November Newsletter – Housing Market Updates for the Greater Bay Area

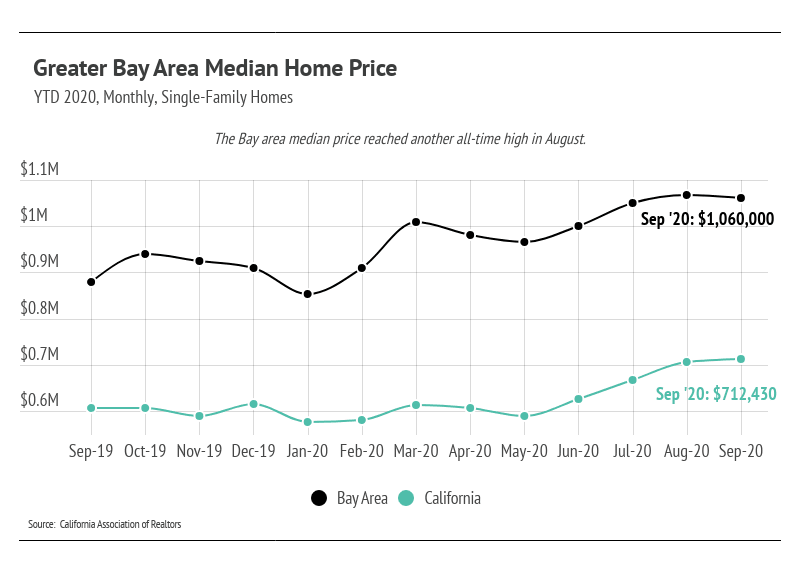

Median single-family home prices continued to increase substantially year-over-year with a median home price of $1.06 million still near the all-time high seen in August.

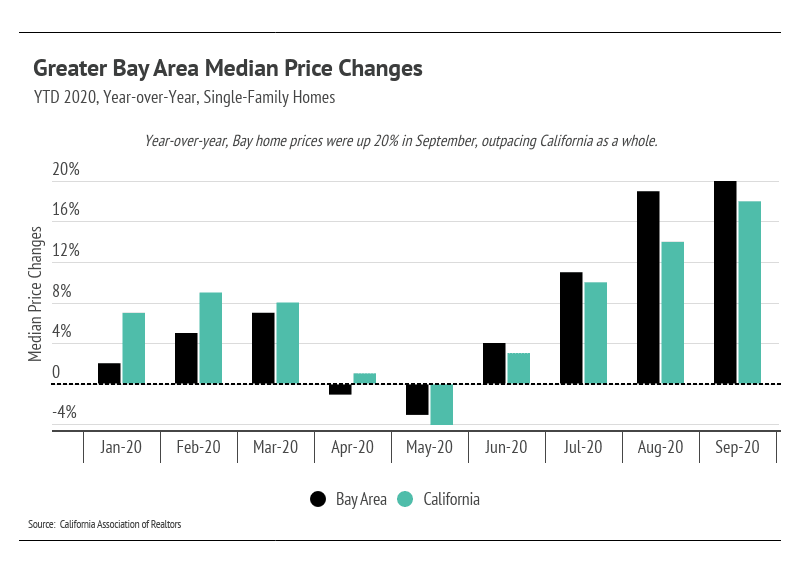

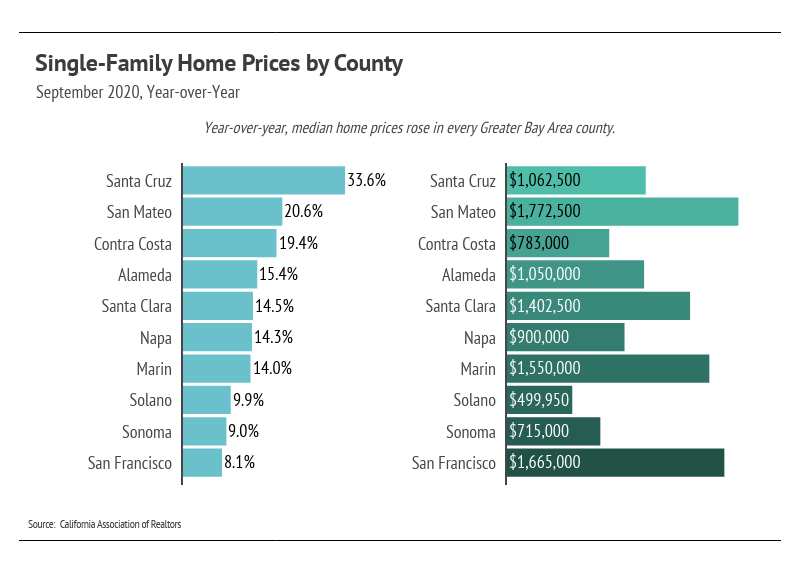

Year-over-year, median single-family home prices were up 20% in the Greater Bay Area.

