Looking back on 2022 Bay Area Housing Market!

Welcome to our last Housing Market Town Hall of 2022! We will be sharing housing market stats from Santa Clara County, San Mateo County, Alameda County, Contra Costa County, and San Francisco County, as well as the hottest topics of the year and how they had influenced the real estate market. You can find the video recording of this episode here.

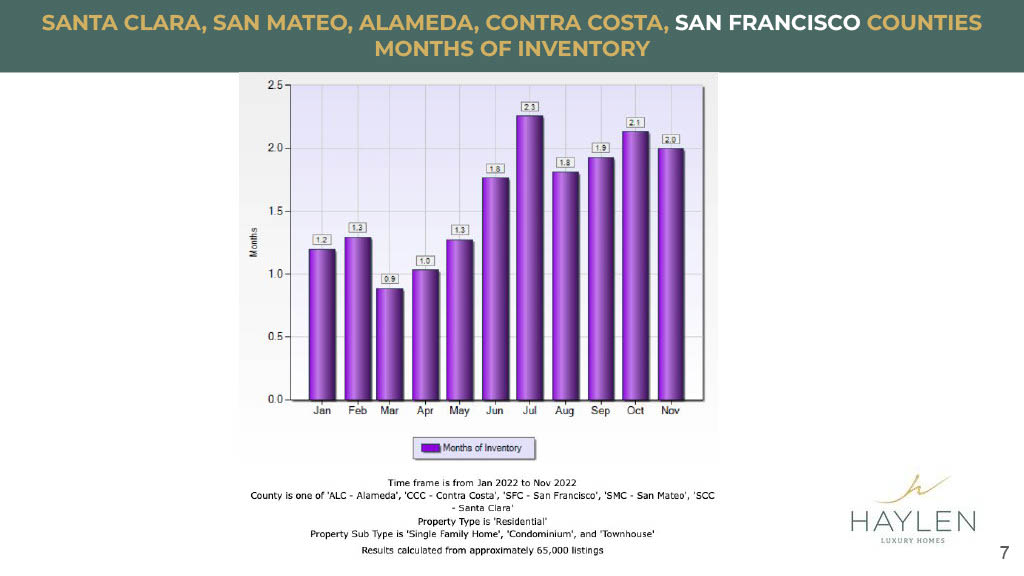

This is months of inventory and let us check how the market is doing. As you can see that at the beginning of the year, the first 5 months, or I should say the first six months, had less than 2 months of inventory. Then, we went up to 2.3 months of inventory in July and went down to 1.8, around August, and went back up in October.

Right now, we came back down two months of inventory again we've mentioned this before. It's still not bad because a normal month of inventory should be 4 to 6 months. For example, when I just started in this real estate market, about 2005, I think our market at that time was about 2 months as well but then from 2008 to 2012, there were over 6 months of inventory. It was very normal for us to wait around for our listings to be sold instead of just selling them within a week or two weeks. Now, we are back to a normal time frame, a lot of our listings that we see will stay on the market for about 30 to 60 days.

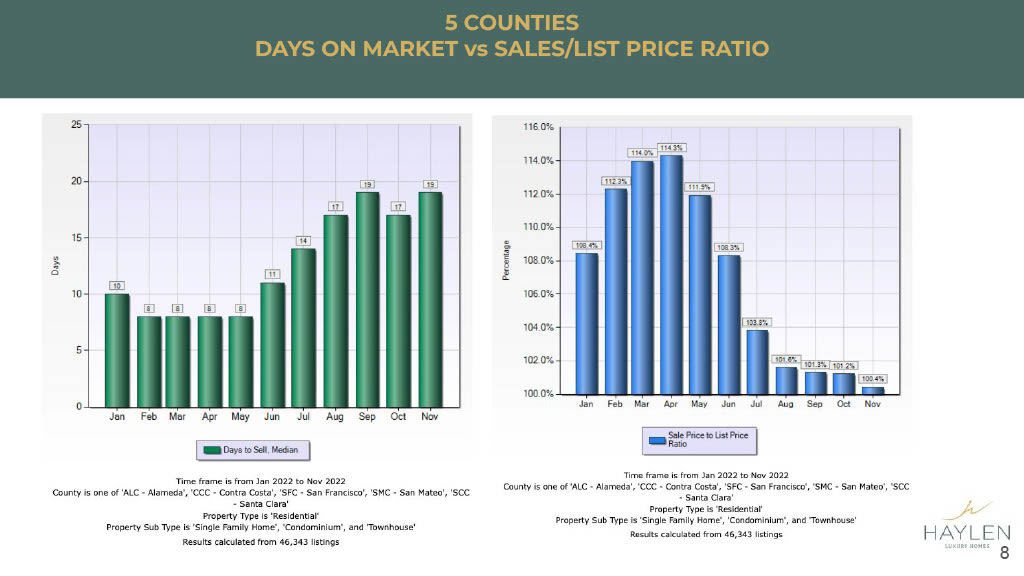

Now, what about the "days on the market" versus the “sell over list price ratio." Let's take a look at days on the market for these 5 counties.

We are staying around almost close to three weeks right now on average for 5 counties. We do see that some of the areas with a very good school district, very close to employment centers, for example, the tech companies, are still moving really fast, especially if they have a good school district. We've still seen multiple offers from those types of properties. But then we do have other types of properties that are staying on the market for, as I said, 30 days to 60 days if they don't have this extraordinary location and the homes and everything stand up. So, an average back out to about three weeks still.

But then, in terms of the sales price over the list price, as you see, it has gone from 114% all the way down to 100.4% even though I mentioned there are multiple offers but still the multiple offers are really conservative right now. People are not willing to pay above and beyond and most of the offers are below asking price.

So, this is really important to understand because it also helps with your "how to price your property." Believe it or not, there are still realtors adjusting sellers to list their property at a very low price. These strategies work in some of these areas that I mentioned that have a really good school district, everything this house is just perfect, perfect floor plan and everything but in terms of, if your house does not have all of those factors, then you should probably price it a little bit higher because most of the buyers nowadays coming in, they still make offers slightly below asking price.

