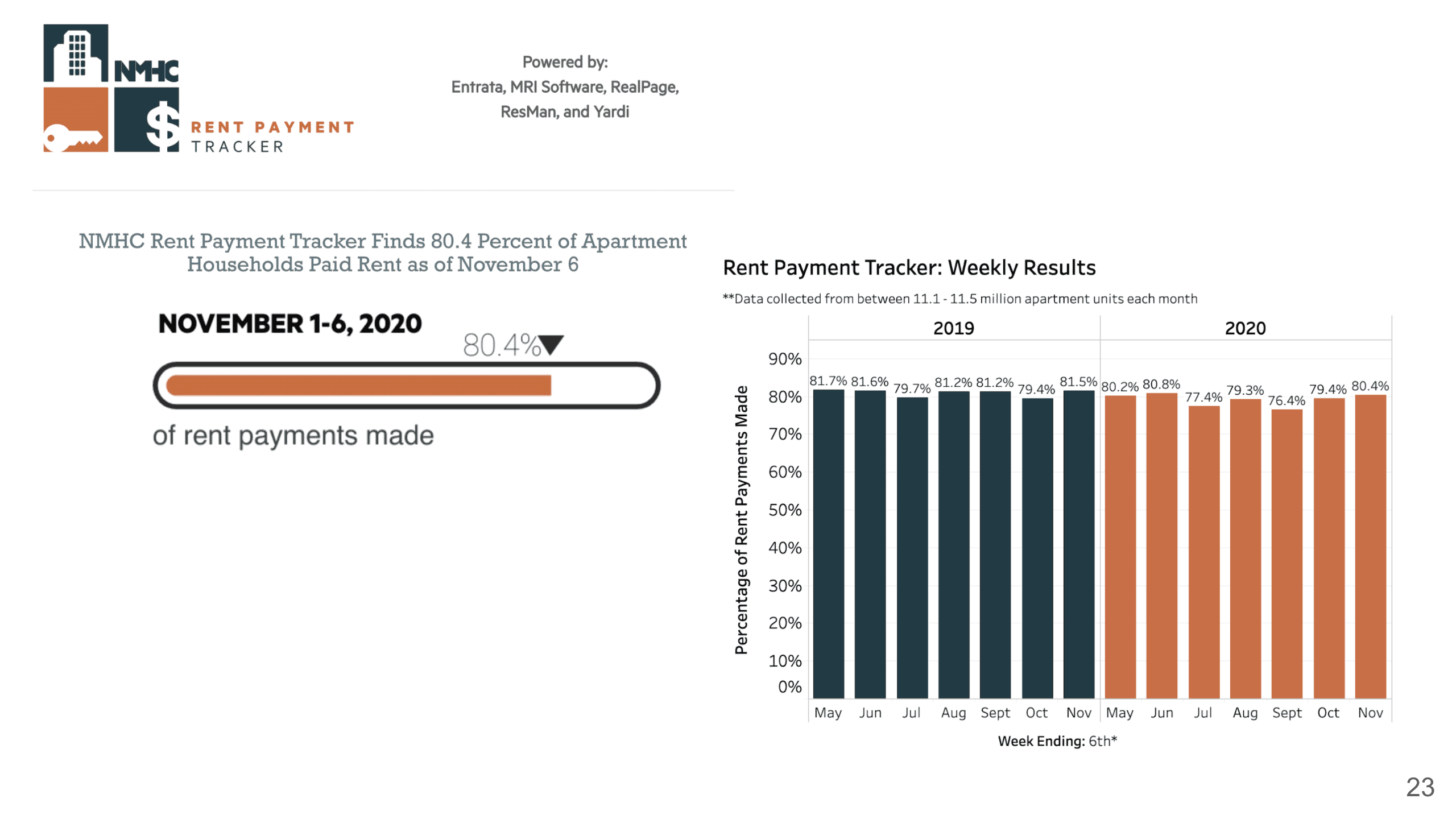

This is the rent payment tracker from the National Multifamily Housing Council, it actually shows that 80.4% of the renters are still paying rent. If you put the chart from 2019 here side by side, we’re pretty much pretty close to how 2019 was doing. We definitely saw a dip here in July at 77.4%, but I think overall 80.4% is very much in line with how we were doing in 2019.

