2022 Review and 2023 Outlook on Bay Area Residential Housing Market

Welcome to our first Bay Area Housing Market Town Hall Webinar in 2023. We’ve been hearing from a lot of our clients that there isn’t enough inventory on the market and this is why they have paused their home buying journey. What has been going on in the market? What's the outlook for 2023? Join us for this month's Bay Area Housing Market Updates! You can find the video recording here on our YouTube Channel.

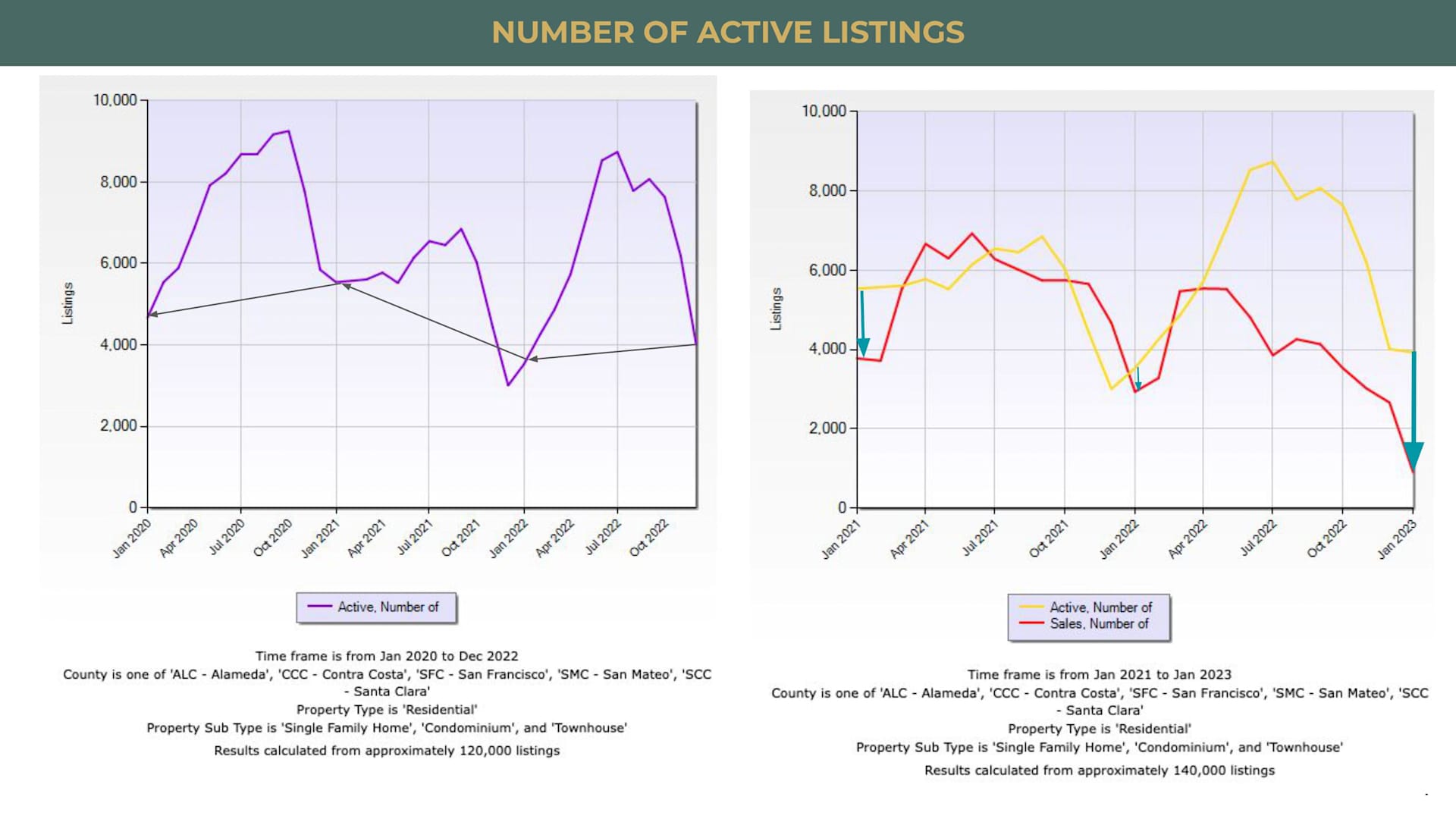

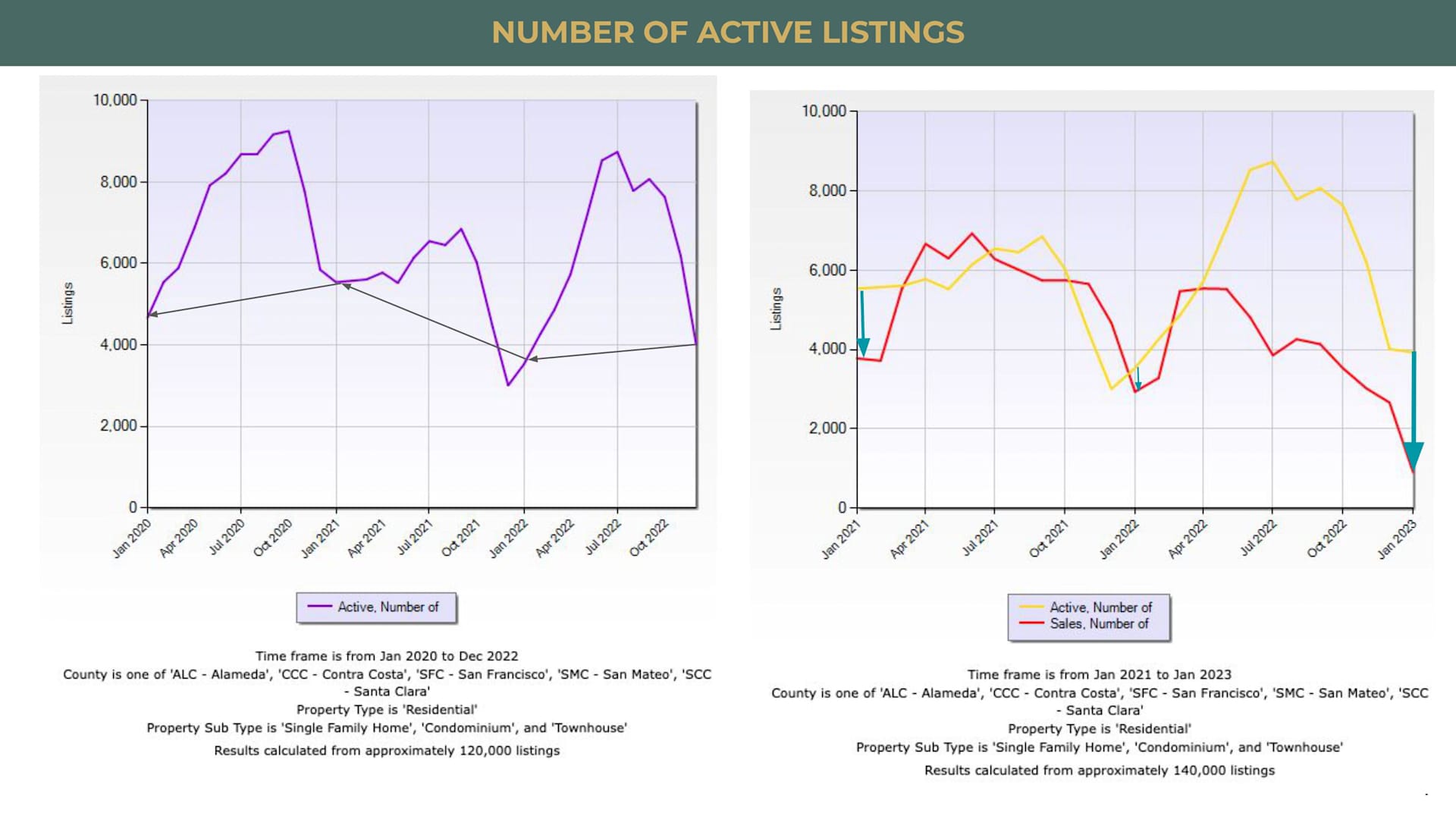

Compared to 2021, we had a lot more listings compared to 2022. Hence, if you remember, in the first four months of 2022, the price had gone up so quickly. In 2020, in January, before COVID started or before the whole market shutdown, we had a little bit less inventory. If you compare 2020 and 2022, we are less than 2020 but we are not that much less. But then, the huge change is really between 2021 and 2022.