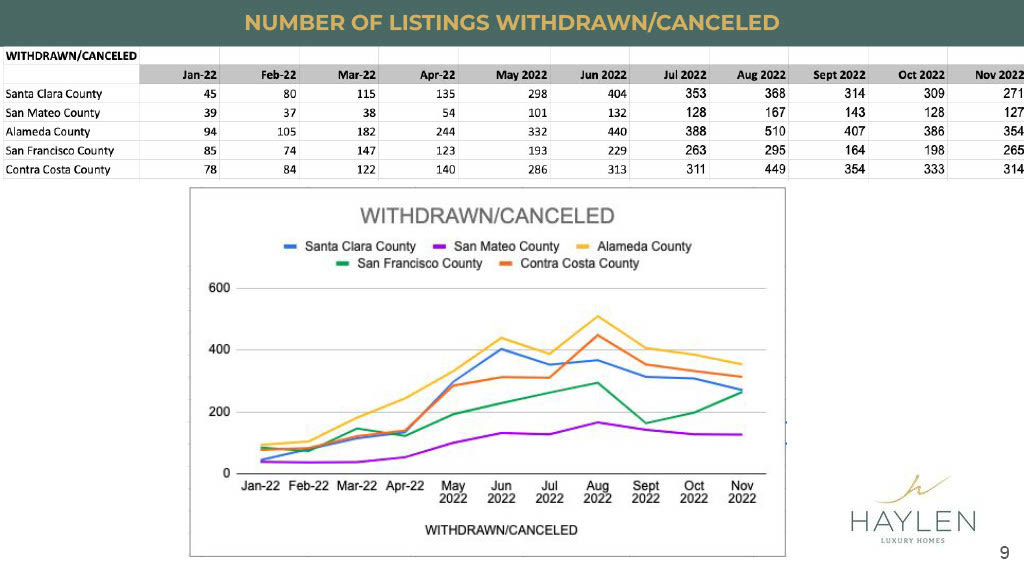

In terms of how many listings withdrawn and canceled, we trapped it because, of course, during around months of May and June which is shot up so much, the market is not even like slow, the market felt like it just paused, went back to 2020 around March and April. Although the market is open but there were no buyers anywhere. Buyers were just not looking at that time. So, you can see that at the time around May and June, there were just these huge numbers of listings being withdrawn or canceled but then the numbers are starting to come back down and they are normalizing. The number of listings, they don't have as many withdrawn and canceled. The sellers who are on the market, they now finally understand that the market has been volatile. If they are ready to put it on the market, they understand that they're not really going to be able to get the price that they were hoping for back in May or June, so we don't see as many withdrawn and canceled anymore.

In terms of the "list price decreased", in Santa Clara County, we do see it topped in August when the price was just decreasing, and then it started to taper down to November, with only 392 verses 688 listings that had list price decreased.

In San Mateo County, we topped 300 and they came down to 222 listings that have price decreased. Alameda County went up to 792 almost 800 listings that had price decreased and now it came down to only 510. And San Francisco, we have topped at 457 which was just October and in November, it came down to 275 listings. Contra Costa topped in August 910 listings and now it came down to 565.

It is interesting as now you see that a lot fewer listings in these counties have price decreased compared to previous months. One of the reasons is probably because again a lot of sellers set better expectations in terms of the asking price. We noticed that a lot of sellers were still trying to act at a really high price and then realizing that hey, it's not moving and then they finally have to lower it. But by the end of the year, a lot of sellers do have to get it sold within this year, ideally by end of the year. So, that's why a lot of them are just like we are going to just go in with a lower asking price, hopefully, we can gain some interest quickly, and then we can close by year-end.

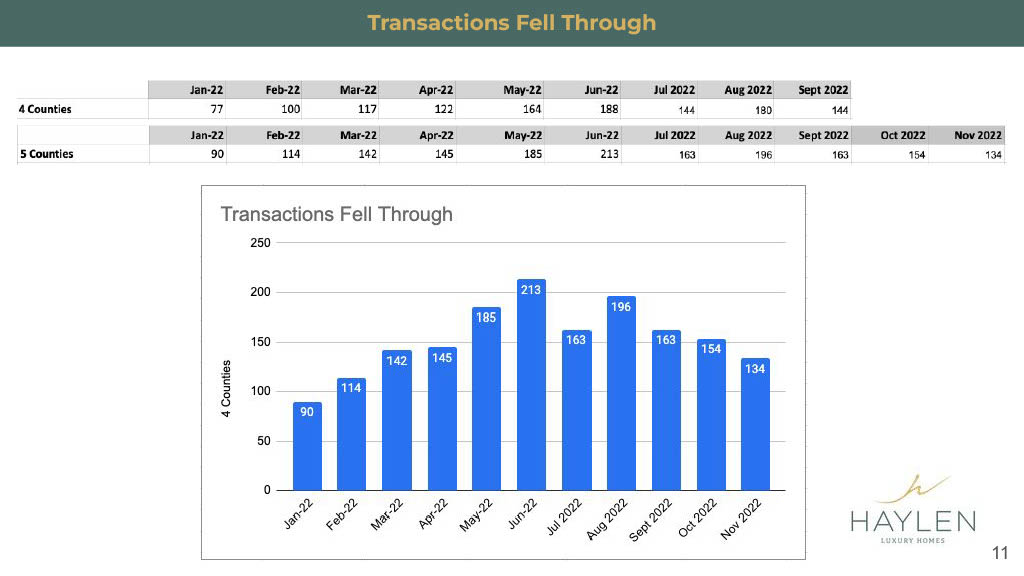

All right and "how many transactions fell through" the reason why we're looking at this is that obviously, mortgages have been a challenge nowadays. We do see a lot more contingencies, people actually have inspection contingency and loan contingencies and that's also another reason why we see some sellers who would prefer to take a lower offer but they would like to take a cash offer because then there's not as much uncertainty with their loan. So that's what we notice for a few of our transactions the sellers would take a relatively much lower price compared to a finance offer by like 50,000 dollars or more just so that they can have peace of mind and just close the deal.

So, when I kind of did both, it's like four counties because I wanted to compare, I redid all the numbers. So in January by adding the San Francisco County in here. You can see that the difference is about like 20% in terms of the number of transactions that fell through.

In November, we actually have dropped quite a bit to only 134 deals that were transactions fell through for all five counties and honestly, 134 is really not that much if you look back to the beginning of the year, March or April, we're around the same numbers over that time. So, really 134, this number is actually pretty good for all five counties.