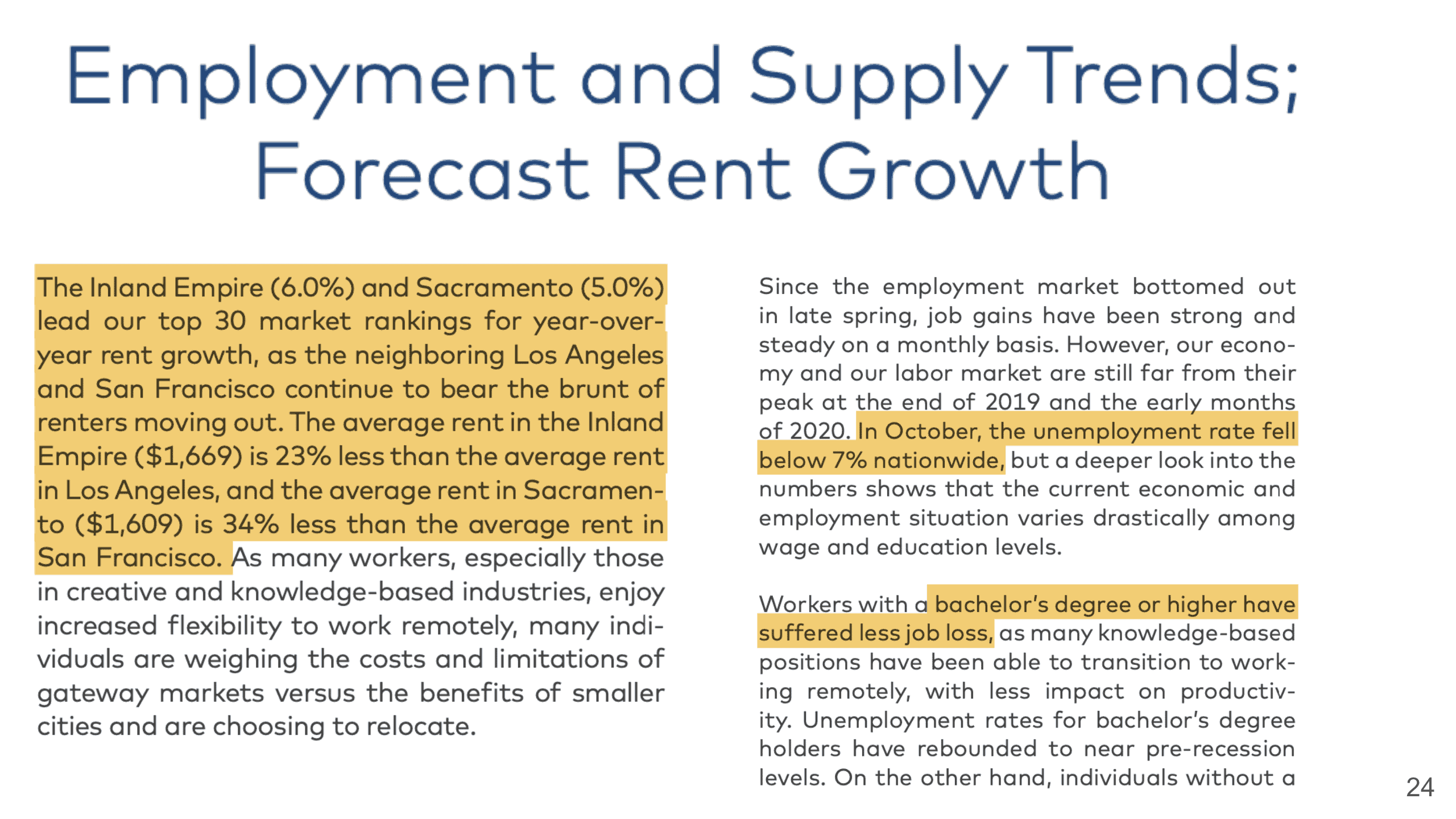

What about employment and supply trends and forecast rent growth? “The inland empire (6.0%) and Sacramento (5.0%) lead our top 30 market rankings for year-over-year rent growth, as the neighboring Los Angeles and San Francisco continue to bear the brunt of renters moving out. The average rent in the Inland Empire ($1,669) is 23% less than the average rent in Los Angeles, and the average rent in Sacramento ($1,609) is 34% less than the average rent in San Francisco.” So that’s why because of the current situation, pandemic, and working from home, we do see more people moving to less expensive areas, out of San Francisco. In October, the employment rate actually fell below 7% nationwide, and we do see that workers with a bachelor’s degree or higher have suffered less job loss.

