December Newsletter – Greater Bay Area Housing Market Updates

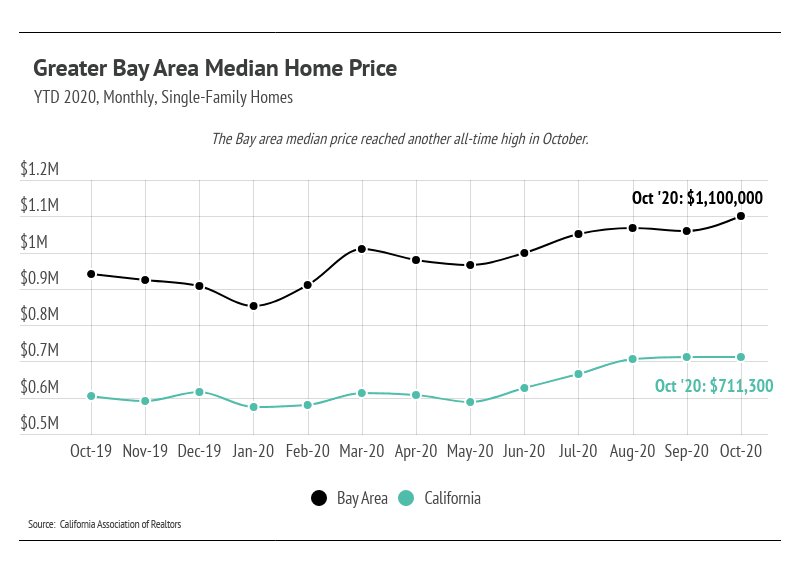

Single-family homes had large month-over-month and year-over-year gains, bringing median prices to another record high.

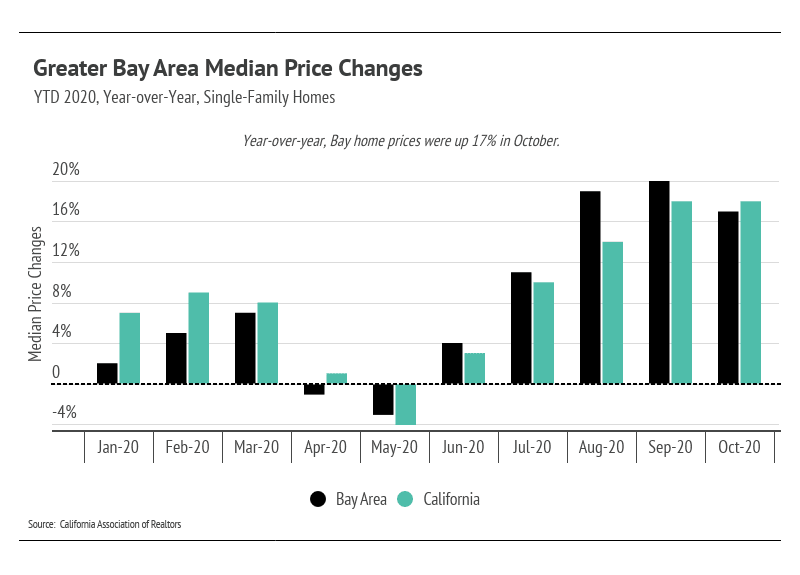

Year-over-year, median single-family home prices were up 17% in the Greater Bay Area.

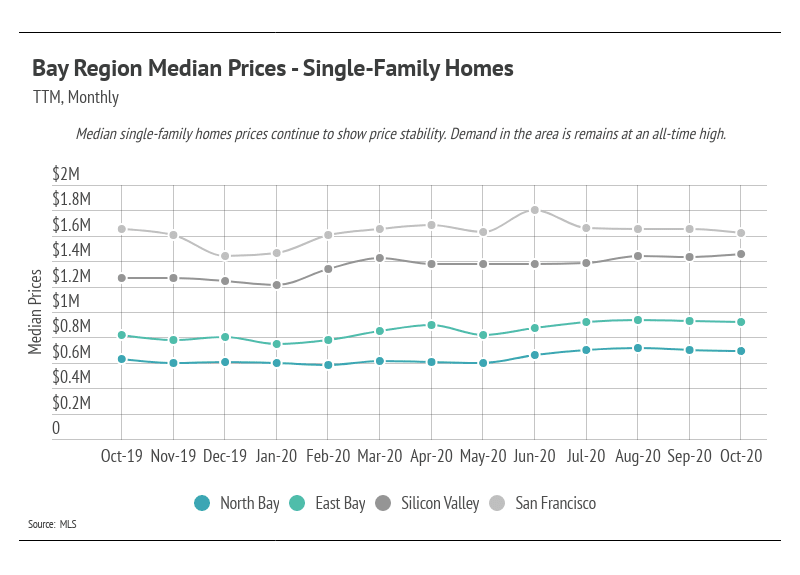

In this newsletter, we break down the Bay Area into four regions, as follows:

