When will the housing market cool down? – Feb. 2022 Housing Market Updates

Welcome to our February Bay Area Housing Market Update. Let us take a look at what happened in January 2022. You can also watch the video recording of this market update on our YouTube channel.

Last time, I showed you the first weekend of an open house. People were lining up out the door. In the last 30 days, a lot had happened. Markets are still flying off the shelf. To be honest with you, a lot of listings do not even get to the market. People are already making offers, left and right.

For example, single-family in West San Jose sold off-market. The townhouse in San Jose got 5 interested pre-emptive offers, and we have to stop them from submitting the offer until the deadline. In the end, it was sold 20% over asking.

The above picture is of a fixture and is staged. I honestly do not think that they needed to stage this, but it is two bedrooms and one bath in Sunnyvale. The asking is 2.3 with mold. But, of course, people are buying this actually to redevelop and to build their dream home. This is just to show you how crazy the market is and that too for a property like this. This is a 9000 square feet lot, and they are able to build 3500 square feet house on this lot. We went under contract really fast though, within seven days. You have to understand though that such properties with peeled paints and mold, typically you cannot get conventional financing. Most of the time you can only buy with cash or hard money lending. It is mainly because conventional lenders cannot lend you on a home that is not considered livable. The reason why they would not lend on these types of properties is that having mold and having peeled paint are considered a health hazard. I know a lot of our clients would like to buy a fixer-upper. This is a different level of a fixer-upper. For this level of a fixer-upper, you will have to consider using hard money lending or some kind of bridge loan that is lending you the money based on equity, instead of based on the loan to value. If you do have any more questions about that, please feel free to let us know.

All these offers have been crazy. If you talk to our team, I can tell you everybody has been so exhausted. It is because of the offers, one after another, and they just keep getting bid out, and the thing is you cannot even comp it out anymore. Unfortunately, we have to tell our clients that you have to expect to pay $100,000 to $200,000 over the appraisal value. Why is this so important? It is because if you are doing 20% down, the bank would only loan up to 80% of the lower purchase price or your appraisal value. If it does not appraise, then that means you have to pay 80% of the appraisal value and then, pay the difference. Now, it is dangerous if you do not understand why that can make a big difference because if you do not have enough money in your bank account to cover that difference and you have made a non-contingent offer, you may not be able to get the loan and you will be risking your 3% earnest money deposit.

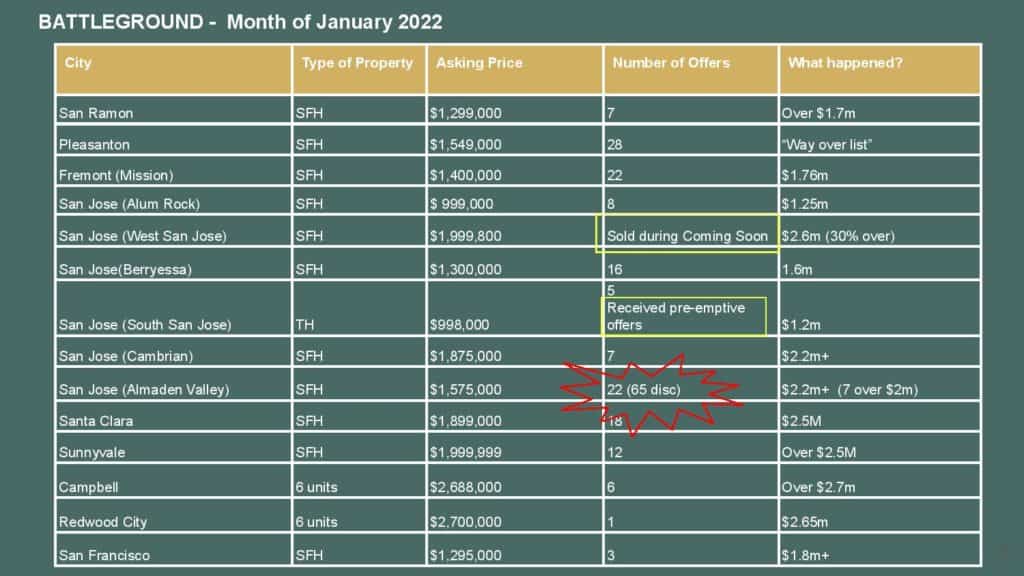

Many properties, in San Ramon, had gone $400,000 over the asking price. We do not even know how much it has gone over for Pleasanton. In Fremont (Mission) area, another $360,000 over and Alum Rock, it is $250,000 over and West San Jose, it is 30% over, sold during coming-soon, not even on the market. In Almaden Valley, they sent 65 disclosures. They received 22 offers and even the asking price is $1.575, 7 of them were willing to pay over $2 million, and we know for a fact that when we did the comparative analysis, the comp is around $2 million. That means appraisal is going to be around $2 million, but still, 7 of those 22 offers were willing to pay above and beyond the appraisal value.

These are some examples. I know it sounds a little bit discouraging; but I guess, if you look at the multi-family side, it is not that crazy. For example, Campbell, the asking price is $2.688. They did get 6 offers, but their offer price is not as aggressive. Some of them made an offer below the asking price, so it just barely went over the asking. The same thing for Redwood City, it got accepted slightly below the asking price.

Single-family definitely is a lot hotter compared to multi-family and townhomes, but then, it is still there. There are so many demands. A lot of them are making offers before you even hit the market.

How do I make an offer on properties that are not even on the market? Well, work with your realtors. They have access to some of the off-market properties.

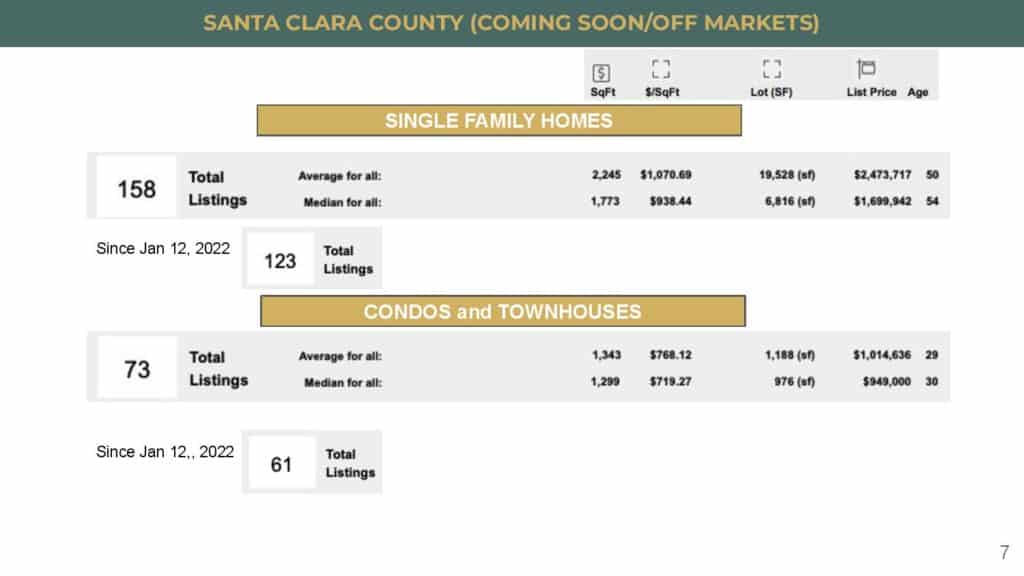

If you are looking on Redfin and Zillow, you may not be able to see everything because if I am looking at my database, there are 158 off-market listings right now in Santa Clara County, for single-family homes. Out of these 158, since the last housing market update that I provided you, they added 123 of these off-market listings. Some of them, you can start seeing and some of them are not ready, yet to be shown, but be sure to work with your realtors and make sure that they are sending these listings to you.