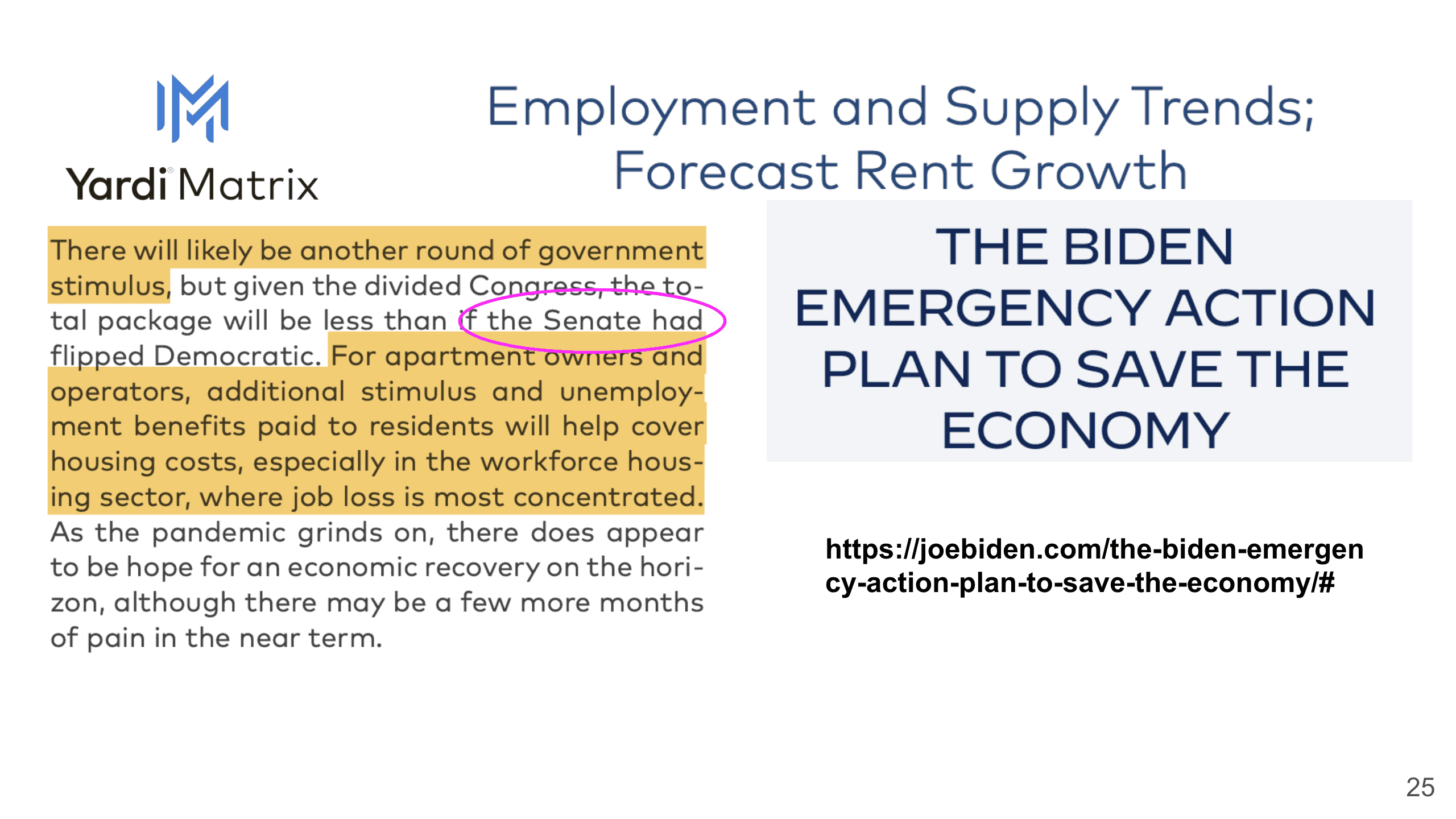

Yardy is a software that most of the property management companies use, so they collect a lot of data. They say that “there will likely be another round of government stimulus, but given the divided Congress, the total package will be less than if the senate has flipped democratic. For apartment owners and operators, additional stimulus and unemployment benefits paid to residents will help cover housing costs, especially in the workforce house housing sector, where job loss is most concentrated”. So, you know, one thing again that we worry the most about is that if there are a lot of job loss, people cannot pay for their rent, and what happens is that it just keeps rolling to basically the landlord cannot pay for their mortgage, and then the property is going to get foreclosed, and that can cause a lot of housing crisis. Now that we know that Biden is our president-elect, he does have an emergency action plan to save the economy, you can go to his website and read through it, and he does have a new stimulus package that he has been talking about. Since the majority of the senate right now still seems to be republican, we do believe that these stimulus packages should be able to be passed, so hopefully, that will be able to help some of these tenants and property owners.

We talked about the eviction moratorium, it has been really scary for a lot of people, because many property owners just cannot afford to pay the mortgage payments, so they really need to sell. The same thing for multifamily buyers, they don’t want to buy it because they don’t know what’s going to happen. Most of the landlords do want to work with their tenants, but at the same time, they are kind of caught in the middle – they cannot afford to lose their building either. That’s why the additional stimulus package for housing and food expenses is really key to ensure the tenant can pay rent, and continue to keep the landlord and tenant relationship healthy.