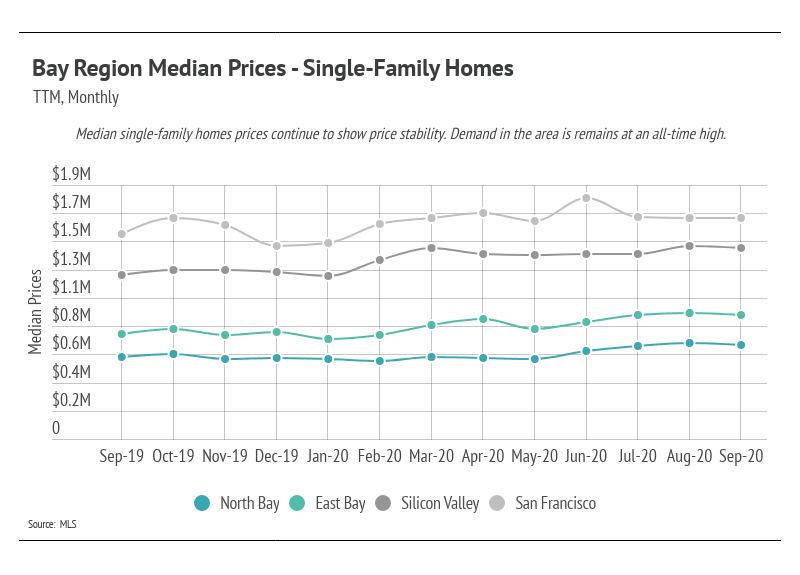

In this newsletter, we break down the Bay Area into four regions, as follows:

