Will Bay Area Housing Price Go Down Further?

Will Bay Area housing prices drop further? Let's look at the numbers and the macro economics to find out. You can find the video recording of this episode here.

Let's take a look at the Consumer Price Index first. You guys probably start hearing a lot of the news or seeing all these headlines the last couple of days. A consumer price index ticked up a little bit, it went to 6.4% and the core index is actually at 5.6% is slightly higher than what they were expecting, but then it just didn't come down as fast, although the Fed actually thought that the inflation probably can't ease a little bit faster even though they are still going to increase rate, but it will be probably going slower so then it's easing some recession risk.

And if you look at here from USA Today, Gregory Daco, Chief Economist at Ernst and Young, said that the rise in the core consumer price index last month isn't "cause for concern" since the big jump and shelter prices could mean there will be smaller increases in coming months. And Daco predicts that annual inflation will fall to 2.3% by the end of the year which is pretty much where the Fed is trying to aim for and the core inflation, he predicts, will fall to 2.8% by then. So, definitely, if we are going to hit that by the end of the year we're probably going to start seeing a lot more improvements in 2024.

Now, the 10-year treasury yield last month when we reported to you, it tumbled below 3.44%, but now this one came back up because of the inflation data. So, went from 3.44 last month and now came back up to 3.81 and when the 10-year treasury bills go up, then that means the interest rate goes up.