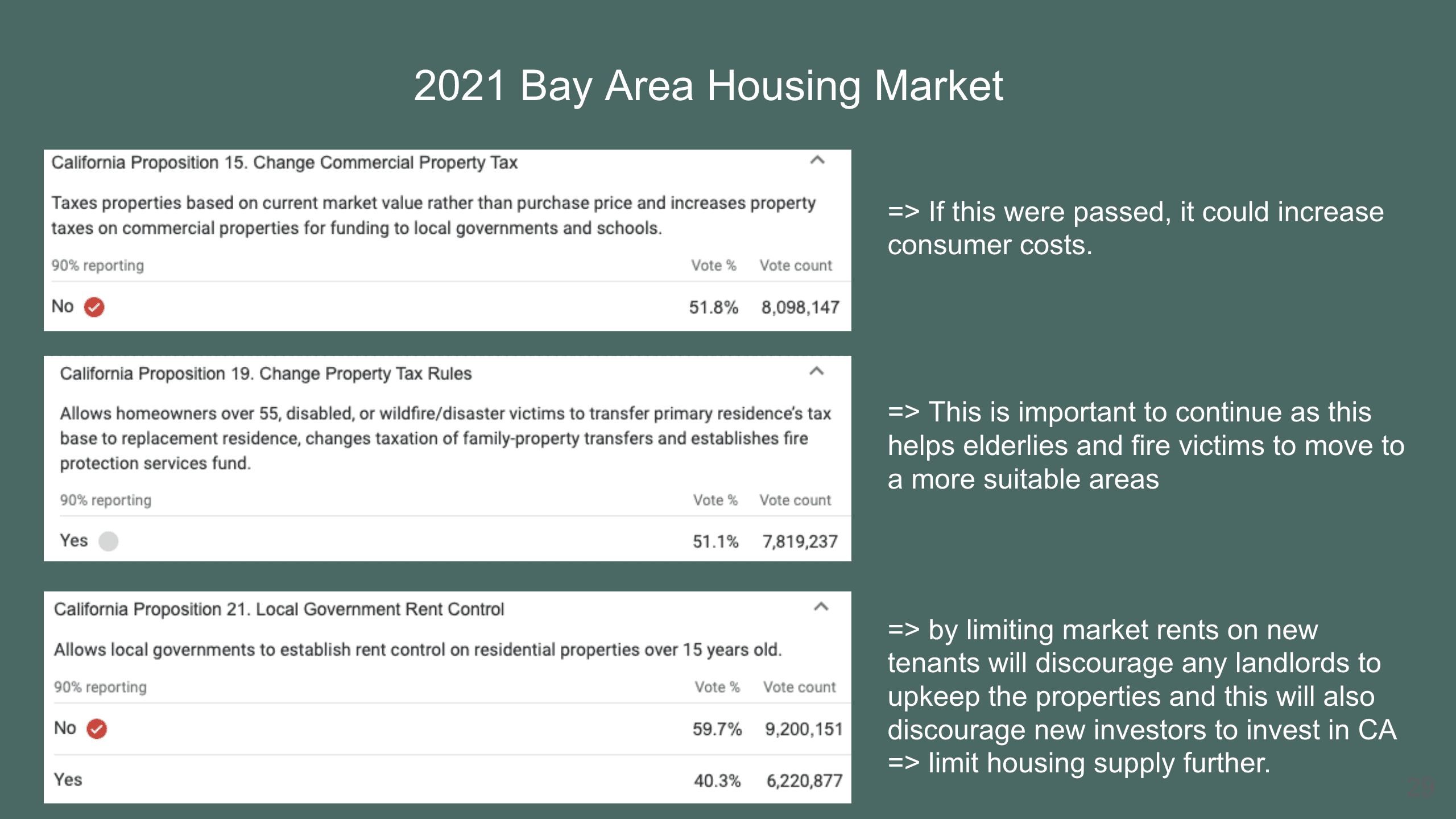

Lastly, I just want to go over these propositions. We just saw Prop 15 that changes commercial property tax didn’t go through, because if this were passed, it definitely would increase the consumer cost. Proposition 19 changes the property tax rules, specifically for wildfire and disaster victims. This is important because it continues to help the elderly and also these fire victims to move to more suitable areas. Prop 21 limiting market rents didn’t pass but if it did pass, it actually limits market rents on new tenants, which will then discourage landlords from upkeeping the property, then the property is going to become very dilapidated. It will discourage investors from coming to invest in California, so I’m really glad to see that Prop 21 did not get passed.