For condos and townhomes, the same thing. Currently, there are 73 of these off-market or coming-soon listings; and since the last house market update, there were 61 added into the database.

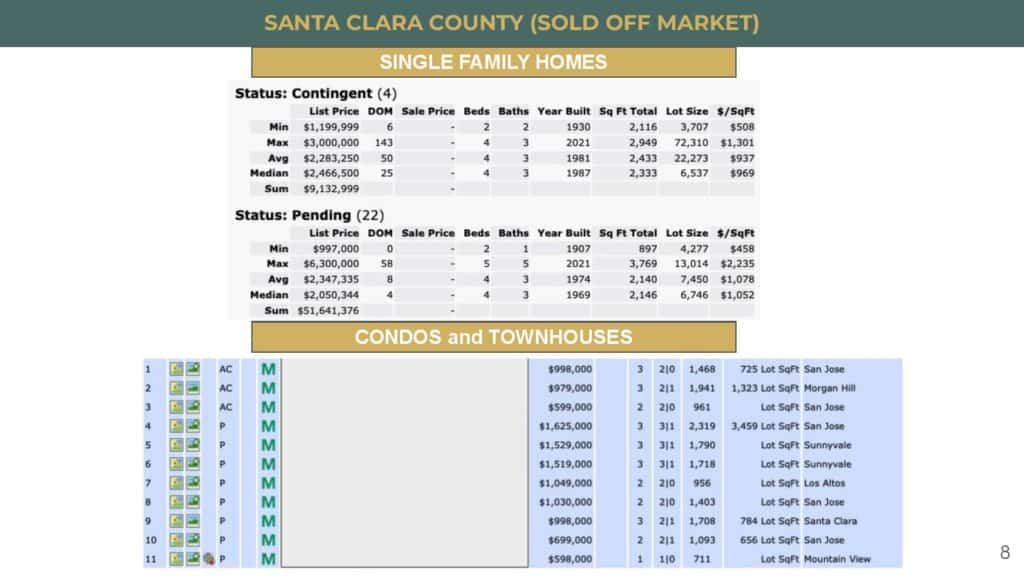

How many of them have sold off-market? To be honest with you and relatively speaking, it is not that much. Because they are only 26 of them that went under contract for single-family homes. Contingent means they have a contingency. When you are off-market, believe it or not, you actually can have some kind of contingencies because they probably do not even have all the disclosures, all the inspection reports yet. If you are buying off-market, there are still chances you can put a contingency on there. But, of course, most of them are still pending, meaning all the contingencies have been removed.

As for condos and townhomes, the same thing. “AC” means active contingent. So, there are contingencies here as well, and “pending” means there are no contingencies. There are 11 of these listings off-market that are never shown on the public portal that had gone under contract.

You can see that people are able to buy off-market, and we have helped quite a few clients to do that as well.

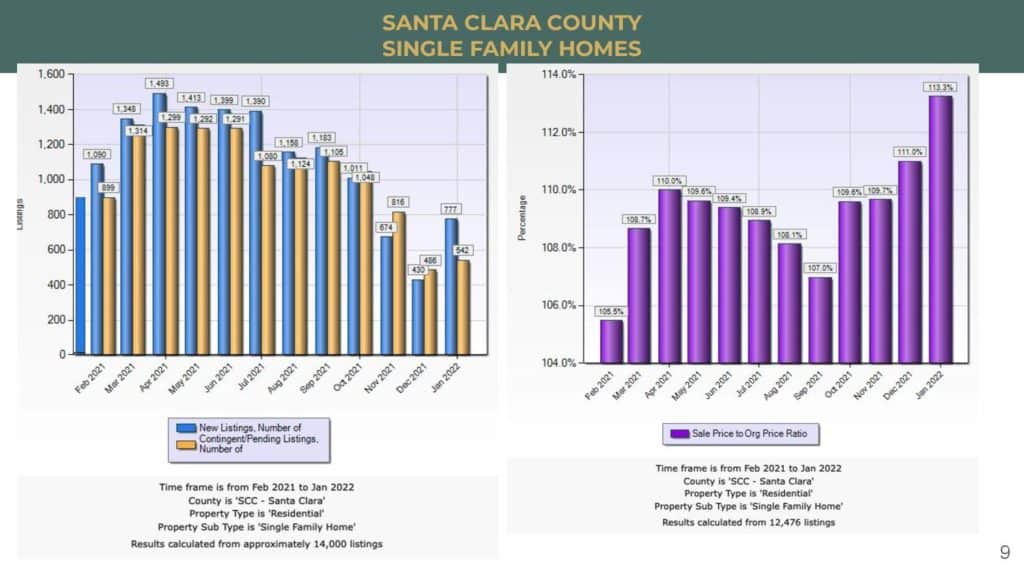

Now, let us look at the inventory level. Today, I am going to use the chart a little bit differently from before. If you look at the blue bars, it says the number of new listings versus the number of contingent and pending listings. Meaning how many new listings came out and how many had gone under contract. We looked at these numbers before already. December has gone down quite a bit and then all of a sudden January starts and sellers are ready to sell. A lot of them started to come onto the market. These are the new listings that came on the market. We have 542 versus 777 properties that have gone under contract.

If you look at the inventory level. I added this bar. It was from January 2021. We were still quite a bit below last year’s January numbers. We are 150 listings less compared to last January.

This is also why you see how crazy we are to bid for these properties. We are at 13% now – Way higher than the last 12 months. We are at 13% over asking in order to win these properties.

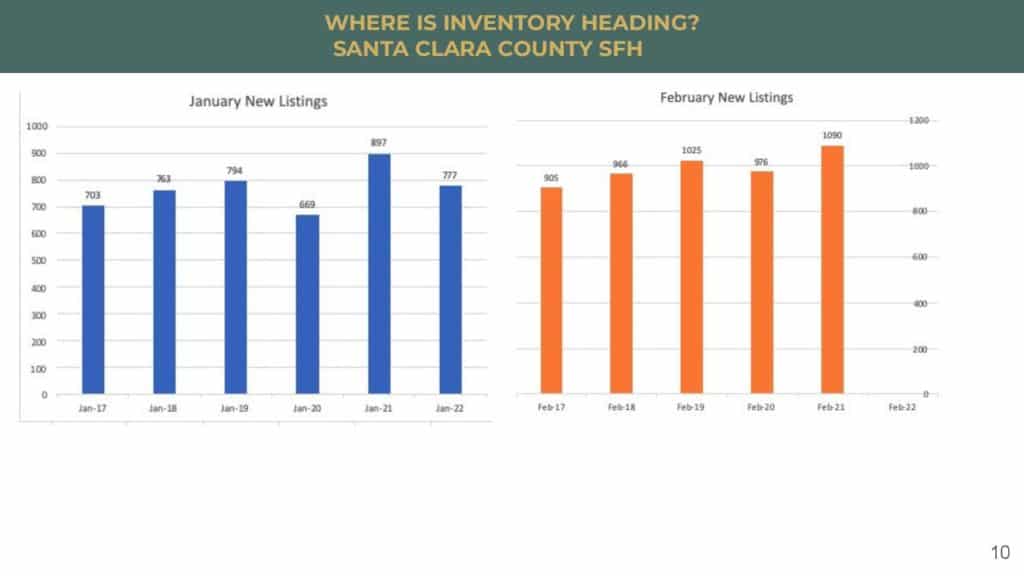

If we look at every January, comparing how many listings as I mentioned earlier; in 2021, we had almost 900 and then, this year, we only have 777 units. But if we look back to the last 5 years, we are not too bad. It was just last year that we had a lot more listings compared to the other years.