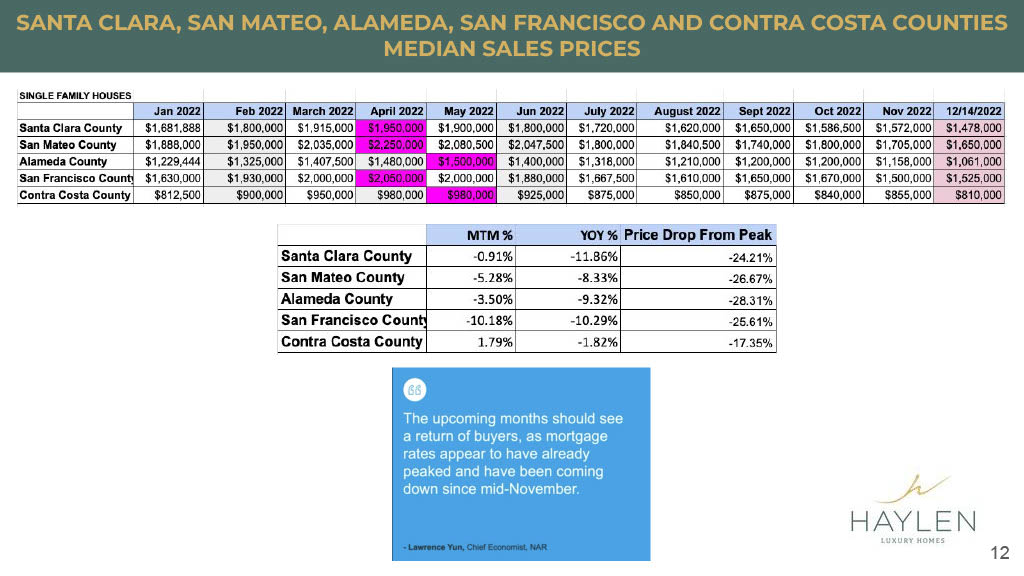

Of course, everybody wants to know is that what happened with the price, right? So, now here we track all these median sales prices for all five counties and these are all for single-family pricing.

Now, the purple area, these are the highest during this whole pricing kept going up and up and then it started coming down. So as you see Santa Clara County peaked in April at $1.95 million and we had a full month of November, it came down to $1.572 and as of today the median sales price is $1.478% for Santa Clara County.

As for San Mateo County, peaked in April at $2.25 million and as of November full month is $1.705 but as of today is at $1.65 million in terms of the median sales price.

For Alameda County, it actually peaked in the month of May at $1.5 million and as of November, it was $1.158 and then as of today is $1.061 million for Alameda County.

Now, as for San Francisco County, we peaked in April at $2.05, and in November, the full month, $1.5 and it's interesting for San Francisco County actually the price had gone up a little bit as of today at $1.525 million. But the price adjusts a little bit, I do see about maybe $50,000 plus or minus in terms of like when I do a half month versus the full month. There's going to be some adjustment there but it's not going to be huge. At least, right now, we see it unless there's this one big deal that happened in the county but it looks like it has gone up. So, we'll see next month when I do a full month of December, and let's say that $1.525 is truly the number.

In Contra Costa County, in May, it peaked at $980,000 and as of November 30th, a full month of November, it had come down to $855,000 and as of today, it is $810,000.

So, what does that mean? We look at their month-to-month percentages, Santa Clara County came down 0.91% compared to last month and year-over-year came down about 11.86%. Year-over-year is comparing last year's December to this year's pricing. But, if you look at the peak number which was kicked in around April and May, then it had dropped quite a bit about 24%.

For San Mateo County, month-to-month is a drop of 5.28%, year-over-year 8.33%, from the peak it had dropped 26.67%.

Alameda County, month-to-month is a 3.5% price drop and a year-over-year is about 9.32% price drop, but then coming down from the peak is about 28.31% almost 30%.

I know some of you probably would be like, oh! my gosh, if I'm close to escrow around April and May... I know it's tough. If you are living in your house on a property for a long term 5 to 7 years still sweat it, you've got this amazing interest rate. A lot of people who are buying right now wish that they have that kind of interest rate, so you are still winning in that sense. But understand it looks really bad right now by looking at these numbers.

So, I just want to allow you guys to see the positive side of it, which is that you've got to enjoy this very low-interest rate and it's going to take some time for us to get there.

San Francisco County, month-to-month percentage came down to 10.18% and year-over-year came down to 10.29%, the price drop from a peak is actually 0.5% to 0.61%.

And, now, Contra Costa County, month-to-month actually went up 1.79%, went up a little bit, but it dropped about 1.82% year-over-year which is really little, it's not much at all and it dropped the least as from the peak of 17.35%.

So, I thought this is interesting to recap, we are in December just kind of look back to see how bad it has been. I know everybody's kind of really worried, the market has changed, completely shifted from this high to really low. Right now, looking at this on average about a 25% drop across the counties.

Do I think that this is the right time to buy? I still think that the price probably going to drop a little bit more next year in the beginning and I'm going to go into a little bit more of the macroeconomics of this as well. So, you guys can take a look at what you think the market is going to be like next year and this is by Lawrence Yun. Lawrence Yun said that the upcoming months should see a return of buyers, as mortgage rates appear to have already peaked and have been coming down since mid-November.

Some of you might notice, I know we did see a couple of price drops, hopefully, Sean will be able to come in and then share that information as well regarding the mortgage rates, but we ourselves among our own clientele, we do hear a lot more about "oh, we're going to pause right now and we're going to come back next year to take a look at the market, see where it is."

So, we do expect more buyers to come back but it doesn't mean that the price is going to come back up just because the psychology is so different now. They're going to come back but then they just going to probably make offers, very clear conservative offers until we start seeing the mortgage rate start to come down, then you're going to see really a lot more buyers are going to come back up to buy. But there are so many other factors that can affect the market and we are going to go into it in a little bit to talk about that as well.

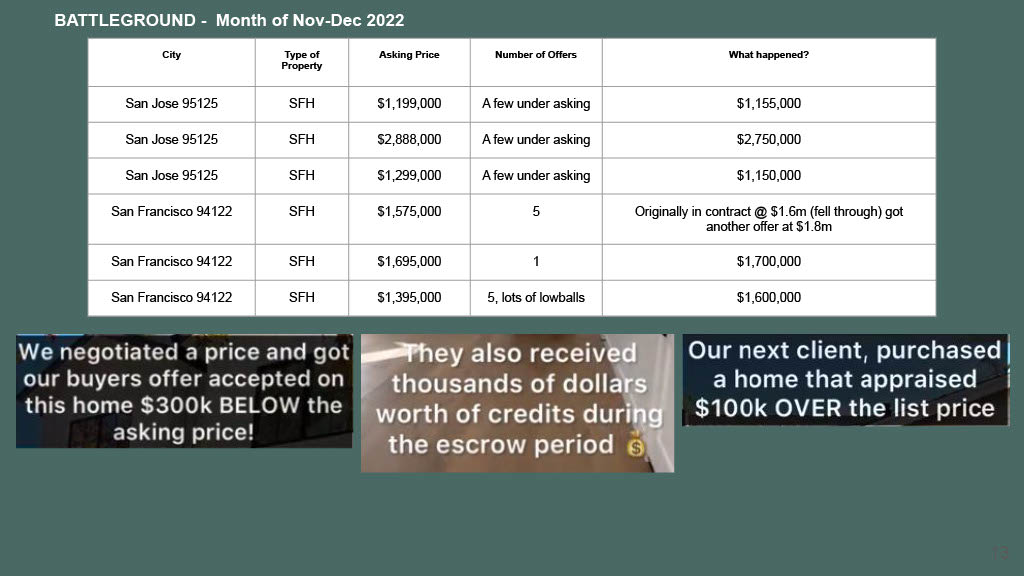

These are some of the Battlegrounds we have for November and December. Definitely slower months but we had a few under the asking price, a few people are offering but they're all under the asking price. For example, in the San Jose, Willow Glen area, it ranges from $1.2 million to almost $3 million, but they all pretty much came in under the asking price.