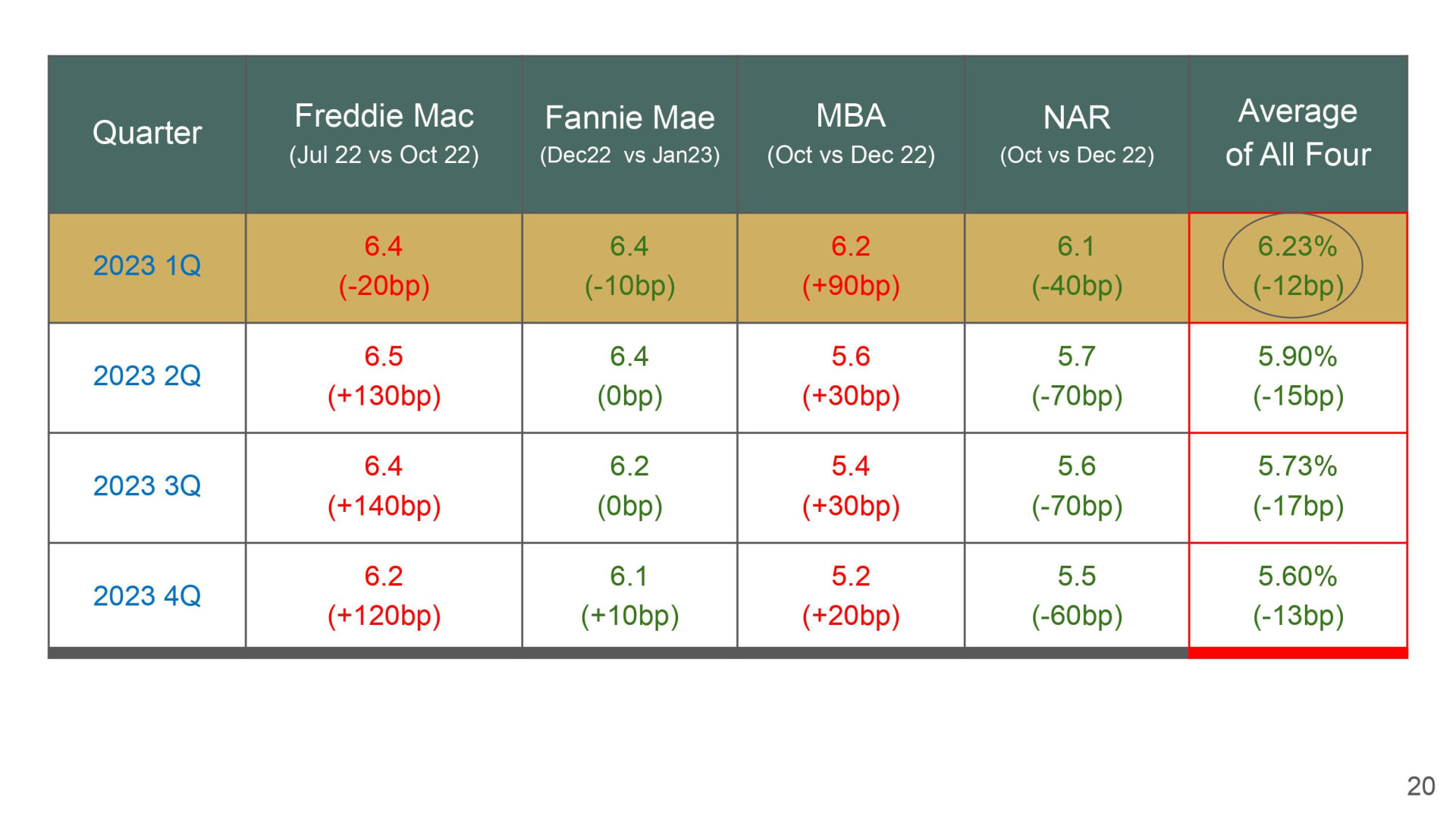

So, we're going to take a look at what's going on and what these agencies think that the rates are going to move towards. Now the only thing changed on this chart compared to last month is just a Fannie Mae one because everyone else didn't really update their numbers yet. So, they are still the same as last month. It's just that I'm still having these numbers in the parentheses to show you what they have changed from their last projections. Freddie Mac had projected a much higher number in July 2022 versus October 2022 so they believe that 1Q 2023 now is at 6.4% which is in line with what Fannie Mae is projecting and the Mortgage Bank Association is about 6.2 and the National Association of Realtors is at 6.14 1Q 2023. So, the average of all four is about 6.23%. Now, if you look at 2Q, Freddie Mac is projecting a 6.5%, Fannie Mae at 6.4%, Mortgage Bank Association of 5.6%, and National Association Realtors at 5.7%, so the average of all four has gone below 6%. So, if you start seeing this actually you notice that basically, they believe that the mortgage rate is going to peak by the end of 1Q 2023, and it's going to start to come down starting 2Q 2023. I think this is very, very important to know because the fact that as you know buyers are very sensitive with their mortgage rates. So, definitely, you're probably going to start seeing a lot more activity starting 2Q 2023. And I want you guys to pay attention to this number here a little bit 6.23% which is 1Q 2023, because I want to show you these historical mortgage rates provided by Victor Chow at Wells Fargo.

If we look at the mortgage rate for January 2023, they have recorded at 6.27% and by the way, I just wanted to clarify one thing is that these rates are based on conforming rate not the Jumbo rates. So, this is 6.27%. If you have Jumbo loan, you probably know that you're not getting a rate as high as 6.27, you're probably in the 5s range.

So, this is pretty much in line with what the agencies have been projecting, but I wanted you to take a look at that the numbers actually came down from October. In October, it peaked at 6.9%, and it just started to come down to 6.27%. On top of that if you compare to last time which is around 6.3% was in 2007. So, since 2007, the mortgage rate has been below 6.34%, I guess like the one before was 6.4, it was 2006 and then from 2003 to 2005 that was kind of like the peak of the housing market at that time it was going up and that was around like 5.8% or so. And then the last time, it was at about 6.3 was in 2007.

Since then, it's been below 6%, and, of course, the lowest ever was in 2021 which was at 2.96% and a lot of people who bought around this time frame they are definitely not thinking about selling because they were able to hold on to. Well, actually not just people who bought, people who refinanced around this time frame, they're just holding on to their houses with such low mortgage rates.

I'm one of those people who had refinanced during that time and our mortgage payments have come down so much that we are not even going to be thinking about selling at all because we just want to hold on to that low monthly payments.

What's going on with the Jumbo rate? Because our area a lot of the mortgages low balance rate, they are all Jumbo rates. So, this is about 5% for 30 years fixed and this was last month and in this month, it has gone up about 50 basis points at 5.5%, as we mentioned earlier the 10-year treasury bill has come back up, so it actually went down last month and it came back up to 5.5%.

I just want to share with you guys a little bit of what's going on if you compare it to the pricing in April 2022 which was the peak. This is the Santa Clara County peak pricing at 1.95%. If you had paid a 20% down payment with a mortgage balance at 1.56, your mortgage payment is actually at $7,561 when the 30-year rate at the time was about 4.125%. As the pricing has come down, now the median sales price is about $1.5 million, the down payment at $300,000 with a mortgage balance of 1.2, your mortgage payment now even at 5.5 is $6813.