In February, as you see compared to January, we always have a little bit more because that is when sellers are getting ready and they are ready to come on the market. In February of 2021, we have about 1000. This year, like January, we expected again less than last year, but it should be going up, towards more than 900 or so new listings are going to come on to the market.

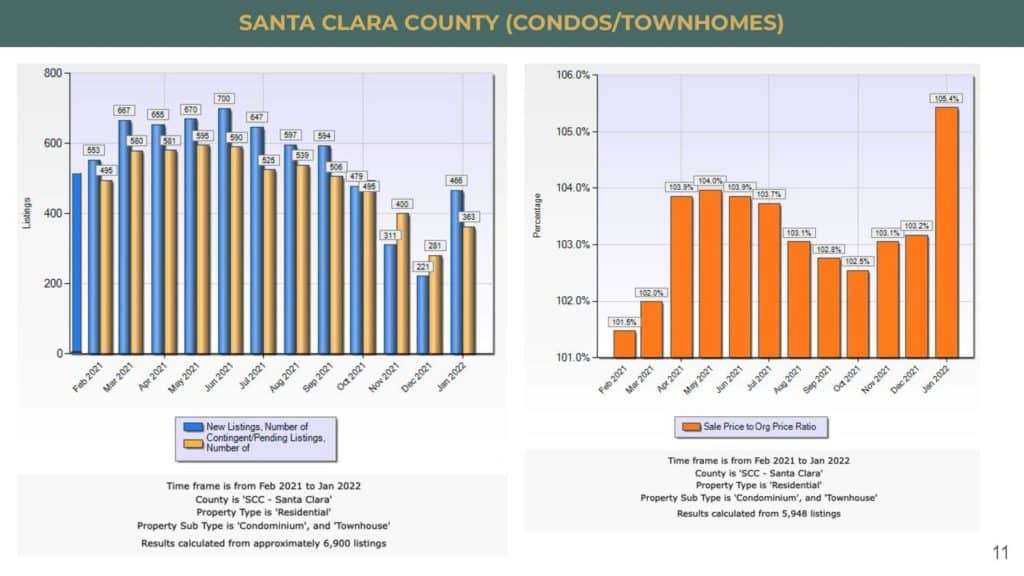

For condos, very similar scenario. We have quite a bit of new listings coming up compared to December more than double for condo and townhomes. Condo and townhomes are a lot faster. When we prepare these properties, we pretty much clean them up interiorly and we do not have to do any exterior work. So, that is why you see that they pop up a lot faster compared to single-family. We do see a lot of people are buying these and as I have shown you earlier some of the townhomes are still getting multiple offers. If we again compare to last year, we also have fewer new listings compared to last January. Just like single-family this year, because we have fewer listings, you see the competition level is also higher, not as bad as single-family. We are at 5.4% versus 13%, but still much higher than the last 12 months.

In terms of the number of units, we are more than 2017 all the way to 2020. In 2021, again, we have had a lot higher listings compared to the past few years. This year, we are still not bad. We have less than last year, but we are still more than the past 2017 to 2020.

In terms of competition level, in 2018, it was the one that has the highest sold-over-list percentage because it has such a low inventory. Right now, we are still around 106% over asking.

You get a sense now that in February, we are probably going to have slightly more still compared to last year, and just know that your competition level is probably going to be around the same of 5% above the asking price.