If you're looking at it in terms of the number of sales, we have lower inventory but then the number of sales, this is where you see this huge drop. This is the reason why even though we don't have a lot of inventory which should drive up the price, but we also do not have a huge demand. A lot of buyers are really sitting on the sideline, kind of just waiting and to see how the market is doing. So, that is why you see this huge drop in the number of sales.

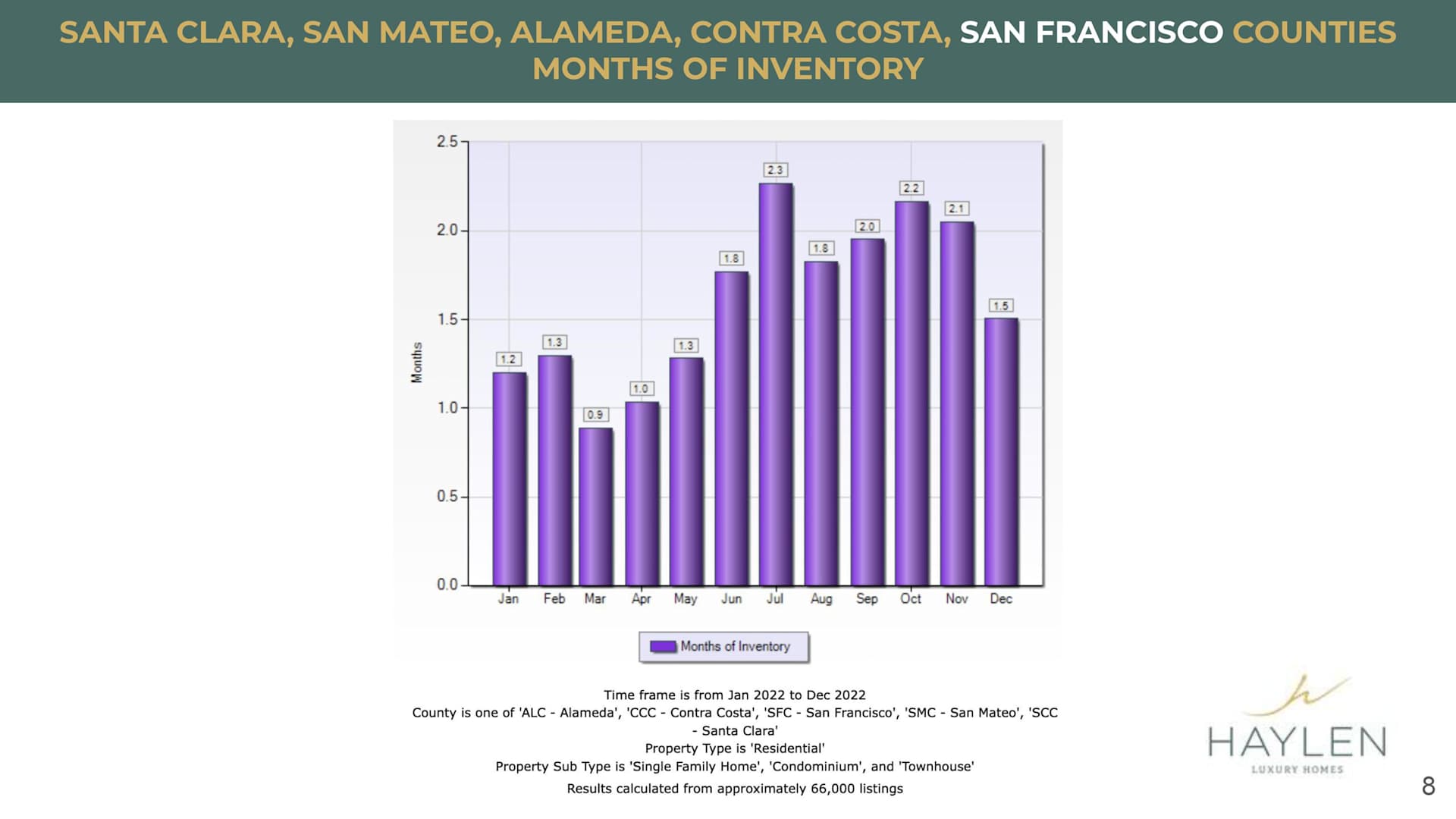

Let's look at the Months of Inventory. Interestingly, we went from a very tight market to a, relatively or I would say that it's not as tight anymore, like up to 2.3 months of inventory, but we have been sharing with you guys that a normal market actually is between 4 to 6 months of inventory. So, relatively speaking, we are still in a little bit of tight inventory if we compare it to a normal market, but in December, we went down to 1.5 months because of that tight inventory.