San Francisco area asking 1.575 and had 5 offers but went to $1.6 million and that it fell through but they got another offer at $1.8 million. I mean it sounds interesting because how come they had multiple offers originally when under contract 1.6 and then all of a sudden, they got another offer at $1.8 million? I do have to say that's something you have to be careful about what kind of agent you're using to make sure that they understand the market, how the market is and how the psychology of all the buyers are right now.

The last one San Francisco with a 1.395 asking price, got five still a bunch of low-ball offers but you just need to take one person to be willing to offer over the asking price and now they had a $1.6 million dollar accepted price for that listing.

Underneath the bottom here, we shared a little bit about our own experience with our buyers. We will even negotiate a price almost $300,000 below the asking price on one of the properties that we knew during the peak would have been crazy, maybe $300,000 over the asking price, but it does have one flaw on this property that it's on the busiest street so they had a lot of interest but they didn't really have a lot of strong offers. So, we were able to negotiate.

Then, also for a few buyers now, we were able to negotiate some credits during escrow due to a lot of different reasons just because like nowadays we do have more contingencies on our offers so after inspection contingencies, sometimes buyers just feel like okay I feel like I need to renegotiate or we had a situation where the loan almost couldn't close, so we had to negotiate some credits back in order to close the deal.

These are some of the situations where we were able to actually negotiate our clients and then lastly, there's a client that we negotiated and when we got the appraisal, it came back $100,000 over our offer price. So, it was really awesome knowing that they already have that equity right off the bat.

Now, what about the multi-family market? We are looking for multi-family, industrial, and office. These are kind of like three sectors that a lot of commercial realtors or investors are looking at right now and I have to say multi-family is still the winner even though in this slow market. The only difference is that we do have fewer buyers right now mainly because the interest rate has gone up so much. So, it makes it a little bit more worrisome for them but multi-family is still a very strong sector in commercial real estate.

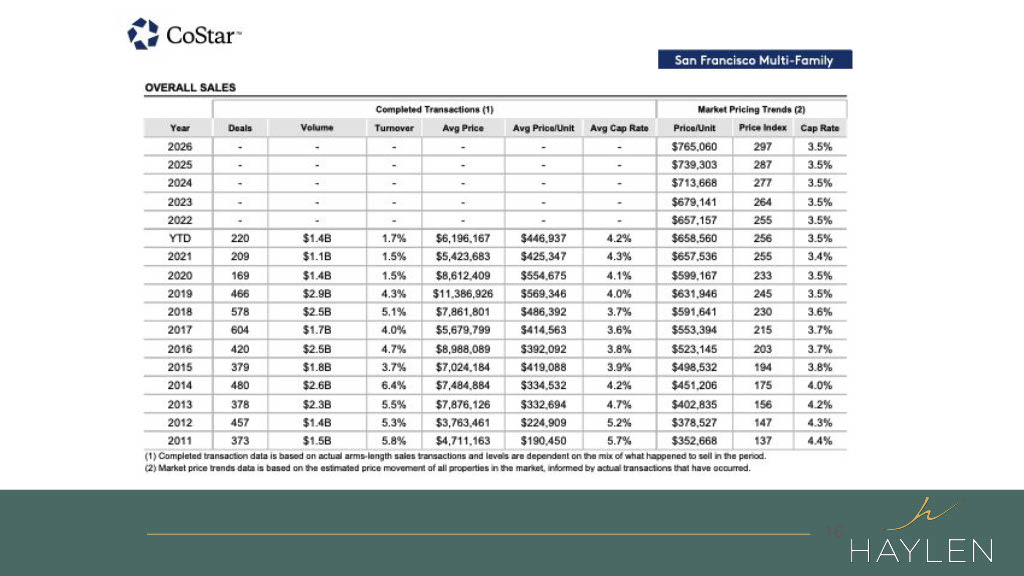

Let's take a look at this report from CoStar. This is for San Francisco multi-family side and as you see, the year-to-date cap rate is still at 3.5%. If you understand cap rate and interest rate, you get a cap rate at 3.5% and while your mortgage rate is at 6%, you're not going to cash flow and even if you put 50% down payment, you still can't get a cash flow on these properties and it's just amazing to know that they are still getting 3.5% cap during this kind of slow market.

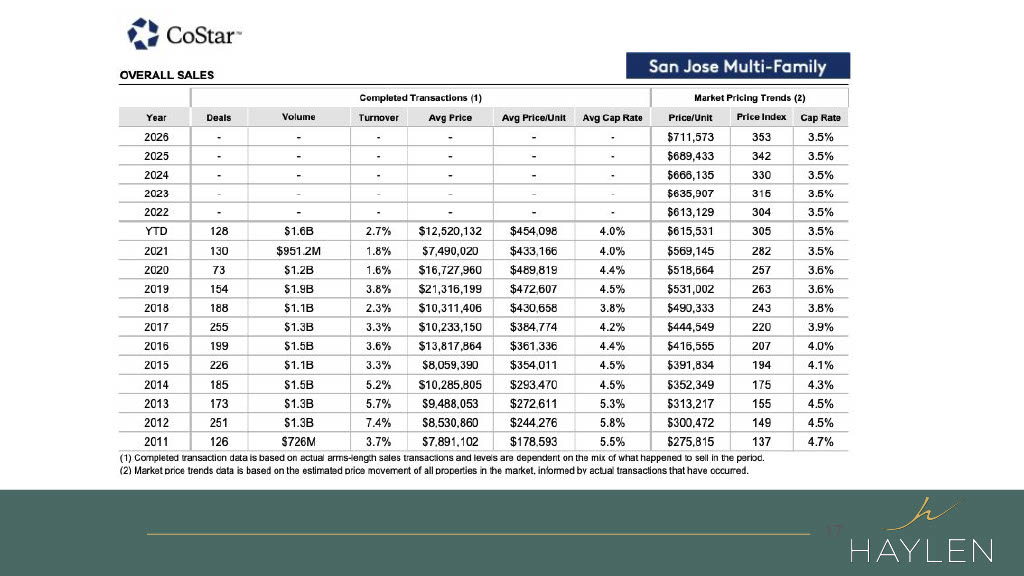

As for San Jose, the same thing, they are actually at a 4% average cap rate and the trend is that it's still thinking that it's going to stay right around 3.5%, mainly because a lot of times sellers are still not willing to come down on their selling price. They still see that there is a lot of rental potential on the market. So, we definitely have this huge discrepancy between the seller's expectations and the buyer's expectations. The market is slowed down quite a bit in 2022 for the multi-family market. But at the same time, the cap rate is still staying really strong.