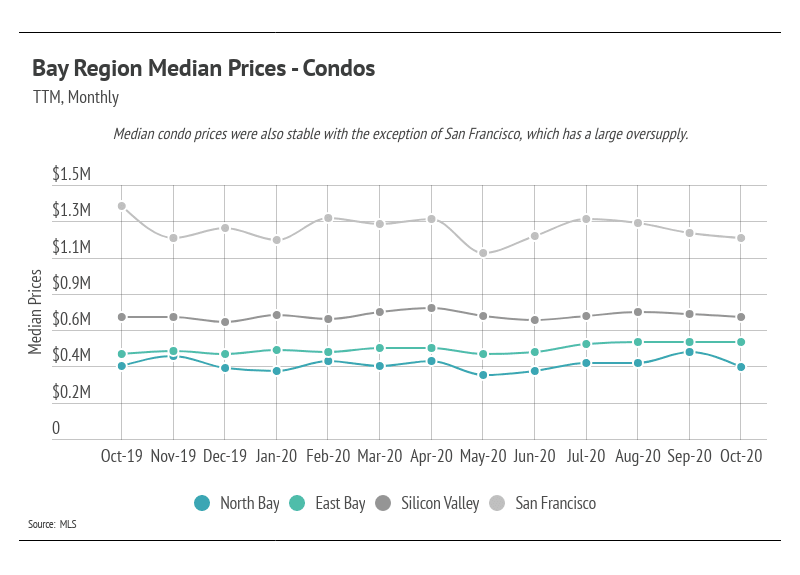

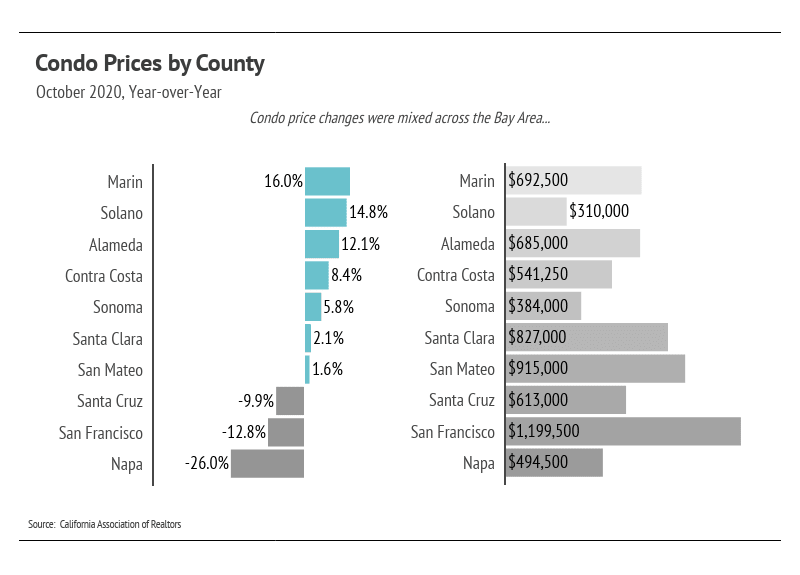

As you can see in the graphs below, median condo prices were mixed across counties. San Francisco was notably lower than last year, while North Bay and Silicon Valley were flat. Condo prices in the East Bay increased year-over-year.