What happens, just saying, if in the future, let's say, the 30 years mortgage rate comes down to 4.5% and you see that as a good opportunity to refinance and at that point when you refinance then your mortgage payment can come down to about $6,080 which is way, way cheaper obviously compared to what you have bought, if you have bought in April 2022.

I just want to show you this chart. I know some people were wondering if they should go into the market right now or not. I do think that the pricing probably not going to come down that much more in the future because the interest rate was so high before that a lot of people just took a pause, literally they're not coming out to look at properties, but right now, we started seeing some activities. So, if you're thinking about long-term, like living in your property, this is where you want to start a family, I think this is a really good time for you to consider buying a property right now.

The biggest question is also Bay Area Housing Market are we going to crash any further? We see Goldman Sachs just came up with this, my friends shared this article with me talking about San Jose is going to be one of the four cities which is going to have this housing crash just like 2008.

I think this had already happened, home prices they were talking about like it can be declining more than 25% as you saw earlier, the pricing coming from the peak has already come down about 25 to 30% or so for a lot of counties. So, we definitely have seen that drop already since last year.

In terms of like the tech layoffs, I know this is also a big, big topic with a lot of our clients right now talking about tech layoffs, it sounds extremely really scary. I know a lot of clients just not sure if they're going to have their job, so they want to take a pause.