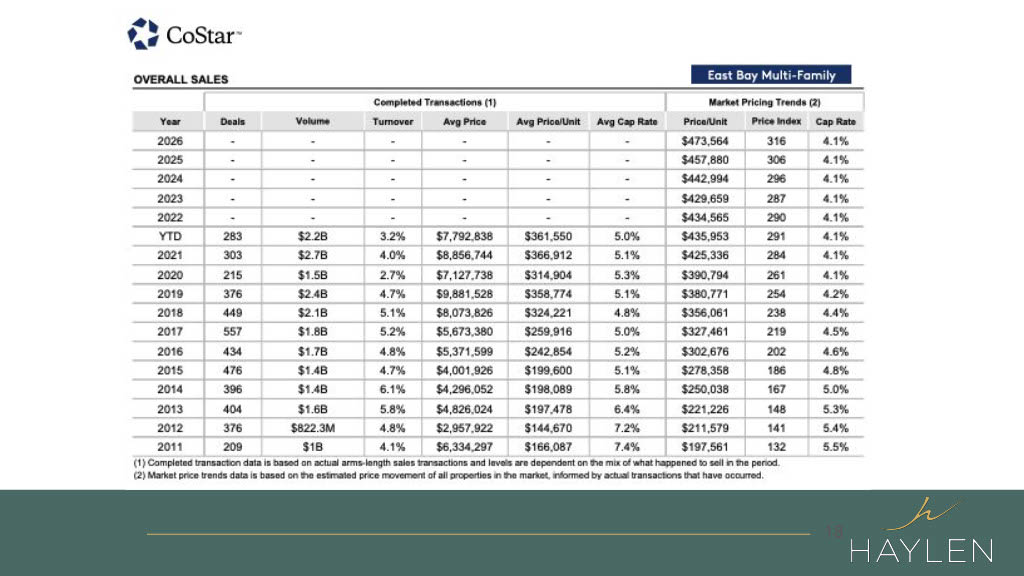

For East Bay Multi-Family, the average cap rate is about 5% which is a little higher and it's very common to see that East Bay cap rate is a little bit higher than San Francisco and also San Jose but then they are expecting the cap rate is going to stay at around 4.1% or so.

This is, I thought, is really interesting to see when the interest rate for the multi-family side is at about 6% or more but their cap rate is so much lower compared to the mortgage rates and it didn't get adjusted drastically compared to how much the mortgage rates have gone up.

Let us talk a little bit more macroeconomic side. In 2022, we have a lot of hot topics this year including

In the last year, during our webinars, I have talked on pretty much all of these topics besides the tech layoffs because it just started to happen towards the end of the year, the fourth quarter.

Let us look at the FED fund rate, today, December 14th, and they just raised the rate by 0.5%, which is a lot but at the same time, the good news is that everyone was expecting they are going to raise the rate by 75 basis point until the inflation rate had come out was lower than expected so they decided that it was like 0.5%. This is already good enough. They don't have to increase by 0.75%.

I thought that it is a really good indication that we are slowing down on increasing the effect funds rate. Right now, the outlook is that they are going to raise it to about 5.1%. So, I think, probably at the beginning of the year, they're going to do a couple more rate raises and then that's it and the rate is probably going to stay pretty much constant.

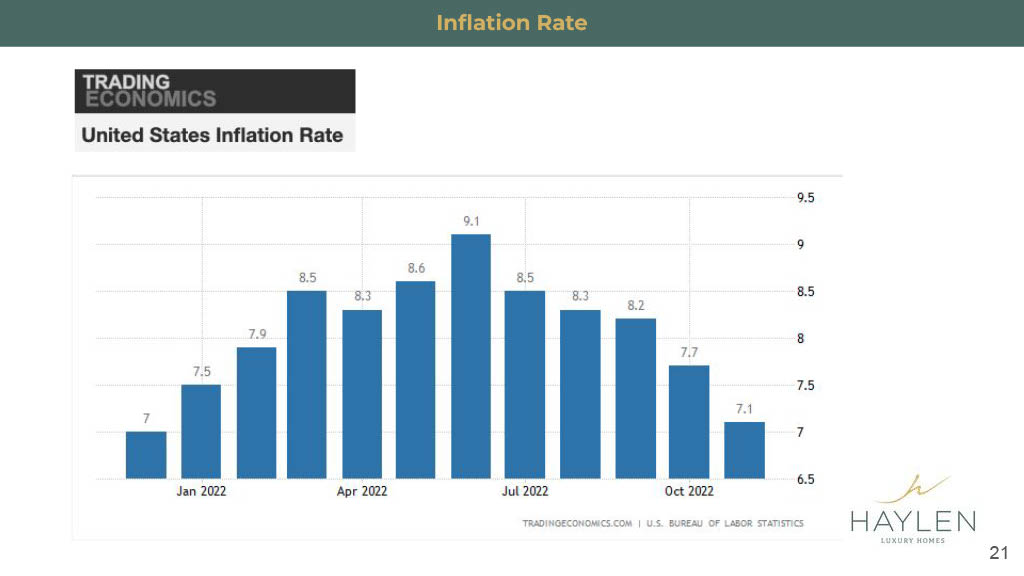

In terms of the inflation rate, as we mentioned, the inflation rate has been pretty high, starting in January, at 7.5%, all the way peaked at 9.1% in June and now it came back down to 7.1%, which is not a great number yet, but it is going into the right direction at least.

In terms of the unemployment rate, I know there is a lot of concern for employment in our area.