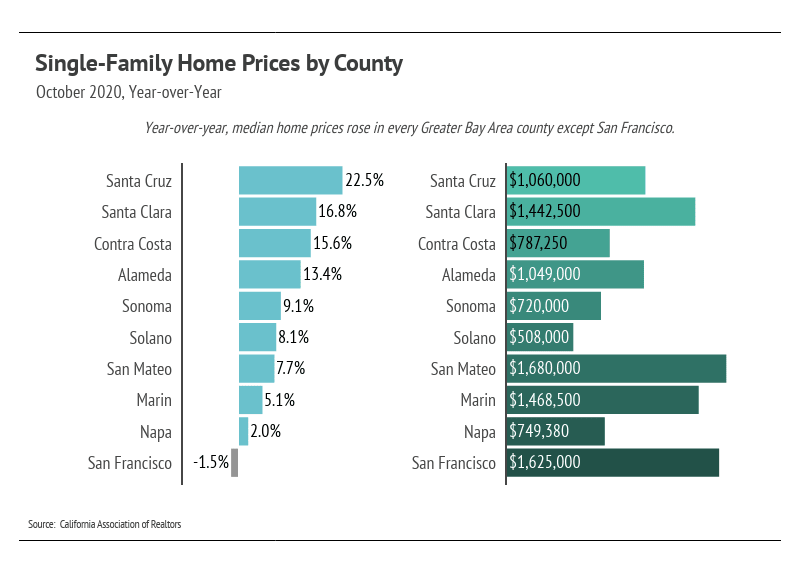

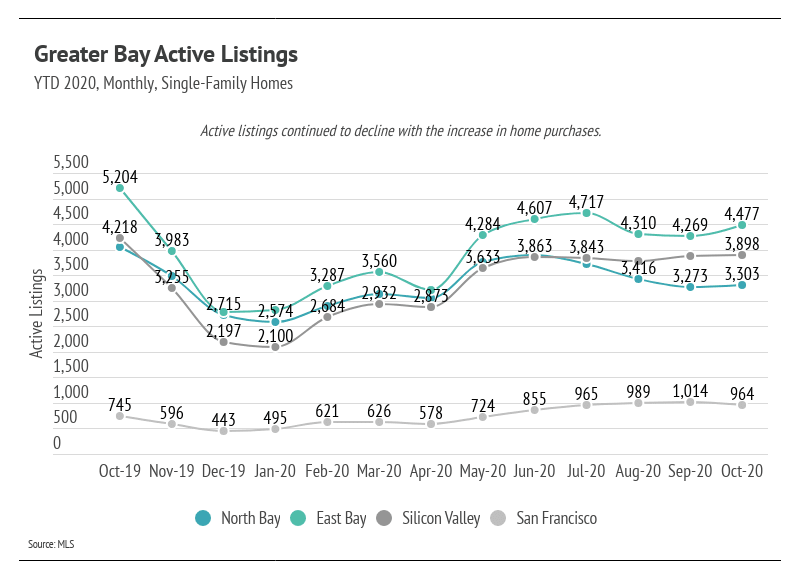

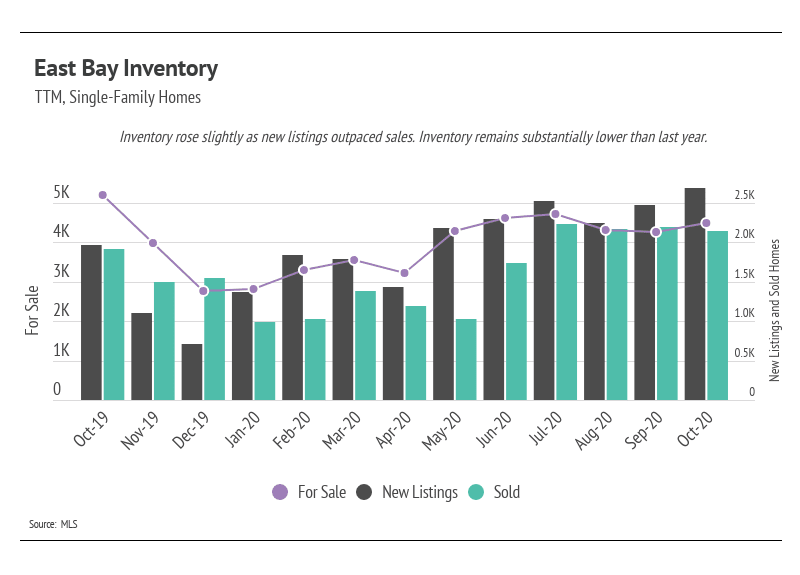

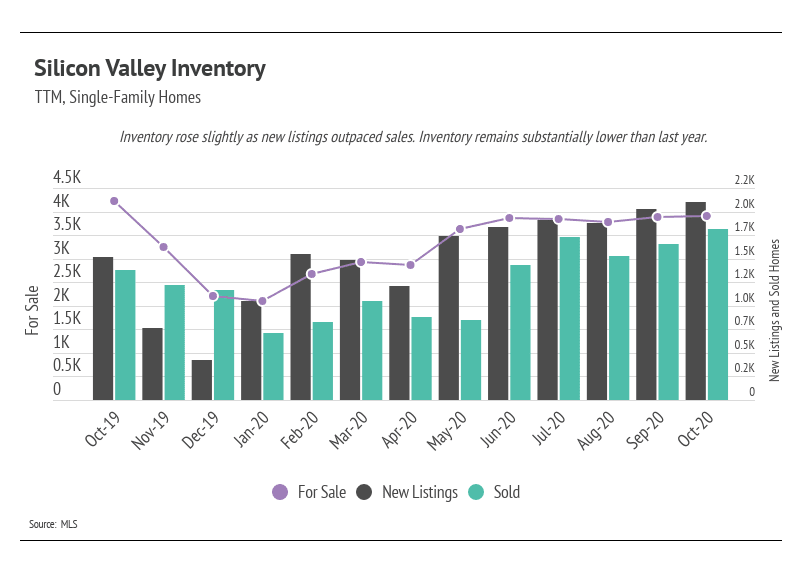

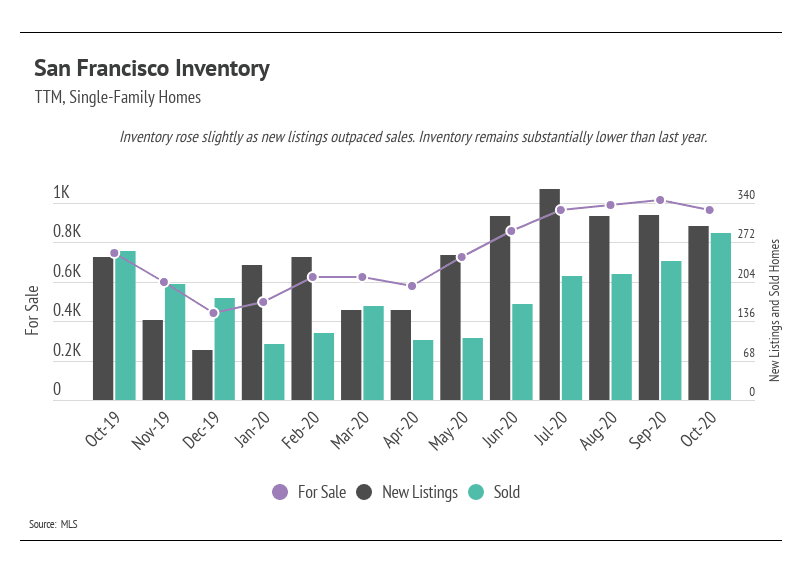

Total inventory remained lower than last year with the exception of San Francisco. Like the rest of the country, demand is outpacing new supply, which buoys Greater Bay Area home prices.

Single-family home sales have climbed since the initial months of the pandemic (March through May). Generally, buyers and sellers left the market in April and May, causing pent-up demand. Since May, sales have increased and are still near their highest levels this year for single-family homes. Usually, we expect sales to decline in the autumn and winter months, but this year’s summer selling season was delayed and seems to be spilling well into autumn. Single-family home inventory is noticeably lower than last year across regions (except for San Francisco, which has started to trend lower), and is likely to decline as we make our way into the winter months.