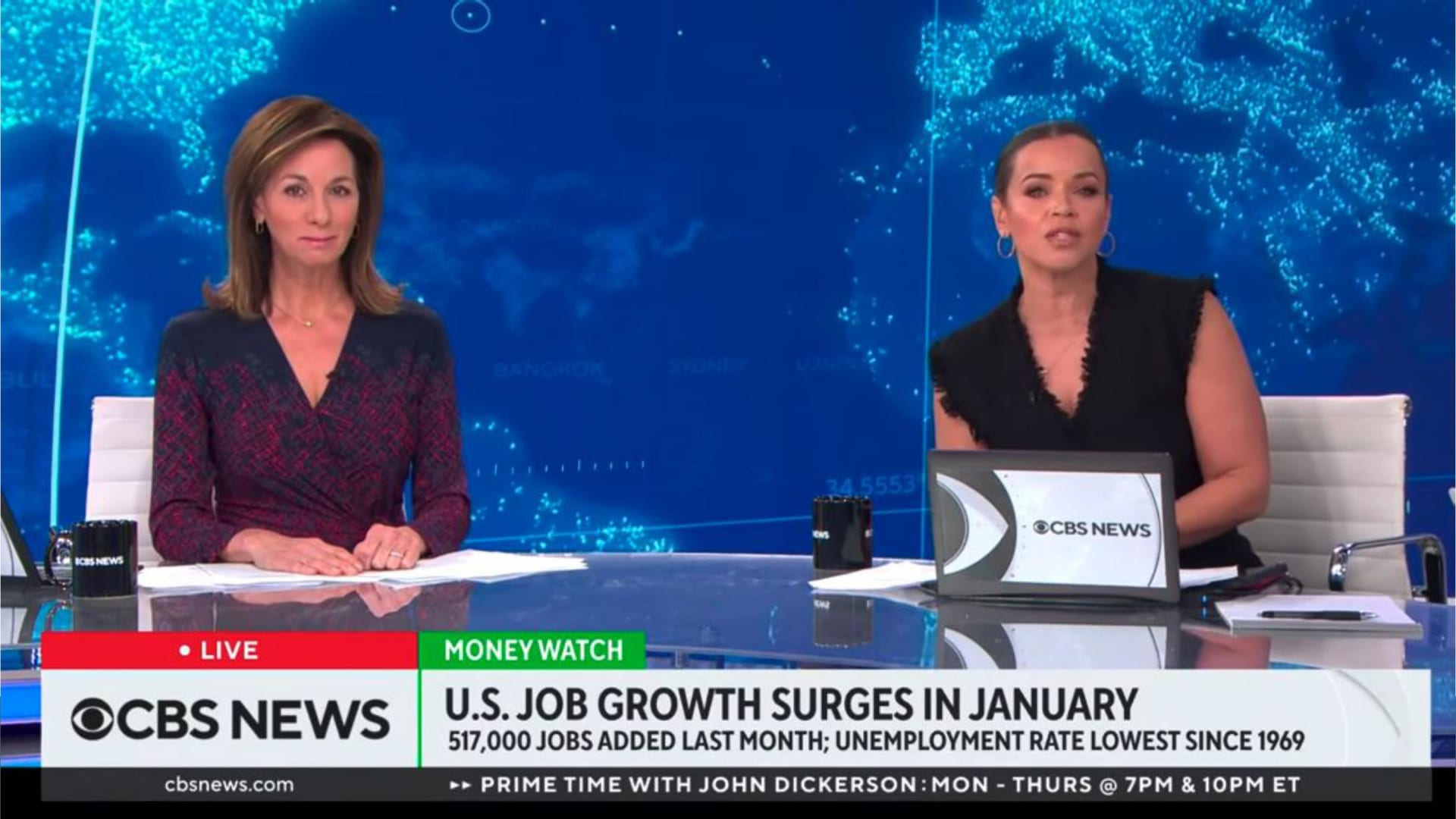

But, at the same time, on the other hand, we have this other news talking about like we just added 517,000 jobs which is way more than what they have expected and the unemployment rate is the lowest since 1969. It's like what is going on? So, it's very confusing I know. And that's why they started saying that well a lot of these tech people are being laid off. But at the same time, they're just so many opportunities out there and may not necessarily be all in the Bay area, it could be somewhere else, but at the same time hopefully, I'm just providing some comfort to those people who are really worried about their future. There is nothing to do with whether you should buy a home here or not. But the idea is that if you are worrying about layoffs at least hopefully this shows you, there is still a lot of other opportunities out there, they are still need your talent on the market.

The great statistic here is that 42% of those people who got laid off actually found a higher-paying job. There you go! May not be here, maybe somewhere else, I don't know it could be here but there are actually a lot more smaller company or government jobs that really need more Tech workers. So, I wish everybody the best of luck in finding a new job if you got laid off. But I do believe that this is still a piece of very good news, even if you get laid off you might be able to find another much better job anyways.

We know that our inventory has been super tight and in multi-family housing, we need them to be built and so Lawrence Yun who is the Chief Economist for the National Association of Realtors has said that "because there isn't really a lot of listings of homes for sale and mortgage rate dips in future months, buyers will return. But without the supply, another revival of multiple biddings could occur again."