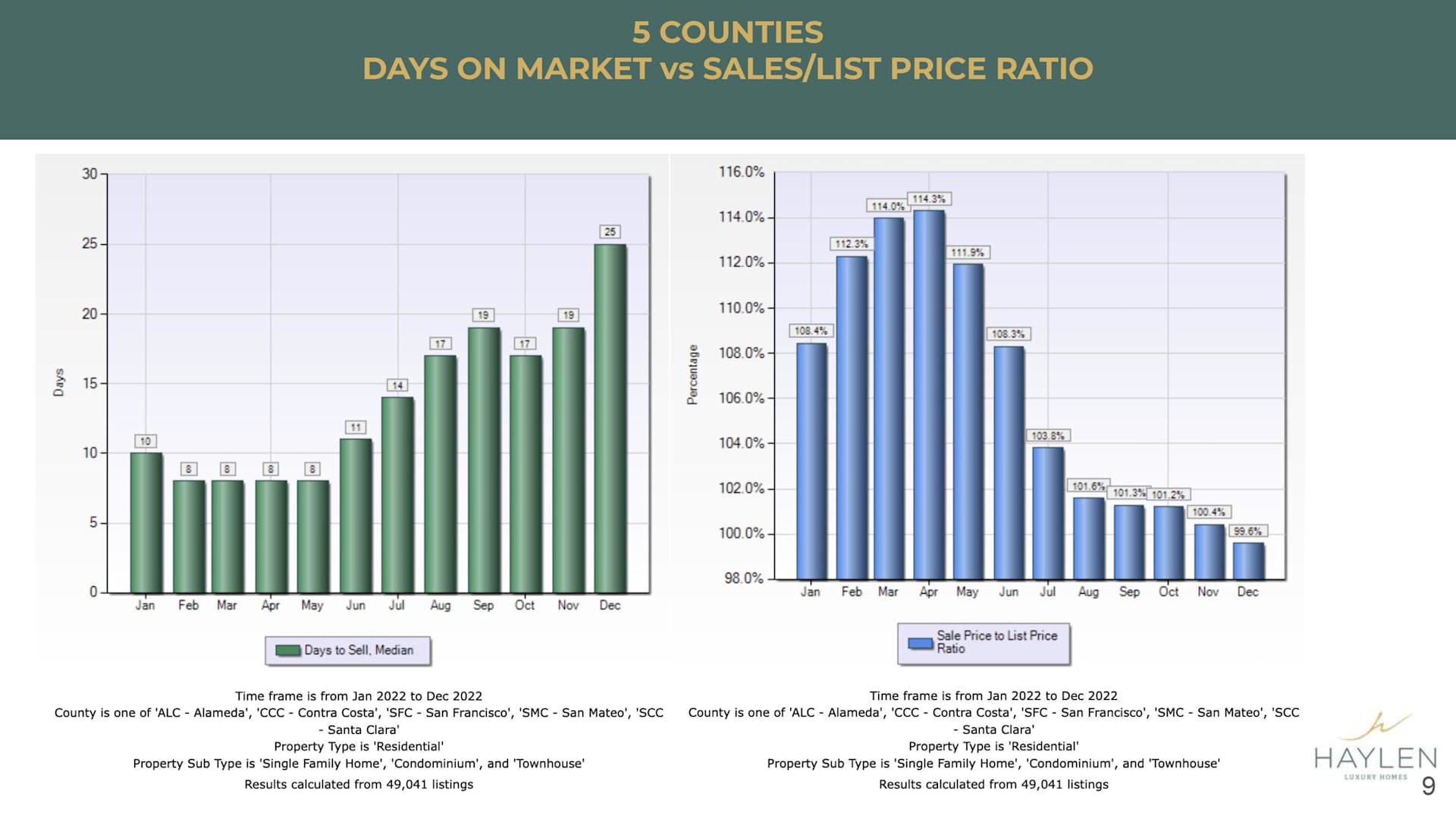

In terms of the median number of days to sell, as you see in December, we went from the beginning of the year last year less than 2 weeks, almost pretty much a week, to sell all the way to 25 days. This December, I have to say from personal experience, it's like the first time in years that we can actually take a break and vacation without really working.

I'm just sharing this with you to show you how slow the market has been. It is really not normal for us for the past 10 years that we actually can take a break without really working. Typically, we are still working during the winter break despite it being a slower market.

In terms of how competitive it is, we finally went below 100% of the list price. People are really offering below the asking price nowadays. Even though in the past few months, it has been slower, but you see that the median sales price to the list price is still over 100%. But we finally went down to under 100% in December because the market was just so slow at the time.