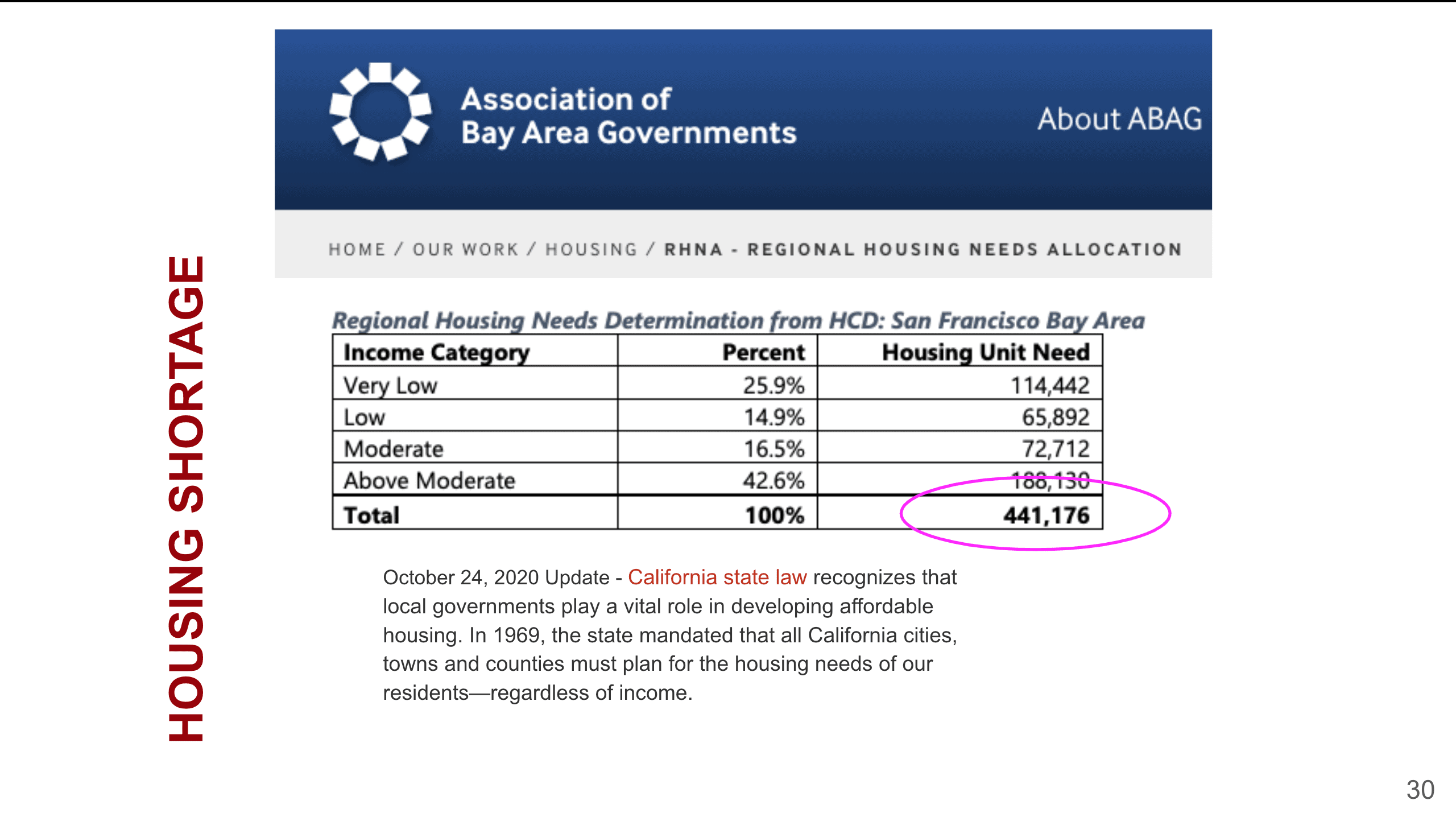

In the Bay Area, we still have a housing shortage. As of October 24, we have 441,176 housing units needed, so RHNA has been coming up with plans and asking local cities to try their best to encourage housing developments. In California, they are actually allowing local governments to do their part to build more housing instead of issuing state laws.