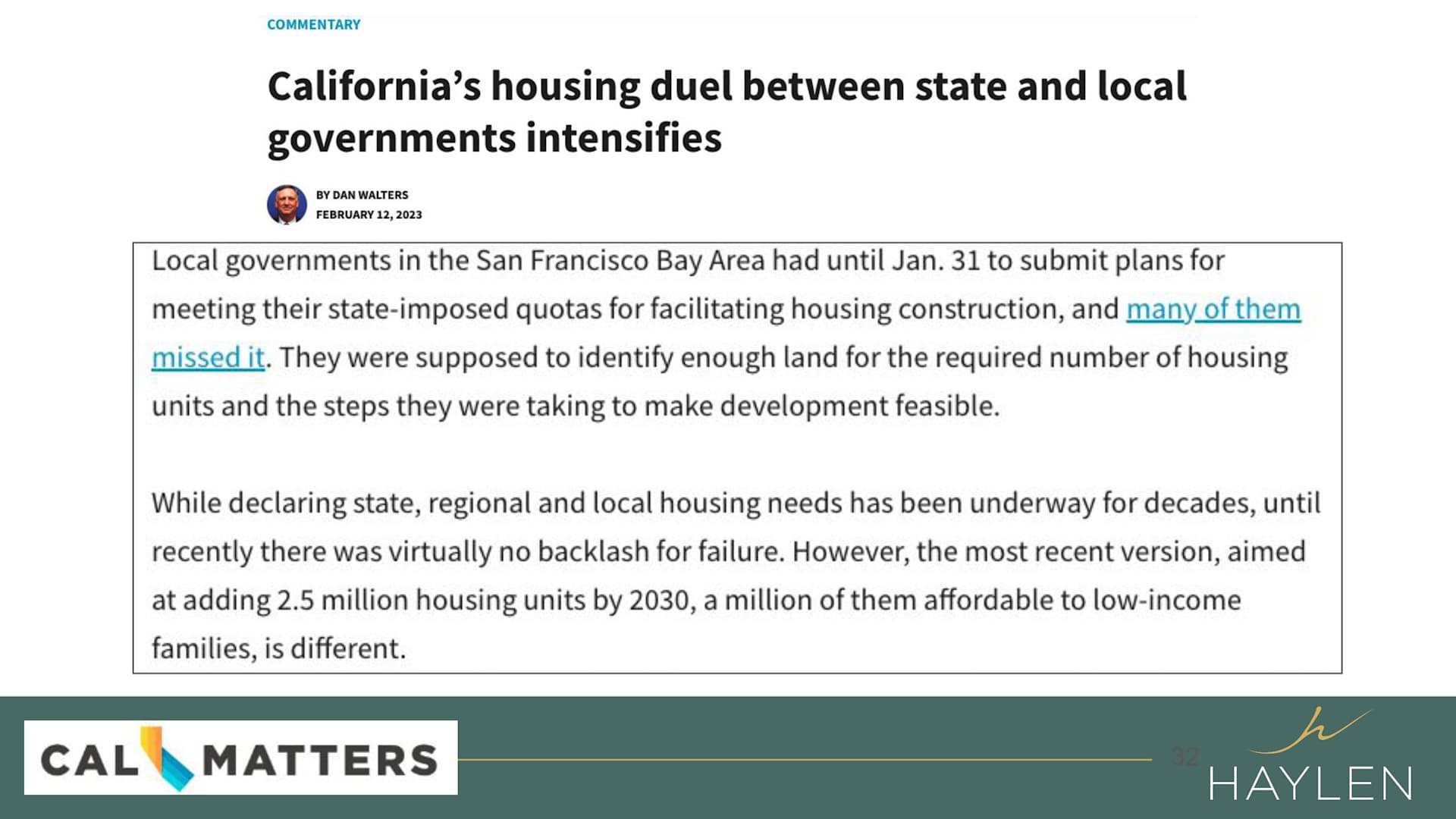

So, this is really important to know and then you will see that there's so many conversations right now about building and building and then the Bay Area’s we're pushing to build 441,000 new homes by 2031 and that's only eight years away. Can we do that? The state officials have been pushing all these cities and counties to really meet these kinds of home-building goals and then two weeks ago, it's been like a very stressful time for a lot of these cities because they need to be able to submit their proposal on how they're going to be able to add housings in their respective cities?

The bulk of the new homes are set for the region's population centers near jobs and transportation, including San Jose, Oakland, and San Francisco. But suburban and rural areas also must plan for more housing.

So, how many homes did the Bay Area actually build in the last housing cycle? It is between 2015 and 2023, the Bay Area had permitted meaning, not built yet, permitted, about 190,000 units, but they only approved 44,000 homes for low or middle-income residents which is well under half the combined target for those groups. So, we are still very, very short on housing for people. So, we definitely need to do everything possible to actually encourage or help our builders to build more in our area.

Unfortunately, there are some areas because they're ultra-wealthy areas for example, Los Altos Hills, they are all single family, so they really did not like the idea of building high-density housing complexes in their area. I'm not saying this is not right or wrong, honestly, I can understand why? You're paying so much money for that type of environment. They just want to have their own privacy. But at the same time, these towns they are also being requested and also demanded by the state to have these housing plans and increasing housing units in the area, so it's been a really tough topic to talk about.

Continuously, you're going to see a lot of news that talk about how the cities and counties they are in those senses, I don't want to say fighting, but at the same time, the state are really pushing down very hard for them to build, to have a plan so that we can build more and increase housing, including San Francisco.

Now they're not allowing landlords to have their units vacant, if they have the units vacant they will imply this new tax on this vacant unit. And, hence now landlords are suing over this new tax on vacant housing units and it is going to be really difficult for a lot of landlords, but the purpose of this is really trying to make sure that they are filling these units for people to live in.