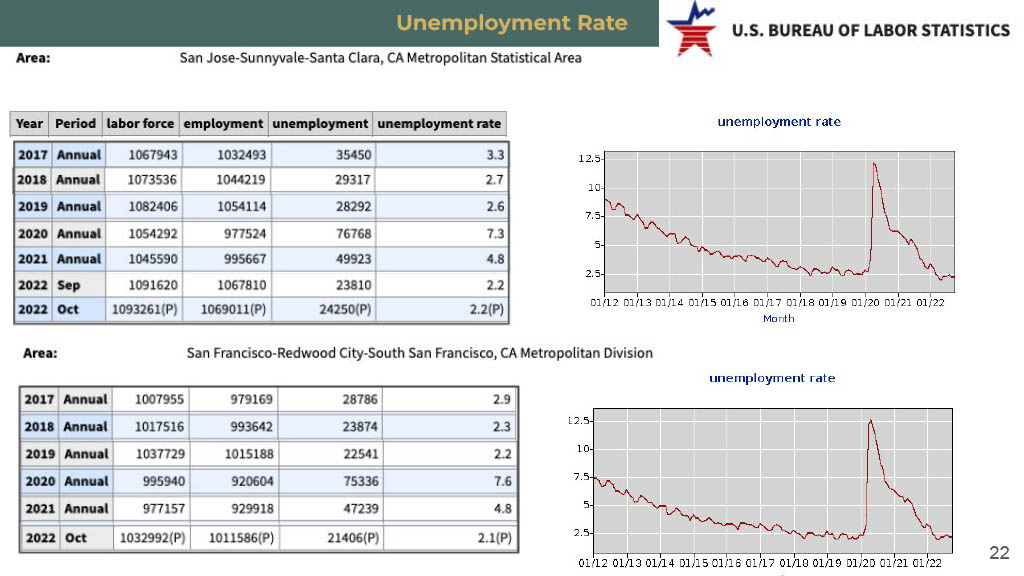

In the San Jose, South Bay Area, let us look back in 2017, the unemployment rate is at 3.3%; 2018, 2.7%; in 2019, 2.6% and of course, in 2020, went up to 7.3%, came back down to 4.8% and as of October 2022, is at about 2.2%.

But I thought it would be interesting to also look at the labor force. We had about 1,068,943 people in the labor force and now we have about 1,093,261 people in the labor force. We definitely have more people in the labor force and unemployment, in terms of the number of people, as you see here, is actually lower than the 2017 numbers. I just thought to point that out. Besides looking at the rate, we can also look at the number of people that they are counting for.

In terms of San Francisco, Redwood City, so more to the peninsula area, in 2017, the unemployment rate is at 2.9%; in 2018 at 2.3%; in 2019 at 2.2%; and then 2020, at 7.6%; in 2021 at 4.8% and then in 2022, it came back down to 2.1. The same thing, they have quite a bit more people in the labor force, but at the same time, the unemployment number of people has come down quite a bit from 28,786 to 21,406 people.

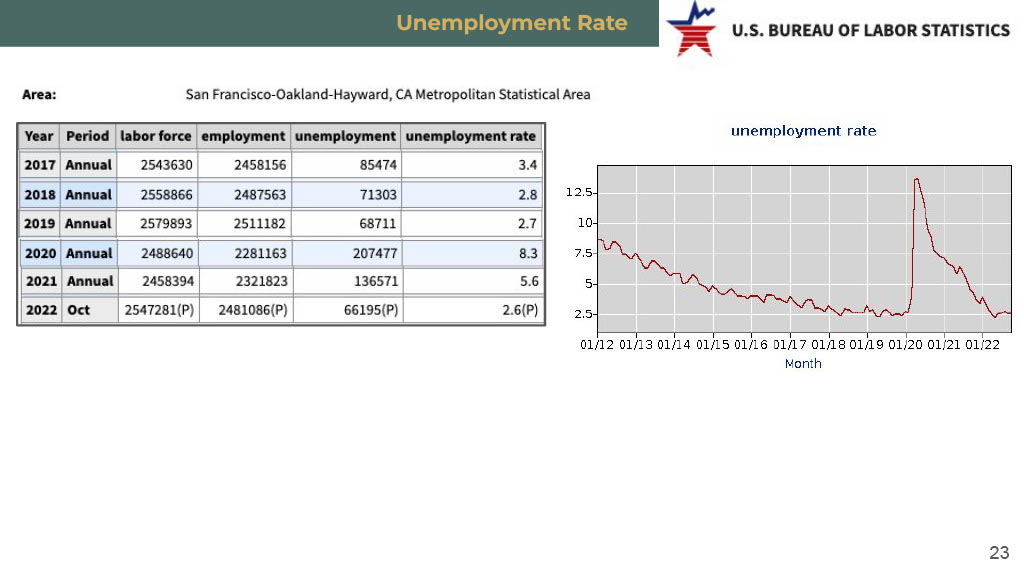

Now, what about on the other side, more like the East Bay, like San Francisco, Oakland, and Hayward area, for 2017, they were at 3.4% on the employment rate; in 2018, 2.8%; in 2019, 2.7%; 2020 at 8.3%; 2021 at 5.6% and 2022, right now, is about 2.6%. However, the labor force for this side is staying around the same. It doesn't have the increase we saw in the San Jose area and also the San Francisco Peninsula area. In terms of the number of unemployed though it still also has a lot fewer people compared to the past five years. But then we still have this concern because we have all these Tech layoffs.

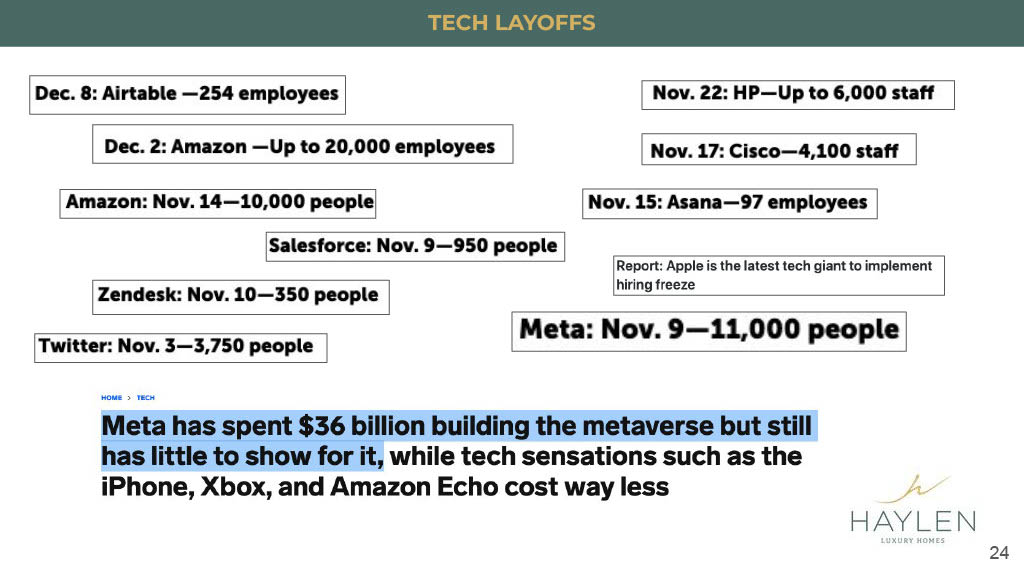

We talk about Airtable, Amazon, HP, Cisco, Asana, Amazon, Zendesk, Salesforce, Twitter, and Apple and of course, Meta and Meta also has spent $36 billion on this Metaverse but it just seems like it's not really catching on.