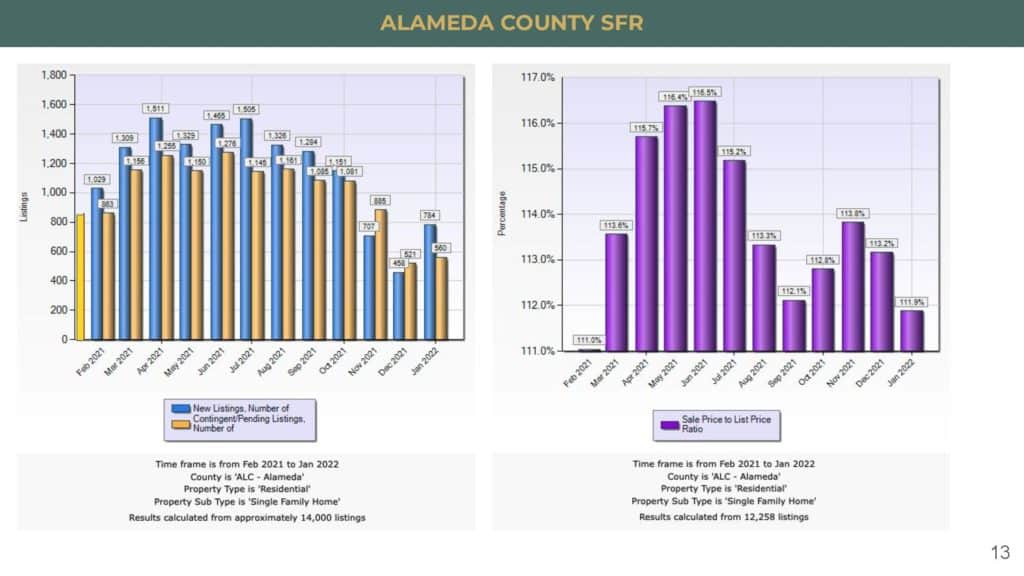

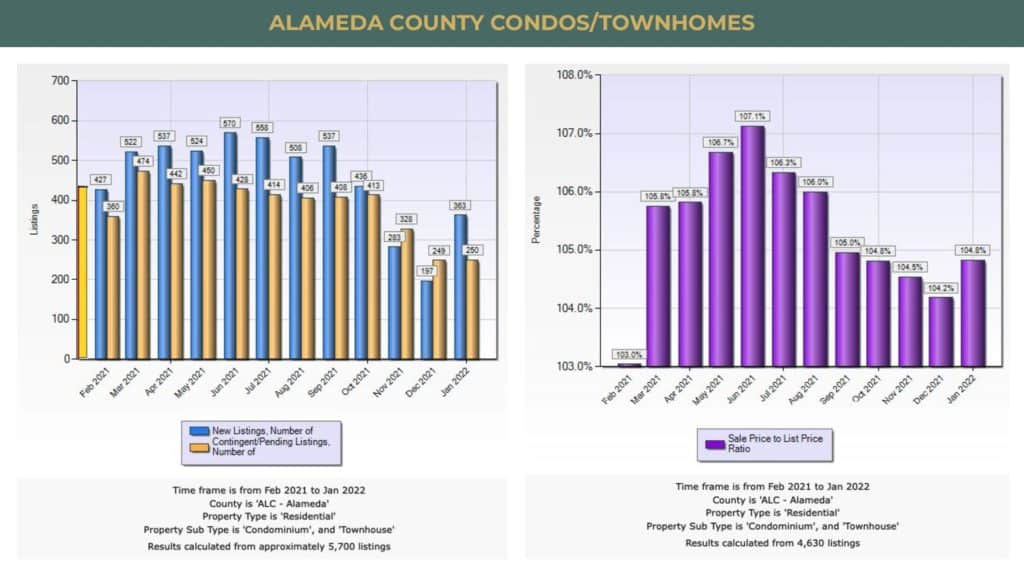

In Alameda County, we have a very, very similar situation. The January listing also had come up quite a bit, but then it is still shy of what we had in January 2021. It is really across the board throughout the whole Bay Area.

Alameda county is really interesting. Last year, it was so competitive. If you remember just now as we were talking about Santa Clara County, we were 13% over and which was the most competitive in a while. Alameda County, last year, they were very, very competitive, but this year, came down a little bit and they are not fighting for the property as hard. We are going to see if it is going to continue this trend, but either way, they are still over 10% over the asking price. It is still very competitive. We are just comparing historically whether it is more competitive or less.

We used to hear a lot of people saying, “It is fine! We can live a little bit further out.” But recently, we are starting to hear that people are thinking, “I might have to go back to the office, so I might have to live a little bit closer to public transportation or a less short drive.” It seems the trend is coming back to saying, “I need to be a little bit closer to work.”

For condos, it is the same thing. It went up quite a bit, almost double, and it is not as competitive. It is not over 10% asking price, but it is 4.8 over the asking price in order to win the properties.

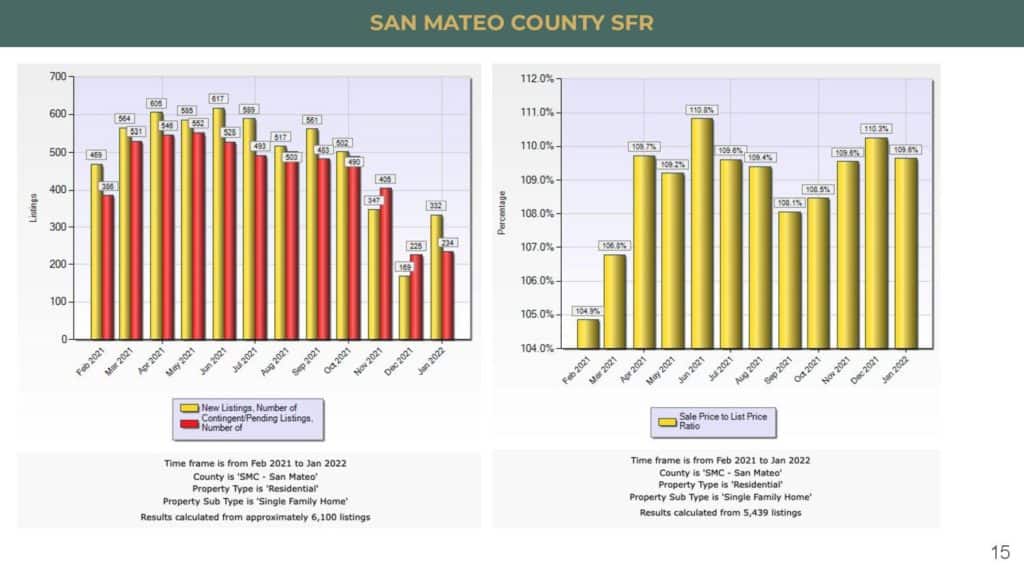

In San Mateo, we went from 169 units to 332 units, new listings in January. As far as competitiveness, it is right around 10%, and it has been pretty consistent since last year. It is right around 10% over the asking price.

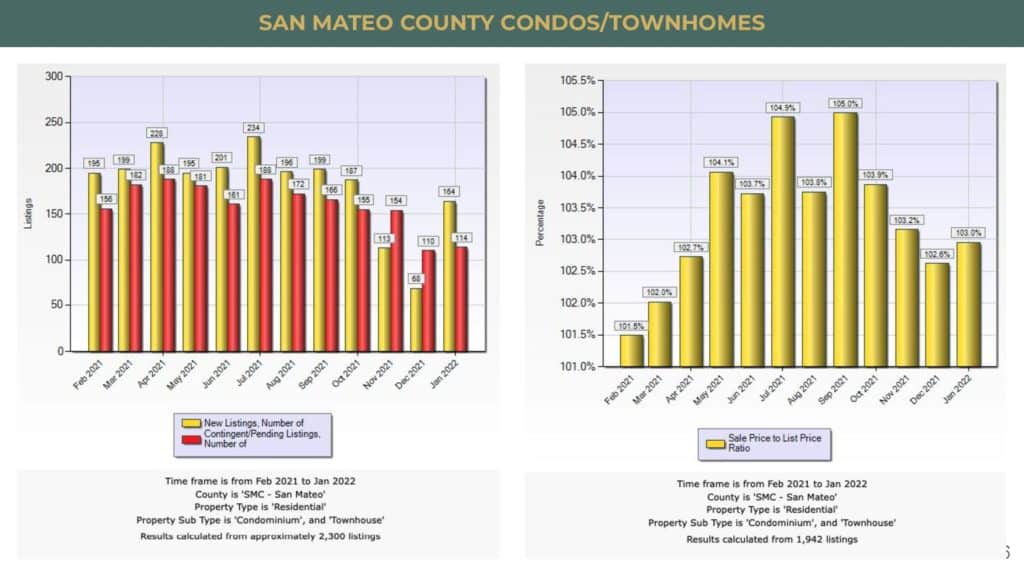

For condos, it is way more than double, from 68 units in December went to 164 units in January. You probably can find a little bit less competition, so you do not have to bid as hard. It is only about 3% over asking. I think in San Mateo County, the condos and the townhomes are less competitive. You do not have to be that stressed out if you are bidding over there.