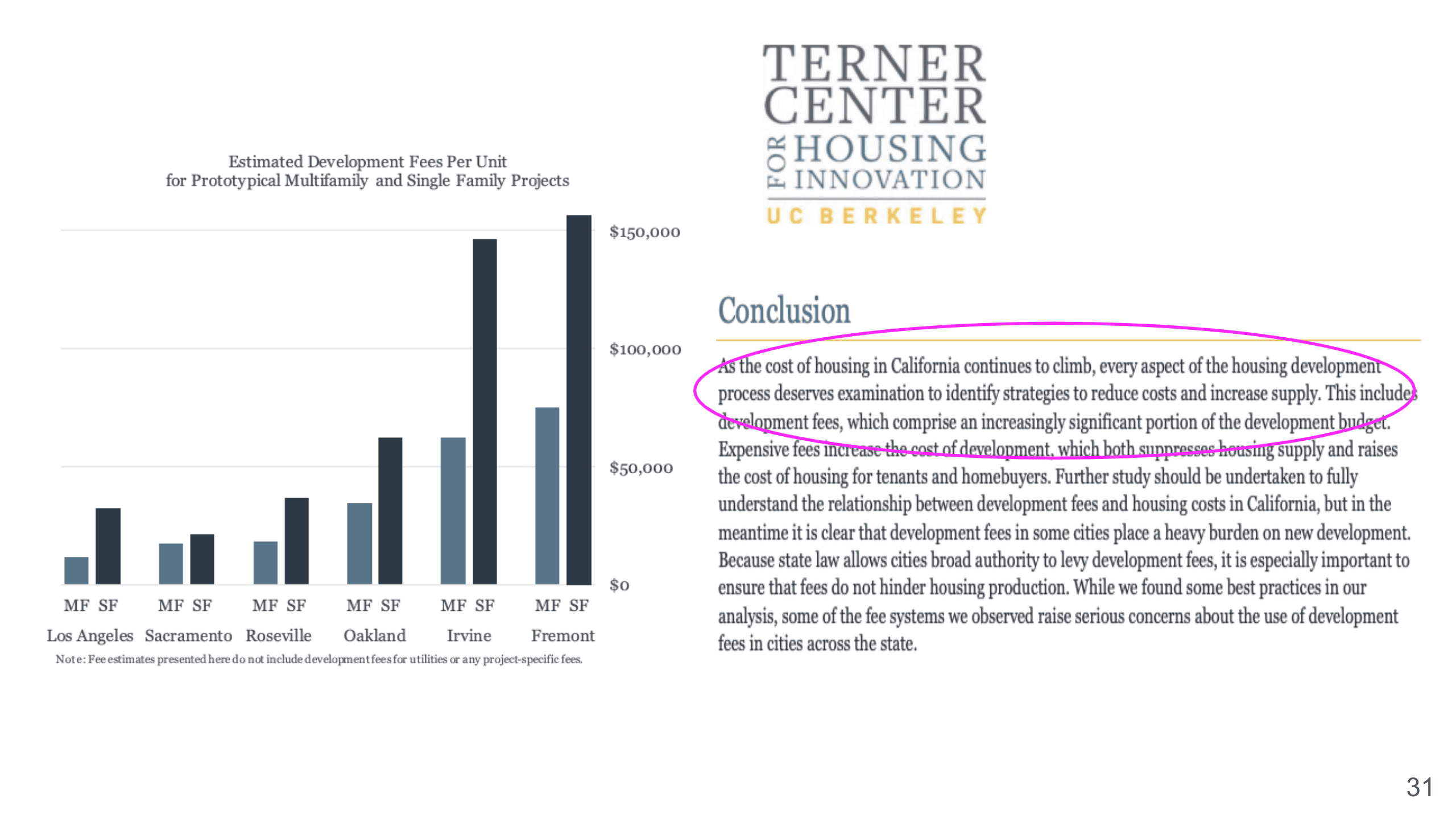

Because of that, as you see here, UC Berkeley has done research on development fees in different cities including Los Angeles, Sacramento, Roseville, Oakland, Irvine, and Fremont. Depending on which city you’re building, you will see a very different development cost. You know, we talk to developers sometimes and a lot of developers do say that they don’t really want to build in certain cities because of the cost.