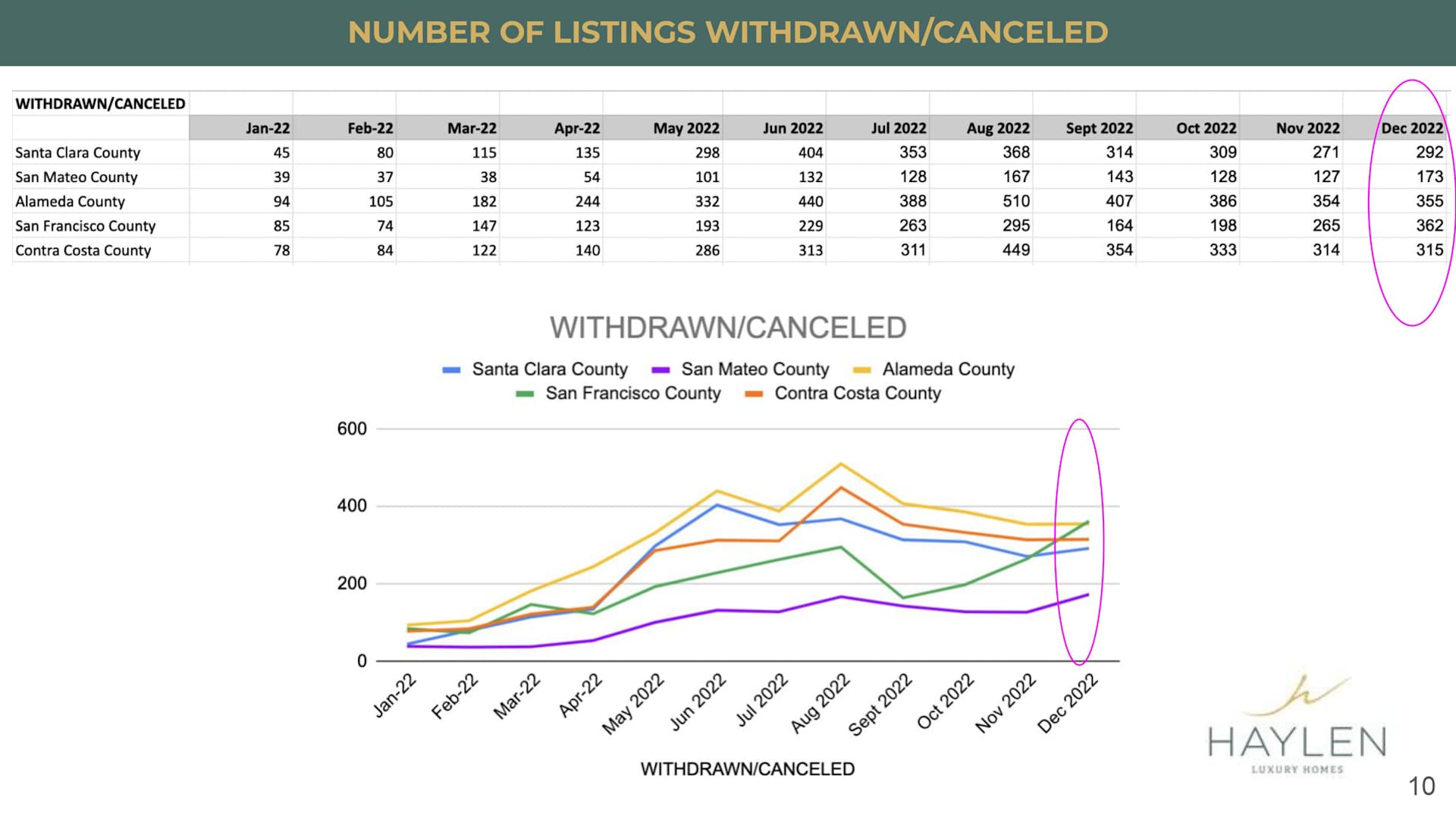

Now, we look at how many listings have been withdrawn and canceled and you'll see that the number of listings withdrawn peaked at around June and July and August and then it just started to come down but then in December, we're starting to see that people kind of pulling their listings off the market again because as you know that if they cannot sell it by December, they would probably decide to just pull it off the market until January. So, we should start seeing a little bit more inventory in January or actually I would say February because we have been having such rainy days and then yesterday and today and finally, I was like wow! I feel like I missed the Sun. We haven't seen the Sun for so long. So, for the month of January, it has been a bit slow as well because of the rain.

In terms of list price decreased, you see that in July and August of last year, there is a huge jump in how many listings have dropped their prices. This is the time when a lot of sellers realize that the market is changing. Now, we have to start dropping the price, but we started seeing much less sellers are dropping the price. Now, they have a completely different listing strategy, meaning that they might try to list a little bit lower but then a more realistic number instead of before they still trying to fetch for that April and May numbers but they're not able to get it. So, they would lower their asking price. But right now, we start seeing a lot of sellers are much more realistic in terms of their asking price.

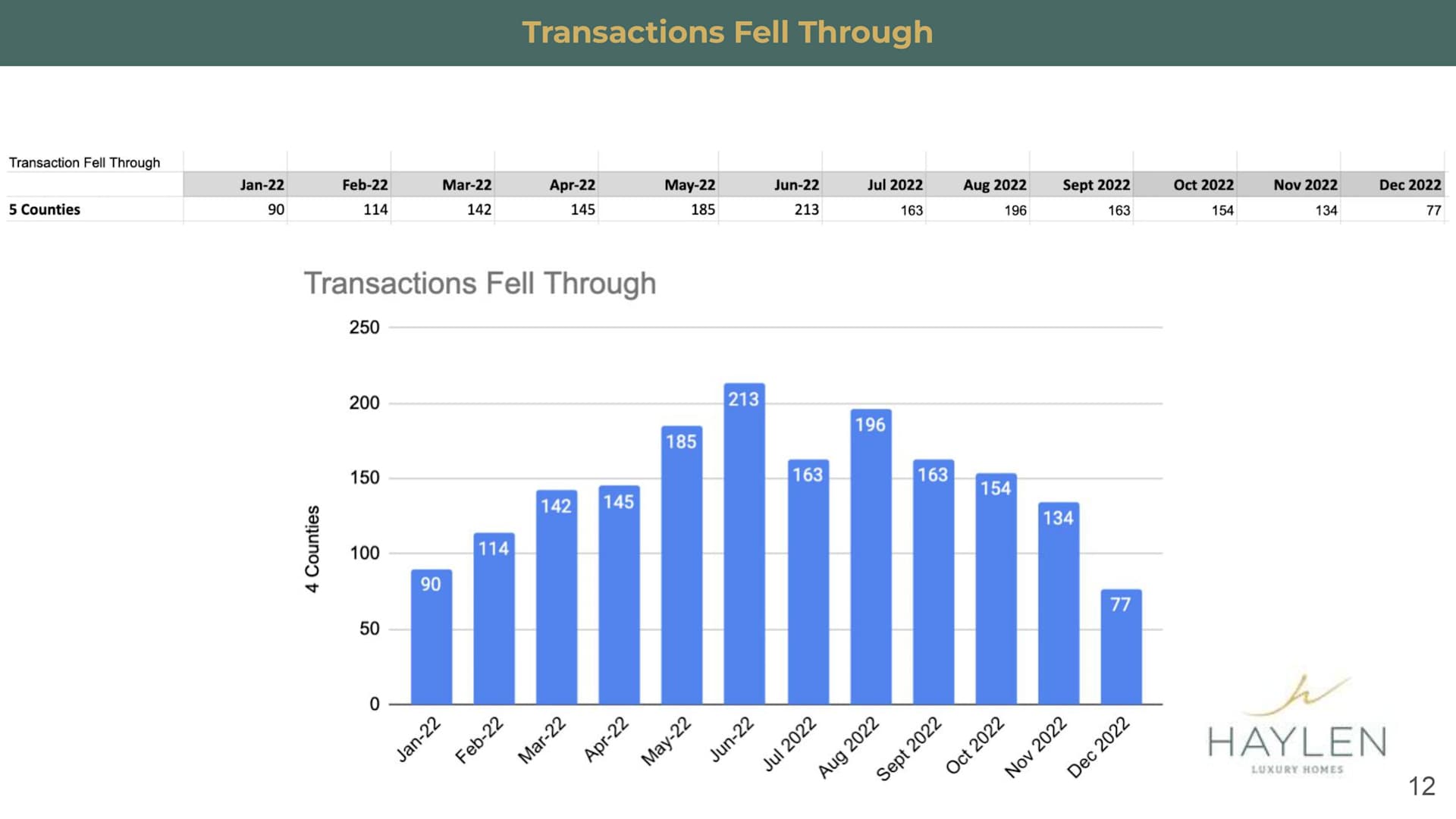

How many transactions fell through? We only have 77 compared to all three digits most of the year. So, only 77 transactions fell through. I would say that this number is not real because everything has been going so well. It is more because we just have so much less transaction in December and that's why we have less transactions that fell through. We just really don't see that many transactions fall through out of all the 5 counties.

