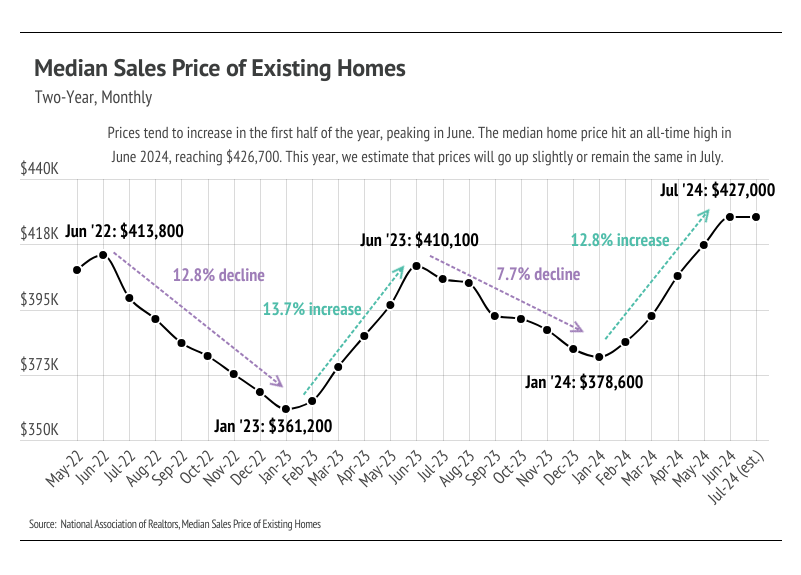

In June, prices rose for the fifth month in a row, reaching all-time highs. Typically, home prices begin to fall in July, but this year may be different. Currently, we estimate data to show that the national median home price rose very slightly in July. We are confident, at least, that prices have not fallen 5% from June to July, which means that July was the 13th consecutive month of year-over-year price growth. Despite the seasonal price dip, which is surely coming in the second half of the year, year-over-year price growth will almost certainly continue for months to come.

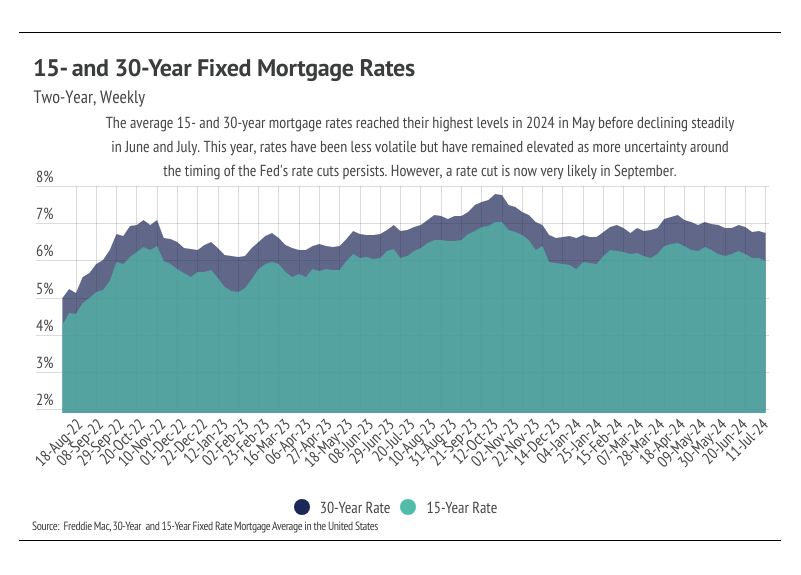

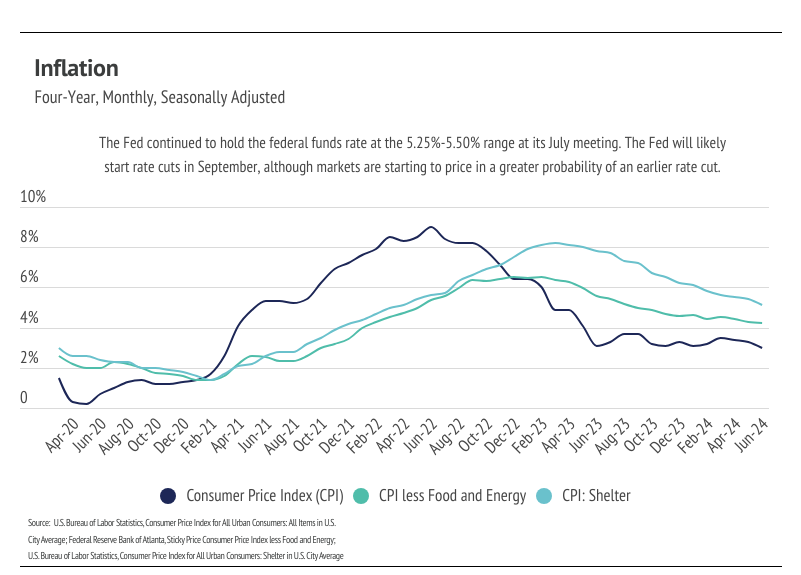

So why won’t prices see a major shift downward in the second half of the year? Seasonal trends already dictate that prices will decline starting around now. Combine that with high mortgage rates, slowing sales, and the highest inventory in four years, and it seems like we have the perfect recipe for prices to fall significantly. While home prices tend to increase over time, the pandemic buying boom set the stage for prices to rise more quickly than expected, and to stay high. In a funny way, higher interest rates have been incentivizing higher prices due to the cost of selling and buying at the same time. From June 2019 to March 2022, the average 30-year mortgage rate was less than 4%, and the averages for all of 2020 and 2021 were 3.11% and 2.95%, respectively. All that to say, those buyers who purchased their homes through financing, as most buyers do, in 2020 or 2021, and who plan to buy their next homes through financing at a much higher rate — they need to sell their current homes for much higher to combat the cost of financing new ones.