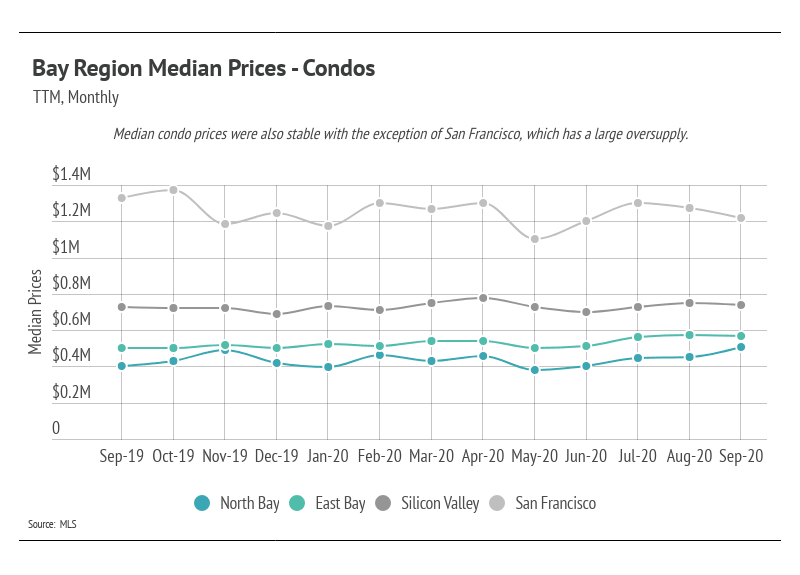

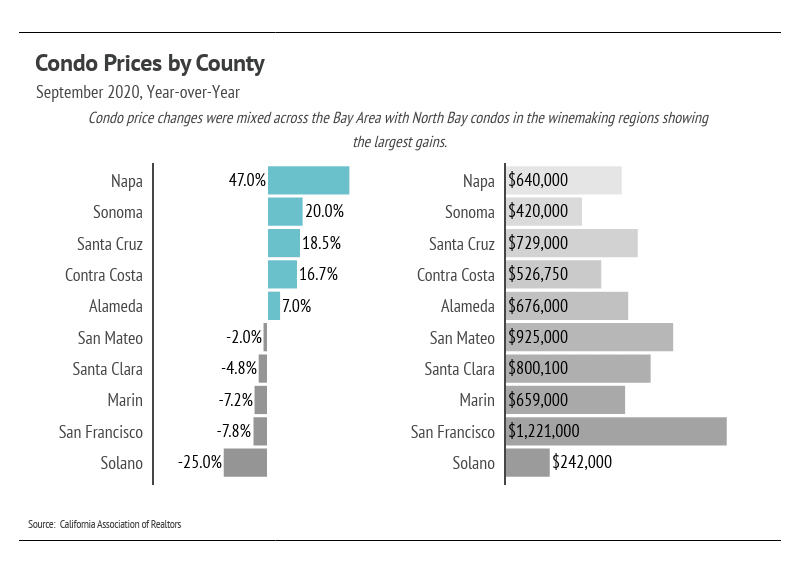

Median condo prices were mixed, but mostly showed positive gains. San Francisco condo prices continued to decline, as the market is still oversupplied.