This is actually a real interesting thing I kept thinking Metaverse is supposedly the thing. This virtual world, I myself is not crazy about it. I just cannot imagine us wearing these goggles and just going to meetings in our Avatar or whatever and communicating and networking with people.

I know it definitely is going to be something but I do hope that my kids are not going to be living in this Metaverse. I hope they will be living in the real world still. So, I don't know. I have this mixed feelings about Metaverse. I think it's really scary at the same time I know it's going to happen. I just hope that they are not going to be hooked into that and live in this virtual world but anyhow.

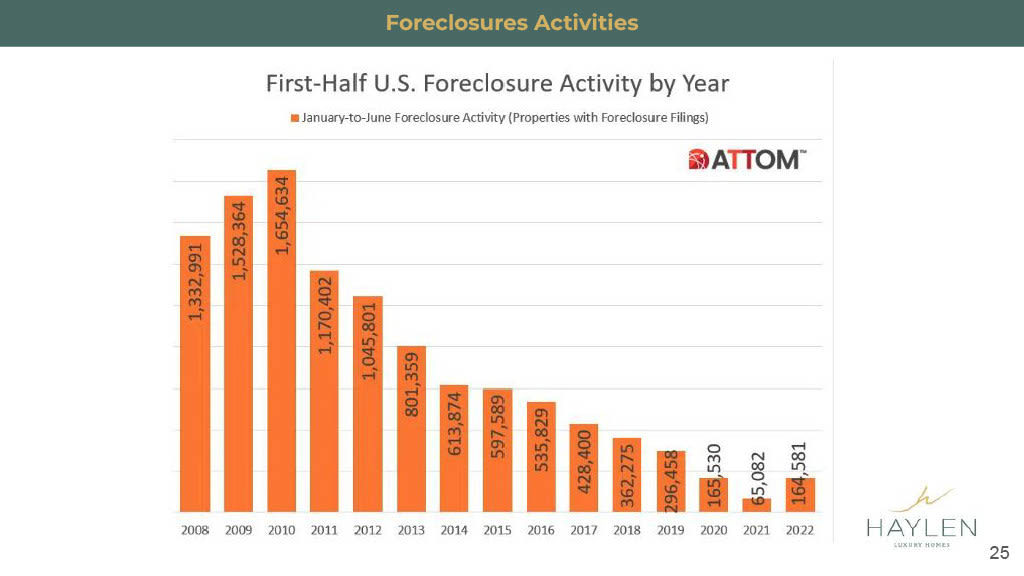

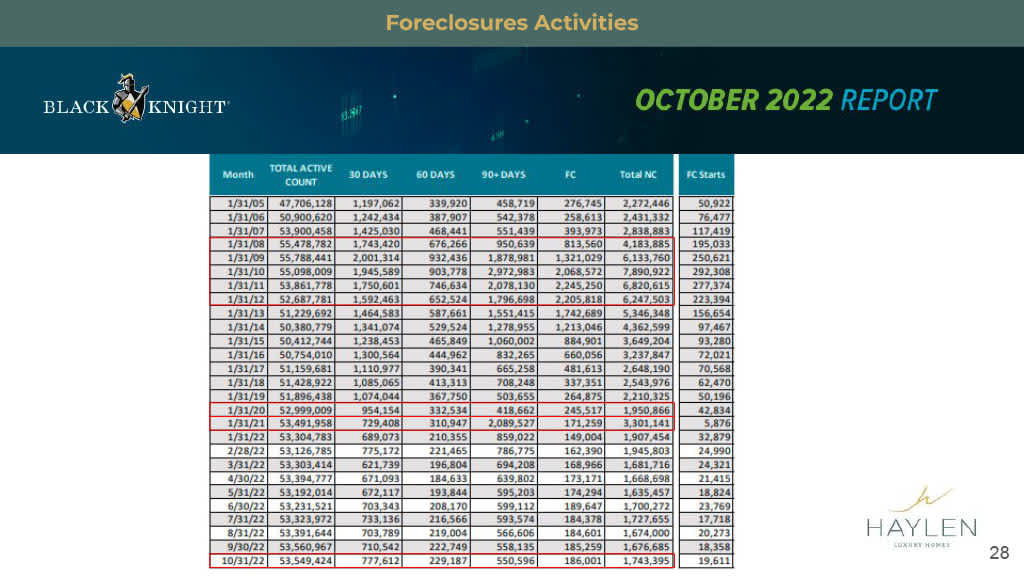

So, let's look at the Foreclosure activities as well. We've been talking about this. There are a lot of reports talking about, "oh, my God, the foreclosures have gone up by 50% or 100%, so let's look at the numbers.

If we look at 2008, the Foreclosure activities from January to June filings, 2008, during the last March recession, those are all over a million foreclosure activities and right now, in 2022, the first half, we had about $164,000 in foreclosure activities.