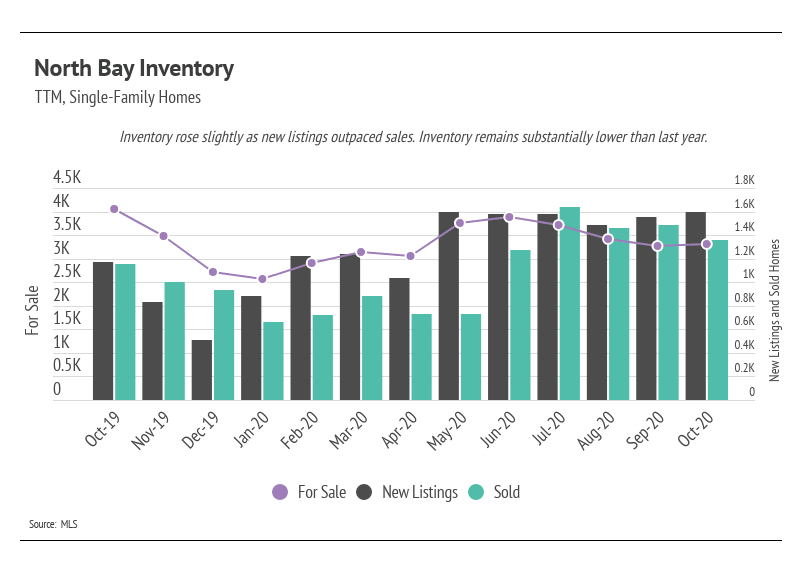

In October, new listings outpaced sales in every region. The Greater Bay Area is typically in a state of undersupply, so new single-family home listings coming to market will make the market more efficient. We expect sales to remain higher than usual during the autumn months as new supply meets the high demand in the area.

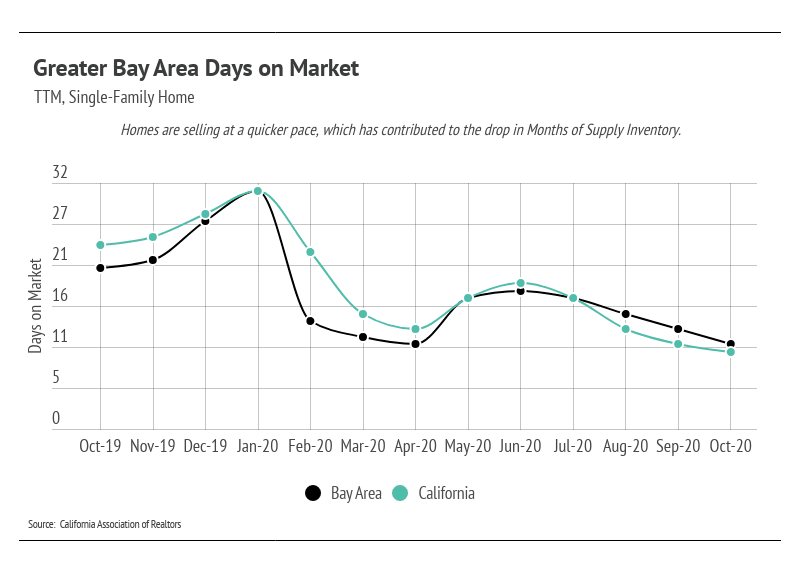

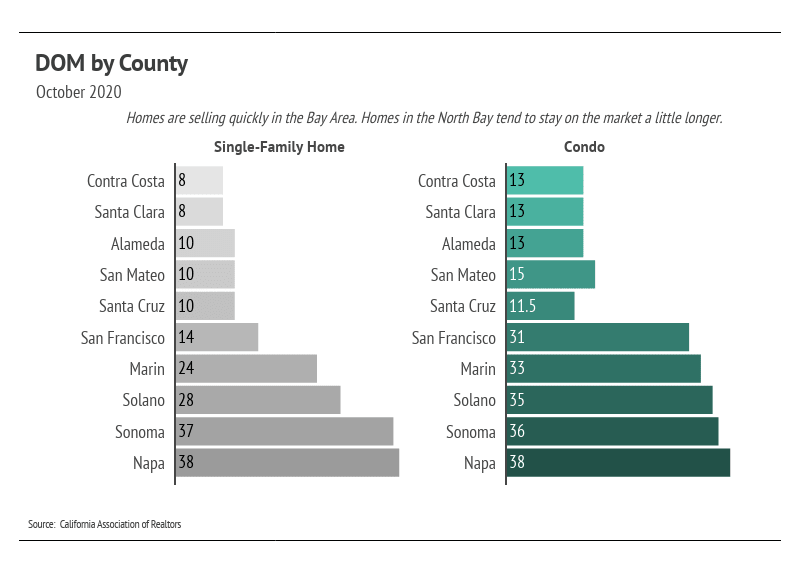

As mentioned earlier, we continue to see the Days on Market (DOM) fall due to rising demand and speedier processing through technological advances. The pace of sales affects MSI and has contributed to the low MSI over the past several months.