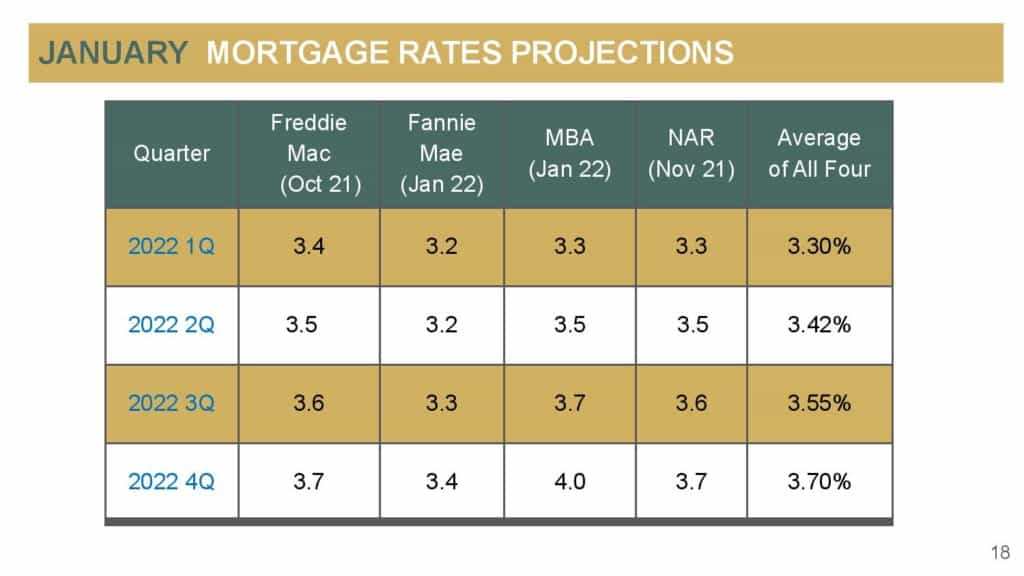

Let us check out the mortgage loans. I have been waiting to see if I can find more updated mortgage rates because I mentioned last month that due to inflation I expected their projection to be higher.

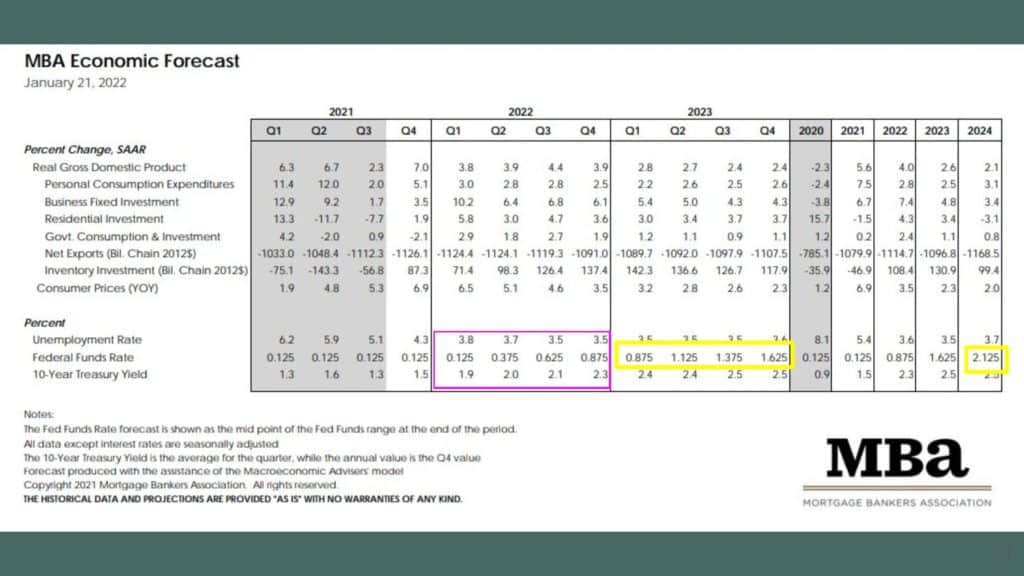

Projection of Mortgage bankers association and Fannie Mae stays the same. They are still projecting about 3.7 on average by the time we hit 2022 4Q. I still have a feeling that it is going to be higher than this. So, we will see if they will change the projections in a month or two.

This is a trendline on the left side, week after week since September, as you see how the rate has gone up quite quickly since December. Now, it is already at about 3.56.

I asked my friend from Wells Fargo, Victor Chow, and he sent me the rate late last night. The Jumbo loan 30-years is at 3.375. I remember in the beginning we have been talking a lot about 2.875, 3, 3.125 and now, it is already at 3.375. Also, the high-balance conforming loan is now at 3.75%. It is getting closer to the 4% range.

Mortgage Bankers Association’s economic forecast, in January 2021, is projecting that the unemployment rate is getting better and better, but Fed Funds Rate, of course, is going up as we have predicted. That is going to raise and probably the first one is going to come up in a few weeks in March and the 10-year treasury yield will continue to go up as well. The mortgage rate correlates with a 10-year treasury yield. It looks a little scarier when you keep looking at the Fed Funds Rate. It just keeps going up and up. Even in 2024, it is going to go up to 2.125. I know it looks really scary and that is because we are so used to seeing Fed Funds Rate close to zero.

Let us look at what other people are saying with these rising rates.

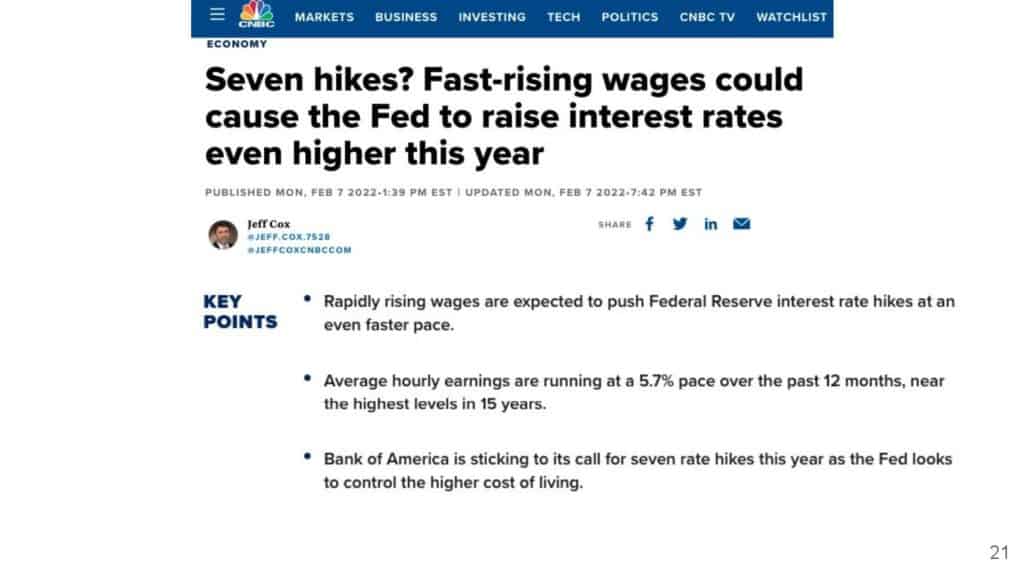

They are talking about they might have seven rate heights. This is probably the most common question. Fast-rising wages could cause the Fed to raise interest rates even higher this year. So, what would happen then? As a matter of fact, they are thinking about that. This whole rate is going to go faster than we have thought because inflation is going really high. The housing market is super hot.