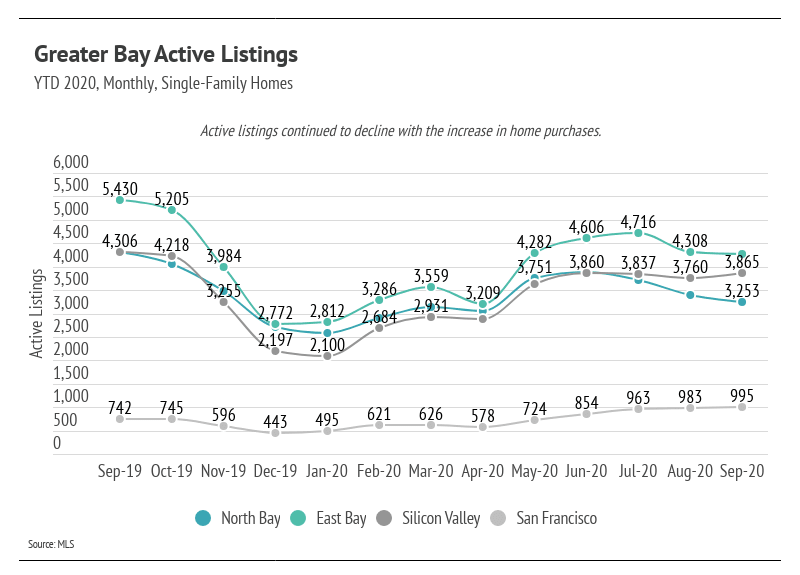

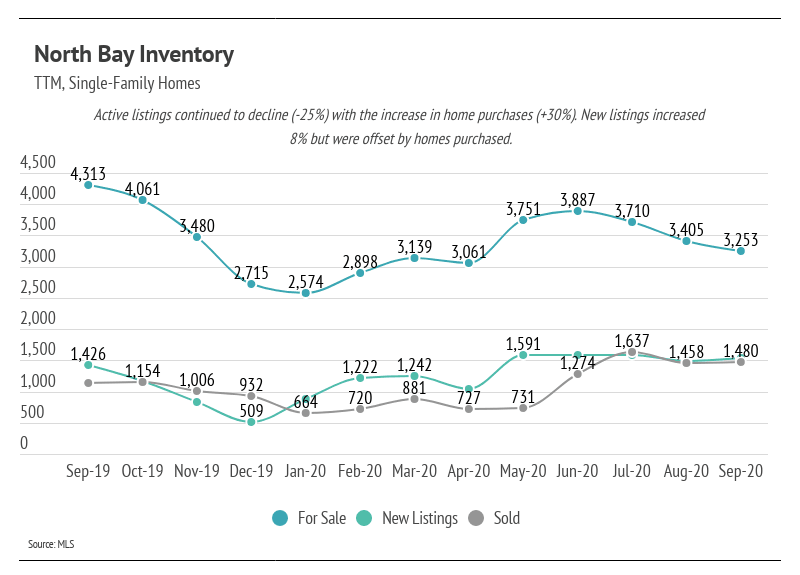

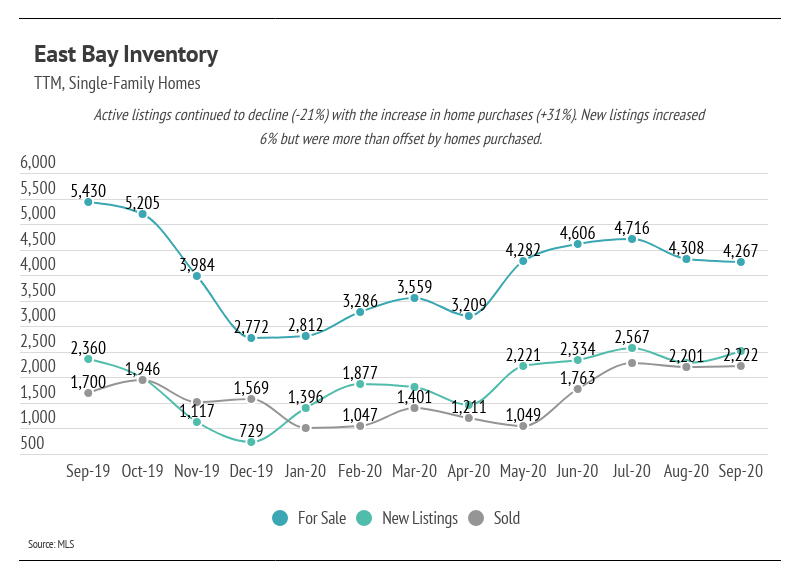

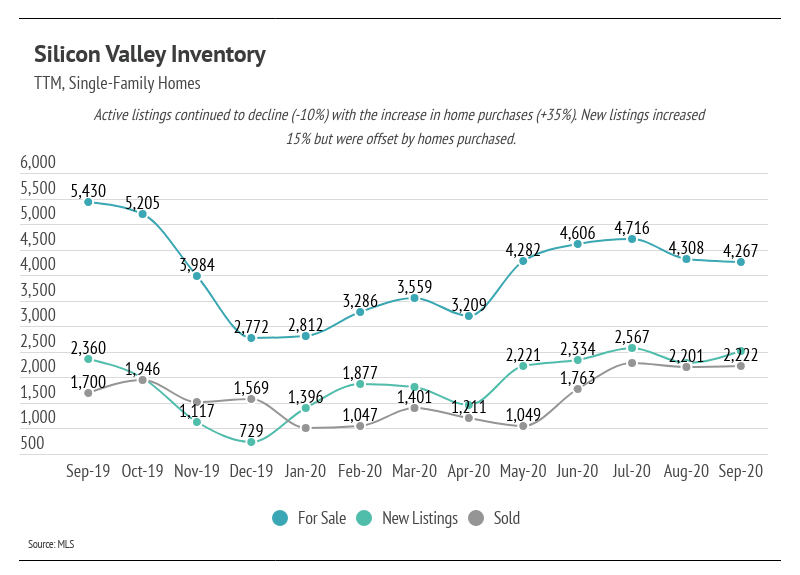

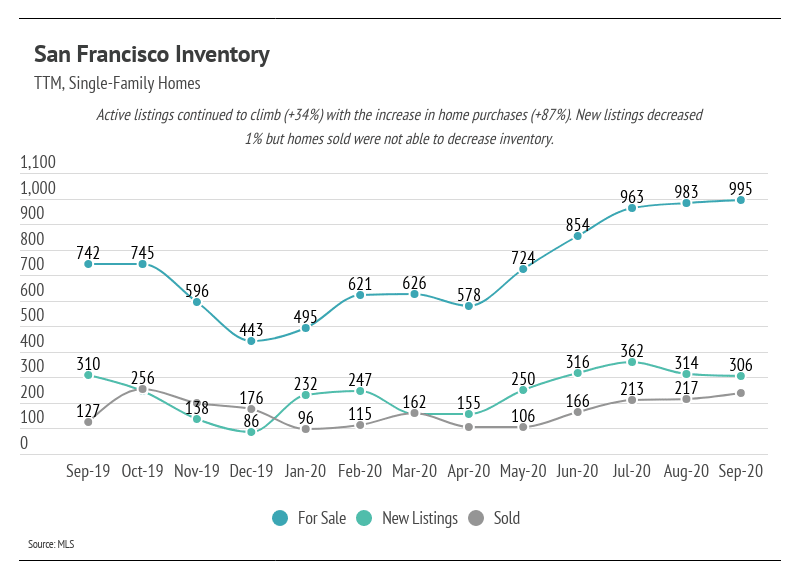

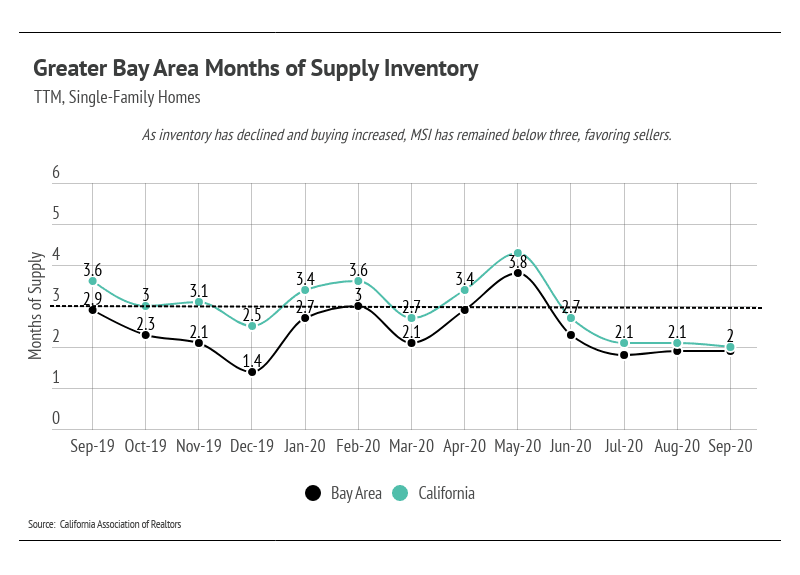

Total inventory continued to decline as the number of sold homes rose, far outpacing the new listings that came to market. Like the rest of the country, demand is outpacing new supply, which buoys Bay Area home prices. Single-family home inventory is noticeably lower, and is likely to decline as we make our way into the winter months. San Francisco is the only area that inventory is increasing despite higher sales.

Single-family home sales have climbed since the initial months of the pandemic (March through May). Generally, buyers and sellers left the market in April and May, causing pent-up demand. Sales increased and are still near the highest level this year for single-family homes. Usually, we expect sales to decline in the autumn and winter months, but this year’s summer selling season was delayed and seems to be spilling into autumn. All markets except for San Francisco have trended fairly similarly, with inventory declining due to more demand than supply. San Francisco is still seeing a large number of sellers that haven’t been fully offset by home purchases.