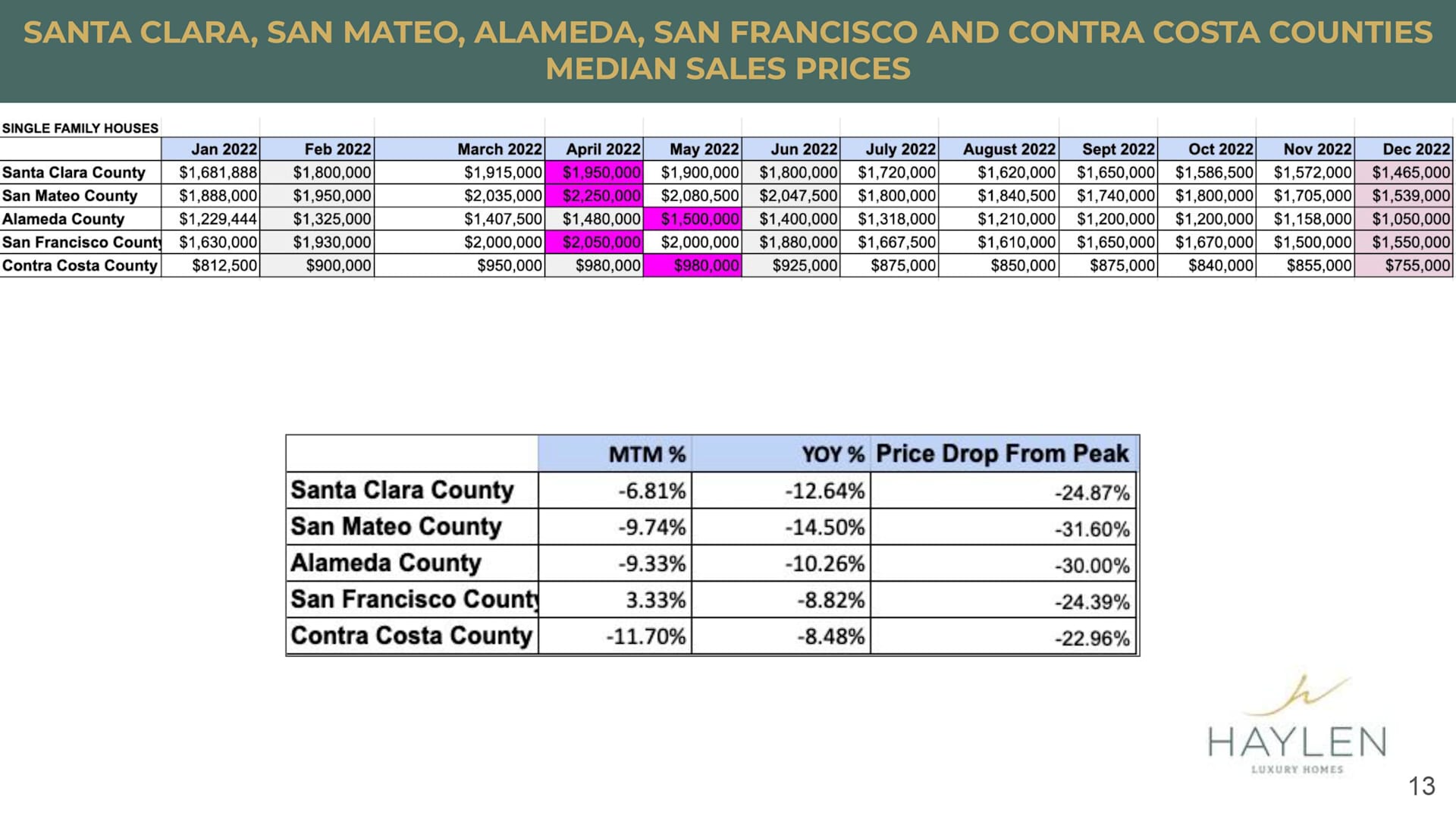

In terms of the pricing, what happened? We have shown you December that the peak prices were in around April and May.

For Santa Clara County, it peaked in April at 1.95 and in December, the median sales price has gone down to 1.465. For San Mateo County, it peaked in April for 2.25 and it came down to 1.539. In Alameda County, they peaked in May for $1.5 million and in December, it went down to 1.05. Then, San Francisco County, it went up to 2.05 in April and came down to $1.55 million in December. For Contra Costa County, it peaked in May at 980,000 and also the pricing at December of 2022 had to come down to 755,000.

What does that mean? So, if you look at Santa Clara County a month-to-month percentage, it dropped about 6.81% and if you look at year-over-year, it is about 12.64%, but if you look at from the peak, which was in April, year-over-year, we look at the last year's number but the price from the peak that's how much it has gone up last year, in the first four months, it dropped close to 25%.

As for San Mateo County, month-over-month, the pricing had dropped about 9.74% from November and then year-over-year, it dropped about 14.5% and the price dropped from a peak, it was 31.6%.

Alameda County, it dropped about 9.33% from last month and year-over-year, it dropped about 10.26% and the price dropped from the peak was about 30% which was in May of 2022.

San Francisco County, it actually went up slightly for 3.3% compared to November. Compared to last year, it dropped about 8.82% and from the peak, it dropped about 24.39%.

Lastly, Contra Costa County, it dropped 11.7% from last month; from last year, it dropped about 8.5% and then it dropped about 23% from May of 2022. Quite significant when you look at how much it has gone up and then compared to the peak, but then if you look at a one-year number, it did not drop as much. It's to show you how much it has gone up in just the first four months of 2022.