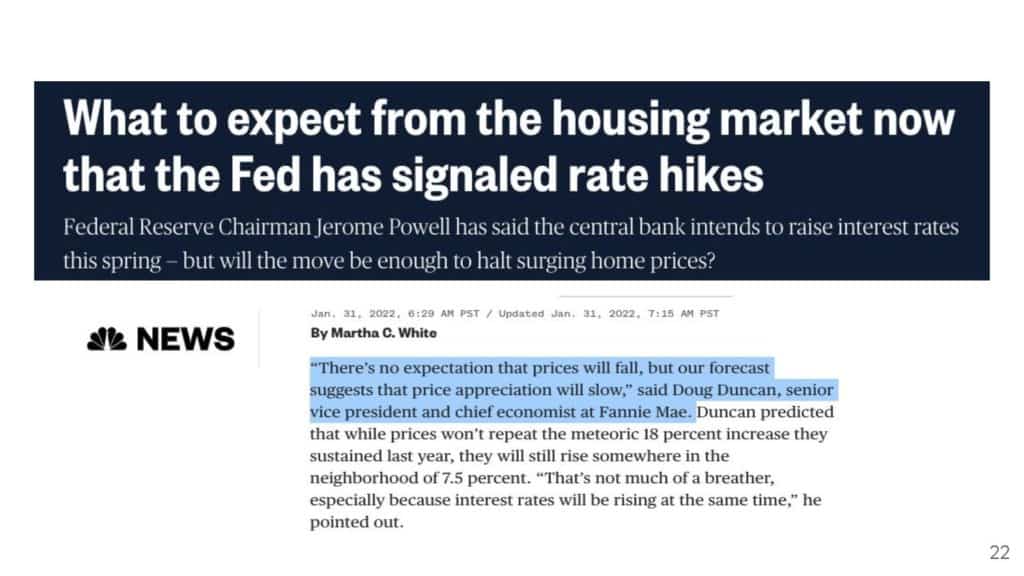

If you ask the chief economist of Fannie Mae, he said that there is no expectation that prices will fall but our forecast suggests that the price appreciation will slow. That is for sure, price appreciation will slow. It is not going to go up 20-30%, double digits like we see right now. Will the price crash? I think that is the question. We have seen a lot of reports. Most economists do not think that the price will crash.

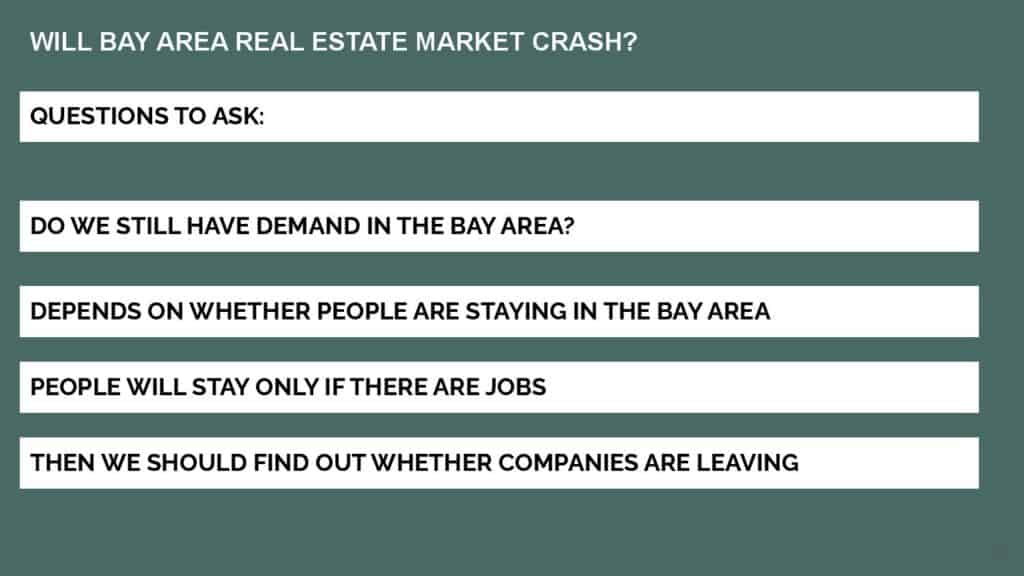

A lot of our clients also ask us this question. When you ask – What do you think about will the real estate market crash because the interest rate is going to go up? By the way, what we are sharing here is very local. We are not talking nationally. We are talking about Bay Area only. The question that you would want to know is – Do we still have enough demand in the Bay Area? If we have demand, then the market should not crash. Knowing if there is demand, we need to know whether people are going to stay here in the Bay Area. But why would people stay here in the Bay Area? Only if there are jobs. If there are jobs, then, of course, people will stay. That means we need to find out whether these companies actually are leaving or are they staying here in the Bay Area.

That is when we started to dig in a little bit more about what is going on with our California market. One thing is that we look at the Fannie Mae report, and they have talked about the select markets with higher expected 2022 employment growth and, of course, San Francisco, which is the bay area, they are part of the top 10. If you want to know which ones are lower than expected. These are Philadelphia, Indianapolis, Cleveland, Pittsburgh, Virginia Beach, Saint Louis Missouri, Chicago, Birmingham, Hartford, and Kansas City Missouri.

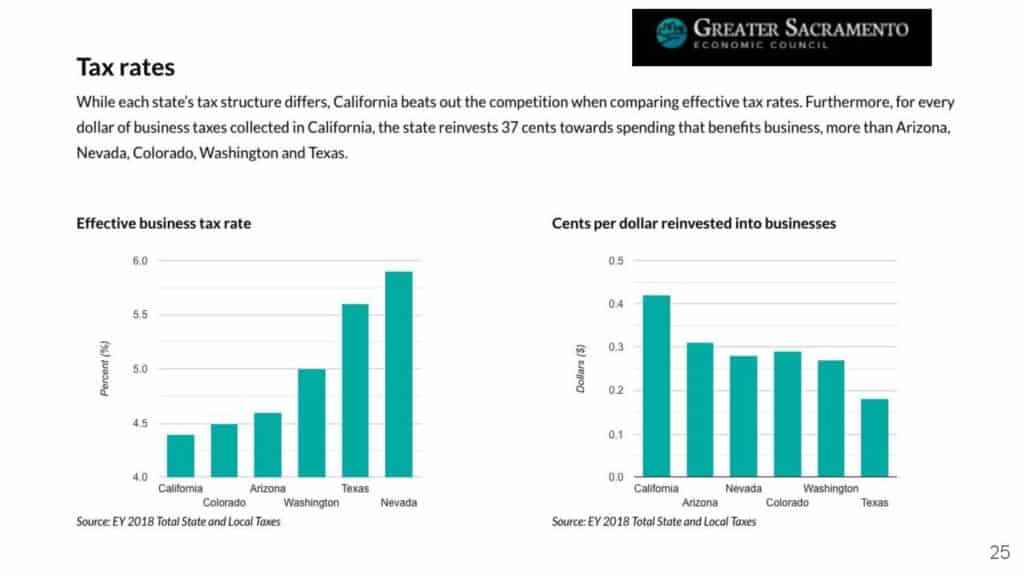

Also, next week, we are going to be doing an event with a few commercial real estate and residential real estate professionals, and one of which, is actually from the Greater Sacramento Economic Council. As I was talking to him, I found their website and then I saw this chart and I was pretty surprised because it is saying that the effective business tax rate in California is actually lower than Colorado, Arizona, Washington, Texas, and Nevada and I just could not believe it because we are so known for high tax rate.

Also, they talked about how many cents per dollar we invested into businesses and California is actually doing better, higher than Arizona, Nevada, Colorado, Washington, and Texas.