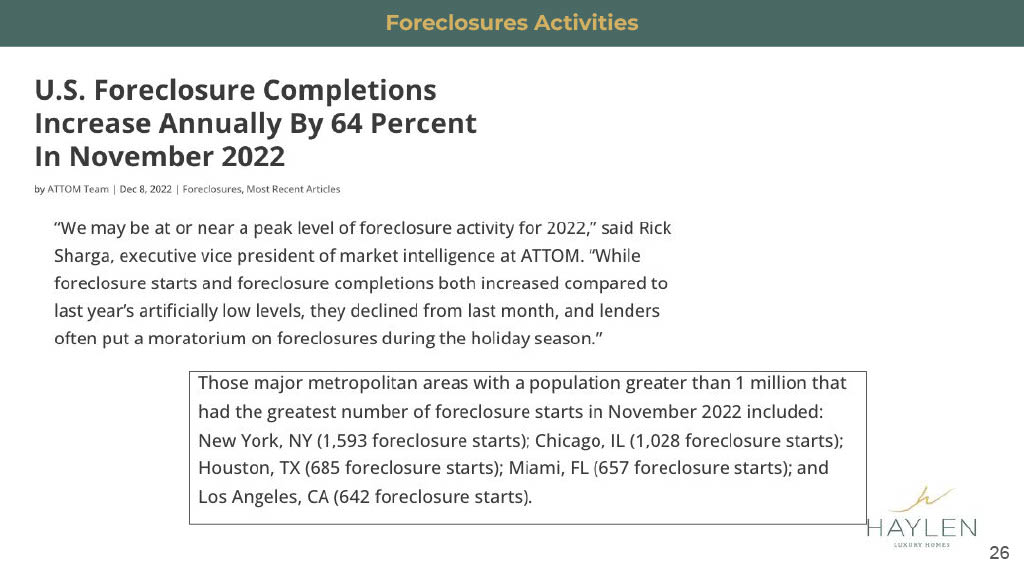

Here is some news article from ATTOM team and U.S. foreclosure completions increased annually by 64 in November 2022. Again, I just want to show we do see a lot of these articles right now talking about how foreclosure activity is peaking. While foreclosure starts and foreclosure completions both increase compared to last year's artificially low levels, they declined from last month, and lenders often put a moratorium on foreclosure during the holiday season.

Why they say "artificially low levels" is mainly because there is a foreclosure moratorium last year still. They just didn't start that foreclosure process and that's the reason why the numbers were really low last year.

Those major metropolitan areas with a population greater than 1 million had the greatest number of foreclosure starts in November 2022 including New York, Chicago, Houston, Miami, and Los Angeles.

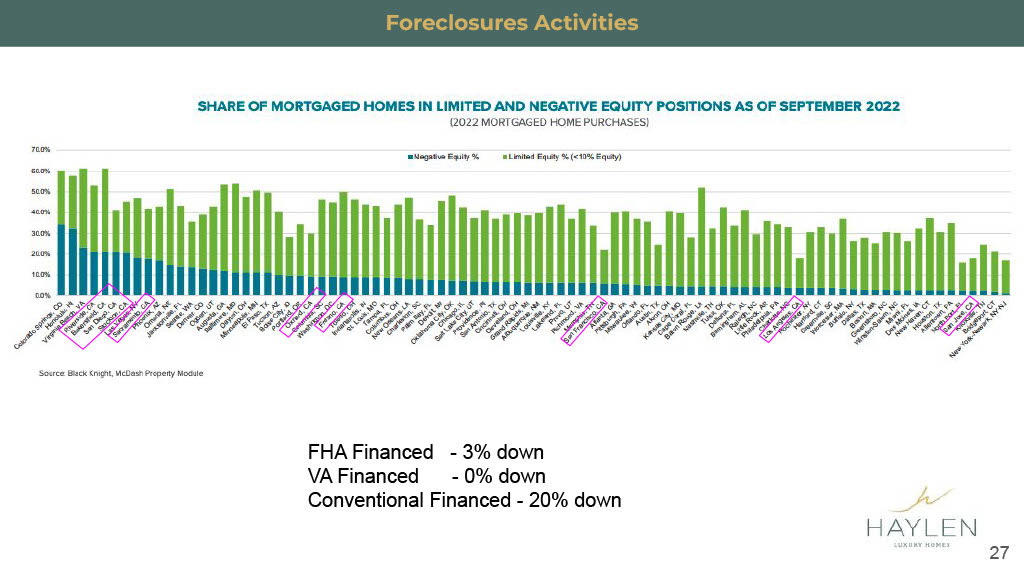

Here it is super small. I know you probably cannot see but I try to highlight all the California cities. So, in this chart, the green bars are showing that how many properties are, in terms of percentage, of less than 10% equity. Then, the blue bar means that they actually have negative equity. Total of all that, meaning that they all have less than 10% equity.

If you look at Riverside, Bakersfield, San Diego, Stockton, and Sacramento, they are ranging quite high. These are all about like over 50% and Bakersfield is over 60% and has less than 10% equity, and they have about 20+% in terms of negative equity.

There is also Oxnard, Fresno and if you look at San Francisco, a little over 20% of the properties have less than 10% equity and about maybe I think this looks like about 5% that have negative equity. Then, Los Angeles, looks like it has less than 20%, probably about 18%, that has less than 10% equity and I don't know the numbers, I'm just eyeballing it is probably about 3%, that's I have negative equity and then San Jose is all the way down here; it looks like maybe 1% or 2% or 1% that has negative equity and has less than 20% that has less than 10% equity.

I thought this is important to look at because if we are worried about foreclosure activities, we definitely need to look at the statistic whether how much equity these properties have. And as you see a lot of times these areas, Riverside, Bakersfield, Stockton, or Sacramento, they probably have a little bit more people use FHA Finance or VA finance and they only require 3% down and 0% down which means that they will have a lot less equity on the property versus in San Jose area, a lot of people have to use 20% down conventional financing in order to buy the property so that's why they have a lot fewer people have negative equity on their property.

In terms of the foreclosure numbers, if we look at comparing 2008 to 2012 where they had $4 million to $6 million non-current loans compared to January 2020 where they had $1.95 million, and also 2021, they had about $3.3 million versus right now in October, we have $1.7 million which is even less than in the year 2005. These are everything, not just foreclosure but all the non-current loans meaning they are not current on their payment.

In summary,

There are still going to be some issues there, so I cannot tell you whether next year is going to be a great year or not I know there's still a lot of negativity about next year, and uncertainty about the economy. I feel that way too but in terms of me being on the ground watching how our buyers are responding to the economy, we just know that there are still a lot of buyers and there are still a lot of demands but they're just really watching how the market is going to go and also in North San Jose, they just approved these 36,000 units housing so that's going to be a huge housing supply onto the market in San Jose area. Downtown San Jose, they still have all these developments going on with offices. Offices are one asset type that I'm really worried about but the smaller offices seem to be moving but if you have a bigger office building that's what is a little bit tough to move right now.

Thank you everyone for joining and happy holidays! This month we also invited Sean Crowley to be the guest speaker for our second episode of the Bay Area Housing Market Townhall Lending Series. Check out this video to learn How To Create a Win-Win Negotiation in a Slow Market. If you have any questions, please don't hesitate to reach out, we are here to help.

Stay up to date on the latest real estate trends.

A Bay Area Realtor's approach to schools, neighborhoods, and long-term value for families making a move

Part 1 of HAYLEN's series on the 2026 CCIM Spring Forum in Philadelphia

You’ve got questions and we can’t wait to answer them.