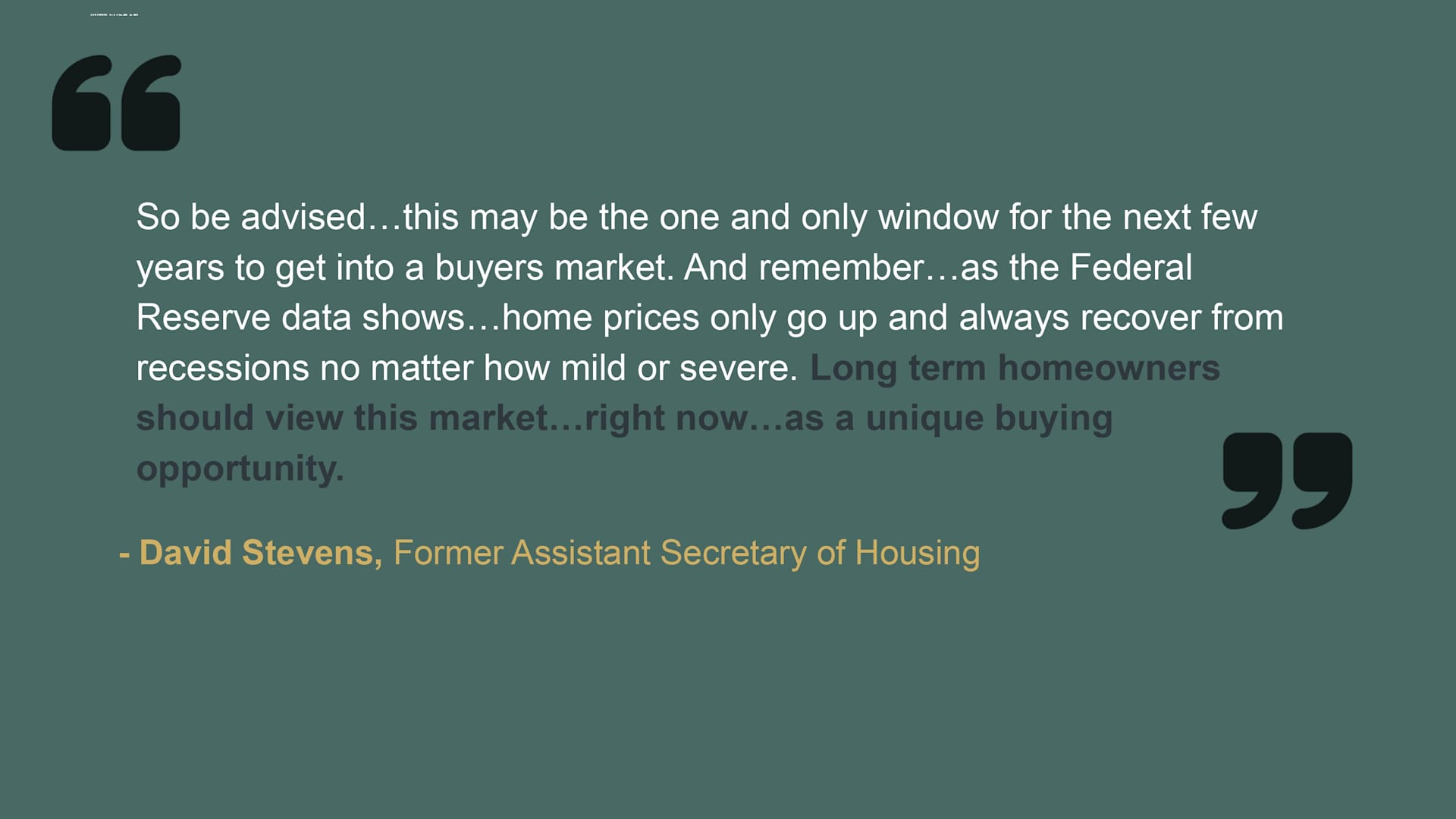

David Stevens who is a Former Assistant Secretary of Housing said, “So be advised… this may be the one and only window for the next few years to get into a buyers market. And remember… as the Federal Reserve data shows… home prices only go up and always recover from recessions no matter how mild or severe. Long-term homeowners should view this market… right now… as a unique buying opportunity.”

Usually, I would question a little bit about what they say but I honestly feel like this time of the year especially, right now. December, we had already told a lot of our buyers to be sure to come and don't stop looking if you're serious about buying because in December we just had such a slow market. We did not have a lot of inventory, the only thing is hard was to find that perfect home. But if you do find that perfect home, it was actually a really good time to buy because you get to negotiate.

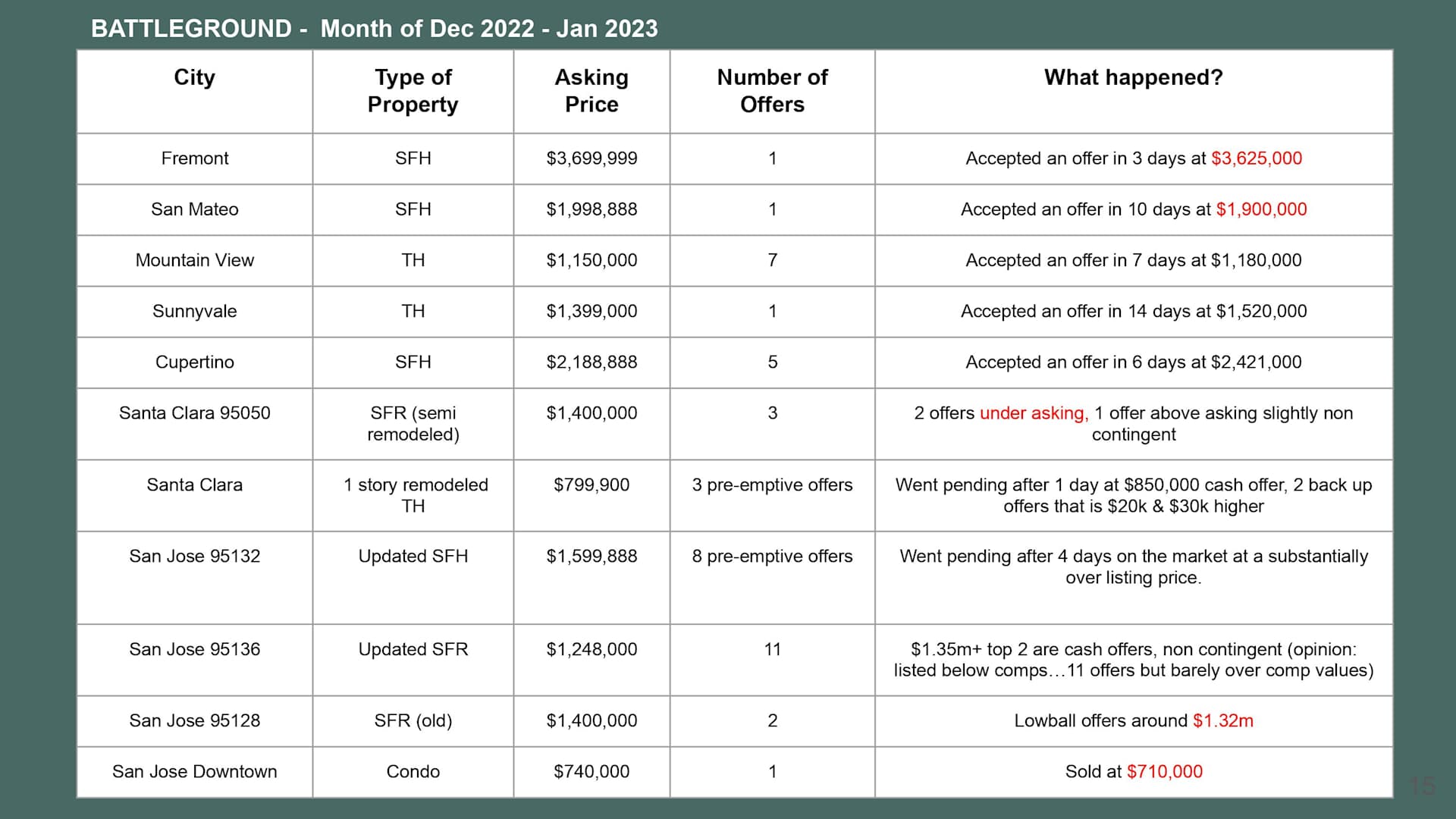

January, right now, we still see a relatively slow Market but I'm going to show you in a little bit regarding how the offers happen in different cities.