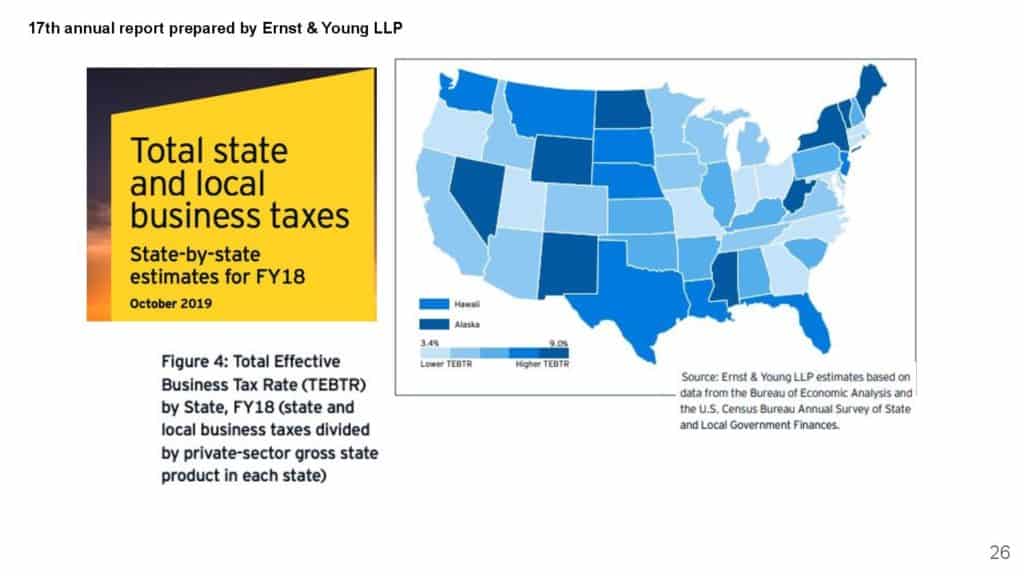

This is a report by Ernest and Young in 2018. At that time, they were looking at why are people doing business in California. I know there are a lot more regulations and a lot of people are frustrated, but then I think at the end of the day businesses need to think about where can they make the most money. This is really interesting. Although I have to say that the business tax rate probably does not apply to small businesses. If you are in small businesses, your tax is probably higher, but then it really works for the larger corporations who are staying here and which will be the ones that support the employment in our area.

Another chart that I found from Ernst and Young reports, back in October 2019, is looking at the total effective business tax rate by state. The lighter the color, the better the lower the effective business tax rate is. I was totally expecting that California is going to be dark blue, but it is not. They are not the lowest, but then they are relatively low. So, this is also another reason why we do not think that companies will leave California even though it does seem like it is really attractive to go to Texas which has a more effective business tax rate. We have to also think about other states. Sometimes they do not have an income tax rate, let us say; but then they do have a much, much higher property tax rate. For example, in California, we are right around low 1%, but in Texas, in some areas is as high as three-point something percent for property tax rate. So, they do makeup in certain areas. This is one of the reasons why I thought it is really interesting to show you and I just found on these reports as well. I just thought it would be great to share.

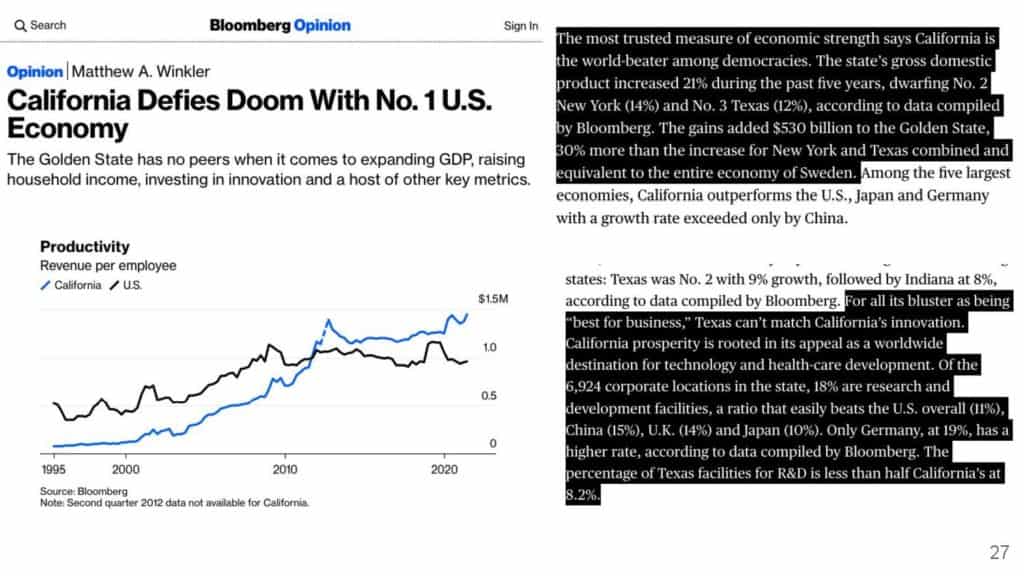

Also, another article I found by Matthew Winkler. He also talked about why is it that everybody talks about California has such a high tax rate, there are so many regulations, people keep saying that they want to move out, but then what is going on? How come California is still so strong? It says like “the most trusted measure of economic strength says California is the world-beater among democracies. The state’s gross domestic product increased 21% during the past five years, dwarfing No. 2 New York (14%) and No. 3 Texas at (12%). The gains added $530 billion to the Golden State and 30% more than the increase for New York and Texas combined and equivalent to the entire economy of Sweden.” This is how strong California is. Also, it says, “For all its bluster as “being best for business,” Texas cannot match California’s innovation. California’s prosperity is rooted in its appeal as a worldwide destination for technology and healthcare development. Of the 6,924 corporate locations in the state, 18% of research and development facilities, a ratio that easily beats the U.S. overall (11%), China (15%), the U.K. (14%), and Japan (10%). Only Germany, at 19%, has a high rate, according to data compiled by Bloomberg. The percentage of Texas facilities for R&D is less than half California’s at 8.2%.” I thought these are really, really interesting articles and how they break it down, why California is so strong.

Of course, when you are a company, you also think about what kind of revenue you can get per employee. In the line for California, you can check that the revenue per employee is much higher than the national average.

I hope you find this interesting too because I was always wondering whether companies are going to leave California.

With that said, should you buy more investment properties then or just real estate in general? I want to share a little bit with you before we go because today we are talking about cost segregation. Cost segregation applies to your investment property. Let us think about whether it is time for you to go into investment properties.