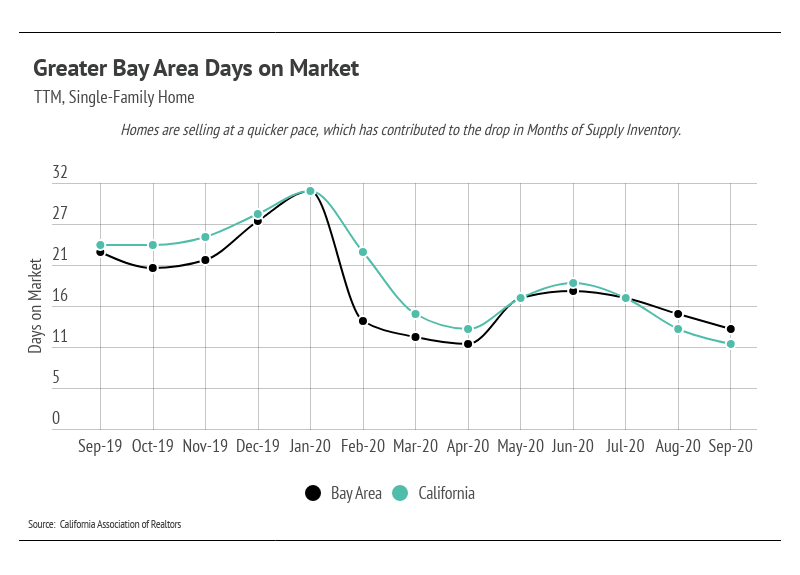

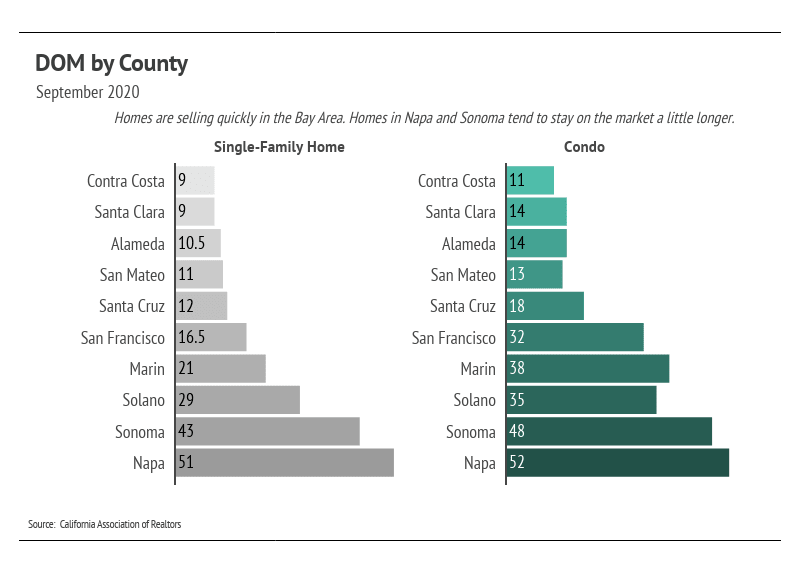

The Days on Market (DOM) is lower year-over-year. Months of Supply Inventory has continued to stay low because of the inventory decline and faster pace of sales.

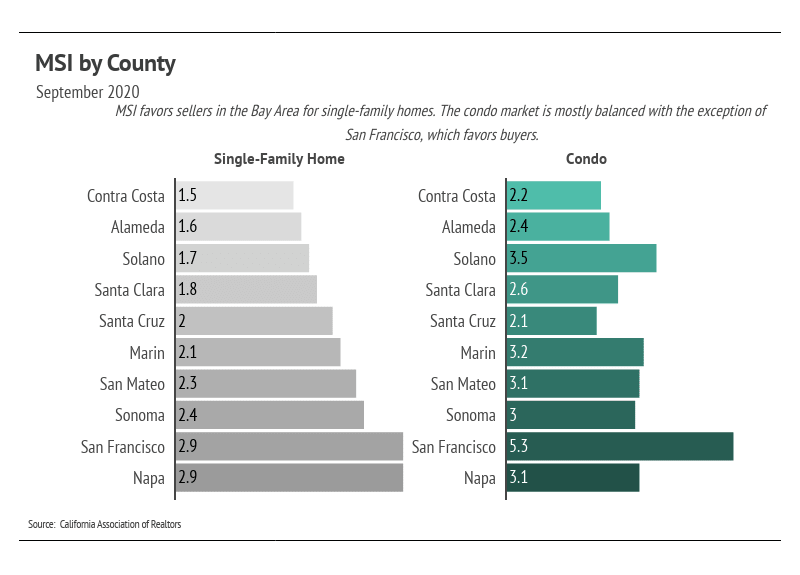

We can use Months of Supply Inventory (MSI) as a metric to judge whether the market favors buyers or sellers. The average MSI is three months in California, which indicates a balanced market. An MSI lower than three means that buyers dominate the market and there are relatively few sellers (i.e., it’s a sellers’ market), while a higher MSI means there are more sellers than buyers (i.e., it’s a buyers’ market). The MSI remained at 1.9 for single-family homes, favoring sellers.

In summary, the high demand in the Greater Bay Area has sustained home prices. Inventory for single-family homes will likely decline further as we enter the winter months with fewer sellers coming to market, potentially lifting prices higher. Overall, the housing market has shown its resilience through the pandemic and remains one of the safest asset classes. Economic indicators are in an anomalous state, meaning that they are out of trend with each other. The data show that housing has remained consistently strong through this period.

We anticipate new listings to slow through the holiday months. Condo prices outside San Francisco will likely remain stable with no outsized gains or losses through the winter months. For San Francisco, the median condo price will likely continue to decline. The autumn/winter season tends to see a slowdown in activity, although we may see a new trend this year with higher-than-normal sales.

As always, we remain committed to helping our clients achieve their current and future real estate goals. Our team of experienced professionals are happy to discuss the information we have shared in this newsletter. We welcome you to contact us with any questions about the current market or to request an evaluation of your home or condo.

Stay up to date on the latest real estate trends.

And what to check before upgrading your internet plan

HAYLEN, an Asian-owned, people-first real estate firm, selected to steward real estate process for J-Sei Home’s next chapter

You’ve got questions and we can’t wait to answer them.