This is what has been going on, and there are a lot of properties that are not receiving any offers but then if the properties are in a really good location, it's like remodeled and it doesn't really have any defects per se. This means that it doesn't have, let's say, a weird floor plan and the location is not good because it is close to the noise and stuff like that, it typically is still getting quite a bit of interest. For example, in Mountain View, this townhouse is asking for 1.15. They did receive 7 offers and went up slightly above the asking price, but in Fremont and San Mateo, these single-family homes, it wasn't too bad. It was on the market still for a short period of time, but they only got one offer and slightly below their asking price.

Cupertino, the asking price is close to 2.2. They still received 5 offers within 6 days and it went above the asking price by about $200,000.

Here is another single family. It is not as remodeled. This one only has one bathroom, so already have a smaller buyer pull and asking price of 1.4, but they received two offers initially but they both under asking and then they just needed that one person to offer above just slightly above 1.4 with no contingency. We still see no contingency offer in this market, believe it or not.

Here are some interesting things. Santa Clara, this is a one-story model townhouse and if you're looking at a townhouse, you'll know how hard it is to find a one-story townhouse. Because most of the time, it is two stories or even three stories. For this one, asking price is 800,000. They received 3 preemptive offers and one pending, just one day. They got a cash offer and they actually accepted the cash offer over the financed offer even though the finance offer were higher. We see this over and over again in this market that a lot of times sellers would much rather accept a cash offer even though the offer might be a lower price, just because they don't really want to risk the financing right now. If the interest rate just shoots up all of a sudden, they're afraid that the buyer may not qualify. So, that is why a lot of times we do see this more often than before when they would accept a cash offer that is lower than the other offers.

Same thing, this one is remodeled and updated a single family, almost 1.6, got 8 preemptive offers. When we say preemptive offer, it means that it's not even a deadline yet they just submitted an offer before the deadline. It was only 4 days on the market, and it really went way above asking price. We don't know exactly what is the accepted price, but it's just seeing that there are 8 offers within 4 days that is something.

But on the other hand, you'll see that some other homes are not as updated. They only get 2 offers and they're all lowball. So, they went below asking price.

Same thing here, San Jose condo, $140,000 asking but they only got one offer. So, they accepted an offer that was below asking price.

Definitely, work with your agents to make sure they understand or see how many offers they are. Don't just go in and then make an offer above and beyond. There are some situations and some properties, but they do still receive multiple offers. Even multiple offers don't mean that they always way over asking because they only need one buyer who is willing to pay above and beyond right. These two offers are both below asking, and I would say that the third offer probably could have just made an offer right at asking, and still can get it accepted.

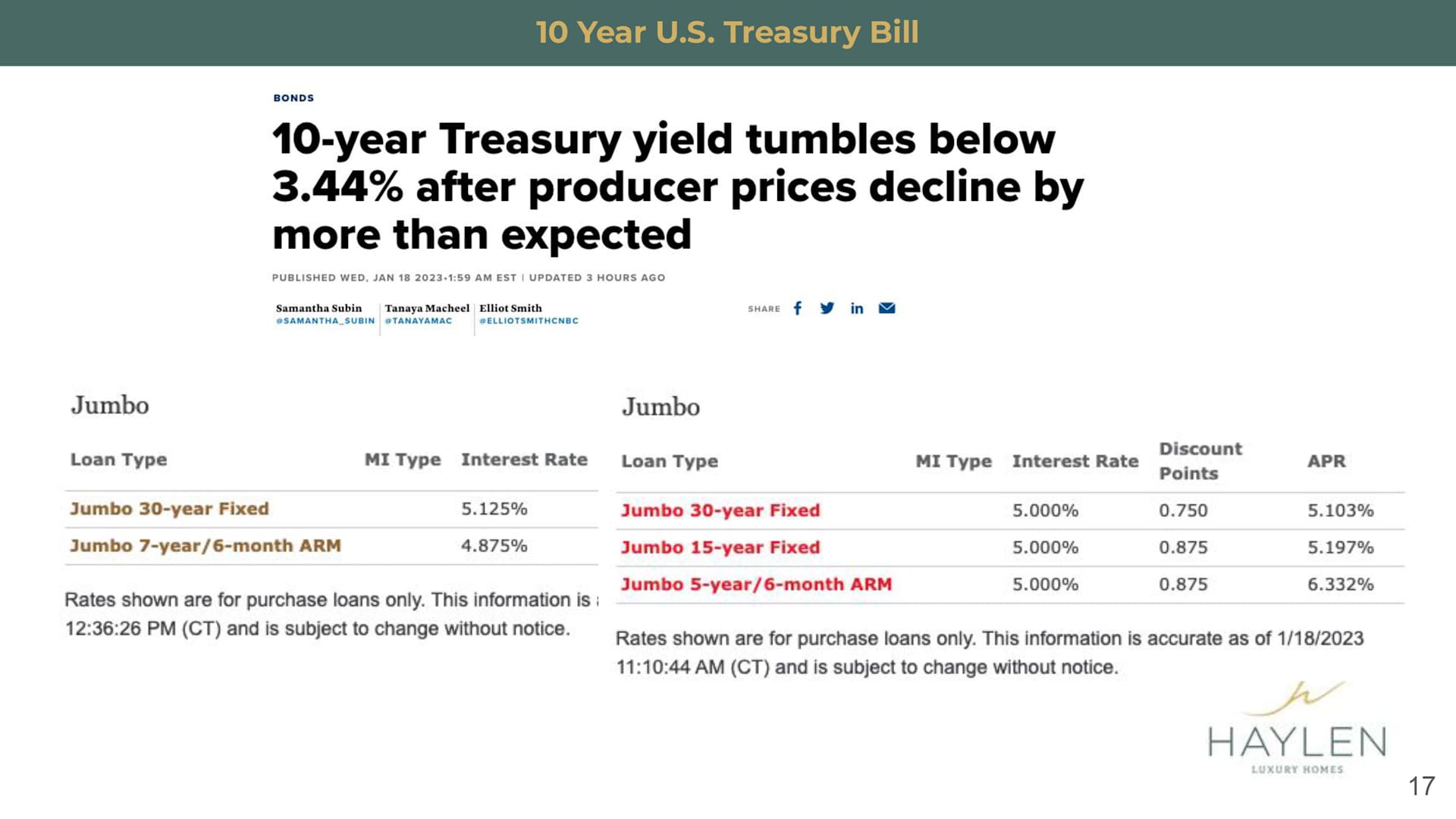

Let's look at the mortgage rates projections now. If you guys paid attention, the 10-year Treasure yield actually had come down a little bit and you know 10-year Treasury yield kind of correlates with the 30-years mortgage rates. As an example, on January 13th, you'll see that Jumbo 30-year fixed is about 5.12%, and this is provided by Wells Fargo by the way. Today, the 30-year Fixed Jumbo has come down to 5%.