To further the point, the cost of financing the median home in June 2024 has increased 83% compared to June 2021, even though the sticker price of the median home is only up 16%. However, let’s say you bought the median home in June 2021 with 20% down, and then in June 2024, both sold your old median price home and bought the June 2024 median price home, your mortgage would only go up 55% rather than 83% because of the $60,000 price appreciation, which would bring you to ~30% equity in the new home. To be clear, 55% is still a lot, but it’s better than 83%.

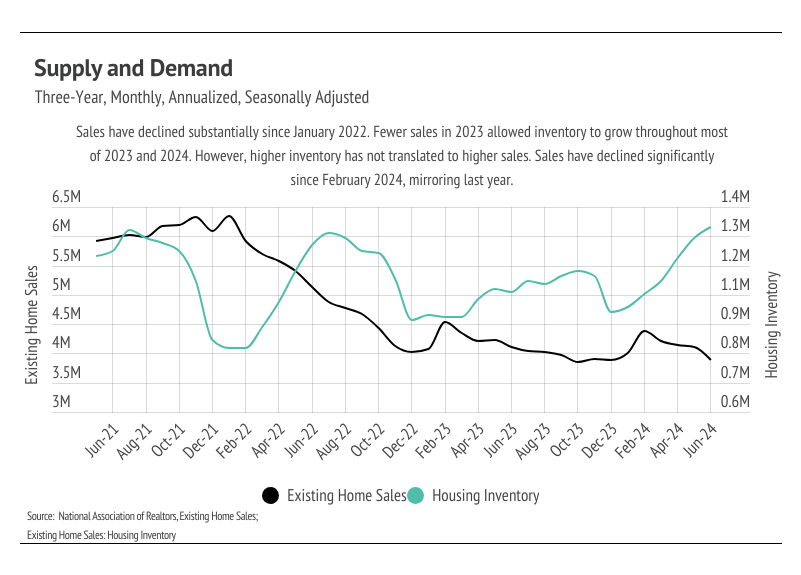

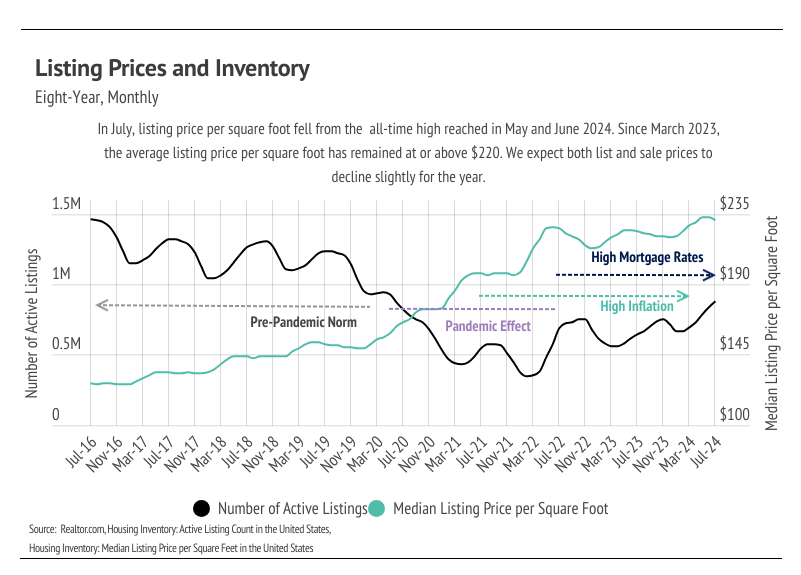

Overall, inventory growth is great news for the undersupplied U.S. housing market. According to data from realtor.com, inventory reached its highest level since June 2020. The increasing inventory level should cause rising home prices to slow. In the pre-pandemic seasonal trends, sales, new listings, inventory, and price would roughly all rise in the first half of the year and decline in the second half of the year. Sales and new listings have been far lower than usual since mortgage rates started climbing, which is to be expected. Because we don’t anticipate sales to pick up until the spring of 2025, inventory could easily continue to grow in the second half of the year. Fed rate cuts will come right when the market really starts to slow down, so they probably won’t drive the market into a buying frenzy in the fourth quarter.

Different regions and individual houses vary from the broad national trends, so we’ve included a Local Lowdown below to provide you with in-depth coverage for your area. As always, we will continue to monitor the housing and economic markets to best guide you in buying or selling your home.

Big Story Data

As your local real estate experts, we feel it’s our duty to give you all the information you need to better understand our local real estate market. Whether you’re buying or selling, we want to make sure you have the best, most pertinent information. Please don’t hesitate to reach out to us with any questions or concerns. We’re here to support you.