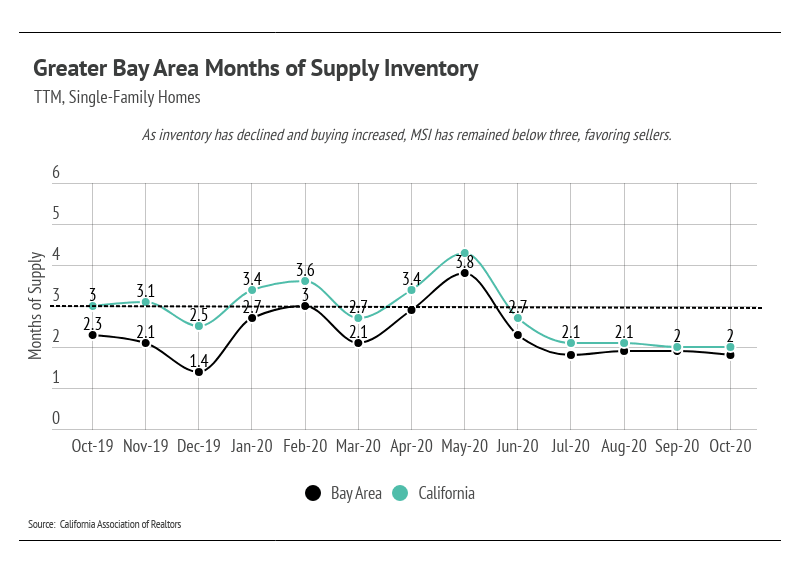

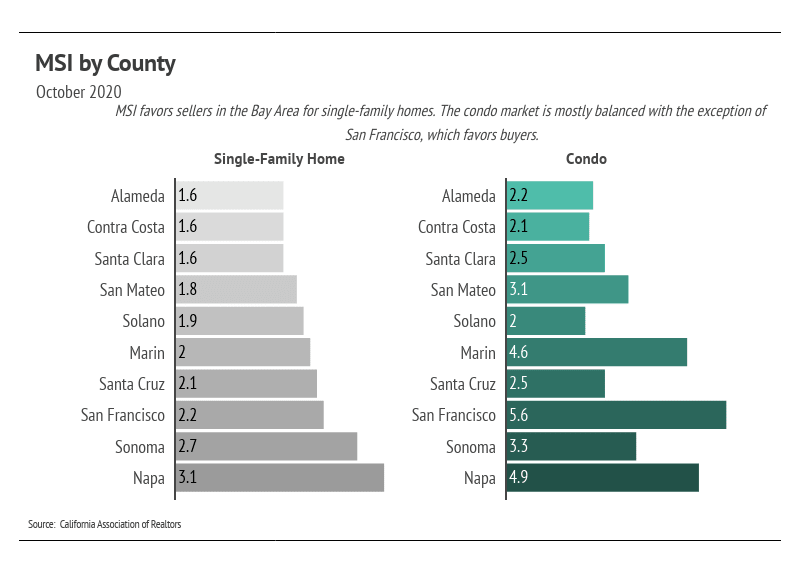

We can use MSI as a metric to judge whether the market favors buyers or sellers. The average MSI is three months in California (far lower than the national average of six months of supply), which indicates a balanced market. An MSI lower than three means that buyers dominate the market and there are relatively few sellers (i.e., it is a sellers’ market), while a higher MSI means there are more sellers than buyers (i.e., it is a buyers’ market). The MSI remains below two for single-family homes, which means that both markets favor sellers.

In summary, the high demand in the Greater Bay Area has sustained home prices. Inventory for single-family homes will likely decline further as we enter the winter months, and fewer sellers will likely come to market, potentially lifting prices higher. At both the national and local levels, home builders simply cannot build quickly enough to bring sufficient supply to the market to satiate demand. Overall, the housing market has shown its resilience through the pandemic and remains one of the safest asset classes. The data show that housing has remained consistently strong through this period.

We anticipate new listings to slow through the holiday months. Condo prices will likely remain stable with no outsized gains or losses through the winter months. The autumn/winter season tends to see a slowdown in activity, although we may see a new trend this year with higher-than-normal sales.

As always, we remain committed to helping our clients achieve their current and future real estate goals. Our team of experienced professionals are happy to discuss the information we have shared in this newsletter. We welcome you to contact us with any questions about the current market or to request an evaluation of your home or condo.

Stay up to date on the latest real estate trends.

Part 1 of HAYLEN's series on the 2026 CCIM Spring Forum in Philadelphia

You’ve got questions and we can’t wait to answer them.