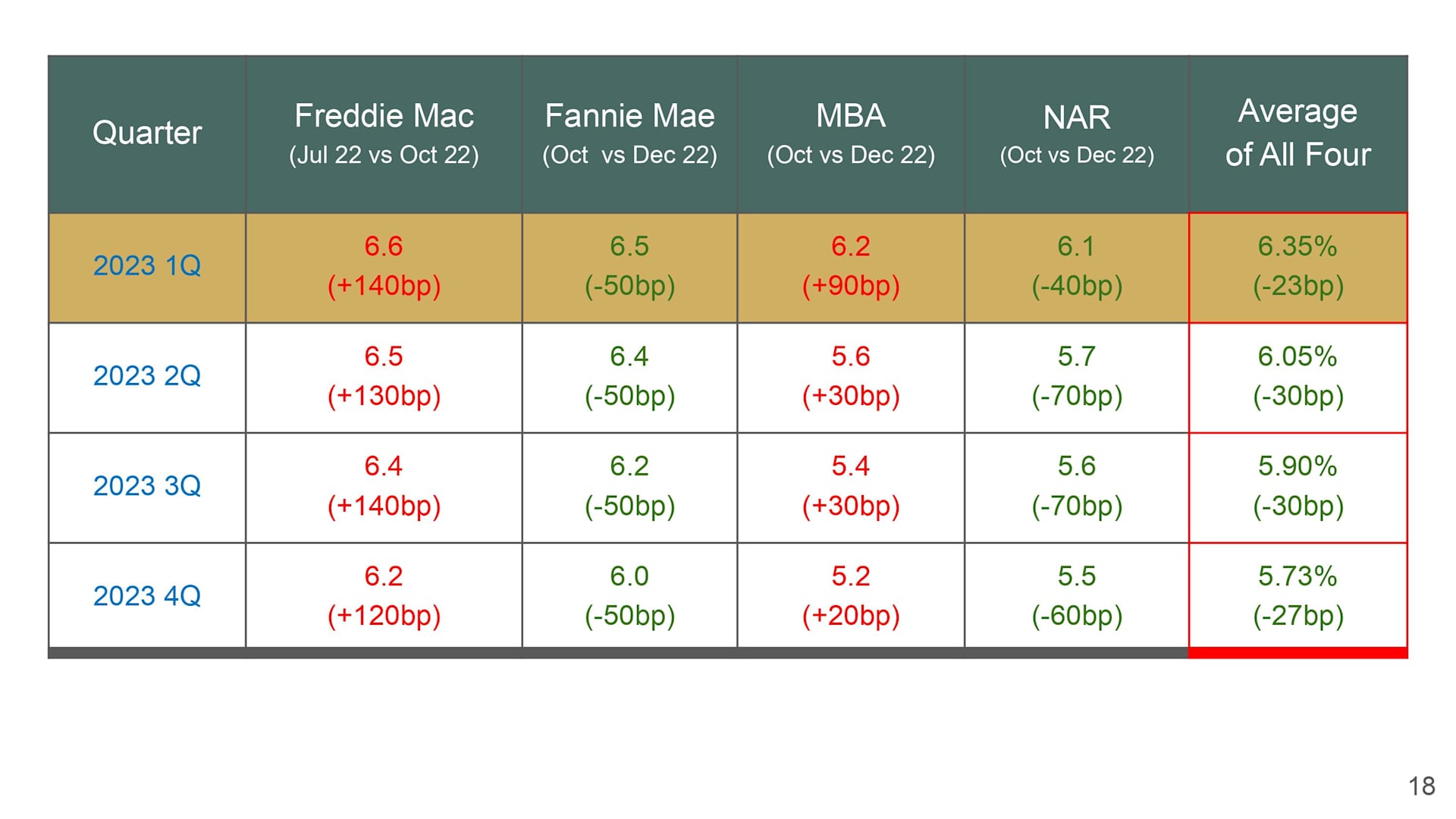

If we look at all these agencies Freddie Mac, Fannie Mae, Mortgage Bankers Association, and National Association Realtors - Very interesting! As you see, Freddie Mac, they haven't updated their numbers, so they're still the same as last time I reported to you that you should have come out with their new numbers end of February.

Fannie Mae, they have adjusted its numbers quite drastically. Last month, when I reported too, it was way up; it was over 7%, but now, they came back down with their projections down to 6.5% for the first quarter of 2023; 6.44% 2Q; 6.2% for 3Q and 6% for 4Q. They are projecting the mortgage rate starting to come down.

For Mortgage Bankers Association is the same thing for the December number. This is the same number that I showed you last month. They are projecting that it peaked around the first quarter of 2023, and it's going to start coming down.

It is the same for National Association Realtors. They have adjusted their projections, so they are projecting that the mortgage rate also peaked in 1Q 2023 and started to come down.

When you look at these numbers start climbing ahead right because once people start seeing the mortgage rate starting to come down, we're probably going to see even an increase in demand as well.

A lot of times now a lot of economists starting to say that this recession is going to be mild. "The rate hikes have begun to quell U.S. inflation." They are starting to see that U.S. inflation is starting to come down. At least, it is towards the right direction, not where they want it to be yet, but then it is towards the right direction.

Over here though it does say that "they don't expect the Fed to raise rates as high as Masters prefers, but future prices suggest that the market thinks the central bank will implement two more quarter-point hikes and then stop."

Linda Hersey, Director, News Reporting for Real Estate News, says, “temporary rate buydowns are a hot trend for mortgages as borrowers face high costs for home loans. Some buyers exploring alternatives to traditional mortgages in the period of rising interest rates that are expected to continue into 2023… Buydowns… are a less costly alternative to traditional fixed-rate mortgages.”

We actually had this episode in December, so be sure to go back and review it. This is where we invited Sean Crowley to come and talk about how you use this buydown to negotiate with the seller and also help your buyers to get a lower mortgage payment.

Thank you for reading! We also invited Daniel Bornstein, a well-known local tenant-landlord attorney, to discuss 2023 Legal Landscape for Residential Landlords, check out the video recording here. As usual, we are here for all your real estate needs, please feel free to reach out with any questions.

Stay up to date on the latest real estate trends.

Part 1 of HAYLEN's series on the 2026 CCIM Spring Forum in Philadelphia

You’ve got questions and we can’t wait to answer them.