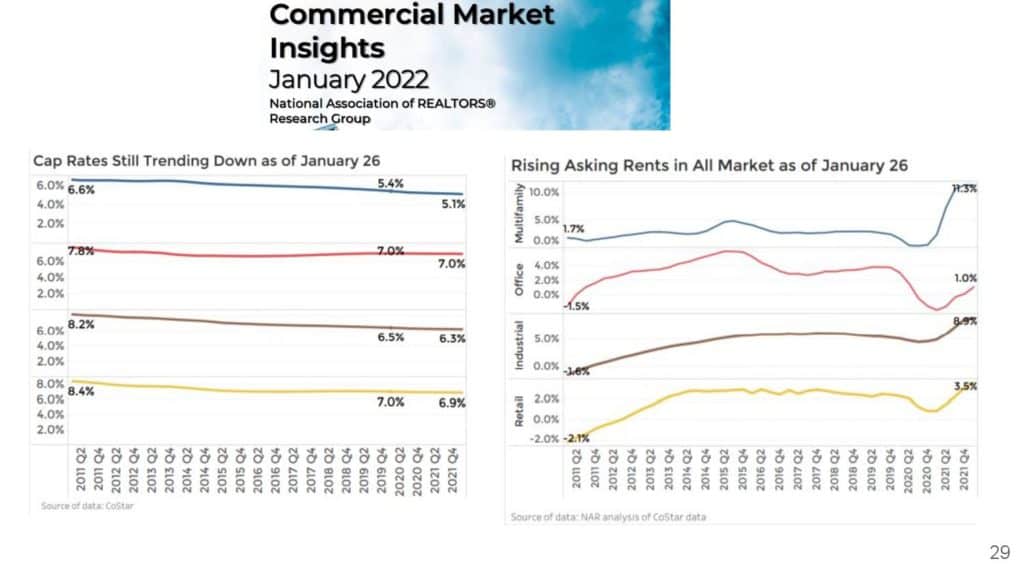

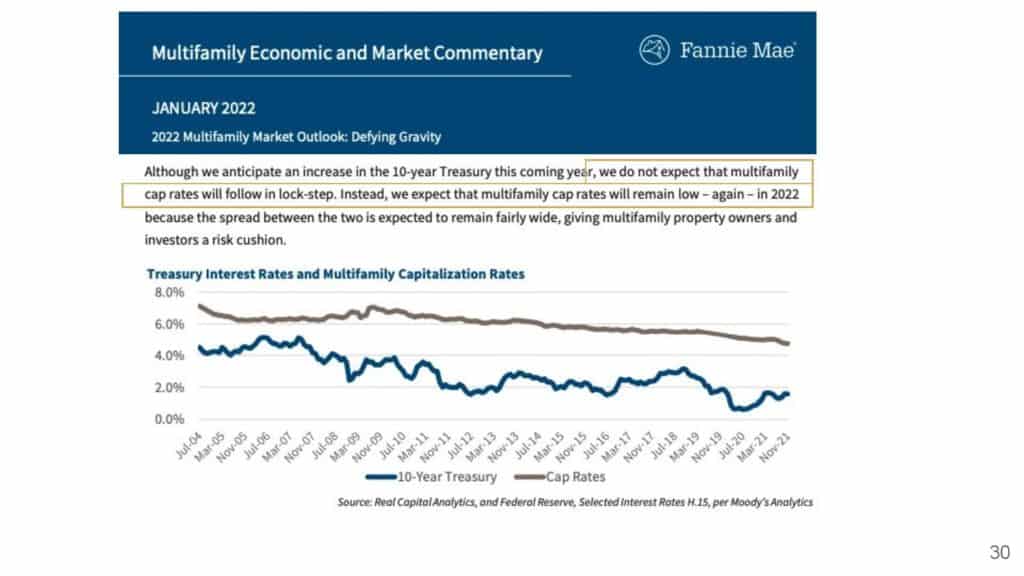

One thing is that when we buy an investment property, we do look at the cap rate. The cap rate is still trending down despite the Fed rate is going to go up. The rents are also continuing to go up and it is actually going up pretty high and especially for multi-family, it went up 11.3%.

Also, with the treasury interest rates and multi-family cap rate, you can check that the cap rate is still maintained pretty low. They do not think that just because the 10-year treasury yield is going to go up that is going to affect the cap rate. So, in the future, the cap rate is still going to maintain pretty low.

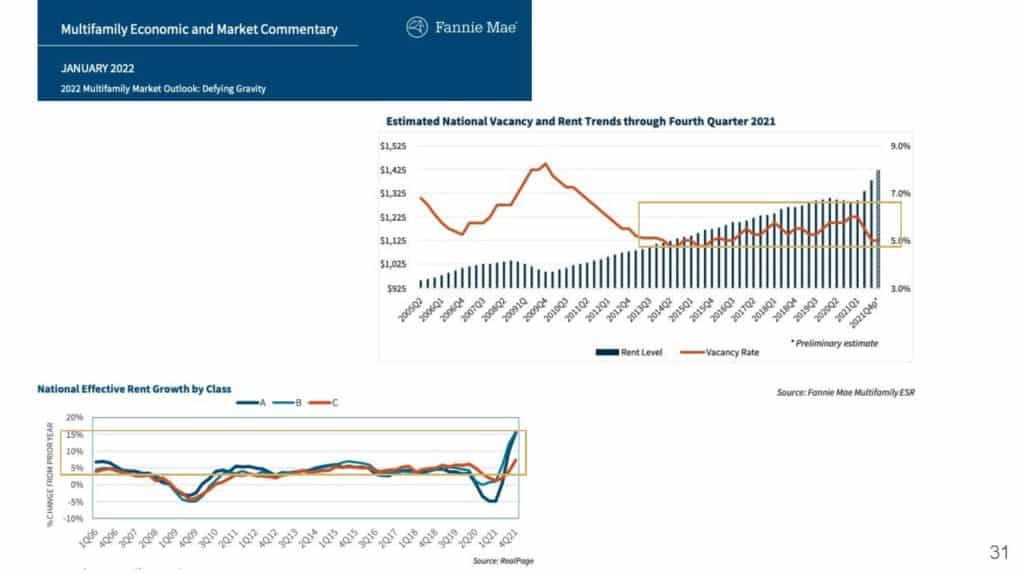

By looking at the vacancy line, we can see that the vacancy has also come down quite a bit while the rent has gone up quite a bit also.

If you are deciding between class A, class B, class C properties, the national effective rent curve for class A and class B properties definitely had gone up a lot more compared to class C properties, especially because of the pandemic. Unfortunately, the blue-collar or the lower-income population got affected the most during this pandemic.

The conclusion here, after looking at all that, is that the businesses most likely in the Bay Area are going to stay because California is still a very ideal place for them to make money. If they want to have business here, obviously they have to think about making money. The supply level definitely going to increase modestly. Mortgage rates will increase in 2022. Rental rates will still remain really strong and go up. The Cap rate will remain low. More importantly, there is also a lot of tax benefits in 2022 that we are going to go into a little bit regarding that. Housing prices will increase gradually, and also we are probably going to start seeing listings that will stay on the market longer. I think that around June 2022, that is when we start seeing that the market is going to go slow down.

For this month’s Bay Area Housing Market Townhall, we invited cost segregation expert Geraldine Serrano to share how to use this powerful tax planning strategy to pay little to no taxes on real estate investments, watch the video here! As always, please don’t hesitate to reach out with any real estate questions or needs, we are more than happy to schedule a call with you.

Stay up to date on the latest real estate trends.

A Bay Area Realtor's approach to schools, neighborhoods, and long-term value for families making a move

Part 1 of HAYLEN's series on the 2026 CCIM Spring Forum in Philadelphia

You’ve got questions and we can’t wait to answer them.