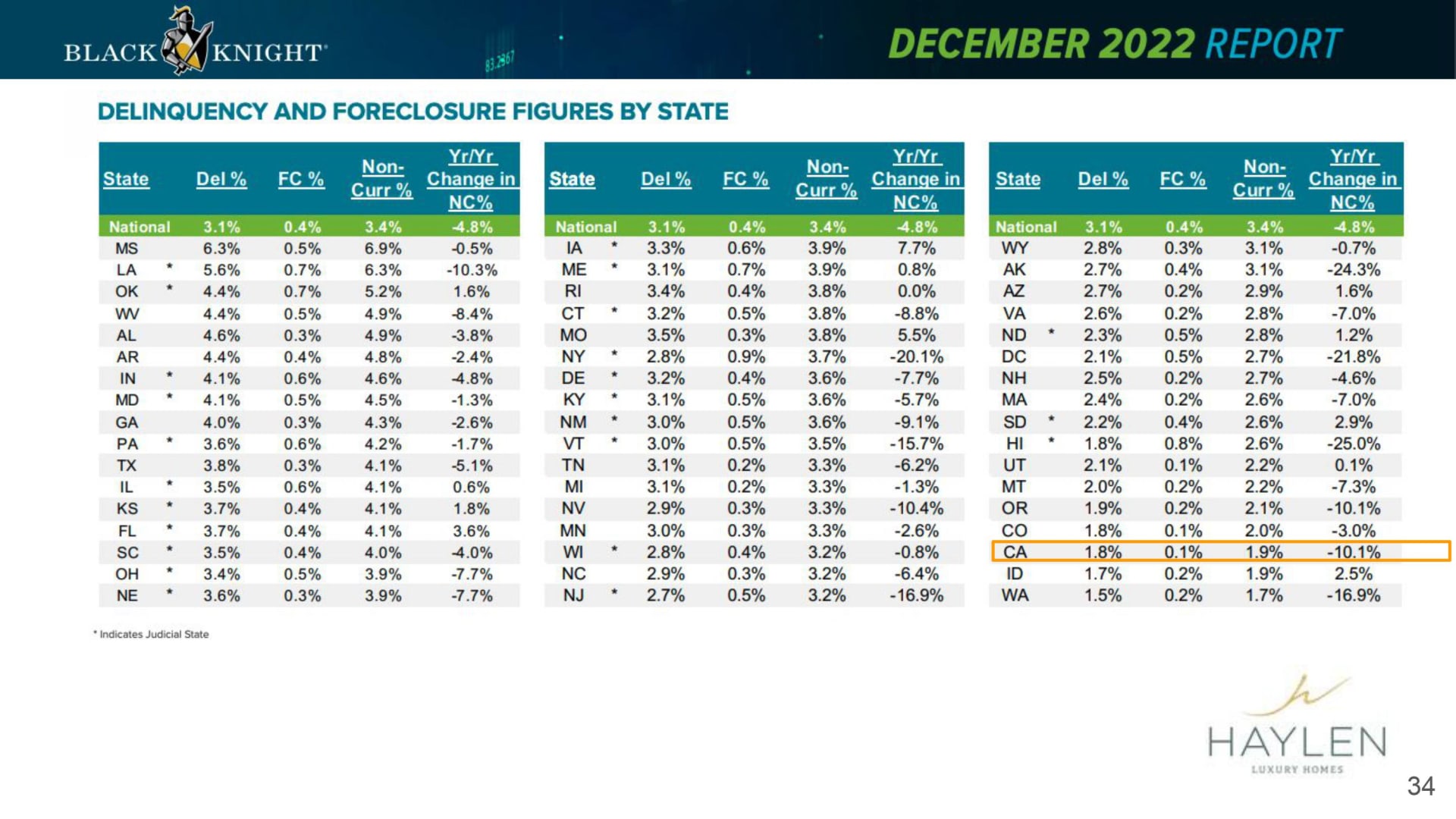

If you're worried about foreclosures as you see California, we're all the way at the bottom ranking. We have a delinquency percentage of 1.8% and then the year-over-year change in non-current percentage is actually down by 10%.

This chart shows that in November 2022, we have about 1.8 million non-current filings, but still if you look at the numbers we are pretty much in line and it's still lower than what we had back in, let's say, right before COVID which is 2019 is at 2.2 million. So, I think so far because of the pricing has gone up so much there's so much Equity that if somebody is really not current on their loans, they would much rather just sell it without going into foreclosure.

Stay up to date on the latest real estate trends.

A Bay Area Realtor's approach to schools, neighborhoods, and long-term value for families making a move

Part 1 of HAYLEN's series on the 2026 CCIM Spring Forum in Philadelphia

You’ve got questions and we can’t wait to answer them.