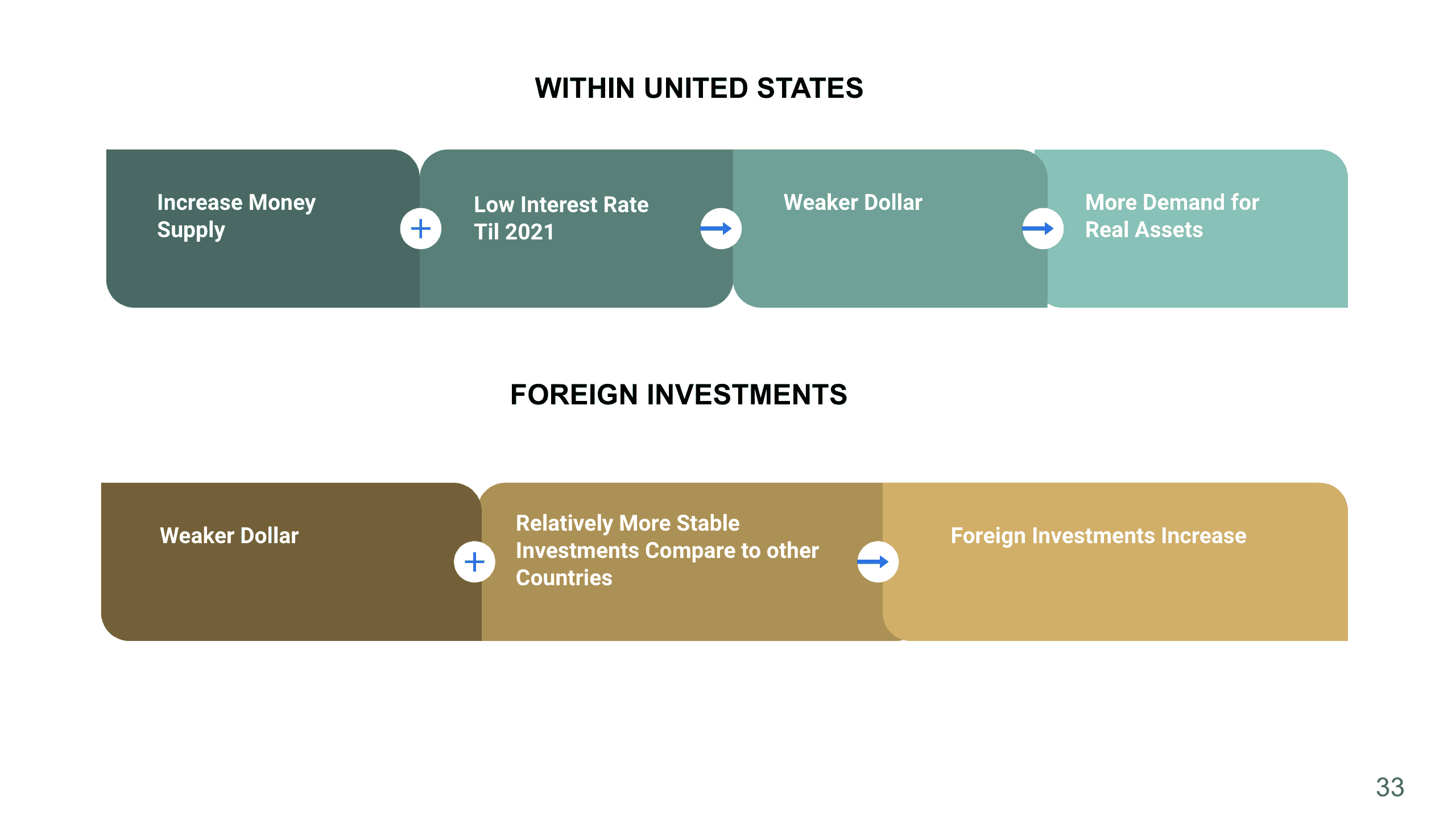

Now, since we have been printing money, the money supply has increased drastically from 3 trillion to 7 trillion dollars.

Plus the lowest interest rate, the dollar will become weaker. As a matter of fact, because of that, more people are going to look into buying real assets instead. We’re probably going to see more foreign investors as well because when they compare globally, the United States still has more stable investment compared to other investments.

Finally, if the vaccine really does come out, more sellers are going to be more comfortable to sell, and that’s why we probably have an increase in inventory, increase in the new listings. That is the reason why I believe that in 2021, even though we continue to have high demand, we probably also will have a higher inventory, so the increase in prices will not be as significant, but we will still have a moderate increase.

We hope this month’s market update is useful to you, if you have any thoughts or questions, please don’t hesitate to reach out to us, schedule an appointment now! Want to learn how to become a successful real estate investor by investing through a partnership? Watch the full episode of this month’s Bay Area Housing Townhall and hear from Jeff Lerman!

Stay up to date on the latest real estate trends.

And what to check before upgrading your internet plan

HAYLEN, an Asian-owned, people-first real estate firm, selected to steward real estate process for J-Sei Home’s next chapter

You’ve got questions and we can’t wait to answer them.